UNIT-5

MANAGERIAL CONTROL

After the planning, organising, staffing and directing have been carried out, the final managerial function of controlling assures that the activities planned are being accomplished or not. Control is a primary goal-oriented function of management in an organisation. Control can be defined as the process of analysing whether actions are being taken as planned and taking corrective actions to make these to confirm to planning. It is a process of comparing the actual performance with the set standards in order to ensure that activities are performed according to the plans and taking corrective action, if necessary. Controlling is performed at the lower, middle and upper levels of the management.

The managerial function of controlling is defined by Koontz and O’Donnell as, “the measurement and correction to the performance of activities of subordinates in order to make sure that enterprise objectives and the plans devised to attain them are being accomplished.”

George R. Terry remarked, “Controlling is determining what is being accomplished, that is evaluating the performance and, if necessary, applying corrected measures so that the performance takes place according to plans.”

Thus, management control is the process by which managers assure that resources are obtained and used effectively and efficiently in the accomplishment of the organisation’s objectives. Further, it is defined as the process by which managers in the organisation assure that activities and efforts are producing the desired objectives in the organisation.

Key Takeaways

- Control is a primary goal-oriented function performed at every level of management in an organisation.

- Controlling process thus regulates companies’ activities so that actual performance conforms to the standard plan.

- Control can be defined as the process of analysing whether actions are being taken as planned and taking corrective actions to make these to confirm to planning.

Based on definitions put forward by different authors, the following nature or characteristics of controlling can be presented below:

1. Control is a Function of Management: Actually control is a follow-up action to the other functions of management performed by managers to control the activities assigned to them in the organisation.

2. Control is Based on Planning: Control is designed to evaluate actual performance against predetermined standards set-up in the organisation. Plans serve as the standards of desired performance. Planning sets the course in the organisation and control ensures action according to the chosen course of action in the organisation. Unless one knows what he wants to achieve in the organisation, he cannot say whether he has done right or wrong in the organisation. Control implies the existence of plans or standards in the organisation.

3. Control is a Dynamic Process: It involves continuous review of standards of performance and results in corrective action, which may lead to changes in other functions of management.

4. Information is the Guide to Control: Control depends upon the information regarding actual performance. Accurate and timely availability of feedback is essential for effective control action. An efficient system of reporting is required for a sound control system. This requires continuing monitoring and review of operations.

5. The Essence of Control is Action: The performance of control is achieved only when corrective action is taken on the basis of feedback information. It is only action, which adjust performance to predetermined standards whenever deviations occur. A good system of control facilitates timely action so that there is minimum waste of time and energy.

6. It is a Continuous Activity: Control is not a one-step process but a continuous process. It involves constant revision and analysis of standards resulting from the deviations between actual and planned performance.

7. Delegation is the key to Control: An executive can take corrective action only when he has been delegated necessary authority for it. A person has authority to control these functions for which he is directly accountable. Moreover, control becomes necessary when authority is delegated because the delegator remains responsible for the duty. Control standards help a manger expand his span of management.

8. Control Aims at Future: Control involves the comparison between actual and standards. So, corrective action is designed to improve performance in future.

9. Control is a Universal Function of Management: Control is a basic or primary function of management. Every manager has to exercise control over the subordinates’ performance. No manager can get things done without the process of controlling. The process of management is incomplete without controlling.

10. Controlling is Positive: The function of controlling is positive. It is to make things happen i.e. to achieve the goal with instead constraints, or by means of the planned activities.

Key Takeaways

- Control is a follow-up action to the other functions of management performed by managers to control the activities assigned to them in the organisation.

- Control is designed to evaluate actual performance against predetermined standards set-up in the organization.

- It involves continuous review of standards of performance and results in corrective action, which may lead to changes in other functions of management.

- Control depends upon the information regarding actual performance.

- The performance of control is achieved only when corrective action is taken on the basis of feedback information.

- It is a continuous process.

- Controlling is futuristic and a positive function.

Controlling helps the management and the organization in many ways. It is an indispensable part of management. Planning will be meaningless in the absence of controlling. The importance of controlling is briefly stated below:

- It helps in achieving organizational goals.

- Facilitates optimum utilization of resources.

- It evaluates the accuracy of the standard.

- It also sets discipline and order.

- Motivates the employees and boosts employee morale.

- Ensures future planning by revising standards.

- Improves overall performance of an organization.

- It also minimizes errors.

- It renders planning effective.

Key Takeaways-

- Controlling helps the management and the organization in many ways. It is an indispensable part of management. Planning will be meaningless in the absence of controlling.

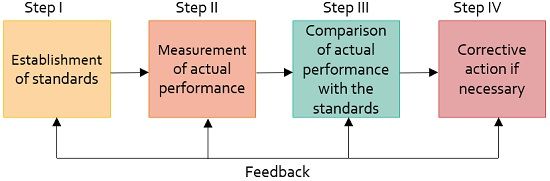

Control process involves the following steps as shown in the figure:

|

- Establishing standards: This means setting up of the target which needs to be achieved to meet organisational goals eventually. Standards indicate the criteria of performance. Control standards are categorized as quantitative and qualitative standards. Quantitative standards are expressed in terms of money. Qualitative standards, on the other hand, includes intangible items.

- Measurement of actual performance: The actual performance of the employee is measured against the target. With the increasing levels of management, the measurement of performance becomes difficult.

- Comparison of actual performance with the standard: This compares the degree of difference between the actual performance and the standard.

- Taking corrective actions: It is initiated by the manager who corrects any defects in actual performance. Controlling process thus regulates companies’ activities so that actual performance conforms to the standard plan. An effective control system enables managers to avoid circumstances which cause the company’s loss.

Key Takeaways

- Controlling function involves establishment of standards of performance, measurement of actual performance, comparison of actual performance with set standards and taking corrective measures, if required.

Below are some of the types of control with explanation:

- Feedback control: Feedback control involves gathering information about a past activity or action, and evaluating that information, and taking steps to improve similar activities or action in the future. Feedback control is historical in nature and is also known as post-action control. The implication is that the measured activity has already occurred, and it is impossible to go back and perform correctly to bring it up to standard. It is the least active of the controls and is generally a basis for reactions. Feedback allows managers to use past performance information to inform future performance in line with planned objectives.

2. Concurrent control: The process of monitoring and adjusting ongoing activities and processes is known as concurrent control. Concurrent controls are dynamic engagement in a current process where observations are made in real-time. Such controls are not necessarily proactive, but they can prevent problems from getting worse. For this reason, we often describe concurrent control as real-time control as it relates to current. A set of procedures are implemented to monitor project execution in order to find and solve problems or potential problems in a timely manner.

3. Feedforward control: Feedforward is a management and communication term that alludes to a representative or an association to give a controlled impact from which you are expecting output. Feedforward controls are future-directed, they attempt to detect and anticipate problems or deviations from the standards in advance of their occurrence. They are in-process control and are very active, aggressive in nature, allowing corrective action to be taken in advance of the problem.

4. Behavioral control: Behavioral control involves direct evaluation of managerial and employee decision making, not the results of managerial decisions. Behavioral control identified rewards for a wide range of criteria, such as in a balanced scorecard. When there are many external and internal factors, behavioral control and appreciative rewards are more appropriate that may affect the relationship between manager’s decisions and organizational performance. They are also suitable when managers must coordinate resources and capabilities across different business units.

5. Financial and non-financial controls: Financial controls involve the management of a firm’s costs and expenses so that they can be controlled in relation to budgetary amounts. Thus, in this way management determines which aspects of its financial position, such as profitability, sales or assets, are most important for the organization, tries to forecast them through budgets, and then compares actual performance to budgetary performance. Does. At a strategic level, total sales and indicators of profitability will be relevant strategic controls.

An increasing number of organizations are measuring customer loyalty, referral, employee satisfaction and other such performance areas that are not financial. Unlike financial control, the non-financial related control monitor aspects of the organization that are not promptly financial in nature, but are expected to lead to positive performance outcomes in the future. The principle behind such non-financial controls is that they can provide managers with a glimpse of the progress of the organization before measuring financial results. And this theory has some practical support. A highly satisfied customer is the best predictor of future sales in many of its businesses, so it regularly tracks customer satisfaction.

Key Takeaway

- Feedback control involves gathering information about a past activity or action, and evaluating that information, and taking steps to improve similar activities or action in the future.

- The process of monitoring and adjusting ongoing activities and processes is known as concurrent control.

- Feedforward controls are future-directed, they attempt to detect and anticipate problems or deviations from the standards in advance of their occurrence.

- Behavioral control involves direct evaluation of managerial and employee decision making, not the results of managerial decisions.

- Financial controls involve the management of a firm’s costs and expenses so that they can be controlled in relation to budgetary amounts.

Control function has many contributions in the smooth functioning of the organization. It is, however, not free from limitations. Some of the limitations of control function is briefly stated below:

1. Difficulty in setting quantitative standards: Control system loses its effectiveness when standard of performance cannot be defined in quantitative terms and it is very difficult to set quantitative standard for human behaviour, efficiency level, job satisfaction, employee’s morale, etc. In such cases judgment depends upon the discretion of manager.

2. No control on external factors: An enterprise can not control the external factors such as government policy, technological changes, change in fashion, change in competitor’s policy etc.

3. Resistance from employees: Employees often resist control and as a result effectiveness of control reduces. Employees feel control reduces or curtails their freedom. Employees may resist and go against the use of cameras, to observe them minutely.

4. Costly affair: Control is an expensive process it involves lot of time and effort as sufficient attention has to be paid to observe the performance of the employees. To install an expensive control system organisations have to spend large amount. Management must compare the benefits of controlling system with the cost involved in installing them.

The benefits must be more than the cost involved then only controlling will be effective otherwise it will lead to inefficiency.

Key Takeaway

- Control function has many contributions in the smooth functioning of the organization. It is, however, not free from limitations.

- The benefits must be more than the cost involved then only controlling will be effective otherwise it will lead to inefficiency.

A sound system of control is essential for the success of management. Essentials of a good controlling system are listed below:

- Simplicity: A good control system must be simple and easily understandable so that all the managers can apply it effectively. Complicated control techniques fail to communicate the meaning of control data to the managers.

- Objectivity: The standards of performance should be objective and specific, quantified and verifiable. They should be based on the facts so that control is acceptable and workable.

- Promptness: The control system should provide information soon enough so that the managers can detect and report the deviations promptly and necessary corrective actions may be taken in proper time. Corrective measures are of no value if those are taken too late.

- Economy: The control system must justify the expenses involved. In other words, anticipated earnings from it should be greater than the expected costs in its working. A small organisation cannot use the expensive control technique applied in large enterprises.

- Flexibility: Internal goals and strategies must be responsive to the changes in the environment and the control system should be flexible enough to adapt the changing conditions or unforeseen situations. It should be adaptable to the new developments. Flexibility in control system can be introduced by making alternative plans.

- Accuracy: The control system should encourage accurate information in order to detect deviations. The technique of control used should be appropriate to the work being controlled.

- Suitability: Control must reflect the needs and nature of the activities of the organisation, the control system should focus on achieving the organisational goals.

- Forward-looking Nature: The control system must be directed towards the future. It must pay attention on how the future actions can be conformed with the plans adopted.

- Focus on Strategic Points: The control system should focus attention on strategic or critical deviations. Only exceptional deviations require the attention of the managers.

- Motivating: A good control system should pay due attention to the human factor, It should be designed to secure positive action from the workers. Self-control tends to be motivated. Direct contact between the controller and the controlled also helps in making the control system motivational.

Key Takeaways

- The control system should focus attention on strategic or critical deviations. Only exceptional deviations require the attention of the managers.

- Internal goals and strategies must be responsive to the changes in the environment and the control system should be flexible enough to adapt the changing conditions or unforeseen situations.

Control is a fundamental managerial function. Managerial control regulates the organizational activities. It compares the actual performance and expected organizational standards and goals. For deviation in performance between the actual and expected performance, it ensures that necessary corrective action is taken.

There are various techniques of managerial control which can be classified into two broad categories namely- 1. Traditional techniques and, 2. Modern techniques.

Traditional Techniques of Managerial Control

Traditional techniques are those which have been used by the companies for a long time now. These include the following:

1. Personal Observation:

This is the most traditional method of control. Personal observation is one of those techniques which enables the manager to collect the information as first-hand information. It also creates a phenomenon of psychological pressure on the employees to perform in such a manner so as to achieve well their objectives as they are aware that they are being observed personally on their job. However, it is a very time-consuming exercise & cannot effectively be used for all kinds of jobs.

2. Statistical Reports

Statistical reports can be defined as an overall analysis of reports and data which is used in the form of averages, percentage, ratios, correlation, etc., present useful information to the managers regarding the performance of the organization in various areas. This type of useful information when presented in the various forms like charts, graphs, tables, etc., enables the managers to read them more easily & allow a comparison to be made with performance in previous periods & also with the benchmarks.

3. Break-even Analysis

Breakeven analysis is a technique used by managers to study the relationship between costs, volume & profits. It determines the overall picture of probable profit & losses at different levels of activity while analyzing the overall position. The sales volume at which there is no profit, no loss is known as the breakeven point. There is no profit or no loss.

Breakeven point can be calculated with the help of the following formula:

Breakeven point = Fixed Costs/Selling price per unit – variable costs per unit

4. Budgetary Control

Budgetary control can be defined as such technique of managerial control in which all operations which are necessary to be performed are executed in such a manner so as to perform and plan in advance in the form of budgets & actual results are compared with budgetary standards.

Therefore, the budget can be defined as a quantitative statement prepared for a definite future period of time for the purpose of obtaining a given objective. It is also a statement which reflects the policy of that particular period. The common types of budgets used by an organization are:

Sales budget: A statement of what an organization expects to sell in terms of quantity as well as value

Production budget: A statement of what an organization plans to produce in the budgeted period

Material budget: A statement of estimated quantity & cost of materials required for production

Cash budget: Anticipated cash inflows & outflows for the budgeted period

Capital budget: Estimated spending on major long-term assets like a new factory or major equipment

Research & development budget: Estimated spending for the development or refinement of products & processes

Modern Techniques of Managerial Control

Modern techniques of controlling are those which are of recent origin & are comparatively new in management literature. These techniques provide a refreshingly new thinking on the ways in which various aspects of an organization can be controlled. These include the following:

1. Return on Investment

Return on investment (ROI) can be defined as one of the important and useful techniques. It provides the basics and guides for measuring whether or not invested capital has been used effectively for generating a reasonable amount of return. ROI can be used to measure the overall performance of an organization or of its individual departments or divisions.

2. Ratio Analysis

The most commonly used ratios used by organizations can be classified into the following categories: Liquidity ratios, Solvency ratios, Profitability ratios, Turnover ratios.

3. Responsibility Accounting

Responsibility accounting can be defined as a system of accounting in which overall involvement of different sections, divisions & departments of an organization are set up as ‘Responsibility centers’. The head of the center is responsible for achieving the target set for his center.

4. Management Audit

Management audit refers to a systematic appraisal of the overall performance of the management of an organization. The purpose is to review the efficiency &n effectiveness of management & to improve its performance in future periods.

5. PERT & CPM

PERT (programmed evaluation & review technique) & CPM (critical path method) are important network techniques useful in planning & controlling. These techniques, therefore, help in performing various functions of management like planning; scheduling & implementing time-bound projects involving the performance of a variety of complex, diverse & interrelated activities.

Therefore, these techniques are so interrelated and deal with such factors as time scheduling & resources allocation for these activities.

Key Takeaways

- There are various techniques of managerial control which can be classified into two broad categories namely- 1. Traditional techniques and, 2. Modern techniques.

- Traditional techniques of controlling includes: Personal observation, Statistical reports, Break-even analysis and Budgetary control.

- Return on investment, Ratio analysis, Responsibility accounting, Management audit and PERT & CPM are the modern techniques of controlling used by organizations.

In the 2021 business climate, organizations are facing a more complex and competitive environment than ever before. As a result, the competencies of the leader who thrives in the modern-day business world is changing. Here are the new trends in management that learning initiatives will need to employ in 2021 and the following years.

1. Flattening organization structures: The days of the “hero” leader, or “the smartest person in the room” who must know everything and micromanage his or her direct reports will be a thing of the past. Organizations are moving towards flatter structures and they will need leaders who can thrive in a collaborative and cross-functional environment. ‘Flatter’ organizations tend to benefit from improved communication between employees, increased morale, less bureaucracy, and the ability to make decisions and changes faster. Typically, employees' responsibility levels tend to be much higher in flatter organizations, thus improving job satisfaction and reducing the need for excess levels of management. As we move through 2021 and towards next year, we will begin to see a shift in the hierarchy structure of many companies, particularly those in creative industries, and start ups.

2. Increasing need to develop self & others: To keep on top of the rapidly changing technological environment, leaders can no longer sit back and say “I know everything I need to know” as what they do know today will be outdated tomorrow. There is now a greater need to develop their self and their teams. When comparing job culture to that of 10 years ago, there is less loyalty amongst employees to their employers, meaning employers need to do everything they can to keep the employees in the company as long as possible to improve staff turnover. A popular method is through offering additional development and training alongside the role.

3. Approaching the “Talent Cliff”: Firms must prepare as the largest workforce in history moves into retirement. Mentoring, coaching, and job shadowing are examples of how organizations can manage the transition of the millennial leader. Many companies teetering on the edge of the talent cliff take the approach of hiring apprentices, and enrolling in apprenticeship programmes, to allow those interested in the industry to gain hands on experience, and for companies to be able to increase their workforce in a way that inexpensively gives back to the community, but also positively impacts the business.

4. Striving for gender balance: Strong women’s representation in leadership teams has been proven to bring organizations better results. A successful leadership development program thus needs to tap into an often woefully underutilized resource - its female managers. Achieving gender equality is important for workplaces not only because it is ‘fair’ and ‘the right thing to do,’ but because it is also directly linked to a country’s overall economic performance and therefore growth. Workplace gender equality is associated with:

- Improved national productivity and economic growth.

- Increased organizational performance .

- Enhanced ability of companies to attract talent and retain employees

- Enhanced organizational reputation.

- Many workplaces are actively striving to reach equality but also complete diversity amongst their workforce, a movement pushed forward largely by generation Z and millennials.

5. Shifting focus to development on soft skills: As the role of a leader migrates towards managing teams of diverse members who have different technical skills and areas of expertise, there will be greater emphasis on the need for leaders to develop their “soft skills". Whilst the focus in the past has been on ‘hard skills’ These types of skills include emotional intelligence, creativity, adaptability and time management. Employees can be taught “hard skills” such as the specific skills needed to carry out their role, however soft skills are learnt over time, and an employee failing in areas like time management could be detrimental to the business. Investing in the development of employees’ soft skills training courses will result in an increase of leadership potential, satisfaction in the workplace, and work performance.

6. Adopting a blended approach to leadership and management development: Leadership and management learning journeys will also need to evolve and use a wide variety of modalities to prepare the modern leader with the skills they need to thrive. Using a blended approach to leadership development allows leaders to break up their courses into more manageable sessions of one to one/class tutoring, with some transportable materials such as online webinars, and on the go tutorials that leaders can easily fit into their day with little disruption. The flexibility of blended learning makes it much easier to keep up as your business scales and grows, particularly nowadays when working from home and remote working is much more common.

7. Remote and flexible working: It’s quite likely that at least one member of your team works remotely, whether they’re a contractor or just somebody who needs to due to factors such as child care. Harnessing the power of the latest technology, social media and communication platforms early on, will allow your company to transition smoothly into remote working, should the time come. Remote working offers better flexibility, and better work life balance to your employees, it also opens up the ability to employ people from different backgrounds, and even countries, making the talent pool you’re fishing from much richer, which in turn will help to grow your business.

8. Training Millennials: Developing training strategies now to ensure millennials are well prepared for leadership is an important way to ensure smooth transitions once the next generations of employees (Gen Z) enter the workforce. It’s important to note that leadership styles have evolved with the ways of working and culture in many environments, and therefore the leadership styles that are taught should be aligned to this. It is often beneficial to seek training from sources outside an organization, to allow employees to bring fresh knowledge into a business, and put a different spin on habits that may have been used for years.

9. Outside Consultants: Once a leader accepts that they don’t know, or need to know everything about their specialism, and may not have all the answers, it opens up the opportunity to bring in external consultants to share their knowledge and experiences. Consultants are often hired to improve communication skills, collaboration and organizational skills, as well as skills specific to the job.

10. Artificial intelligence: AI is gradually being developed and implemented to both augment and replace human customer service agents to save costs and reduce the needs for human customer service staff. Whilst these bots are able to answer basic questions, there is still a need for a strong presence of a customer services team in order to keep customers happy. Using bots to take away need to answer repetitive and simple questions will free up your team to put more focus on the more difficult questions, and ultimately keep your customers happy.

Key Takeaway

- In the 2021 business climate, organizations are facing a more complex and competitive environment than ever before. As a result, the competency of the leader who thrives in the modern-day business world is changing.

References

- Gupta, S.K. & Joshi, R. Human Resource Management. Kalyani Publishers, New Delhi (2002).

- Khanka, S.S. Organizational Behavior. S. Chand & Company Pvt. New Delhi (2000), pp. 560.

- Prasad, L.M. Principles and Practices of Management. Sultan Chand & Sons, New Delhi (2019).

- Sarkar, S.S., Sharma, R.K., Gupta, S.K. Principles of Business Management. Kalyani Publishers, New Delhi (2017), pp. 339.

- Tripathy, P.C. and Reddy, P.N. Principles of Management. McGraw Hill Education (2017), pp. 680.