Unit I

Double Entry System

For management to take future decision requires financial information. This is where accounting steps in that record, summaries, analyze all the business transaction.

Accounting is the process of recording, classifying, summarizing, analyzing, and interpreting the financial transactions and communicating the results to the persons interested in such information. Two methods for accounting are Single Entry System and Double Entry System. Mostly, we use Double Entry for better accounting purposes.

Double entry system

Double entry system of accounting deals with two aspects of every business transaction. In other words every transaction has two effects. For ex, a person buys a cold drink from a store and in return pays the money to shopkeeper for the cold drink. This transaction has two effects in terms of both buyer and seller. Buyer cash balance will decrease by the cost of purchase on the other hand he will acquire a cold drink. Seller will have one drink short but his cash balance will increase.

Accounting attempts to record both effect of transaction in the financial statement. This refers to double entry concept. Under this every transaction involves two parties , one party gives the benefit and other party receives it. It is also called dual entity of transaction.

Accounting records the two affects which are known as Debit (Dr) and Credit (Cr). Accounting system is based on the duality principal that for every Debit entry, there will always be an equal Credit entry.

Debit entries are ones that account for the following effects:

- Increase in assets

- Increase in expense

- Decrease in liability

- Decrease in equity

- Decrease in income

Credit entries are ones that account for the following effects:

- Decrease in assets

- Decrease in expense

- Increase in liability

- Increase in equity

- Increase in income

Accounting equation recorded in double entry are

Assets – Liabilities = Capital

Any increase in expense (Dr) will be offset by a decrease in assets (Cr) or increase in liability or equity (Cr) and vice-versa. The accounting equation will still be in equilibrium.

Examples of double entry

- Purchase of machine by cash

Machine account debited (increase in assets)

Cash account credited (decrease in assets)

2. Payment of utility bills

Utility expenses account debited (increase in expenses)

Cash account credited (decrease in assets)

3. Receipt of bank loans

Cash account credited (increase in assets)

Bank loan account credited (increase in liability)

Characteristic of double entry system

- Two parties – every business transaction involves two parties – debit and credit. According to the duality principal that for every Debit entry, there will always be an equal Credit entry.

2. Giver and receiver – every transaction must have giver and receiver. For ex, purchase a car, the buyer purchase a car from seller in return of cash – hence the buyer is the receiver and seller is the giver. When the seller receives the cash for the purchase made by buyer – the seller is the receiver of cash and buyer is the giver.

3. Exchange of equal amount – the amount of money of a transaction the party gives is equal to the amount the party receives.

4. Separate entity - the business enterprise and its owner are two separate independent entities. Thus, the business and personal transaction of its owner are separate.

5. Dual aspects – every transaction has two aspects – debit and credit. Debit is on the left side of account ledger and credit is on the right side of account ledger.

6. Result – under double entry system, total of debit is equal to total of credit.

7. Complete accounting system: Double entry system is a scientific and complete accounting system.

The process of keeping accounts under the double-entry system;

- Journal - It is called as daily book because transaction are recorded on day to day basis as and when takes place

2. Ledger - Ledger is the principal or primary book of accounts. The transactions are classified under appropriate heads, called accounts

3. Trial balance - Trial balance is a statement, prepared with debit and credit balances of ledger accounts to test the arithmetical accuracy of the books

4. Financial statement - The final accounts are prepared for ascertaining the operational results and financial position of the business. These are prepared with the help of trial balance.

Advantages of double entry system

- Through the trial balance, the system increase the accuracy of the accounting

- Profit and loss during the year can be calculated in detail

- The company keep accounting records which helps in controlling

- Using double entry system of accounting, current year can be compared with previous year to formulate the future course of action

- Under double entry system, the total amount of assets and liabilities can be ascertained

- Under the double-entry system, the accounts are maintained systematically thus it become easier to fix the price of the commodity

- The balance sheet ascertains the financial position of the business.

Accounting concepts defines the assumption on the basis of which financial statement of a business entity is prepared. Concepts are those basic assumption and condition which form the basis upon which the accountancy has been laid.

Accounting principles

- They should be based on real assumption

- They must be simple, understandable and explanatory

- They must be followed consistently

- They should be able to reflect future predictions

- They should be informational to users

Accounting convention emerges out of accounting practices, commonly known as accounting principle, adopted by various organizations over a period of time. Accounting bodies may change any of the convention to improve the quality of accounting information.

Accounting concepts

- Entity concept – Entity concept states that the business enterprise and its owner are two separate independent entities. Thus, the business and personal transaction of its owner are separate.

For example, when owner invests money in the business, it is recorded as liability of the business to the owner. Similarly, when owner takes money from business for personal use, it is not treated as business expenses.

2. Money measurement concept – This concept assumes that all business transaction must be in terms of money. Thus transactions expressed in terms of money are recorded in the books of account.

For example – sale of good, rent paid are expressed in money so recorded in books of account. Whereas sincerity, loyalty are not recorded in books of account because they cannot be measured in monetary terms.

3. Going concern concept - This concept states that a business firm will continue to carry on its activities for an indefinite period of time. It means every business entity has continuity of life and will not be resolved in the near future.

4. Accounting period concept –All transaction are recorded in the books of account on the assumption that profits on these transaction are to be ascertained for a specific period. Thus, this concept states that a balance sheet and profit and loss account should be prepared at regular interval

5. Accounting cost concept – It states that all assets are recorded in the books of account at their purchase price which include cost of acquisition, transportation and installation and not at its market price.

For example – fixed assets like building, machinery are recorded at purchase price

6. Dual aspect concept – dual aspect is the basic principle of accounting. It provides the basis of recording accounting transactions. For every credit, a corresponding debit is made. Therefore the transaction should be recorded in two places.

7. Matching concept – this concept states that revenue and expenses incurred to earn profit must belong to the same accounting period. So once the revenue is realized, the next step is to allocate it to the relevant accounting period. It is very helpful for the investors to know the exact amount of profit and loss in the business

8. Realization concept – the concept states that, revenue is realized at the time when goods and services are actually delivered. An advance or fee paid is not considered a profit until the goods or services are delivered to the buyer.

9. Accrual concept – accrual concept means the amount of money is yet to be paid or received at the end of the accounting period. It means cash received or not and expenses paid or not, both the transaction will be recorded in the books of account in that accounting period

Accounting convention

- Consistency – consistency means same accounting principles should be uses year after year, so that same standards are applied to calculate profit and loss. While comparing over a period of time a meaningful conclusion can be drawn. If a different accounting principles are used , then it cannot be comparable

2. Full disclosure – It includes all material and relevant facts concerning financial statements should be fully disclosed. Full disclosure means full, fair, adequate disclosure of accounting information. Parties like investor, lender, etc are interested in the financial information, so the business entity should disclose full and fair information.

3. Materiality – it means all material fact should be recorded in accounting. Accountant should record important data and leave insignificant data. Material fact influence the decision of the users.

4. Conservatism – the conservatism is based on the principle that “Anticipate no profit, but provide all the possible losses”. The main objective is to show minimum profit. Profit should not be over estimated. It is an unfair convention, it will lead to reduction in the capital of an enterprise

Definition

“The journal is a book of original entry in which transactions are recorded not provided for in specialized journals”

Eric L. Kohler

- The word journal has been derived from French word ‘Jour’ which means day. Thus, journal means daily record

- Entries in journal are recorded in chronological order, as and when the business transaction occurs

- It is called as daily book because transaction are recorded on day to day basis as and when takes place

- Entry in journal is followed with narration which describes briefly the true nature of transaction

Proforma of a Journal

- Date/ S.No: date or serial number is the first column of Journal. The transaction record date or its serial number is updated in this column.

- Particulars: particulars are the second column of Journal. This column is updated with the particulars of business transactions that is related to the description of account type.

- Ledger Folio: The third column of Journal is Ledger Folio number where the journal entry is posted.

- Amount (Dr.) : The fourth column of Journal is used to update the debit amount of transaction.

- Amount (Cr.): The fifth column of Journal is used to update the credit amount of transaction.

Rules of double entry system

- Personal accounts – Account related to human beings and artificial person such as Anils account, accounts of firms, hospital, etc

RULE

Debit the receiver and credit the giver

2. Real accounts – accounts which can be touched, felt such as plant, building, cash, etc. It also includes account which cannot be touched but are measured in terms of rupee such as goodwill, etc

RULE

Debit what comes in and credit what goes out

3. Nominal account – account relate to business gains, loss, incomes and expenses such as wages account, interest account, etc

RULE

Debit all expenses and losses. Credit all incomes and gains

Examples of journal entry

A firm sold its product at 1500 and received full amount in cash

Definition

In a large business concern a journal is divided into parts so that several clerk could work at the same time. This is known as subdivision of journal.

Objectives of subdivision

- To simplify the recording of business transaction in the book of original entry

- It enables the transaction are classified according to their name.

- To make it easier to locate any transaction recorded in the book of original entry

- Recording the transaction in the books of account result in reducing the chances of error and fraud

Advantages

- The transaction recorded in the sub division books is not bulky and hence there will be no difficulty in handling them.

- Accounting work is divided into large number of employees so the work is done nicely and promptly

- Because of division of labour, efficiency of employees increases

- The chances of fraud is minimised as the transaction are recorded in the books.

Types of subdivision of journals

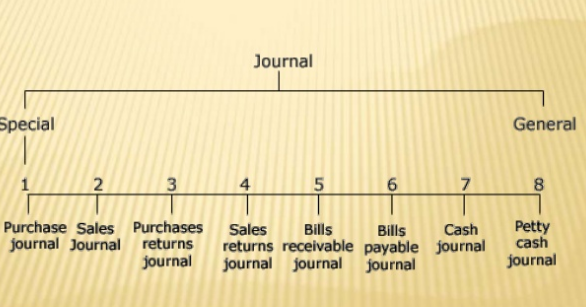

Special journal – special journal is popularly known as the subsidiary book. The transaction are recorded in regular basis and in chronological order. Special journal are divided into eight groups as follows

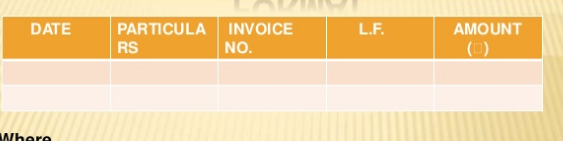

- Purchase book – purchase book is also called as purchase journal, invoice book, bought day book which records all credit purchase made by the organisation. Cash purchase of book are not recorded in the purchase book, they are recorded in cash books. Credit purchase other than goods such as stationary item are not recorded in the purchase book

Format

Where, data – represents when the transaction took place

Particulars- it includes the name of the seller and the particulars of goods purchased

Invoice no – reveals the serial number of the inward invoice

LF – This column represent the page number of supplier account in ledger books

Amount – amount column represent the price of the goods

2. Sales books – this book is also known as sales day book or sales journal. It records all credit sales of goods made by the organisation during a specified period of time.

Cash sales, cash and credit sales of assets are not recorded in the books. The entries are recorded on the basis of invoice issued to the customers

Format

Where,

Date – represents when the transaction took place

Particulars- it includes the name of the customer and the particulars of goods sold

Invoice no – reveals the serial number of the outward invoice

LF – This column represent the page number of supplier account in ledger books

Amount – amount column represent the price of the goods

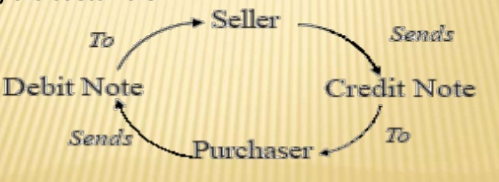

3. Purchase return books – this books records all the return of goods to the supplier by the business. It is also called returns outward book or purchases returns day book. Goods may be returned due to many reasons such as not up to sample or because they are damaged etc. When good are returned to the supplier then an intimation is sent which is known as debit note

Format

Where,

Date – represents when the transaction took place

Particulars- it includes the name of the purchaser and the particulars of goods purchased

Debit note no – records the serial number of each debit note

LF – This column represent the page number of supplier account in ledger books

Amount – amount column represent the price of the goods

4. Sales returns books – this book records all the return of goods by the customers to the business. Sales returns book is also called returns inwards book. Customers who return goods should be sent a credit note by the business. This credit note means note sent by the business to another person showing the amount credited to the account of the later.

Format

Where,

Date – represents when the transaction took place

Particulars- it includes the name of the purchaser and the particulars of goods purchased

Credit note no – records the serial number of each credit note

LF – This column represent the page number of supplier account in ledger books

Amount – amount column represent the price of the goods

5. Bills receivable book – bills receivable books is used to record the bills received from debtor. The details of the bill received from the debtors are recorded in the bills receivable books. The bills receivable are drawn when the seller makes credit sale to the business.

Format

Where,

Date – represents when the transaction took place

From whom received column - it includes the name of the person from whom the amount is to be received.

Term column – how much time

Due date column – last date

LF – This column represent the page number of supplier account in ledger books

Amount – amount column represent the price of the goods

6. Bills payable book – bills payable book is used to record bill accepted by us and payable by the business. When a bill drawn by our creditor is accepted particulars of the same are recorded in this book. In the ledger the amount of each person whose bill has been accepted is debited with the bill amount. The total of bills accepted is credited to the bills payable account ledger.

Where,

Date – represents when the transaction took place

To whom given - it includes the name of the person from whom the amount is to be paid.

Term column – how much time

Due date column – last date

LF – This column represent the page number of supplier account in ledger books

Amount – amount column represent the price of the goods

7. Cash book – a separate book is kept to record cash transaction refers to cashbook. The function of cash book is to keep records of all cash transaction.

Types of cash book

- Simple cash book - it record only cash transactions. All cash received are entered on the debit side, and all cash paid are entered on the credit side.

Format –

Where,

Date – represents when the transaction took place

Particulars- it includes cash transaction particulars

LF – This column represent the page number of supplier account in ledger books

Amount – amount column represent the price of the goods

b. Double cash book – it record cash as well as bank transactions. It is also called as two column cash book. The cash column is used to record all cash transactions and bank column used to record all receipts and payments made by checks and works as a bank account

Format

Where,

Date – represents when the transaction took place

Particulars- it includes cash and bank transaction particulars

Cash – records cash transaction

Bank – records transaction made on cheque or which are held via bank

c. Triple cash book – it record cash, bank and purchase discount and sales discount. It is also called as three column cash book

Format

Where,

Date – represents when the transaction took place

Particulars- it includes cash and bank transaction particulars

Cash – records cash transaction

Bank – records transaction made on cheque or which are held via bank

Discount – shows discount allowed and received

d. Petty cash book - A petty cash book to record small day to day cash expenditures. For ex, stationary, cleaning charges, postages, etc

The petty cash book is defined as relatively small amount of cash kept at hand for making quick payments for miscellaneous small expenses in the business concern.

General journal

The transaction which do not fall within the scope of the above mentioned book are recorded in general journal. For ex, purchase of assets on credit, depreciation of assets, bad debts, etc. It is also known as modern journal, journal proper, principal journal.

Where,

Date – represents when the transaction took place

Particulars- it includes all transaction particulars

Debit column – shows amount received

Credit column – shows amount paid

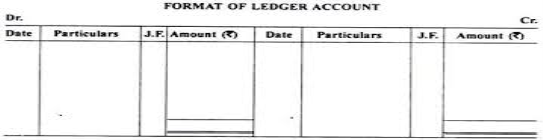

Ledger

Definition

“Ledger is the permanent storehouse of all the transactions” Field house Arther

- Ledger is the principal or primary book of accounts

- The transactions are classified under appropriate heads, called accounts

- The accounts contain the condensed and summarized record of all the related transactions

- It is the basis of preparing final account.

- Ledgers provide information of

- Debtors and creditors

- Purchase, sales and return

- Type of assets and value of assets

- Expenses and income

- Cash and bank balance

- Date on which the transaction taken place

- Particulars – on debit side, the account is written with prefix “To”. On the credit side, the account id written with prefix “By”.

- JF is the page number of journal provided for cross reference.

- The amount written in journal is written in ledger

Characteristics of ledger accounts

- The account has two sides left side of the account is debit and right side of the account is credit.

- Debit side record all the debit attitudes of transactions and credit side record all the credit attitudes of transactions

- Difference between the two sides are represented as balance. The debit balance shows excess of debit over credit side. The credit balance shows excess of credit over debit side.

- In the month/year end the excess balance is written over the closing balance at the end of the month date

- At the end, closing balance are forwarded as the beginning balance next year.

How double entry works in ledger

A ledger implemented in double entry book keeping method means each transaction make atleast two account. Each transaction has debit and credit account. Left side shows debit entry and right side shows credit entry.

For better understanding lets use a n example of ledger accounts

Transaction

On jan1 2015, abc company sold to customers for cash 25,000.

The journal entry and ledger posting are as follows

In the above journal entry, the debit part is cash account and the credit part is sales account. All journal entries are similarly posted to accounts in general ledger.

Examples 2

Apple limited sell 20 kilos apple at rs. 100per kilo on 8 august 2020

Journal entry

Cash A/C Dr 20000

To Sales A/C 20000

Ledger account

Cash A/C | |||||

Dr. |

| Cr. | |||

Date | Description | Amount (Rs) | Date | Description | Amount (Rs) |

8.8.2020 | To Sales | 20000 |

|

|

|

Similarly, in Sales account, the entry will reflect as follows

Sales A/C | |||||

Dr. |

| Cr. | |||

Date | Description | Amount (Rs) | Date | Description | Amount (Rs) |

|

|

| 8.8.2020 | By Cash | 20000 |

Trial balance

Definition

“Trial balance is a statement, prepared with debit and credit balances of ledger accounts to test the arithmetical accuracy of the books”. J.R. Batliboi

- It is the statement from which final accounts are prepared

- It is the list of balances of all the ledger accounts

- The total of debit and credit column of trial balance must tally

How does trial balance work?

The trial balance is the statement of all debits and credits. Business man prepares trial balance at the end of the reporting period regularly to ensure that the entries are mathematically correct in the books of account. The total of trial balance should be equal. In case the debit and credit does not match it means there is an error. For example, the accountant may have recorded an account or classified a transaction incorrectly.

Preparation of trial balance

- Before starting the trial balance all the ledger accounts should be closed. The ledger balance is provided by the difference between the sum of all the debit entries and the sum of all the credit entries

- Prepare trial balance worksheet. The column headers should be for the account number, account name and the corresponding columns for debit and credit balances.

- Every ledger account is transferred to the trial balance worksheet. The account name and number along with the account balance in the appropriate debit or credit column

- Add up the debit and credit column. In an error free trial balance the total should be same. Trial balance are closed when the total are same

- Accountants have to locate and rectify the errors, if there is a difference,

A trial balance looks like

All the account title are the closing balance of ledger account

ABC LTD - Trial Balance as at 31 December 2019 | ||

| Debit | Credit |

Account Title | Rs | Rs |

Share Capital | - | 15,000 |

Furniture & Fixture | 5,000 | - |

Building | 10,000 | - |

Creditor | - | 5,000 |

|

|

|

Debtors | 3,000 | - |

Cash | 2,000 | - |

Sales | - | 10,000 |

Cost of sales | 8,000 | - |

General and Administration Expense | 2,000 | - |

Total | 30,000 | 30,000 |

Final Accounts are prepared, normally, for a complete period. It must be kept in mind that expenses and incomes for the relevant accounting period are to be taken, while preparing final accounts. If an expense has been incurred but not paid during the period, a liability for the unpaid amount should be created, before finding out the operating result and financial position of a concern. In order to prepare the final accounts on mercantile system of accounting, all expenses and incomes relating to the period, whether incurred or not, received or not, should be brought into the books. For doing this, a concern is required to pass certain entries at the end of the year to adjust the variousitemsofincomesandexpenses.Suchentriesarecalledadjustingentries.

Accounting Treatment: Trading and Profit and Loss and Balance sheet, together, are called as final accounts. Item appearing in the trial balance appears only once in final accounts, either on the debit or credit. Any adjustment entry requires two postings, debit and credit for the same amount. Important point is students should do the posting (debit and credit) in the concerned accounts, simultaneously. Care is to be exercised that the amount is the same for the total debit and credit.

The following are the important adjustments, which are, normally made at the end of accounting period.

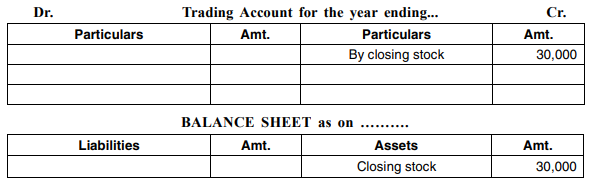

- Closing Stock

Every concern prepares a list of unsold goods at the end of the period and puts value against it. It is to be remembered that stock is valued at cost or market price, whichever is less.

Closing Stock appears below the Trial Balance as an adjustment entry: Normally, closing stock appears as an adjustment entry in the problem and is given at the end of the trial balance. For example, if the value of stock at the end of the period is Rs. 30,000 and is shown below the trial balance, then the following adjusting entry will be passed:

Closing Stock A/c …Dr 30,000

To Trading Account 30,000

The two-fold effect of this entry will be:

(i) Stock will have a debit balance. Being a real account, it will be shown on the assets side of the Balance Sheet.

(ii) Closing stock will be shown on the credit side of the Trading Account.

Closing Stock appearing in Trial Balance: Sometimes, opening and closing stock are adjusted through purchases. In this case, closing stock (debit balance) appears in the Trial Balance. Closing stock, under this case, will not be shown on the credit side of the Trading Account but will be shown on the assets side of Balance Sheet only. Remember, any entry appearing in the Trial Balance appears only once either on the debit side or credit side, depending on the nature of the transaction.Closing stock is a real account, hence appears on the assets side of the balance sheet.

2. Outstanding Expenses

There are certain expenses, which have been incurred but not paid. These expenses are called outstanding expenses. For example, salary to the clerk Rs. 1,000 is due for the month of December. Books are closed at the end of December. In order to bring this transaction into accounts, the following adjustment entry will be passed:

Salary Account…..Dr. Rs.1, 000

To Outstanding SalaryA/c. Rs. 1,000

The two-fold effect of this entry will be:

- Outstandingsalarywillbeaddedtosalary,ifany,onthedebitsideofProfit&Loss

Account.

2. Outstanding Salary Account, being personal and having credit balance, will be shown on the liabilities side of the Balance Sheet.

3. Prepaid or Unexpired Expenses

Those expenses which have been paid, in full, but their utility or benefit has not expired during the accounting period are called prepaid or unexpired expenses. In other words, amount has been paid even for the period subsequent to the balance sheet date. For example, annual premium Rs. 12,000 is paid on 1st July, where accounting year closes on 31st December. Rs. 6000 will be insurance paid in advance. To bring this into account, the following adjusting entry will be passed:

Prepaid Insurance Premium Account…..Dr. Rs.6, 000

To Insurance Premium Rs.6, 000

The double effect of this adjusting entry will be:

- Prepaid insurance will be deducted from the insurance premium on the debit side of the Profit & Loss Account.

- Prepaid insurance, being personal account and having debit balance, will be shown on the assets side of the Balance Sheet.

4. Accrued Income

Income earned but not received during the accounting period is called accrued Income.

Suppose, the interest on investments shown in the trial balance is Rs. 19,500.

The adjustment may run like this. Interest @10% is due on investments of Rs. 10,000 for 6 months, though accrued, has not been yet been received.

This interest Rs. 500 will be accrued income. In order to bring this into account, the following adjusting entry will be passed:

Accrued Interest on Investments Account …..Dr. Rs. 500

To Interest on Investment Account Rs. 500

The two fold effect of this entry will be:

- Interest on Investment account (accrued interest) will be added to the interest account on the credit side of the profit & loss account.

- Accrued interest, being personal account and having debit balance, will be shown on the debit side of the Balance Sheet.

Illustration No. 1

On the 1st January, 2008 Nilesh lent Rs 5,000 @ 6% per annum. Interest is receivable on 31st December each year. The accounts are closed on 30th June each year.

Give journal entries on 30th June, 2008 and 1st July, 2008 and show the ledger, profit & loss account and balance sheet 30th June, 2008.

Solution:

5. Unearned Income or Income Received in Advance

Sometimes, the amount received in respect of an income during the year pertains, partially, to the next year. Suppose a landlord corrects rent for one quarter, in advance, and closes his account on 30th June each year. Suppose, a tenant has occupied a house on 1stJune and pays Rs. 1,800 as rent for 3 months. The landlord must not treat the whole of the rent received as income for the current year. Two months’ rent pertains to the next year and should be credited to the Profit and Loss Account of next year. This will ensure that the income for the current year is not overstated.The required entry is:

Rent Account ….Dr Rs.1,200

To Rent Received in Advance Account Rs. 1,200

In the Profit and Loss Account and the Balance Sheet, the item will be shown as indicated below:

The Rent Received in Advance Account will be transferred to the Rent Account in the next year.

This principle should be applied to all incomes, which pertain wholly, or partially to the next year. Other examples can be the fees received from students, before the summer vacation or subscription received in respect of a magazine. The fees applicable to the period after the close of the accounting year or the subscription for copies, to be supplied after the end of the year, should be credited to unearned income account by debit to the account of the students’ fees or the subscription. This will ensure that the income for the current year is not overstated.

- Depreciation

The value of fixed assets goes on reducing year by year because of wear, tear and efflux of time. This fall in the value should be treated as a loss or expense, to be considered before profit or loss is ascertained. The value to be shown in the Balance Sheet must also be, suitably, reduced. To continue to show it at the old figure will be overstating the assets. Depreciation is usually computed on the basis of the life of the assets. Suppose, a machine costs Rs. 1,00,000 and has a life of 5 years. Then, each year 1/5th of the cost, i.e., Rs. 20,000 should be treated as an expense;onlytheremainingamountistobeshowninthebalancesheet.Theentryis:

Depreciation Account …Dr.20,000

To Machinery Account 20,000

Depreciation is debited to the Profit & Loss Account. In the final accounts, the item will figure as shown below:

Depreciation appearing in Trial Balance: In this case, depreciation entry has, already, been passed, before preparation of the trial balance. In that case only, the Depreciation Account will figure in the trial balance itself. The concerned asset will appear at its reduced value since the amount of the depreciation would have been credited to it. In such a case, no further adjustment will be necessary; the Depreciation Account will be transferred to the debit of the Profit & Loss Account like other expenses.

Again, it is reminded if any entry appears in the trial balance, only once it appears in the financial statements. Here, it appears in profit &loss account. Only Adjustment involves two entries.

Pro rata depreciation: While computing depreciation, the period for which the asset is used should be kept in mind. Suppose, a machine is purchased on 1st January, 2008 for Rs. 10,000 and another machine is purchased on 30th June, 2008 for Rs. 6,000: the rate of depreciation is 10%. Accounts are closed at the end of the calendar year. The depreciation for 2008 will be Rs. 1,300 as shown below:

Rs.

OnRs.10,000foroneyear@10% 1,000

OnRs.6,000forsixmonths@10% 300

1,300

Treatment in case of Loose Tools: In some cases like loose tools, depreciation is arrived at by comparing the value on two dates. Suppose loose tools were valued at Rs. 2,300 on 1st January, 2008andatRs.2,100on31stDecember,2008,thedepreciationwillbeRs.200.

6. Interest on Capital

The proprietor may wish to ascertain his profit, after considering the interest for the amount invested in the firm. Suppose, the capital is Rs. 2, 00,000 and the rate of interest is 5%. Then, the interest will be Rs. 10,000. It will be treated like other expenses and debited to the Profit and Loss Account; the amount will also be credited to the Capital Account. The entry is:

Interest on Capital Account …Dr.10, 000

To Capital Account 10,000

In the final statements of account, the item will appear as shown below:

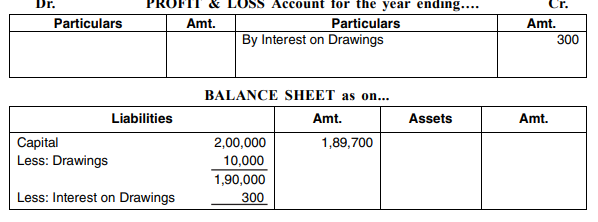

- Interest on Drawings

The proprietor may also realize that when he draws money for private use, the firm loses interest as funds for business are reduced. Therefore, the proprietor’s capital may be debited with the interest on the money drawn by him. Interest will depend on the amount and the date of withdrawal concerned. In absence of information about the date of drawings, it should be assumed that the drawings were made, evenly, throughout the year; therefore, interest should be charged for six months on the full amount. Suppose, capital is Rs. 2, 00,000 and the total drawings are Rs.10,000.The rate of interest is 6% on the drawings.

The average amount of drawings on which interest is to be charged is Rs. 5,000. So, interest @ 6% on drawings Rs. 5,000 will be Rs. 300. The entry to be passed is:

Interest on Drawings ...Dr. Rs.300

To Profit &Loss Account Rs.300

It will be shown as follows:

Drawings and Interest on drawings are reduced from Capital account.

Drawings and Interest on drawings are reduced from Capital account.

7. Interest on Loan

Interest must be paid on loans, whether there is profit or loss. It is calculated by reference to the rate of interest agreed to be paid by the firm. Suppose a loan of Rs. 20,000 is taken on 1st May 2008 at 18%, if the accounts are closed on 31st December, the interest for the year will be Rs. 2,400 i.e., Rs. 20,000 × 18/ 100 × 8/ 12. The amount of the interest, if not paid, is to be credited to the Outstanding Interest Account. The debit entry will be to the Interest on Loan Account. The entry is:

Interest on Loan Account ….Dr. Rs.2, 400

To Outstanding Interest Account Rs. 2,400

The item will figure as follows in the final accounts:

8. Classification of Debtors

Once goods are sold on credit, debtors appear in accounts. In place of debtors, bills receivable may also appear. Debtors and bills receivable represent the amounts to be received by the firm for the credit sales made. All debtors and bills receivable may not be realizable. Where recovery is impossible, those amounts are to be written off as bad debts. Against likely bad debts, provision is required to be made. Both bad debts and provision for bad debts reduce the profits of the firm.

9. Bad Debts

Credit sales have become a must these days and bad debts occur, when there are credit sales. Bad Debt is a loss to the business and a gain to the debtor. The following journal entry should, therefore, be passed in the event of a debt becoming bad.

Bad Debts A/c Dr.

To Debtor’s Personal A/c

Illustration No. 2

Kalyan & Co. Has been running its cloth business. At the end of Dec. 2008, the firm’s books of accounts show the debtors at Rs. 4,00,000. Out of those debtors, Rs. 20,000 have been recognized as bad debts as those debtors have become insolvent.

Show the position in the financial statements.

Solution:

Illustration No. 3

Following are the extracts from Trial Balance of a business.

Additional information: Mehata, one of the debtors became insolvent and it was learnt on 31st December, that out of the total debt of Rs. 5,000 only Rs. 2,500, will be recovered from him. No adjustment has so far been made.

You are required to pass necessary adjusting entries and show how the items will appear in the Final Accounts of the business.

Solution:

Note: Bad debts, appearing in Trial Balance, have already seen provided for. Now, the adjustment relates to additional bad debts for the amount appearing in sundry debtors.

10. Provision for Bad and Doubtful Debts

Prudent accounting principle is to make provision for expected losses and not to take credit for expected profits.

All credit sales would not be realized in the year in which the sales are made. Sales may be made in one year and actual realizations may happen in the succeeding year. A firm, therefore, makes provision at the end of the accounting year, for likely bad debts, which may happen during the course of the next year. The simple reason is all collections do not occur in the same year in which sales are made. Some sales are likely to become bad in the course of the next year. So, the proper course would be to charge such likely bad debts in that accounting year in which sales have been made, since, the profit on such sales has been considered in the year in which the sales have been made.

The following journal entry is passed for creating a provision for bad debts.

Profit &Loss A/c Dr.

To Provision for Bad and Doubtful Debts

The provision for bad debts is charged to the Profit & Loss Account and is deducted from debtors in the Balance Sheet.

Calculation of Provision for Bad and Doubtful Debts: Normally, problem states the % of Provision for Bad and Doubtful Debts. On which amount of debtors, this % of Provision for Bad and Doubtful Debts is to be calculated?

From debtors, first deduct total bad debts from debtors. Bad debts are that amount, appearing in the trial balance and any further provision that may be required in the adjustment for bad debts.

On the balance amount of debtors only, Provision for Bad and Doubtful Debts is to be calculated. Reason is simple. Once, debt becomes bad, it would be written off. So, bad debts amount is already excluded from debtors. The balance amount of debtors is only good debts, expected to be realized. Even this amount may not be totally recoverable and for this reason only, Provision for Bad and Doubtful Debts would be created.

Provision for Bad and Doubtful Debts is to be calculated on that amount of debtors, after deducting bad debts. Provision for Bad and Doubtful Debts is not to be calculated on the total amount of debtors.

Illustration No. 4

Following are the extracts from the Trial Balance of a firm.

Additional Information:

- After preparing the Trial Balance, it is learnt that a debtor, Talwar has become insolvent and therefore, the entire amount of Rs3,000 due from him was irrecoverable.

- Create10%provisionforbadanddoubtfuldebts.

You are required to pass necessary adjusting entries and show how the items will appear in the firm’s Balance Sheet.

Solution:

The provision for bad debts created at the end of the accounting year is carried forward to the next year. At the end of the next year, suitable adjusting entry is passed for keeping the provisionfordoubtfuldebtsatanappropriateamounttobecarriedforward.

Illustration No. 5

Kishore & co. Has been a running garment business. At the end of Dec, 2007, the firm’s books of accounts show the debtors at Rs. 3, 00,000. Out of those debtors, Rs. 1,000 are not traceable and to be treated as bad debts. By practice, over the years, it has been noticed that the business loses money even on the expected realizations from the good debtors too. The business adopts a consistent policy of making a provision of 5% on the expected good debtors towards bad and doubtful debts.

Show the position in the financial statements.

Solution:

Note: Provision for Bad and doubtful debts is to be made on Rs. 2,90,000 but not on Rs. 3,00,000 as Rs. 10,000 has already, been removed as bad debt from sundry debtors. Chance of becoming bad is on the balance amount only i.e. Rs.2, 90,000.

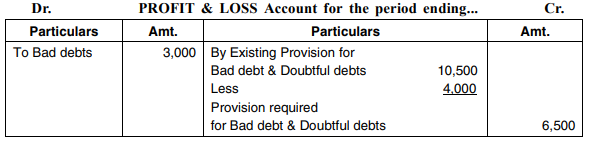

Presentation in Accounts for Bad Debts &Provision for Bad and Doubtful Debts: Students, in particular non-commerce people, often experience difficulty when both bad debts and provision for bad doubtful debts are to be made, in particular, when the trial balance is already showing the provision for bad and doubtful debts.

Trial balance is showing the provision for bad and doubtful debts. So, this was the balance for bad and doubtful debts at the end of the last year, which has been carried forward.

Follow the simple approach:

Show bad debts and provision for bad and doubtful debts, separately, in Profit and Loss Account.Do not club them up.

Presentation in Profit & Loss account:

If the current year’s provision for bad and doubtful debts, required to be made, is more than the provision for bad and doubtful debts shown in the trial balance, show the additional provision on the debit side of the profit and loss account as this is an additional expense.

Is the current year’s provision for bad and doubtful debts, required to be maintained at the end of the year, is less than the provision for bad and doubtful debts shown in the trial balance? Show the excess provision (Last year’s provision in shown Trial Balance

– provision required to be maintained in current year) on the credit side of the profit and loss account. This is an income, as the earlier estimated expense is no longer needed to be continued.

Presentation in Balance Sheet:

Deduct first provision for bad debts and later provision for bad and doubtful debts, required to be maintained at the end of the year, from the debtors in the balance sheet.

The following problem explains the treatment of higher provision for bad and doubtful debts:

Illustration No. 6

At the end of the year 2008, Radhi & Co. Has observed that their the debtors are Rs. 5, 00,000. Out of those debtors, Rs. 5,000 are not traceable and to be treated as bad debts. By practice, over the years, it has been noticed that the business loses money on the expected realizations from the good debtors too. The business adopts a consistent policy of making a provision of 5% on the expected good debtors. Provision for bad and doubtful debts stand at Rs. 14,500 at the end of Dec, 2007.

Show the position in the financial statements.

Solution:

The following illustration shows the presentation when provision for bad debts, now, needed is lower than the existing provision in the trial balance:

Illustration No. 7

At the end of the year 2008, Dimpy & Co. Has observed that their the debtors are Rs. 2,00,000. Out of those debtors, Rs. 3,000 are to be treated as bad debts. Provision for bad & doubtful debtsRs.4,000isneededattheendofDec,2008.

Provision for bad & doubtful debts stand at Rs. 10,500 at the end of Dec, 2007. Show the position in the financial statements.

Solution:

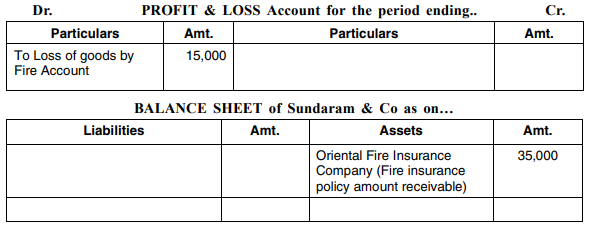

11. Accidental Losses

Stock of goods may also be destroyed or damaged by fire, etc. As a result, the value of the closing stock will be lower than otherwise. This will reduce the amount of the gross profit and, in turn, net profit, automatically. It is always better to ascertain the gross profit, which would have been earned, in absence of the loss since this enables the firm to judge its trading operations, properly. This will be possible if the amount of the loss of goods is credited to the Trading Account and debited to the Profit and Loss Account. By this entry, the increases in the gross profit will be neutralized by the debit to the Profit and Loss Account and thus the net profit will not be affected.

The entries to be passed, say, in case of fire, are as follows:

Loss of goods by Fire Account ……Dr.

To Trading Account.

If there is an insurance policy to cover the goods concerned, part or the whole amount of loss may be admitted by the insurance company. The amount received or agreed to be paid by the insurance company will be credited to the Loss of Goods by Fire Account. The remaining amount only will be transferred to the Profit and Loss Account as a write off as this would be the final loss due to accident.

(ii) Profit and Loss Account …..Dr. To Loss of goods by Fire Account

Illustration No. 8

Sundaram & Co. Has lost stocks in a fire accident Rs. 50,000. Amount admitted by Oriental Fire insurance company under the fire insurance policy is Rs. 35,000. The claim amount is yet to be received from the insurance company. Show the presentation in the Trading, Profit and Loss Account and Balance Sheet.

Solution:

Note: Out of a loss of Rs. 50,000, Oriental Fire insurance company has admitted the claim for Rs. 35,000. Sundaram & Co. Can recover Rs. 35,000 only from the Oriental Fire insurance company. Hence, the net loss duetofireaccidentRs.15, 000 has been written off to Profit and Loss Account.

12. Commission Payable on Net Profits

Sometimes, Company may provide an incentive to the manager in the form of commission on profits to improve profitability of the company. Suppose the profit earned by the firm is Rs. 80,000, without considering the commission; commission is 5%. The commission will be then Rs. 4,000. The profit will be reduced to Rs. 76,000. The entry to be passed will be to debit the Profit and Loss Account and credit the Commission Payable Account. This account will be a liability and shown in the balance sheet.

Sometimes, commission may be on the net profits of the company. If the rate of the commission is 5%, then the profit remaining after the commission should be Rs. 100. In such an event, the profit before the commission should be Rs. 105. In other words, commission is Rs. 5 out of every Rs. 105 profit, before the commission.

The formula to calculate the commission in such a situation is: 5/105 × Profits before the commission.

Illustration No. 9

Kalyan & Co. Agrees to pay a commission 5% on net profits to its manager. The profit before commission is Rs. 80,000. The commission has not yet been paid by the company to its manager.

Show the necessary entries in the financial Statements.

Note: The manager is entitled to a commission of 5% on net profits. So, before deducting commission, profits should be Rs. 105 to enable him to get a commission of Rs. 5. The commission will be Rs. 3,810, i.e., Rs. 80,000 × 5/105. The profit after the commission is Rs. 76,190 and Rs.3, 810 is 5% of this figure.

If the commission is calculated, directly, on Rs. 80,000, it will be wrong as the remaining profit would be Rs. 76,000 and 5% of Rs. 76,000 is not Rs. 4,000.

Meaning: - Revenue means gross inflow of cash, receivable or other consideration arising in the course of ordinary activities of an enterprise such as

a) Sale of goods.

b) Rendering of services.

c) Use of the enterprises resources by other, yielding interest, dividend and royalties.

Timing: - Revenue should be recognized at the time of sale of rendering of services.

Transaction Excluded: - AS 9 is not applicable to the following:

a) Revenue arising from construction contracts.

b) Revenue arising from hire, purchase, lease agreements.

c) Revenue arising from government grants and subsidies.

d) Revenues of insurance companies arising from insurance contracts.

Sale of Goods: - As per AS 9 revenue from sale of goods is recorded when

a) Seller has transferred the ownership of goods to the buyer for a price.

b) All significant risks and rewards of ownership have been transferred to the buyer.

c) Seller does not retain any effective control of ownership of the transferred goods.

d) There is no significant uncertainty in collection of amount of consideration.

Rendering of Services: - Revenue from service is recorded as the service is performed. It is measured by 2 methods.

a) Completer Service Contract Method: - Revenue is recorded on completion of the contract i.e. when rendering of service is complete.

b) Propionate Completion Method: - Revenue is recorded proportionately i.e. in proportion to the degree of completion of services under a contract.

Effect of Uncertainties: - Revenue is recorded only when there is no significant uncertainty in collection of amount of consideration. Revenue recognition is if the ultimate collection is uncertain.

When uncertainty of collection of revenue arises after the revenue recognition it is better to make provision for the uncertainty in collection.

Disclosure: - If revenue recognition is postponed, then the circumstances necessitating the postponement must be disclosed.

References:

- Gupta R.L. And Radhaswamy. M, Sultan chand & Sons, New Delhi.

- Shukla M. C. Grewal T. S and Gupta S.C., S. Chand & Sons. New Delhi.

- Shukla S. M., Sahitya Bhawan Publication, Agra.

- Murti Guru Prasad, Himalaya Publishing House, Mumbai.

- Jain and Narang, Kalyani Publisher, New Delhi.

- S. N. Maheswari, Vikas Publishing House, New Delhi.

- Sharma and Gupta, RBD Publishing House, Jaipur.

- Khatik S. K., Jitendra Saxena K, Extol Publication, Bhopal.

- Gangwar Sharda, Himalaya Publishing House, Agra.