UNIT 4

Hire – purchase and installment purchase system

If you purchase a TV for cash, you pay, say, Rs.15,000. But if you wish to make the payment by installments of say, Rs.3,000 each, every year, you may be required to pay four installments, that is Rs.20,000 in all. The extra amount of Rs.3,000 is for interest. If you choose the latter mode of the payment, you should debit Rs.5,000 to interest and treat the TV as valued at Rs.15,000 (and not at Rs.20,000). In case payment is to be made by installments, there may be two kinds of arrangements. Each installment may be treated as a ‘hire’ the purchaser becoming the owner only if he pays all the instalments. In other words, property does not pass to him even if one installment remains unpaid. The seller will have the right to take away the goods in case of default in respect of any installment. This is known as ‘Hire Purchase ‘system.

According to J.R. Batliboi, ‘‘Under the Hire Purchase System, goods are delivered to a person, so agrees to pay the owners by equal periodical instalments, such instalments to be treated as hire of those goods, until a certain fixed amount has been paid, when these goods become the property of the hirer.

Important Terms in Hire Purchases system

Hire purchase price=Cash price + Interest

5. Interest-Interest is the amount which is payable in addition to the actual cash price of the goods. It is the amount paid by the buyer for the delayed and postponed payment.

6. Hire Installment-It is the amount payable periodically by the hirer or the buyer, installment may be an equal amount or different amounts which are based on the agreement.

7. Down Payment or initial amount-The amount is a lump-sum out of the total Hire purchase price, payable to the vendor in advance while the agreement is signed, which does not carry any interest on it.

Features of hire purchase system

Installment purchase system:

It is a system where the buyer is given the ownership as well as the possession of the goods at the same time of signing the contract. The buyer has the facility to pay the price in installment.

According to J.B Batliboi, installment purchase system is a system under there is an agreement to purchase and pay by installment, the goods which become the property of the purchaser immediately when he receives the delivery of the same.

Features of installment purchase system:

Calculation of interest:

Interest: In either case (hire purchase or instalment) interest must be separated from the principal sum due. Since payments continue over two or more financial year’s interest must be calculated for each year separately. Usually information is available regarding cash price and the rate of interest. Calculation of interest then becomes easy. Just prepare the account of one of the parties on ordinary lines and charge interest on the balance due. Suppose on 1st January, 2000 A purchases from B machinery whose cash price is Rs.15,000; Rs.5,000 is to be paid down, that is on signing of the contract, and Rs.4,000 is to be paid at the end of each year for 3 years. Rate of interest is 10% p.a. If we prepare B’s account (on a memorandum basis) in A’s books, we shall know the interest for each year.

A’s Books

Dr. |

|

| B’s Account |

| Cr. |

|

| Rs. |

|

| Rs. |

2000 |

|

| 2000 |

|

|

Jan.1 | To Cash | 5,000 | Jan.1 | By Machinery A/c | 15,000 |

Dec.31 | To Cash | 4,000 | Dec.31 | By Interest A/c | 1,000 |

’’ | To balance c/d | 7,000 |

| (10% on Rs.10,000) |

|

|

| 16,000 |

|

| 16,000 |

2001 |

|

| 2001 |

|

|

Dec.31 | To Cash | 4,000 | Jan.1 | By Balance b/d | 7,000 |

| To Balance c/d | 3,700 | Dec.31 | By Interest A/c |

|

|

|

|

| (10% on Rs.7,000) | 700 |

|

| 7,700 |

|

| 7,700 |

2002 |

|

| 2002 |

|

|

Dec.31 | To Cash | 4,000 | Jan.1 | By Balance b/d | 3,700 |

|

|

| Dec.31 | By Interest A/c* | 300 |

|

| 4,000 |

|

| 4,000 |

* As it is the last year of installment, interest amount will be the difference between the Outstanding balance and the actual amount of installment. [Students should note that if you calculate interest for the last year as per the given percentage on the O/S amount (3700 x 10%=370), total amount payable becomes (3700+370=4070) which is greater than the installment paid. So there will be again Rs. 70 payable even after the last installment being paid.]

If the rate of interest is not given, the interest for each year will be in proportion to amount outstanding in each year. In the example given above, the total sum payable is Rs.17,000 out of which Rs.5,000 is paid immediately. This leaves Rs.12,000 as outstanding throughout the first year at the end of which Rs.4,000 is paid. In the second year Rs.8,000 is outstanding and in the third year Rs.4,000 is due. The total interest is Rs.2,000. i.e., Rs.17,000. minus Rs.15,000. The interest should be apportioned over the 3 years in the ratio of amounts outstanding, that Rs.12,000; Rs.8,000 and Rs.4,000 or in the ratio of 3 : 2 :1. The interest for the first year is Rs.1,000 : for the second year it is Rs.670 and for the third year it is Rs.333. Note that the amount cannot be the same as worked out when the rate of interest isgiven.

To ascertain Cash Price, rate of interest and instalments being given. Sometimes the cash price is not given. Since the asset cannot be debited with more than the cash price, it must be ascertained. The process is to take the last year first and separate interest from principal out of the total sum due. In the example given above, Rs.4,000 is due at the end of 2002. The rate of interest is 10%. If in the beginning of 2001 Rs.100 was due, Rs.10 would be added making Rs.110 as due at the end of 2002. Thus, out of the sum due at the end of the year, one-eleventh is interest; rest is principal. We can proceed year by year like this.

Thus: —

| Rs. |

Amount due on 31-12-2001 | 4,000 |

Interest @ 1/11 | 364 |

Amount due on 1-1-2002 or 31-12-2001 | 3,636 |

Paid on 31-12-2001 | 4,000 |

Total amount due on 31-12-2001 | 7,636 |

Interest @ 1/11 | 694 |

Amount due on 1-1-96 or 31-12-2000 | 6,942 |

Paid on 31-12-2000 | 4,000 |

Total amount due on 31-12-2000 | 10,942 |

Interest @ 1/11 | 995 |

Amount due on 1-1-2000 | 9,947 |

Paid Cash down on 1-1-2000 | 5,000 |

Cash Price | 14,947 |

The interest for three years is Rs.995, Rs.694 and Rs.364 respectively. | |

Key takeaways:

Hire purchase agreement is a credit agreement. While buying expensive goods hire purchase agreement is made. During the purchase the consumer makes a down payment and the balance outstanding will be paid in instalments with an interest charge.

The ownership in hire purchase is not transferred to the purchaser until all payments are made. Hire purchase is similar to rent to own concept. The lessee pays the rent over a period of time for the property or a vehicle. If the actual price of the property is paid by the lessee than he will have the option to own the property or vehicle at any time.

Merits of hire purchase-

Demerits of hire purchase-

Legal provision regarding hire – purchase contract:

The Hire-Purchase Act came into being on 1st Sept. 1972.

According to the Act, a hire-purchase agreement means an agreement under which goods are let on hire and under which the hirer has an option to purchase them in accordance with the terms of the agreement and includes an agreement under which:

Hire-purchase agreement must be in writing and signed by parties. A surety, if any, must sign the hire-purchase agreements. The agreement shall be void if the above requirements have not been complied with — Sec. 3.

According to Sec. 4 contents of hire-purchase agreement includes:

Key takeaways –

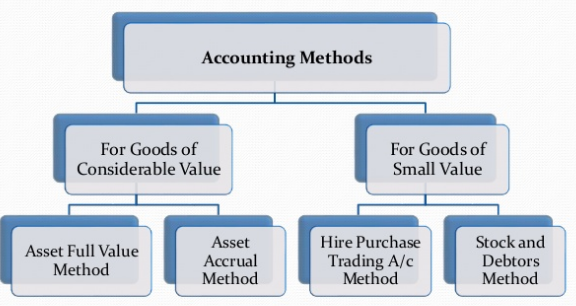

For such high value goods, two methods of records can be maintained.

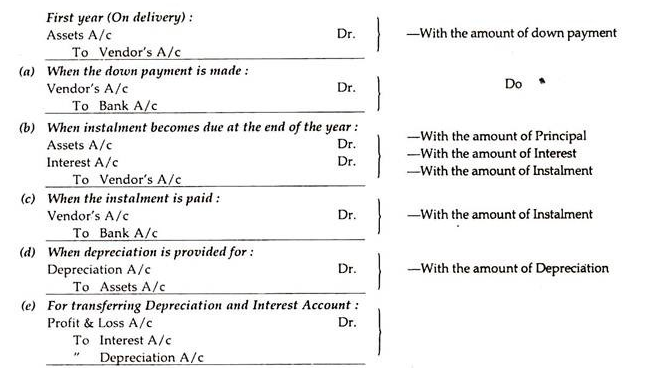

First method - Capitalising only the portion of cash price paid or asset accrual method.

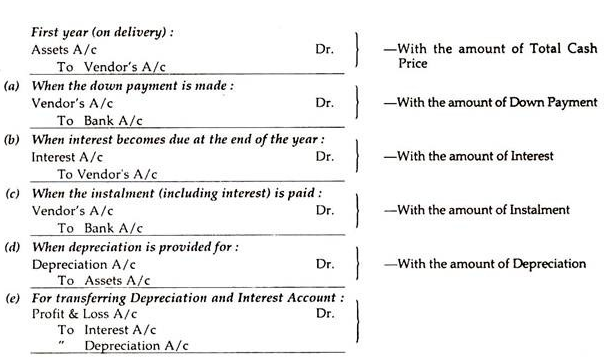

Second method - Capitalising the full cash price or credit purchase with interest method.

In this method cash price paid is alone capitalized. The asset account is debited with the amount of cash price paid in that instalment. This method as use that the title pages two the buyer only after the last instalment is paid. Unit then the seller is the owner. So as and when the instalment amount is paid the case price in the instalment is capitalized. In this method the goods are consider to the acquired only gradually when the cash price is paid each time.

In the subsequent years (b), (c), (d) and (e) with their respective amounts will appear in the books.

2. Credit purchase with interest:

In this method the full case price is capitalised. The hire purchaser debits the Asset account A/c with full case price and credits the higher vendor A/c. this method assumes that the assets are consider to be acquired immediately when the position is taken. The purchaser enters into an agreement with the intention of fulfilling it.

Journal entry in the books of hire purchase

In the subsequent years (b), (c), (d) and (e) with their respective amounts will appear in the books.

Journal entry in the books of hire vendor

In the subsequent years (c), (d) and (e) with their respective amounts will appear in the books.

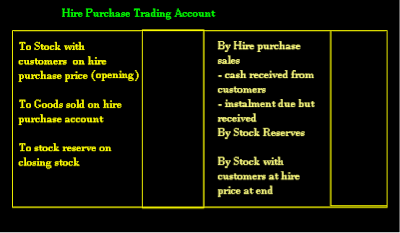

Accounting records for goods of small values-

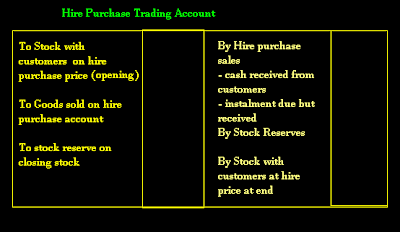

2. Stock and debtor method

In this method, hire purchase stock, hire purchase debtor and hire purchase adjustment account are maintained. Following entries will pass in the books of vendor

a) When goods are sold on hire purchase

hire purchase stock account Dr. ( Hire purchase price)

stock account Cr. ( Actual cost of sale of goods )

hire purchase adjustment account Cr. ( difference between hire purchase price and actual cost )

b)When installments become due for payment

hire purchase debtors account Dr.

hire purchase stock account Cr.

c) When cash is received

Cash account Dr.

Hire purchase debtor account Cr.

d) stock reserve account on opening stock

stock reserve account Dr.

hire purchase adjustment account Cr.

e) Stock reserve on closing stock

Hire purchase adjustment account Dr.

Stock reserve account Cr.

Key takeaways-

Accounting method for high value goods-

Installment purchase system where an agreement to purchase and sale is made between the buyer and the seller, here there is an immediate sale on signing the agreement. In actual purchase the price of the goods is paid in lump-sum, but in instalment system instead of paying in a lumpsum, it is spread over a period, interest is being paid on the unpaid balance. This interest amount is determined at the time of signing the agreement itself. The possession of the goods is taken by the buyer after signing the contract itself. The basic difference between instalment system and hire purchase system is the transfer of ownership. In instalment system the title or the ownership is immediately passed to the purchaser, but in the hire purchase system until the entire amount to the last instalment is paid the ownership with the vendor. In case the purchaser makes default of any payment, the seller has no right to repossess like in the hire purchase system, but he can recover the amount due to him by filing a suit in the court of law and can recover the unpaid amount since the buyer is the legal owner of the goods he has every right to sell, transfer, exchange or even destroy it.

Basis of difference | Hire-purchase system | Instalment purchase system |

Operation | This system operates on the basis of hire-purchase agreement. | This system operates on the basis of instalment purchase agreement. |

Nature of agreement | This system is based on a agreement of hiring. | This system is based on agreement of sale. |

Statutory governance | This is governed by the hire-purchase Act, 1972. | This is governed by the sale of goods Act, 1930. |

Parties in agreement | The parties entered into agreement, under this system are called hire and hire-vendor. | The parties concerned are called buyer and seller. |

Ownership rights | The ownership passes onto the purchase only on last payment of instalment. | The ownership passes immediately after signing the agreement, although the price of goods will be paid in instalment. |

Return of goods | The purchaser may return goods. | The buyer cannot return goods unless and until sells defaults. |

Repossession | If the higher makes default in instalment payment, the vendor can take back goods from hirer. | Even if there is any default in instalment payment, the seller cannot take back from buyer. |

Risk of loss | Risk of loss of goods lie with vendor. | Risk of loss of goods lie with buyer. |

Right of disposal | Buyer cannot hire out, lease, mortgage, destroy, damage, or transfer of goods. | Buyer can have right to dispose goods purchased under this system. |

Position relating to instalment | The instalment paid is treated as hire charges for use of goods. | Instalment paid is treated as part redemption of value of goods. |

Charges other than cash price | Component other than cash price included in instalment is called ‘Hire Charges.’ | Under this system, it is called ‘interest’. |

After sales service:

Generally , the vendor provide free after sales service for a specified period to the customers and an estimated cost is loaded on the price of the goods for such services. Since the amount is received by the vendor for this purpose in advance, a separate account is to be opened known as Maintenance Suspense Account, or Repairs Reserve Account or Service Charges Account.

This account is to be debited for the actual amount of expenses incurred for the purpose and the balance represents profit or loss. When such service contract is extended for more than one year, the total service charges are to be allocated against the different related years and each year’s actual expenses are to be compared with the actual amount so allocated for that year. If the actual amount of such charges is, however, less than the estimated amount, the excess to be carried forward until the period of maintenance is over. On the other hand, if there is any deficit means excess of actual amount over estimated figures that should be provided for.

Key takeaways-

REFERENCE

1. Gupta R.L. and Radhaswamy. M, Sultan chand & Sons, New Delhi.

2. Shukla M. C. Grewal T. S and Gupta S.C., S. Chand & Sons. New Delhi.

3. Shukla S. M., Sahitya Bhawan Publication, Agra.

4. Murti Guru Prasad, Himalaya Publishing House, Mumbai.

5. Jain and Narang, Kalyani Publisher, New Delhi.