Preface

Marginal costs aren't a costing method like costing jobs, batches, or contracts. It's actually a technology costing that only considers variable manufacturing costs when determining cost of products sold. It also can be wont to evaluate inventory. In fact, this system is predicated on the subsequent basic principles. The total costs are often divided into fixed and variable. Although total fixed costs remain constant in the least levels In production, variable costs still change counting on the extent of production. Will increase if there's production When production decreases, it increases and reduces incremental cost method helps supply Relevant information to assist management make decisions in several areas ahead folks .Allocate all manufacturing costs to the merchandise , whether the merchandise is fixed or variable. This approach is known as Absorption Costing / Total Costing. However, only variable costs are relevant to deciding .This is referred to as marginal / variable cost.

Marginal cost: The term incremental cost refers to the number at a specific production volume. If the assembly volume is modified by 1 unit, the entire cost are going to be charged. Therefore, it is Additional or additional cost of additional output units. Marginal costs show that there's certainly some change in production wherever there's a change. Changes in total cost it's associated with fluctuations in variable costs. Fixed costs are treated as a period it costs money and is transferred to the P & L account. This is a costing system that treats only fluctuating manufacturing costs as product costs. Fixed manufacturing overhead is taken into account period cost.

Simple steps to know the above theory:

Example: When a factory produces 1000 units at a complete cost of Rs.3,000 and increases production by one the cost goes up to Rs.3,002, and therefore the incremental cost of additional output is Rs.2. (3002-3000). If there are multiple output increases, dividing the entire rise by the entire output increase Shows the typical incremental cost per unit.

Example: The output has increased from 1000 units to 1020 units, and therefore the total cost to supply these units is Rs.1,045, average incremental cost per unit is Rs.2.25. (That is, additional cost / additional unit = 45/20 = Rs.2.25)

Assumption:

Marginal cost:

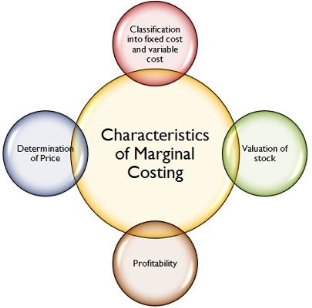

Marginal cost characteristics

(1) All elements of cost are classified into fixed costs and variable costs.

(2) Incremental cost may be a method of cost management and deciding.

(3) Variable costs are billed as manufacturing costs.

(4) Inventories of work-in-process and finished products are evaluated supported variable costs.

(5) Profit is calculated by subtracting fixed costs from contributions. In other words, it's the surplus of the asking price Marginal cost of sales.

(6) Profitability of varied levels of activity is decided by cost volume profit analysis.

Key takeaways:

Decision making involves choosing one course of action from the various viable options available. Many quantitative and qualitative aspects need to be taken into account in decision making. The manager chooses the course of action he considers most effective in achieving his goals, solve a problem. Decision making is an integral part of all management functions such as planning, organization, coordination and management. All decisions are futuristic in nature and involve management predicting what is likely to happen, but that is highly uncertain. The term "cost" has multiple nuances. The meaning is different in various situations. Cost calculators play a key role in decision making by scrutinizing each situation, deciding what type of cost concept to use, and making accurate and relevant data available to management “Will play. “

Decisions include two main types of decisions: long-term decisions and short-term decisions.

Short-term decisions are usually special in nature. The specificity of information for decision making depends on the specific circumstances that require the decision. Here, such information is referred to as "related data." Short-term decisions are affected almost within a year. Such short-term operational decisions can include many special, non-regular decisions, such as decisions and purchases. Sell or process; accept or reject orders and other decisions.

Due to long-term decisions, management needs to look beyond this year. The time value of money and the rate of return on investment are key considerations in the long run.

Determining the period. Uncertainty is an integral part of decision making. Therefore, the decision-making task is very difficult, important and important.

A business decision is the act of making a decision about something, a position, an opinion, or a judgment that will be reached after some consideration. Business decision-making is the process of choosing from several options, products, or ideas and taking action.

Decision-making steps:

It is appropriate here to describe some of the key important steps that help you make logical decisions.

1. Problem Definition and Clarification: The first step is to define the problem clearly and accurately for decision making so that the quantitative data associated with the solution can be determined. You need to identify possible alternative solutions to your problem. The more alternative solutions you consider, the more complex the problem can be. Then a suitable scanning device will help remove the unattractive choices.

2. Data collection and analysis: If the decision maker feels the need in this regard, he can ask for more information. In fact, many decisions are improvised by obtaining more information, and it is usually possible to obtain such information.

3. Problem analysis: Every option has its own strengths and weaknesses. Decision makers need to make decisions based on the strength of the problem. To determine the maximum net benefit, you need to observe the problem from different perspectives.

4. Confirm alternative actions: The decision maker identifies the course of alternative actions. Select possibilities by calculating different cost structures and revenues under each option

5. Evaluation of each option: There are two types of aspects.

6. Alternative Choices: After defining, collecting, analyzing, checking, and evaluating various alternatives, decision makers can choose alternatives and get started.

7. Evaluation of Results: After making a decision, the decision maker should ask for an evaluation of the results on a regular basis. This will help him correct his mistakes, correct his goals and make better predictions for the future. In this regard, many techniques are used for decision making as follows:

a) Marginal cost

b) Break-even point analysis

c) Difference cost analysis

Management decision-making issues:

Business decisions typically rely on three types of issues:

1. Crisis: Crisis problems are serious problems that require immediate attention.

2. Non-crisis: Non-crisis problems that need to be resolved

At the same time, it has the characteristics of crisis importance and immediacy.

3. Opportunity Issues: Opportunity issues are situations that, if appropriate measures are taken, are likely to bring significant benefits to the organization.

Key takeaways:

5.3 Marginal costing vs absorption costing

5.3 Marginal costing vs absorption costing

Absorption costing

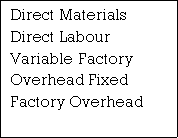

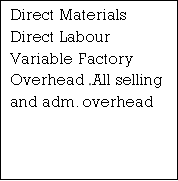

Absorption costing is also known as total costing or total costing or traditional costing. It's a technique of cost confirmation. With this method, both fixed and variable costs are charged to the product or process operation. Therefore, the cost of a product is determined by considering both fixed and variable costs.

Distinction between Absorption Costing and Marginal Costing

The distinction in these two techniques are illustrated by the following diagrams

The distinction in these two techniques are illustrated by the following diagrams

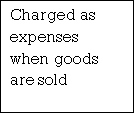

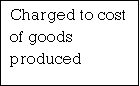

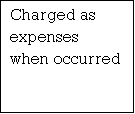

Fig. 1 Absorption Costing Approach

Fig.

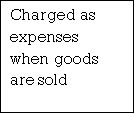

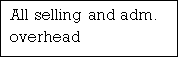

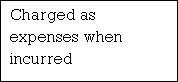

Fig. 2 Marginal Costing Approach

Application of marginal cost-

Marginal cost is a very useful cost calculation method and has great potential for management in various fields. Administrative tasks and decision-making processes. Regarding the application of marginal costs.

1) Cost Control: One of the key challenges facing management is managing costs. In today's competitive environment, rising selling prices to improve profit margins it is dangerous because it can lead to loss of market share. Another way to improve profits is to reduce costs. Cost management, Cost control aims to ensure that costs do not rise above current levels. Marginal cost techniques help with this task by separating variable and fixed costs. Fixed costs remain Variable costs vary depending on production, regardless of production. Certain fixed cost items cannot be managed at the middle or subordinate level. In these situations, it is advisable to focus on variable costs for cost control purposes. Since then separation of costs between fixed and variable costs is done at marginal costs and concentration. It is a variable cost rather than a fixed cost, which allows unnecessary efforts to manage the fixed cost.

2) Profit Planning: Another important use of marginal costs is in the area of profit planning. A plan, commonly known as a budget or operational plan, may be defined as a future plan. Operations to achieve defined profit targets. Marginal cost methods help generate the data you need For profit planning and decision making. For example, calculating profits when there is a change in Impact on profit if there is a change in product composition, selling price, change in profit if there is one of the products Decisions regarding changes in sales structure if there are discontinuances or new product introductions. Some of the areas of profit planning that can generate the information needed by the limits Cost for decision making. Therefore, the separation of fixed and variable costs is very convenient.

3) Key Factor Analysis: Management should consider the following when planning. When various resources are constrained. These constraints are limiting factors or the main budget factors described in the "Budget and Budget Management" topic. These important factors could be raw material availability, skilled worker availability, machine time availability, or market Product demand. Marginal costs help management determine the optimal production plan in the following ways. Use scarce resources in the most profitable way, thereby optimizing your profits. For example-

Ingredients are an important factor, their availability is limited to a certain quantity, and the company We manufacture three products, A, B and C. In such cases, the marginal cost method helps prepare a statement indicating the amount of contribution per kg of material. Products with the highest yields Contribution per kg of raw material is prioritized and produced as much as possible. After that, other products are picked up in order of priority. Therefore, the resulting product mix is Best profit in a given situation.

4) Decision Making: Management decision making is a very important function of any organization decision .The creation should be based on relevant information. Through the marginal cost method Information on cost behavior is provided in the form of fixed and variable costs. The Separation of costs between fixed and variable helps administrators predict cost behavior various options. Therefore, it makes decisions easier. Some decisions.

In some decisions, the resulting income is the deciding factor, while the basis for comparative cost analysis. Marginal costs help generate both types of information, so the decision is as follows. It's not intuitive, it's rational and factual. Some of the key areas of decision making is listed below:

5) Decision or purchase decision.

a) Approval or rejection of export proposal.

6) Fluctuations in selling price.

7) Variations in product composition.

8) Changes in sales composition.

9) Key factor analysis.

10) Evaluation of various alternatives for improving profits.

Department closure / continuation.

Key takeaways:

Break-even analysis is additionally referred to as cost-volume profit analysis. Break-even point analysis is a relationship between asking price, sales volume, fixed costs, variable costs, and profits at various level activity. Break-even analysis may be a widely used technique for studying the cost-volume-profit relationship narrow

Here, the entire cost is adequate to the entire asking price. The broader interpretation refers to the analytical system. Determines expected profits for all levels of activity. It describes the connection between production costs, Production volume and sales value.

Here, CVP analysis is additionally commonly performed, but it's not accurate, but it's called "break-even point analysis". The difference between the 2 terms is extremely narrow. CVP analysis includes full range Break-even analysis is one among the techniques utilized in this process. But as mentioned the above break-even point analysis techniques are so popular in CVP analysis research that the 2 terms are used as a synonym. For the needs of this investigation, we also these two terms to know the concept of break-even analysis, it's helpful to understand the following specific basic terms listed below application

1. Contribution

This is a more than the asking price that exceeds the variable cost. Also called "gross profit". The amount of profit (loss) is often confirmed by deducting fixed costs from contributions. In other words, it had been fixed Costs and benefits correspond to contributions. It is often expressed by the subsequent formula.

Contribution = Selling Price – Variable Cost or Contribution = Fixed Cost + Profit = Contribution – Fixed Cost

Profit / Volume ratio (P / V ratio)

This term is important for studying the profitability and profit ratio of operating a business.

Establish a relationship between contribution and sales. The ratio can be displayed in the following format Percentage too. The expression can be expressed as:

This ratio can also be found by comparing changes Contribution to changes in sales or changes in profits due to changes in sales. Increased contribution .Fixed costs are assumed to be constant at all production levels, which mean increased profits.

Therefore,

P/V Ratio (or, C/S ratio) = Contribution S𝑎𝑙𝑒𝑠 = C S or, P/V Ratio = Sales−Variable Cost S𝑎𝑙𝑒𝑠 = S−V S or, 1- Variable Cost S𝑎𝑙𝑒

This ratio is also known as the "contribution / sales" ratio. This ratio can also be found by comparing changes Contribution to changes in sales or changes in profits due to changes in sales increased contribution. Fixed costs are assumed to be constant at all production levels, which mean increased profits.

Therefore, Thus, P/V Ratio = Change in Contribution by Change in S𝑎𝑙𝑒𝑠 or, P/V Ratio = Change in Profit (or Loss) Change in S𝑎𝑙𝑒

The characteristics of the P / V ratio are as follows.

(I) Helps administrators see the total amount of contribution to a particular sale.

(II) The selling price and the variable cost per unit are constant or constant as long as they are constant. It fluctuates at the same rate.

(III) Not affected by changes in activity level. In other words, the PV ratio of the product. The amount of activity is the same whether it is 1,000 units or 10,000 units.

(IV) Fixed costs are not considered at all, so the ratio is also unaffected by fluctuations in fixed costs while calculating the PV ratio. For multi-product organizations, PV ratios are very important for management to decide which one to find. The product is more profitable. Management is trying to increase the value of this ratio by reducing variable costs or by raising the selling price.

3. Break-even point: A point that indicates the level of output or sales by dividing the total cost and sales price evenly. There is no profit or loss, it is considered a break-even point. At this point, business income exactly equal to that spending. If production is boosted beyond this level, profits will be generated in the business. And if it decreases from this level, the loss will be incurred by the business. Here it is appropriate to understand the different concepts of marginal costs and break-even points. Go further. This is explained below.

It's neither a profit nor a loss. Therefore, at the break-even point, the contribution is equal to the fixed cost.

Contribution = Fixed cost (1) Break-even point (in units) = Fixed Cost Contribution per unit (2) Break-even point (in amount) = Fixed Cost Contribution per unit x Selling Price per unit Or, = Fixed Cost Total Contribution x Total Sales Or, = Fixed Cost 1− Variable Cost per unit Selling price per unit = Fixed Cost P/V Ratio

Sales at break-even point = break-even point x selling price per unit

At the break-even point, the desired profit is zero. When calculating production or sales

You need to add a fixed amount of "desired profit" or "target profit" "desired profit" or "target profit" The cost of the above formula. For example:

(1) No. of units at Desired Profit = Fixed Cost+Desired Profit Contribution per unit (2) Sales for a Desired Profit = Fixed Cost+Desired Profit P/V Ratio

(2) Sales at break-even point = break-even point x selling price per unit

(3) At the break-even point, the desired profit is zero. When calculating production or sales

(4) You need to add a fixed amount of "desired profit" or "target profit" "desired profit" or "target profit"

(5) The cost of the above formula. For example:

Break-even point analysis: Relationship between selling price, sales volume, fixed costs, variable costs, and profits at various levels activity application.

C. You can use break-even analysis to determine your company's break-even point (BEP).

D. The break-even point is the level of activity where total revenue is equal to total cost.

E. At this level, the company does not make a profit

Break-even point analysis assumptions

F. Related range

G. The relevant range is the range of activities for which fixed costs remain fixed in total.

H. Variable costs per unit remain constant

I. Fixed costs

Key takeaways:

Resource-rich countries like Africa are more aware of the value of dealing with international organizations. In some parts of the world, labor relations are tense and public opinion is often hostile to oil and gas companies, even where they depend on natural resources for their livelihoods. In recent industries, there have been incidents in Africa that everyone is facing, although the companies doing business in the region are out of control. How do companies manage risk to better mitigate such incidents?

While executives are undoubtedly aware of the need to manage risk, comprehensive risk programs in many organizations in the oil and gas industry have not kept pace with operational complexity. In many cases, risk is prioritized only when there is a significant incident or event that affects risk within the sector. Given the rapidly changing environment, keep management and board up-to-date to identify new exposures, monitor known risks, make risk-informed decisions, and take advantage of market opportunities. Incorporating risk management into your business is essential to staying in shape.

Common industry mistakes: Many oil and gas companies have been implementing risk management or corporate risk management processes for several years. However, risk management is often misplaced as a compliance function or governance obligation and is seen as a mechanism solely for explaining risks and communicating them to the board of directors. This is not considered a strategic function and is not part of the business planning cycle. Risks are often left in silos and are not organized so that all categories of risk can be viewed in one view.

Risks and threats: Corporate-wide risks, especially emerging threats in new markets, are on the board agenda to understand and manage, but bottom-up assessments are also important. Historically, companies have always invested in risk management activities to address function-specific risks such as exploration risk, production risk, and financial risk, but the current challenge is to bring all these initiatives into a common framework to integrate with and strengthen decision making.

Geopolitical instability: Significant threats to the industry are geopolitical instability and potential risks. In addition to the potential nationalization of assets as recently seen in Argentina, there are also predatory fines by governments in urgent need of money. Reducing geopolitical risk means not only working on the legal and contractual frameworks that underlie a transaction or business, but also understanding the political situation in the region. Predicting changes in political conditions may not be enough to control its impact. Recognizing future political risk factors is one thing, but managing these risks in time to protect assets and people is another issue, especially when: Like Algeria in January 2013, risk is primarily security related.

Cyber security: Recent attacks on the industry show the actual impact that cyber threats can have on the sector through the leakage of commercially sensitive information such as exploration data and malicious interference with industrial control systems. -A tanker course with its proper equipment. Managing cybersecurity as strategic risk rather than operational risk is an important step change needed across the industry to drive long-term risk reduction with quantifiable benefits.

Cyber risks often perform scenario analysis to provide a detailed assessment of their impact on real risk, their greatest vulnerabilities, their exposure quantification, and how companies monitor and address potential cyber attacks. Is not enough to analyze. That is the biggest risk. Collaboration with the UK Government on FTSE350 Cyber Risk Management indicates that we need to rethink how cyber is reported upwards to the Board of Directors using more open and non-technical indicators.

Third party risk: Every company needs to interact with third parties that pose a variety of potential integrity and reputational risks, from customers and suppliers to agents to local or global strategic partners. In particular, increasing attention to regulatory compliance with anti-corruption laws and anti-corruption laws, such as the UK Foreign Corrupt Practices Act and the US Foreign Corrupt Practices Act, is due to a proper understanding of trading partners, their ownership and methods. It means that you can prevent illegal activities. The business may ultimately be responsible. This reduces the risk of public accusations, fines and even imprisonment. Flexible and responsive third-party risk management programs based on the right level of due diligence are essential for managing the widely talked about risk areas.

Operate with risk in mind: You should incorporate risk thinking from the first step to the end of the planning process, such as oilfield life cycle, labor relations, and entry into new markets. Companies often do not fully analyze the practical impact of risk. For example, leave risk described as geopolitical risk or cyber without careful consideration of the true exposure and readiness to prevent or respond in a way that minimizes adverse consequences and optimizes opportunities. Such exposures allow companies to fully assess the scope of their potential, measure their impact from a financial perspective in those scenarios, and incorporate accountability to monitor specific events using defined metrics. We rarely evaluate and report on the effectiveness of our mitigation plans. With this kind of data, you can determine if your company is at sufficient risk or too much. Are competitors of the same size more valued in the equity market because they are making better risk-based decisions? The difference may be due to a cautious and prudent approach to investing in uncertainty.

Required skills: Control functions and risk management need to be coordinated appropriately. Lack of skills and lack of knowledge and experience on how to achieve this form of integration are major obstacles to the convergence or integration of risk and management functions in oil and gas companies. Compliance, corporate governance, assurance, risk finance, etc. need to converge, but managers of these silos are often willing to give up their budget and perceived influence and power within their organization. You need one executive who understands a wide range of governance, risk management, and compliance issues. KPMG recently helped utilities consolidate six risk-related departments into one, standardizing risk-related functions for superior synergies, driving cost savings, and overall risk programs increased effectiveness.

Conclusion-

If risk management is viewed by business leaders as a proforma exercise solely for the consumption of board members, it remains forever isolated from operational reality. The CEO needs to take the lead in helping the board make risk-aware decisions at the corporate level. At the same time, help managers at the bottom of the hierarchy understand how choices affect a company's risk profile. Oil and gas companies often manage their health and safety and environmental risks well, but these challenges tend to mask other risks that may be equally dangerous to the company's health. There is. Only by developing a more strategic approach and integrating risk management processes into everyday business thinking can executives build a risk-aware culture.

Key takeaways:

References:

References: