UNIT IV

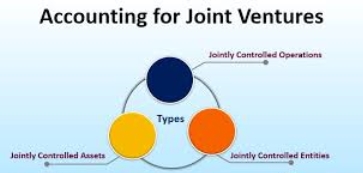

Accounting for Joint venture

|

How to explain a joint venture

The accounting for the joint venture depends on the level of control exercised on the joint venture. If a significant amount of control is made, the exemplarity method should be used. This article describes the concept of significant impact and how to use the exemplarity method to account for investments in joint ventures.

Impact of significant impact

A key factor in deciding whether to use the exemplarity method is the degree of impact investors have on the joint venture. The basic rules for managing the presence of significant influence are:

- Voting rights - If the investor and its subsidiary hold at least 20% of the voting rights in the joint venture, it is estimated that there will be a significant impact. When considering this item, consider the impact of potential voting rights currently exercisable, such as warrants, stock options and convertible bonds. This is the highest priority rule for managing the presence of significant influence.

2. Board sheet -Investors manage the seats on the board of directors of the joint venture personnel. Administrators are shared between entities.

3. Policy decision- Investors participate in the policy-making process of the joint venture. For example, investors can influence decisions about distribution to shareholders.

4. Technical guidance- Important technical information is provided by one party to the other transaction. There are important transactions between entities.

5. Unless there is clear evidence that there is no significant impact, these rules should be followed. Conversely, if voting rights are less than 20%, significant impacts can only exist if they are clearly indicated.

Despite the presence of one or more of the factors mentioned above, investors can lose significant control over the joint venture. For example, governments, regulators, or bankruptcy courts can effectively manage joint ventures, thereby eliminating what was previously a significant investor influence.

EExampleuity method

If there is a significant impact, investors will need to account for their investment in the joint venture using the eExampleuity method. In essence, the eExampleuity method reExampleuires that the initial investment be recorded at cost, after which the investment is adjusted to the actual performance of the joint venture. The following calculation shows how the eExampleuity method works.

+ Initial investment recorded at cost

Investor share of joint venture profit or loss

-Distribution received from joint venture

= End investment in joint venture

The investor's share of the joint venture's profit and loss is recorded in the investor's income statement. In addition, if the joint venture records changes in other comprehensive income, investors must also record their share of these items in other comprehensive income.

If the joint venture reports a large loss or a series of losses, recording the investor's share of these losses can significantly reduce the investor's recorded investment in the joint venture. In that case, the investor will stop using the eExampleuity method when the investment reaches zero. If the investor's investment in the joint venture has been reduced to zero, but there are other investments in the joint venture (such as loans), the investor will continue to recognize the share of the loss in the additional joint venture and other losses. Must be offset with. In the order of investments, priorities of those investments (first at offset to the most junior items). If the joint venture later begins to report profits again, investors will use the eExampleuity method until a share of the joint venture's profits offsets all losses of the joint venture that were not recognized during the period of use of the eExampleuity method. Will not resume. It was interrupted.

How to maintain a joint venture account

Method 1: If another set of books is maintained

Joint venture account

Joint venture account

Joint bank account

Method 2: If another set of books is not maintained

Case 1: When each co-venture records all transactions

Joint venture account

Coventurer account

Case 2: When each co-venture records only its own transactions

Memorandum of Understanding Joint Venture Account

Joint venture with joint venture account

METHOD 1 : WHEN SEPARATE SET OF BOOKS ARE MAINTAINED

JOURNAL ENTREIS

SL. NO | PARTICULAR’S | ENTRIE’S |

1. | When the contribution made by the co- venture’s | Joint bank account Dr. To co-ventures’ account |

2. | When the expenses paid through joint bank account | Joint venture account Dr. To joint bank account |

3. | When the expenses paid or materials supplied by the co-ventures from private Account | Joint venture account Dr. To co-venture account |

4. | When the sales proceeds or collections | Joint bank account Dr. To joint venture account |

5. | When the collections received by co- Ventures | Co-ventures account Dr. To joint venture account |

6. | When the assets taken over by the co- venture’s | Co-ventures account Dr. To joint venture account |

7. | When the liabilities taken over by the | Joint venture account Dr. |

| co-ventures | To co-venture account |

8. | When there is profit on joint venture | Joint venture account Dr. To co-venture account |

9. | When there is loss on joint venture | Co-venture account Dr. To joint venture account |

10 | When the final settlement made to co- venture’s | Co-venture account Dr. To joint bank account |

METHOD - 2

WHEN SEPARATE SET OF BOOKS ARE NOT MAINTAINED WHEN EACH CO-VENTURER KEEP RECORD OF ALL TRANSACTIONS

JOURNAL ENTRIES

SL.NO | PARTICULARS | ENTRIES |

1 | When goods supplied to joint venture form own business stock | Joint venture account Dr. To purchase account |

2 | When joint venture expenses paid | Joint venture account Dr. To cash/bank account |

3 | When the material supplied to or expenses paid for joint venture by other co-ventures | Joint venture account Dr. To co-venture’s account |

4 | When the sales made | Cash/bank account Dr. To joint venture account |

5 | When the sales made by other co- ventures | Co-venture ‘s account Dr. To joint venture account |

6 | When the venture profit | Joint venture account Dr. To profit and loss account (own share) To co-venture’s account |

7 | When the ventures loss | Profit and loss account (own share) Dr. Co-venture’s account Dr. To joint venture account |

8 | When the final settlement to co-ventures | |

B | When amount is received from co- ventures | Cash/bank account Dr. To co-venture’s account |

METHOD 3

WHEN EACH C0-VENTURER KEEP RECORD OF OWN TRANSACTIONS ONLY MEMORANDUM JOINT VENTURE ACCOUNT

JORNAL ENTRIES

SL. NO | PARTICULARS | ENTRIES |

1 | Goods supplied to joint venture form business stock | Joint venture account Dr. To purchase account |

2 | When joint venture expenses paid | Joint venture account Dr. To cash/bank account |

3 | When the sales made | Cash/bank account Dr. To joint venture account |

4 | When own share in the joint venture profit | Joint venture account Dr. Profit and loss account |

5 | When own share in the joint venture loss | Profit and loss account Dr. To joint venture account |

6 | When cash received from other co-venture | Cash/bank account Dr. To joint venture account |

7 | When cash remitted to other co- venture | Joint venture account Dr. To cash/bank account |

8 | When the final settlement | |

9 | When amount is paid to co- ventures | Joint venturers account Dr. To cash/bank account |

10 | When amount is received from co-ventures | Cash/bank account Dr. To joint venture account |

Key takeaways:

- A JV is a business agreement in which two or more parties agree to pool resources for the purpose of performing a particular task.

- They are colloExampleuially partnerships, but they can take any legal structure.

- A common use for JVs is to partner with local companies to enter foreign markets.

- A strategic joint venture is a business agreement that actively involves two companies that make collaborative decisions to work together to achieve a particular set of goals.

- Joint ventures help companies establish a foreign presence and gain a competitive advantage in a particular market.

The joint venture has helped many companies achieve access to emerging markets that are otherwise difficult to enter

MEANING:

- To consign means TO SEND

- Consignment is an AGREEMENT between two parties i.e., Consignor and Consignee, whereby Consignor agrees to send goods to consignee on regular basis for the purpose of sale in exchange of commission and reimbursement of expenses to be paid by consignor to consignee.

- The party who sends the goods is called CONSIGNOR (Principal).

- The party to whom the goods are sent is called CONSIGNEE (Agent).

- The ownership of the goods i.e., Property in goods remain with consignor. Agent does not become the owner. It means the POSSESSION of the goods is transferred but not OWNERSHIP. On sale, the buyer will become the owner.

- Principal does not send invoice to agent he only sends PROFORMA INVOICE which looks like invoice. The object of proforma invoice is to convey information to agent regarding particulars of goods sent.

- Goods are sold by consignee on behalf of consignor AT THE RISK OF CONSIGNOR. Consignee gets commission for the goods sold and he is not responsible for any Bad Debts that may arise.

- If the agent has to be made responsible for any BAD DEBTS that may arise, he is to be paid additional commission called DEL-CREDERE COMMISSION. Such commission is calculated on total sales, not only on credit sales until and unless agreed.

- Agent sends periodical statement to principal called ACCOUNT SALES. It includes information about sales made by agent, expenses incurred on behalf of principal, commission charged by agent and balance due to principal.

ACCOUNT SALES:

An Account sale is the periodical summary sent by consignee to consignor.

It contains:

a) Sales made.

b) Expenses by consignee on behalf of consignor.

c) Commission earned.

d) Unsold inventory left with consignee.

e) Advance payments if any.

f) Balance payment due or remitted

ADVANCE TO CONSIGNEE | SECURITY AGAINST CONSIGNMENT |

Advance is paid by consignee at the time of delivery of goods which is adjusted in full against amount due. | Deposit is in the form of security against goods. In case if unsold inventories are left with consignee, only proportionate security on respect of sold goods is adjusted against amount due and balance security in respect of goods unsold is carried forward. Full amount of security is not adjusted against amount due |

DIFFERENCE BETWEEN CONSIGNMENT & SALE:

CONSIGNMENT | SALE |

Ownership of the goods remains with the consignor. | Ownership of the goods transfer to buyer. |

Consignee can return unsold goods. | Goods sold can be returned only if seller agrees. |

Consignor bears the loss of goods held with consignee. | Buyer have to bear the loss if any after delivery of goods. |

Relationship between CONSIGNOR and CONSIGNEE is that of PRINCIPAL and AGENT. | Relationship between buyer and seller is that of Creditor and Debtor |

Expenses incurred by consignee to keep goods safely are borne by consignor. | Expenses by buyer to keep goods safely is borne by buyer. |

CALCULATION OF STOCK ON CONSIGNMENT

VALUE OF STOCK ON CONSIGNMENT

= Proportionate Cost of Goods + Proportionate Consignor’s Exp + Proportionate Consignee’s Non-Selling Exp.

CONSIGNEE’S EXPENSE

- NON-SELLING EXPENSES (Incurred by consignee before goods reaches at consignee’s place)

Packing, Freight, Carriage inward, Cartage, Octroi, Transit insurance.

- SELLING EXPENSES (Incurred by consignee after goods reaches at consignee’s place)

Godown rent, Godown insurance, Delivery charges, Advertisement & Other selling exp.

VALUE OF GOODS IN TRANSIT

= Proportionate Cost + Proportionate consignors Exp.

COMMISSION

NORMAL COMMISSION | OVER-RIDING COMMISSION | DEL-CREDERE COMMISSION |

Given to agent as a reward for his services. | Given to agent for selling goods over and above a targeted price. This type of commission includes agent to sell at higher selling price. | Given to agent for shifting responsibility of collection and risk too. In case if Del-Credere Commission is given, agent bears the loss of Bad Debts (if any) |

NORMAL & ABNORMAL LOSS

NORMAL LOSS

- A loss which is unavoidable and essential.

- A loss which can be anticipated well in advance

- Such loss would be spread over entire consignment. It means good units will bear the normal loss.

ABNORMAL LOSS

- A loss which is incurred over and above the normal loss.

- A loss which is avoidable.

- Such loss would not be spread over entire consignment. It means good units will not bear the abnormal loss.

ABNORMAL LOSS IN TRANSIT does not include consignee’s non-recurring exp.

ABNORMAL LOSS AT CONSIGNEES GODOWN include consignee’s non-recurring expenses.

GOODS RETURNED BT CONSIGNEE does not include consignee’s expenses.To return the goods.

JOURNAL ENTRIES IN THE BOOKS OF CONSIGNOR

GOODS SENT ON CONSIGNMENT. Consignment A/c. Dr To GSOC A/C. EXPENSES PAID BY CONSIGNOR Consignment A/c. Dr To Cash/Bank A/c. EXPENSES PAID BY CONSIGNEE Consignment A/c. Dr To Consignee A/c SALES BY CONSIGNEE Consignee A/c. Dr To Consignment A/c EXPENSES & COMMISSION BY CONSIGNEE. Consignment A/c. Dr To Consignee A/c FINAL REMITANCE RECEIVED Cash/Bank A/c. Dr To Consignee A/c

| TRANSFER OF GSOC GSOC A/c. Dr To Trading A/c. GOODS RETURNED BY CONSIGNEE GSOC A/c. Dr To Consignment A/c

ADV. RECEIVED FROM CONSIGNEE Cash/Bank/BR A/c. Dr To Consignee A/c. BR DISCOUNTED Bank A/c. Dr Discount A/c. Dr To BR A/c.

DISCOUNT CHARGED/TRF.TO CONSIGNMENT A/c. Consignment A/c. Dr To Discount A/c.

| NORMAL LOSS NO ENTRY Cost of normal units will be shifted to other Good units and finally borne by customer. ABNORMAL LOSS P&L A/c. Dr. To Consignment A/c

This loss is not shifted to good units but shifted to P&L A/c. It means it is borne by businessman In case if insurance Claim is admitted, entry for abnormal loss will appear as follows Insurance claim. Dr P&L A/c. Dr. To Consignment A/c |

GOODS SENT ON CONSIGNMENT AT INVOICE PRICE

Dr. CONSIGNMENT A/c Cr.

Particulars | Amount | Particulars | Amount |

To Opening stock | Invoice Price | By Opening Stock Reserve | LOADING |

To GSOC(Goods sent) | Invoice Price | By GSOC(Goods sent) | LOADING |

TO GSOC(Goods returned) | LOADING | BY GSOC(Goods returned) | Invoice Price |

To Closing Stock Reserve | LOADING | By Closing Stock | Invoice Price |

GOODS SENT ON CONSIGNMENT AT INVOICE PRICE Consignment A/c. Dr To GSOC A/c. | GOODS RETURNED FROM CONSIGNMENT AT INVOICE PRICE GSOC A/c. Dr To Consignment A/c. |

LOADING ON GOODS SENT ON CONSIGNMENT AT INVOICE PRICE GSOC A/c. Dr To Consignment A/c. | LOADING ON GOODS RETURNED FROM CONSIGNMENT AT INVOICE PRICE Consignment A/c. Dr To GSOC A/c. |

JOURNAL OF CONSIGNEE

GOODS RECEIVED ON CONSIGNMENT.

NO ENTRY

EXPENSE PAID BY CONSIGNOR

NO ENTRY

EXPENSES PAID BY CONSIGNEE.

Consignor A/c. Dr

To Cash/Bank A/c.

CASH SALES MADE BY CONSIGNEE.

Cash/Bank A/c. Dr

To Consignor A/c.

CREDIT SALES MADE BY CONSIGNEE.

Consignment Debtor A/c. Dr

To Consignor A/c.

COLLECTION FROM CONSIGNMENT DEBTOR.

Cash/Bank A/c. Dr

To Consignment Debtors A/c.

COMMISSION CHARGED.

Consignor A/c. Dr

To Commission / Del-credere commission A/c

AMOUNT PAID TO CONSIGNOR.

(advance or final remittance)

Consignor A/c. Dr

To Cash / Bank / BP A/c

BAD DEBTS

(a) If Del-Credere Commission is charged

Del-Credere A/c. Dr.

To Consignment Debtors A/c

(b) If Del-Credere Commission is NOT charged

Consignor A/c. Dr.

To Consignment Debtors A/c.

2.4. SOLVED EXAMPLES:

Example.1). RAWAL RATAN SINGH of Chittorgarh consigned 1000 units of 100 each to RANI PADMAVATI of SINGHAL. Expense made by RAWAL RATAN SINGH in such consignment are Rs. 20,000.

RANI PADMAVATI paid unloading charges Rs. 5,000 and Rs.2 P.U. selling expenses.

She sold all the goods at Rs.140 each and deducted 5% as commission and remitted draft for the balance. Prepare Ledger accounts in the books of Consignor.

SOLUTION: -

Ledger of Rawal Ratan Singh(Consignor)

Dr. CONSIGNMENT A/c Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To Goods sent on Consignment (1000 X 100) | 1,00,000 | By Padmavati (Sales-1000 X 140) | 1,40,000 |

T0 Cash (1000 X 20) | 20,000 |

|

|

To Padmavati Non selling exp (1,000 X 5) Selling exp (1,000 X 2) |

5,000 2,000 |

|

|

To Padmavati (Comm-1,40,000 X 5%) | 7,000 |

|

|

To P&L (Bal.Fig) | 6,000 |

|

|

|

|

|

|

TOTAL | 1,40,000 | TOTAL | 1,40,000 |

Dr. PADMAVATI A/c Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To Consignment | 1,40,000 | By Consignment | 6,600 |

|

| By Consignment | 5,600 |

|

| By Bank (Bal.Fig) | 1,27,800 |

|

|

|

|

TOTAL | 1,40,000 | TOTAL | 1,40,000 |

Dr. Goods Sent On Consignment A/c Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

|

| By Consignment | 1,00,000 |

To Trading (transfer) | 1,00,000 |

|

|

TOTAL | 1,00,000 | TOTAL | 1,00,000 |

EXAMPLE.2. On 15 Jan, 2013 J&K Co. of Mumbai sent to Muku & Co. of Kolkata 400 bicycle at an invoice price of Rs.100 per bicycle to be sold on commission. Freight and insurance were Rs.600.

Accounts sale was received from consignee as follow: -

15 March - 100 per bicycle were sold @ Rs.145 on which 5%. Commission and Rs.375 for expenses were deducted.

10 April - 150 per bicycle were sold @ Rs.140 on which 5%. Commission and Rs.290 for expenses were deducted.

From the above information prepare Consignment A/c in the books of J&K Co. and close it on 30 April, 2013 keeping in mind that no salves were made afterwards. Also show accounts in the books of Muku & Co.

Solution: -

Ledger of J&K CO. (Consignor)

Dr. CONSIGNMENT A/c Cr.

DATE | PARTICULAR | AMOUNT | DATE | PARTICULAR | AMOUNT |

2013 |

|

| 2013 |

|

|

Jan 15 | To GSOC | 40,000 | Mar. 15 | By Muku (sales) | 14,500 |

Jan 15 | To Cash/Bank (J&K exp.) | 600 | Apr. 10 | By Muku (sales) | 21,000 |

Mar. 15 | To Muku (exp.) | 375 | Apr. 30 | By Stock on Consignment | 15,225 |

Mar. 15 | To Muku (commission) | 725 |

|

|

|

Apr. 10 | To Muku (exp.) | 290 |

|

|

|

Apr. 10 | To Muku (commission) | 1,050 |

|

|

|

Apr. 30 | To P&L (Bal. Fig.) | 7,685 |

|

|

|

|

|

|

|

|

|

| TOTAL | 50,725 |

| TOTAL | 50,725 |

Dr. MUKU’s A/c (Consignee) Cr.

DATE | PARTICULAR | AMOUNT | DATE | PARTICULAR | AMOUNT |

2013 |

|

| 2013 |

|

|

Mar. 15 | To Consignment (Sales) | 14,500 | Mar. 15 | By Consignment (expense) | 375 |

Apr. 10 | To Consignment (Sales) | 21,000 | Mar. 15 | By Consignment (Commission) | 725 |

|

|

| Apr. 10 | By Consignment (expense) | 290 |

|

|

| Apr. 10 | By Consignment (Commission) | 1,050 |

|

|

| Apr. 30 | By Balance c/d | 33,060 |

| TOTAL | 35,500 |

| TOTAL | 35,500 |

Dr. Goods sent on Consignment A/c Cr.

DATE | PARTICULAR | AMOUNT | DATE | PARTICULAR | AMOUNT |

2013 |

|

|

| 2013 |

|

Apr. 30 | To Trading A/c (transfer) | 40,000 | Jan. 15 | By Consignment | 40,000 |

|

|

|

|

|

|

| TOTAL | 40,000 |

| TOTAL | 40,000 |

LEDGER OF MUKU & CO. (Consignee)

Dr. J&K Co. A/c Cr.

DATE | PARTICULAR | AMOUNT | DATE | PARTICULAR | AMOUNT |

2013 |

|

| 2013 |

|

|

Mar. 15 | To Cash/Bank (expense) | 375 | Mar. 15 | By Cash/Bank (Sales) | 14,500 |

Mar.15 | To Commission | 725 | Apr. 10 | By Cash/Bank (Sales) | 21,000 |

Apr. 10 | To Cash /Bank (expense) | 290 |

|

|

|

Apr. 10 | To Commission | 1,050 |

|

|

|

Apr. 30 | To Balance c/d | 33,060 |

|

|

|

|

|

|

|

|

|

| TOTAL | 34,500 |

| TOTAL | 34,500 |

Dr. COMMISSION A /c Cr.

DATE | PARTICULAR | AMOUNT | DATE | PARTICULAR | AMOUNT |

2013 |

|

| 2013 |

|

|

Apr. 30 | To P&L (Bal.Tfd.) | 1,775 | Mar.15 | By J&K (14,500 X 5%) | 725 |

|

|

| Apr. 10 | By J&K (21,000 X 5%) | 1,050 |

|

|

|

|

|

|

| TOTAL | 34,500 |

| TOTAL | 34,500 |

Working note: -

Closing Stock

Cost of Goods Sent.

- EXAMPLEuantity sent 400

Cost of Goods (400 X 100) 40,000

Add: - J&K Co. Expense 600

b) Total Cost 40,600

c) EXAMPLEuantity Sold 250

d) EXAMPLEuantity in stock 150

e) Closing Stock - Cost

= Total Cost X EXAMPLEuantity in Stock / EXAMPLEuantity Sent

= 40,600 X 150/400

= 15,225

Note: - It is assumed that the consignee's expenses are incurred after the goods have reached their godown and hence not included in valuation of stock.

EXAMPLE.3. On 1st November,2015, A of Calcutta sends goods costing Rs.1,00,000 to B of Delhi on Consignment basis. A paid Rs. 5,000 as freight and Rs. 2,000 as insurance.

On 31st December,2015, an Account Sales was received from B disclosing that the entire Exampleuantity of goods were sold for Rs.1,50,000 out of which Rs. 30,000 was sold on credit A customer who purchased goods for Rs. 5,000 failed to pay and the debt proved bad. All other debts were collected by B in full. As per the agreement, B is allowed a commission @ 10% on sales. B sends the amount due to A by cheExampleue.

Prepare necessary Ledger accounts in the books of A & B.

Solution: -

LEDGER OF A

Dr. CONSIGNMENT A/c Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To Goods sent on Consignment | 1,00,000 | By B’s (Cash sales) | 1,20,000 |

To Cash/Bank Freight. 5,000 Insurance. 2000 | 7,000 | By B’s (Cr. Sales) | 30,000 |

To B's (commission) (10% of 1,50,000) | 15,000 |

|

|

To B's A/c (Bad debt) | 5,000 |

|

|

To P&L A/c (bal.fig.) | 23,000 |

|

|

|

|

|

|

TOTAL | 1,50,000 | TOTAL | 1,50,000 |

Dr. B's A/c. Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To Consignment (Cash sales) | 1,20,000 | By Consignment (commission) | 15,000 |

To Consignment (Cr. Sales) | 30,000 | By Consignment (bad debts) | 5,000 |

|

| By Bank A/c (Remittance) | 1,30,000 |

|

|

|

|

TOTAL | 1,50,000 | TOTAL | 1,50,000 |

Dr. Goods sent on Consignment A/c. Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To Trading A/c (transfer) | 1,00,000 | By Consignment A/c | 1,00,000 |

TOTAL | 1,00,000 | TOTAL | 1,00,000 |

LEDGER OF B

Dr. A's A/c. Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To Commission | 15,000 | By Cash/ Bank (Sales) | 1,20,000 |

To Consignment Debtors (Bad debts- no del credere comm) | 5,000 | By Consignment Debtors (Cr. Sales) | 30,000 |

To Cash/Bank (Remittance) | 1,30,000 |

|

|

TOTAL | 1,50,000 | TOTAL | 1,50,000 |

Dr. CONSIGNMENT DEBTORS A/c Cr.

PARTICULAR | AMOUNT | PARTICULAR | AMOUNT |

To A's | 30,000 | By Cash/Bank (collection) | 25,000 |

|

| By A's (Bad debts no del cr. commission) | 5,000 |

TOTAL | 30,000 | TOTAL | 30,000 |

EXAMPLE.4 Refer to Exampleuestion 3. Prepare the necessary ledger account, if in the above Exampleuestion the consignee is given a del credere commission of 5% on sales (In addition to ordinary commission)—other things remaining the same.

SOLUTION: -

LEDGER OF A

Dr. CONSIGNMENT A/c. Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To GSOC | 1,00,000 | By B’s (Cash sales) | 1,20,000 |

To Cash/Bank Freight. 5,000 Insurance 2000 | 7,000 | By B's (Cr. Sales) | 30,000 |

To B's (commission) (10% of 1,50,000) | 15,000 |

|

|

To B's (Del-Credere Commission) | 7,500 |

|

|

To P&L (bal.fig.) | 23,000 |

|

|

TOTAL | 1,50,000 | TOTAL | 1,50,000 |

Dr. B's A/c. Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To Consignment (Cash sales) | 1,20,000 | By Consignment (commission) | 15,000 |

To Consignment (Cr. Sales) | 30,000 | By Consignment (Del-cr. commission) | 7,500 |

|

| By Cash/Bank(Remittance) | 1,27,500 |

TOTAL | 1,50,000 | TOTAL | 1,50,000 |

Dr. Goods sent on Consignment A/c Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To Trading A/c (transfer) | 1,00,000 | By Consignment A/c | 1,00,000 |

TOTAL | 1,00,000 | TOTAL | 1,00,000 |

LEDGER OF B

Dr. A's A/c. Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To commission | 15,000 | By Cash/ Bank (Sales) | 1,20,000 |

To Del credere commission | 7,500 | By Consignment Debtors (Cr. Sales) | 30,000 |

To Cash/Bank (Remittance) | 1,27,500 |

|

|

TOTAL | 1,50,000 | TOTAL | 1,50,000 |

Dr. CONSIGNMENT DEBTORS A/c Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To A's | 30,000 | By Cash/Bank (collection) | 25,000 |

|

| By A's (Bad debts Adjusted) | 5,000 |

TOTAL | 30,000 | TOTAL | 30,000 |

Dr. Del Credere Commission A/c Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To Consignment Debtors (Bad Debts) | 5,000 | By A's | 7,500 |

To P&L (Bal. Fig) | 2,500 |

|

|

TOTAL | 7,500 | TOTAL | 7,500 |

Dr. COMMISSION A/c Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To P&L (Bal. Fig) | 15,000 | By A's | 15,000 |

TOTAL | 15,000 | TOTAL | 15,000 |

Dr. PROFIT & LOSS ACCOUNT Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To Profit c/d to B/S | 17,500 | By Commission | 15,000 |

|

| By Del Credere Commission (Net trfd.) | 2,500 |

TOTAL | 17,500 | TOTAL | 17,500 |

EXAMPLE.5. Amit of Mumbai consigned 100 sewing machines to Sanjay of Surat to be sold on his risk. The cost of one machine was Rs.150, but the invoice price was Rs.200. Amit paid freight Rs. 600 and insurance in transit Rs.200

Sanjay sent a draft to Amit for Rs. 10,000 as advance and later sent an account sales showing that 80 machine were sold at Rs.220 each. Expenses incurred by Sanjay were carriage inward Rs. 25, Octroi Rs.75, godown rent Rs.500 and advertisement Rs.300. Sanjay is entitled to a commission of 5% on sales.

Journalise the above transaction in the books of Amit and Sanjay.

SOLUTION: -

LEDGER OF AMIT

Dr. CONSIGNMENT A/c Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To GSOC | 20,000 | By Sanjay (Sales) | 17,600 |

To Cash/Bank (Amit expenses) | 800 | By Stock on Consignment | 4,180 |

To Sanjay (Expenses) | 900 | By GSOC (Load) | 5,000 |

To Sanjay (Commission) | 880 |

|

|

To Stock Reserve c/d | 1,000 |

|

|

To P&L(bal.fig.) | 3,200 |

|

|

TOTAL | 26,780 | TOTAL | 26,780 |

Dr. SANJAY A/c. Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To Consignment (Cash Sales) | 17,600 | By Cash/ Bank (Advance) | 10,000 |

|

| By Consignment (Expenses) | 900 |

|

| By Consignment (Commission) | 880 |

|

| By Balance c/d | 5,820 |

TOTAL | 17,600 | TOTAL | 17,600 |

Dr. Goods sent on Consignment A/c Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To Consignment | 5,000 | By Consignment A/c | 20,000 |

To Trading A/c (transfer) | 15,000 |

|

|

TOTAL | 20,000 | TOTAL | 20,000 |

LEDGER OF SANJAY

Dr. AMIT A/c Cr.

PARTICULAR | AMOUNT | PARTICULAR | AMOUNT |

To Cash/ Bank (Advance) | 10,000 | By Cash/ Bank | 17,600 |

To Cash/ Bank (Expenses) | 900 |

|

|

To Commission | 880 |

|

|

To Balance c/d | 5,820 |

|

|

TOTAL | 17,600 | TOTAL | 17,600 |

EXAMPLE.6. On 1st July,2016, Rustom House of Ahmedabad consigned 100 keyboards to TCS of Mumbai. The cost of each keyboard was Rs.450 but the pro forma invoice price was Rs.600. Rustom House paid Rs.3000 for freight and insurance. On 7th July,2016, TCS accepted a 3 months’ bill drawn upon them by Rustom House for Rs. 30,000. TCS paid Rs. 1,200 as rent and Rs.750 for advertisement and up to 31st December,2016(On which Rustom House closes their books) they sold 80 keyboards @ 615 each. TCS were entitled to a commission of 5% on sales.

Show the ledger accounts recording the above transaction in the books of Rustom House and TCS

SOLUTION: -

LEDGER OF Rustom House

Dr. CONSIGNMENT A/c Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To GSOC | 60,000 | By TCS (Sales) | 49,200 |

To Cash/Bank (Rustom House expenses) | 3,000 | By Stock on Consignment | 12,600 |

To TCS (Expenses) | 1,950 | By GSOC (Load) | 15,000 |

To TCS (Commission) (49,200 X 5%) | 2,460 |

|

|

To Stock Reserve (Load) | 3,000 |

|

|

To P&L(bal.fig.) | 6,390 |

|

|

TOTAL | 17,600 | TOTAL | 17,600 |

Dr. TCS A/c Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To Consignment (Cash Sales) | 49,200 | By Bills Receivable (Advance) | 30,000 |

|

| By Consignment (Expenses) | 1,950 |

|

| By Consignment (Commission) | 2,460 |

|

| By Balance c/d | 14,790 |

TOTAL | 49,200 | TOTAL | 49,200 |

Dr. Goods sent on Consignment A/c Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To Trading A/c (transfer) | 45,000 | By Consignment A/c | 60,000 |

To Consignment | 15,000 |

|

|

TOTAL | 60,000 | TOTAL | 60,000 |

LEDGER OF TCS

Dr. Rustom House A/c Cr.

PARTICULARS | AMOUNT | PARTICULARS | AMOUNT |

To Bills Payable (Advance) | 30,000 | By Cash/ Bank(Sales) | 49,200 |

To Cash/ Bank (Expenses) | 1,950 |

|

|

To Commission | 2,460 |

|

|

To Balance c/d | 14,790 |

|

|

TOTAL | 49,200 | TOTAL | 49,200 |

EXAMPLE.7. D. Dogra of Delhi sent to his agent, M. Monga of Madras, 500 articles costing Rs.15/- per article at an invoice price of Rs.20 per article. The following payments were made by D. Dogra in this connection: freight and carriage Rs. 450, miscellaneous exp. Rs. 50. M. Monga sent a bank draft for Rs. 3,000 as an advance against the Consignment M. Monga sold 300 articles at a flat rate of Rs.28 per article and sent an Account Sales showing deduction for storage charges Rs.550 insurance Rs.550 and his Commission of 3% plus 2% Del Credere on gross sale proceeds, and remitted the amount due on consignment. M. Monga also informed D. Dogra that 50 articles were damaged in transit and thus they were valued at Rs.550. Journalize the above transactions in the books of the consignor and consignee.

SOLUTION: -

Books of Dogra (Consignor)

Journal

|

|

|

| Dr. | Cr. |

|

| Rs. | Rs. | ||

(1) | Consignment to madras A/c Dr | 7,500 |

| ||

| To Goods sent on Consignment A/c |

| 7,500 | ||

(500 articles sent to M. Monga, Agent, Cost being Rs.15 per article). | |||||

(2) | Consignment to Madras A/c Dr | 500 |

| ||

| To Bank Account |

| 500 | ||

(Expenses incurred on the Consignment) | |||||

| Freight & Carriage | Rs. | 450 |

|

|

| Miscellaneous Exp. | Rs. | 50 |

|

|

|

|

| 500 |

|

|

(3) | Bank Account Dr | 3,000 |

| ||

| To M. Monga |

| 3,000 | ||

(Advance received from the Agent in the form of Bank Draft.) | |||||

(4) | M. Monga Dr | 8,400 |

| ||

| To Consignment to Madras A/c |

| 8,400 | ||

(Sales affected by M. Monga as per Account Sales.) | |||||

(5) | Consignment to Madras A/c Dr | 570 |

| ||

| To M. Monga |

| 570 | ||

(Expenses incurred by M. Monga Rs.150 and Commission due to him, Rs.550 (5% of Rs. 8,400). | |||||

(6) | Bank Account Dr | 4,830 |

| ||

| To M. Monga |

| 4,830 | ||

(Amount due from the consignee received.) | |||||

(7) | P & Loss A/c Dr | 350 |

| ||

| To Consignment to Madras A/c |

| 350 | ||

(Abnormal Loss on 50 damaged Articles) | |||||

(8) | Stock on Consignment A/c Dr | 2,850 |

| ||

| To Consignment to Madras A/c |

| 2,850 | ||

| (Value of stock unsold at Madras) |

| Rs. |

|

|

| 150, goods articles, @ Rs.20 |

| 2,250 |

|

|

| Add: Expenses Rs.150 |

| 150 |

|

|

| 50 damaged articles |

| 450 |

|

|

|

|

| 2,850 |

|

|

(9) | Consignment to Madras A/c Dr | 3,030 |

| ||

| To Profit & Loss Account |

| 3,030 | ||

(Profit on consignment transferred to Profit & Loss Account) | |||||

(10) | Goods sent on Consignment A/c | 7,500 |

| ||

| To Trading A/c |

| 7,500 | ||

(Goods sent on consignment A/c closed by transfer to trading Account) | |||||

Books of M. Monga (Consignee)

Journal

|

|

|

| Dr. | Cr. |

|

| Rs. | Rs. | ||

(1) | D.Dogra A/c Dr | 3,000 |

| ||

| To Bank A/c |

| 3,000 | ||

(Advance sent to the Consignor against consignment) | |||||

(2) | D. Dogra A/c Dr | 150 |

| ||

| To Bank A/c |

| 150 | ||

(Expenses incurred on the Consignment on behalf of D. Dogra | |||||

| Storage |

| 50 |

|

|

| Insurance |

| 100 |

|

|

|

|

| 150 |

|

|

(3) | Bank A/c Dr | 8,400 |

| ||

| To D. Dogra A/c |

| 8,400 | ||

(Sale of 300 articles @ Rs.28 each out of the Consignment.) | |||||

(4) | D. Dogra A/c Dr | 420 |

| ||

| To Commission A/c |

| 420 | ||

(5% Commission on Sales made on half of D. Dogra; 3% Commission + 2% Del Credere) | |||||

(5) | D. Dogra A/c Dr | 4,830 |

| ||

| To Bank A/c |

| 4,830 | ||

(Amount due to D. Dogra remitted). | |||||

EXAMPLE.8. Philips Radio of Calcutta dispatched 1,000 transistors at Rs.700 each to Mohan Bros. of Delhi, the consignors paid freight Rs.7,500, cartage Rs.500 and insurance Rs.2,500 Mohan Bros. received only 900 sets and incurred he following expenses.

Rs.

Octroi and other Expenses 1,00,000

Cartage 5,000

Sales expenses 6,000

The consignee sold 600 sets only. You are reExampleuired to calculate the value of closing stock.

SOLUTION: -

Calculation of value of unsold stock

Particulars | Units |

Sets Received | 900 |

Sets Sold | 300 |

Unsold Stock | 600 |

Particulars | Rs. |

Cost of Unsold Stock (300 x 700) | 2,10,000 |

Add: Proportionate expenses of Consignor (7500 + 500 + 2500) x 300/1000 | 3,150 |

Add: Proportionate expenses of Consignee (Octroi & Cartage) (1,00,000 + 5000) x 300/900 | 35,000 |

| 2,48,150 |

EXAMPLE.9. Deepak sold goods on behalf of Geep Sales Corporation on consignment basis. On 1 January 2002 he had with him a stock of Rs.20,000 on consignment. During the year he received goods worth Rs.2,00,000.

Deepak had instructions to sell goods at cost plus 25% and was entitled to a commission of 4% on sales in addition to 1% del credere commission.

During the year ended 31 December 2002 cash sales were Rs.1,20,000; credit sales Rs.1,05,000; Deepak’s expenses relating to consignment Rs.3,000 being salaries and insurance bad debts amounted to Rs.3,000.

Prepare necessary accounts in the books of Geep Sales Corporation.

SOLUTION: -

Solution : |

|

|

|

In the books of Geep Sales Corporation | |||

Consignment Account | |||

Dr. |

|

| Cr. |

| Rs. |

| Rs. |

To Consignment Stock b/d | 20,000 | By Deepak |

|

To Goods sent on Consignment Account | 2,00,000 | Cash Sales 1,20,000 |

|

To Deepak (Commission) | 9,000 | Credit Sales 1,05,000 | 2,25,000 |

To Deepak (Commission) | 2,250 | By Consignment Stock c/d | 40,000 |

To Deepak (expenses) | 3,000 |

|

|

To Profit & Loss Account |

|

|

|

(Profit) | 30,750 |

|

|

| 2,65,000 |

| 2,65,000 |

Deepak’s Account | |||

Dr. |

|

| Cr. |

| Rs. |

| Rs. |

To Consignment account (Sales) | 2,25,000 | By Consignment account |

|

|

| (Commission) | 9,000 |

|

| By Consignment Account |

|

|

| (Commission) | 2,250 |

|

| By Consignment Account |

|

|

| (Exp.) | 3,000 |

|

| By Balance c/d | 2,10,750 |

| 2,25,000 |

| 2,25,000 |

Working Notes:

(1) Calculation of Consignment Stock Sale Price = 100 + 25 = 125

Cost of Sales = Sales × 100/125

= 2,25,000 × 100/125

= Rs.1,80,000

Cost of the goods available for sale = Rs. 20,000 + Rs. 2,00,000 = Rs.2,20,000. Hence stock at the end = Rs. 2,20,000 - Rs. 1,80,000 = Rs. 40,000

(2) Since Deepak is paid del-credere commission, bad debts of Rs. 3,000 would be borne by him.

EXAMPLE.10. S of Bombay consigned 10,000 kg. of oil to D of Calcutta. The cost of oil was Rs.2 per kg. S paid Rs. 5,000 as freight and insurance. During transit 250 kg were accidentally destroyed for which the insurers paid directly to the consignors Rs.450 if full settlement of the claim.

D reported that 7,500 kg were sold @ Rs.3 per kg. The expenses being on godown rent Rs. 200 on advertisement Rs. 1,000 and on salesman salary Rs. 2,000 D. is entitled to a commission of 3% plus 1.5% del credere. D reported a loss of 100 kg. due to leakage. D. settled the accounts by bank draft. Prepare the accounts is the books of S.

SOLUTION: -

Consignment to Calcutta A/c | |||||

Dr. |

|

|

|

| Cr. |

|

| Rs. |

|

| Rs. |

To Goods on Consignment A/c |

| 20,000 | By Bank (Ins. Co.) |

| 450 |

To Bank—Freight & Insurance |

| 5,000 | By P & L A/c (abnormal loss |

| 175 |

To D—Expenses |

| 3,200 | By D— (Sale proceeds) |

| 22,500 |

To D—Commission |

|

|

|

|

|

Ordinary 3% | 675 |

| By Consignment Stock A/c |

| 5,431 |

Del Credere 1.5% | 338 | 1,013 | By P & L A/c—Loss |

| 657 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| 29,213 |

|

| 29,213 |

Goods Sent on Consignment A/c | |||||

Dr. |

|

|

|

| Cr. |

|

| Rs. |

|

| Rs. |

To Trading A/c |

| 20,000 | By Consignment to Calcutta A/c |

| 20,000 |

Consignment Stock A/c | |||||

Dr. |

|

|

|

| Cr. |

|

| Rs. |

|

| Rs. |

To Consignment Calcutta A/c |

| 5,431 | By Balance c/d |

| 5,431 |

D’s A/c | |||||

Dr. |

|

|

|

| Cr. |

|

| Rs. |

|

| Rs. |

To Consignment to Calcutta A/c |

|

| By Consignment to Calcutta A/c |

|

|

—(sale proceeds) |

| 22,500 | (Exp.) |

| 3,200 |

|

|

| By Consignment to Calcutta A/c |

|

|

|

|

| (commission) |

| 1,013 |

|

|

| By Bank |

| 18,287 |

|

| 22,500 |

|

| 22,500 |

Working Notes: |

|

|

|

|

|

(A) Cost of Goods destroyed |

|

| Rs. |

|

|

Cost of 10,000 kg.@Rs.2 |

|

| 20,000 |

|

|

Freight |

|

| 5,000 |

|

|

Total cost of 10,000 kg. |

|

| 25,000 |

|

|

|

|

|

|

|

|

(B) Value of Stock still unsold |

|

|

|

|

|

EXAMPLEuantity received by D (Excluding accidental loss) | 9,750 |

|

| ||

Less: Normal Leakage |

|

| (100) |

|

|

|

|

| 9,650 |

|

|

Cost of 9,650 kgs (25,000-625) | Rs. 24,375 |

|

| ||

Cost of 2,150 kgs (24,375 / 9650 x 2150) |

|

| Rs. 5,431 |

|

|

|

|

|

|

|

|

Royalty

Royalty is the consideration received by an entity or individual who sells and uses the work to a third party. Loyalty is usually considered synonymous with rent, but its concept and use are completely different.

However, the user of the property pays the owner for the use of the owner's property, both when acExampleuiring a rental property or a book for publication. However, the usage fee is different from the rent paid by the user.

When rent is paid to use tangible assets such as buildings and machines, royalties are paid to use intangible assets or to take advantage of special rights such as patents, copyrights and mines.

In addition, the amount of rent paid by the user is fixed. On the other hand, the royalties that users pay to their owners depend on the Exampleuantity of goods produced or sold.

This article describes loyalty accounting, key terms related to royalties in final accounts, the treatment of loyalty accounting, and the types of royalties in accounting.

Meaning of royalties in accounting

Royalty is nothing more than a user of an asset paying the owner or creator of such an asset on a regular basis for its use. In other words, the owner / author of an asset such as mine, a patent, a book, a work of art, etc. may allow a third party, such as a licensee, publisher, to use the creation in exchange for consideration. ..

Therefore, such payments made by the user to the owner are known as royalties. In addition, the consideration paid instead of using the owner's assets is determined by the number of items produced or sold.

Royalty accounting parties

- Lender

A person who creates or owns an asset and provides a third party with the right to use such asset is called a lessor or landlord. In addition, the lessor receives compensation from a third party for using the right to use his property.

Examples of lenders include mine or Exampleuarry owners, book authors, artists in the case of musical works, and so on.

2. Borrower

A lessee is a person who uses the property of the creator or owner instead of the consideration for using such property. Examples of borrowers include publishers, miners, and so on.

3. Account loyalty type

There are the following types of usage fees for accounting. These include:

4. Copyright

Copyright provides the creator or owner of assets such as books, artwork, and musical works with the right to claim royalties from publishers. Therefore, the publisher pays the author a copyright royalty based on the publisher's sales.

5. Patent royalties

The royalties are paid by the user to the owner based on the number of items produced.

6. Mining royalties

For mining royalties, the user or borrower pays royalties to the owner or lessor based on the output generated.

Therefore, in the case of patents or copyrights, the publisher pays royalties to the author based on the number of copies of the book sold. In other words, the patent or copyright owner receives royalties based on the number of items sold by the user.

In the mining industry, on the other hand, royalties are received by the mine owner based on the number of items the user produces.

An important term for Royalty accounting

Minimum rent

As mentioned above, the lessor contacts or agrees with the lessee on the payment of royalties. This royalty is based on the number of merchandises produced or the Exampleuantity of merchandise sold.

Currently, the number of products produced or sold may be zero or relatively small. In such cases, the lessor will receive no or little royalty that directly affects the lessor's royalty income. In other words, if there is no or little production or sale, the lessor will suffer a loss because the amount of royalties received from the lessee is no or less. This is despite the lessee using the asset.

To relieve this situation, the lessor reExampleuires the minimum amount to be paid by the lessee, regardless of the number of goods the lessee has produced or sold.

That is, the borrower must pay the lender a minimum amount. This is despite the fact that the actual royalty amount calculated based on the items produced or sold is less than the minimum rent paid.

Such a guaranteed minimum amount that the lessor receives is called the minimum rent. The minimum rent is set when the lessor signs a contract with the lessee.

This is the period included in the contract for the benefit of the landlord to guarantee the minimum rent even when sales and production are low. Therefore, the lessee pays the minimum rent or the actual royalty amount, whichever is higher.

The minimum rent paid is fixed and is also known as fixed rent or dead rent. However, this may vary depending on the terms and conditions of the agreement.

Example

For example, mine A produces 4,000 tonnes. The royalty paid by the borrower is 100 rupees per ton and the minimum contract rent is 5 rupees.

The actual royalty paid for each production is 4 rupees. The actual royalty amount is less than the minimum rent, so the lessee must pay the lessor a minimum rent of 5 rupees.

Short work or redeemable dead rent

Short-term work is nothing more than a minimum rent that exceeds actual royalties. In other words, short-term work is the difference between minimum rent and actual royalties.

In the above example, Short Workings would be Rs1 Lakh (5 Lakh – 4 Lakh). It should be noted that short-term work will only be revealed if the minimum rent clause is included in the contract.

Excessive work

Overwork is nothing more than an amount of actual royalties that exceeds the minimum rent.

For example, in the above example, the output produced is 6000 tonnes. Therefore, overwork is Rs 2 Lakhs (6 Lakh – 4 Lakh).

Recovery of short work

Contracts between lessors and lessees under royalty accounting typically provide for provisions. This provision allows you to carry forward a short task to adjust the same thing in the future.

Therefore, in the following year, Short Workings will be adjusted for excess royalties. Such a process of adjusting short-term working capital is known as short-term working capital recovery.

In other words, the royalty contract collection clause provides the borrower with the right to recover any excess payments the borrower has made to the lessor in order to comply with the minimum rent clause of the previous year.

In addition, the contract has a fixed term. Such a period defines the number of years a lessee can recover or recover short-term work. This period may be fixed or variable.

If the lessee fails to recover the short-term work within the specified time, the short-term work will expire and will be debited on the income statement for the period in which the collection has elapsed.

Fixed right

Fixed rights mean that the lessee can recover short-term work from the lessor within a certain period of time from the date of lease of the asset.

For example, according to fixed rights, lessees can recover short-term work within two years of the lease date. If he does not, the recovery will expire or end.

Fluctuating rights

Under variable rights, the lessee can recover short-term work for any period during the subseExampleuent one or more periods. For example, the short work of the previous year can be recovered in the next year.

Strikes and lockouts

Strikes and lockouts may occur during the loyalty contract period. Therefore, loyalty contracts can provide for a proportional reduction in minimum rent in the event of a strike or lockout.

Royalty accounting

There are three types of situations in which both the lender and the borrower need to pass journals. Let's use an example to understand royalty accounting.

Royalty accounting example

Zen is the owner of Minea A in Gujarat. He has a royalty agreement with Kapoor Ltd. According to the contract, the minimum rent is Rs 5,00,000 and the royalty paid is Rs 100 per ton of monthly production. The output for the different years is:

2017 – 4000 tons

2018 – 5000 tons

2019 – 6000 tons

1. Royalty accounting journals in the debt book

Case I: When the minimum rent exceeds the actual royalty amount (2017)

1. Royalty date

Loyalty A / c Dr 4,00,000

Short Working A / c Dr 1,00,000

To Zen A / c 5,00,000

(Zen royalty and short-term work)

2. Entry to make payment

Zen A / c Dr 5,00,000

To cash / bank A / c 5,00,000

(Paid to Zen in cash)

3. Year-end closing entry

P & L A / c Dr 5,00,000

Royalty A / c to 5,000,000

(Royalty transferred to P & L A / c)

Case II: If the minimum rent is eExampleual to the actual royalty amount (2018)

1. Royalty date

Loyalty A / c Dr 5,00,000

To Zen A / c 5,00,000

(Being a Zen royal family)

2. Entry to make payment

Zen A / c Dr 5,00,000

To cash / bank A / c 5,00,000

(Paid to Zen in cash)

3. Year-end closing entry

P & L A / c Dr 5,00,000

Royalty A / c to 5,000,000

(Royalty transferred to P & L A / c)

Case III: When the actual royalty amount exceeds the minimum rent and short-term work is recovered (2019)

1. Royalty date

Loyalty A / c Dr 6,00,000

To Zen A / c 6,00,000

(Being a Zen royal family)

2. Entry to pay and get back work in a short period of time

Zen A / c Dr 6,00,000

To cash / bank A / c 5,00,000

Short-time work A / c To 1,00,000

(Paid to Zen in cash, Short Working Recouped)

3. Close the entry at the end of the year and do not get back to work in a short period of time

P & L A / c Dr 6,00,000

Royalty A / c to 5,000,000

Short-time work A / c To 1,00,000

(Loyalty and short-term work will be transferred to P & L A / c)

According to the terms and conditions, short working can be collected in the year when the actual royalty exceeds the minimum rent. If the lessee fails to recover short-term work for a certain period of time, it will be irrevocable and will be charged to profit or loss in the year the short-term work recovery expires.

On the other hand, recoverable short-term work must be carried forward and displayed as current assets on the balance sheet.

2. Loyalty accounting journals in the lessor's books

Case I: When the minimum rent exceeds the actual royalty amount (2017)

1. Royalty date

Kapoor Ltd 5,00,000

To loyalty A / c4,00,000

Short working A / c 1,00,000

(Royalty received from Kapoor Ltd and short-term work)

2. Entry to make payment

Cash / Bank A / c Dr 5,00,000

To Kapoor Ltd 5,000,000

(Receiving cash from Kapoor Ltd)

3. Year-end closing entry

Royalty A / c Dr 5,00,000

To P & L A / c 5,000,000

(Loyalty credit to P & L A / c)

Case II: If the minimum rent is eExampleual to the actual royalty amount (2018)

1. Royalty date

Kapoor Ltd 5,00,000

To loyalty A / c5,00,000

(Received royalties from Kapoor Ltd)

2. Entry to make payment

Cash / Bank A / c Dr 5,00,000

To Kapoor Ltd 5,000,000

(Receiving cash from Kapoor Ltd)

3. Year-end closing entry

Royalty A / c Dr 5,00,000

To P & L A / c 5,000,000

(Loyalty credit to P & L A / c)

Case III: When the actual royalty amount exceeds the minimum rent and short-term work is recovered (2019)

1. Royalty date

Kapoor Ltd 6,00,000

To loyalty A / c6,00,000

(Received royalties from Kapoor Ltd)

2. Entry to pay and get back work in a short period of time

Cash / Bank A / c Dr 5,00,000

Short time work A / c Dr 1,00,000

To Kapoor Ltd 6,00,000

(Receiving cash from Kapoor Ltd and Short Working Recouped)

3. Close the entry at the end of the year and do not get back to work in a short period of time

Royalty A / c Dr 5,00,000

Short time work A / c Dr 1,00,000

To P & L A / c 6,00,000

(P & L A / c will be granted loyalty credits and Short Working will be transferred)

Key takeaways:

- Loyalty is the amount paid by a third party to the owner of a product or patent in order to use the product or patent.

- The terms of payment for royalties are set forth in the license agreement.

- The royalty rate or royalty amount is usually a percentage based on factors such as monopoly rights, technology, and available alternatives.

- Consignment sales are the sale of products by consignment to a third party.

- The party selling the consignment product receives a portion of the profit as a flat rate or commission.

- Selling under consignment arrangements can be a low-fee, low-time investment method for selling goods and services.

- Most consignment dealers and online dealers offer the terms, but some are willing to negotiate.

- If you don't have a physical store or online marketplace to sell your products, consignment is a good workaround.

References:

- Financial Accounting by K.R.Das

- Financial Accounting by B.B.Dam