Unit 4

Role of Government

Monetary policy refers to the actions undertaken by monetary authority of a country to control money supply and achieve sustainable growth. In India it is issued by the RBI to control the credit capacity of commercial banks. The objectives of monetary policy are-

a) To control inflation.

b) To reduce unemployment.

c) To promote moderate long term interest rate.

The structure of monetary policy is highlighted in figure 1

Figure 1: Monetary policy

a) Quantitative credit control

a) Cash reserve ratio: It is the proportion of time and demand liabilities of commercial banks kept with RBI in the cash form.

b) Statutory liquidity ratio: It is the proportion of time and demand liabilities of commercial banks kept with RBI in other than cash form like gold, silver, precious metal, government securities etc.

b) Qualitative methods

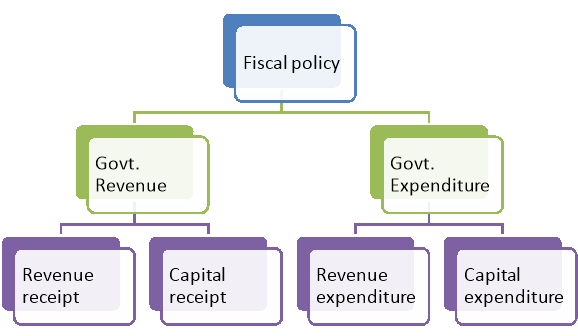

Fiscal policy is related to Govt. revenue and Govt. expenditure. Government annually determine fiscal policy under the Govt. budget. The sources of Government revenue and Govt. expenditure are-

a) Revenue receipts: Revenue receipts are those receipts that do not lead to a claim on the government. They are divided into tax and non-tax revenues. Tax revenues, an important component of revenue receipts, have for long been divided into direct taxes (personal income tax) and firms (corporation tax), and indirect taxes like excise taxes (duties levied on goods produced within the country), customs duties (taxes imposed on goods imported into and exported out of India) and service tax1. Other direct taxes like wealth tax, gift tax and estate duty (now abolished) have never brought in large amount of revenue and thus have been referred to as ‘paper taxes’.

b) Capital Receipts: All those receipts of the government which create liability or reduce financial assets are termed as capital receipts. The government also receives money by way of loans or from the sale of its assets. Loans will have to be returned to the agencies from which they have been borrowed. Thus they create liability. Sale of government assets, like sale of shares in Public Sector Undertakings (PSUs) which is referred to as PSU disinvestment, reduce the total amount of financial assets of the government.

2. Government expenditure

a) Revenue expenditure: Revenue Expenditure is expenditure incurred for purposes other than the creation of physical or financial assets of the central government. It relates to those expenses incurred for the normal functioning of the government departments and various services, interest payments on debt incurred by the government, and grants given to state governments and other parties (even though some of the grants may be meant for creation of assets). Budget documents classify total expenditure into plan and non-plan expenditure. According to this classification, plan revenue expenditure relates to central Plans (the Five-Year Plans) and central assistance for State and Union Territory plans. Non-plan expenditure, the more important component of revenue expenditure, covers a vast range of general, economic and social services of the government. The main items of non-plan expenditure are interest payments, defence services, subsidies, salaries and pensions.

b) Capital expenditure: There are expenditures of the government which result in creation of physical or financial assets or reduction in financial liabilities. This includes expenditure on the acquisition of land, building, machinery, equipment, investment in shares, and loans and advances by the central government to state and union territory governments, PSUs and other parties. Capital expenditure is also categorised as plan and non-plan in the budget documents. Plan capital expenditure, like its revenue counterpart, relates to central plan and central assistance for state and union territory plans. Non-plan capital expenditure covers various general, social and economic services provided by the government.

Figure 2: Fiscal Policy

Key takeaways-

1) Monetary policy refers to the actions undertaken by monetary authority of a country to control money supply and achieve sustainable growth. In India it is issued by the RBI to control the credit capacity of commercial banks.

2) Fiscal policy is related to Govt. revenue and Govt. expenditure. Government annually determine fiscal policy under the Govt. budget

Industrial Policy is a formal declaration by the Government whereby it outlines its general policies for industries. Any industrial policy has broadly two parts. First part generally deals with the ideology of the current political dispensation, while other one provides a framework of certain rules / principles. The main objective of any industrial policy is to augment the industrial production and thereby enhance the industrial growth which leads to economic growth by optimum utilization of resources; modernization; balanced industrial development; balanced regional development (by providing concessions for industrial development in backward areas); balanced development of basic and consumer industry; coordinated development of large as well as small, medium and cottage enterprises; determination of area of operation under private and public sector; enhance cordial relations between workers and management and proper utilization of the domestic / foreign capital. The figure 2 shows fiscal policy-

Importance of Industrialization

Some of the industrial policy are-

Need, Objectives and Importance of Industrial Policy

The need, objectives and importance of an industrial policy can be explained through following points:

The industrial policy helps in full deployment of natural resources of the country. It helps in identifying, collecting and using resources properly. It facilitates increase in national income of the country.

2. To Augment Industrial Production:

The main objective of the industrial policy is to augment industrial production of the country. It provides an impetus to rapid development of industries and industrial growth.

3. Modernisation:

The industrial policy encourages modernisation for increasing industrial output and productivity. It envisages the use of modem and latest production techniques m industrial sector. It facilitates maximum output at minimum cost of production.

4. Balanced Industrial Development :

The industrial policy envisages balanced industrial development of the country. It also facilitates balanced development of various sectors of the economy.

5. Balanced Regional Development

The industrial policy helps in balanced regional development of the country. The industrial policy may contain provisions regarding providing facilities or concessions for rapid development of industrially backward areas/regions of the country.

6. Coordination between Basic and Consumer Industries

The balanced development of basic and consumer industries is essential for economic growth. The industrial policy encourages development of basic and key industries on the one hand, while attention is paid to the development of consumer industries also on the other. Thus, by balanced and coordinated development of both types of industries it provides a pace to economic growth.

7. Coordination between Small Scale and Large Scale Industries

The industrial policy plays a vital role in coordinated development of small scale or cottage industries and large scale industries. These industries can be made mutually helpful to each other through the provisions of industrial policy.

8. Area Determination

The industrial policy determines the area of operation under public and private sector. Proper direction can be shown to private sector through the country’s industrial policy.

9. Cordial Industrial Relations

A comprehensive industrial policy is needed to establish cordial relations between workers and management. Cordial industrial relations are essential for rapid and sustainable industrialisation.

10. Proper Utilisation of Foreign Assistance/investment

An appropriate industrial policy envisages to attract foreign capital and entrepreneurs. It helps rapid industrial development of the country; A well thought of industrial policy checks the demerits of “foreign assistance. The foreign aid can be used in the national interest if an appropriate industrial policy is pursued by the country.

Key takeaways-

1) Industrial Policy is a formal declaration by the Government whereby it outlines its general policies for industries. Any industrial policy has broadly two parts. First part generally deals with the ideology of the current political dispensation, while other one provides a framework of certain rules / principles.

The industrial policy reforms have reduced the industrial licensing requirements, removed restrictions on investment and expansion, and facilitated easy access to foreign technology and foreign direct investment. Under the Industries (Development & Regulation) Act, 1951, an industrial licence is required in respect of the following:

i. Items of manufacture falling under the list of compulsory licensing (only 5 industries are in the list)

ii. If a non SSI unit intends to manufacture items reserved exclusively for the Small Scale Sector.

In addition certain industries are reserved exclusively for the Public Sector (presently Atomic Energy and Railway Transport come under this category). With progressive delicensing of industries, only 5 industries have been retained under compulsory licensing under the Industries (D&R) Act, 1951 viz.

(i) Distillation and brewing of alcoholic drinks;

(ii) Cigars and cigarettes of tobacco and manufactured tobacco substitutes;

(iii) Electronic aerospace and Defence equipment: all types;

(iv) Industrial explosives including detonating fuses, Safety Fuses, gun powder, nitrocellulose and matches;

(v) Hazardous chemicals: viz. (a) Hydrocyanic acid and its Derivatives; (b) Phosgene and its derivatives; (c) Isocyanates and diisocyanates of hydrocarbon, not elsewhere specified (example: Methyl Isocyanate)

At present there are 20 items which are exclusively reserved for manufacture in the small scale sector (SSI). Any non-SSI unit desirous of manufacturing these items needs an industrial licence which is issued with an obligation to export 50% of annual production.

Key takeaways-

1) The industrial policy reforms have reduced the industrial licensing requirements, removed restrictions on investment and expansion, and facilitated easy access to foreign technology and foreign direct investment.

Privatisation refers to transfer of ownership, management and control of the public sector enterprise to the private sector. In India, the concept of privatisation was introduced under LPG policy in the year 1993. It allows the private companies to enter into the banking sector, insurance sector, Production Company etc. which were not allowed before the introduction of LPG policy. For example, privatisation of Bharat Aluminium Company in 2006, privatisation of Delhi and Mumbai airports in 2006. Its main objectives are-

a) To increase the inflow of FDI to India.

b) To improve the financial strength of the company.

c) To improve the efficiency of PSU by giving them autonomy to make decision.

d) It promotes government dynamism due to lack of government interference.

The methods of privatisation of companies are-

Figure 1: Methods of privatisation

Under this method, transfer of ownership, management and control of the public sector enterprise is made to the private sector.

2. Disinvestment:

When the government withdraw its investment from the PSUs and sell it to the public, than it known as disinvestment.

3. Public auction:

Share of public company or long term assets are sold under this method to raise highest amount for government owned property.

4. Sale of shares:

Under this method, shares of PSUs can be sold through stock exchanges.

5. Direct negotiations:

Under this method, the government directly deal with specific private bodies for the privation of PSUs.

6. Lease with a right to purchase:

Under this method, a private company is also assumes possession and usage of a state run company or meeting by certain criteria. The private company can later chose to exercise the option to convert the lease of a property to ownership.

Key takeaways-

1) Privatisation refers to transfer of ownership, management and control of the public sector enterprise to the private sector. In India, the concept of privatisation was introduced under LPG policy in the year 1993.

Currency devaluation refers to the downward adjustment to a country’s value of money relative to a foreign currency or standard. Many countries use it as a monetary policy tool to control supply and demand.

Advantages of devaluation

Disadvantages of devaluation

Key takeaways-

1) Currency devaluation refers to the downward adjustment to a country’s value of money relative to a foreign currency or standard. Many countries use it as a monetary policy tool to control supply and demand.

The Exim policy/trade policy of India from 2009-14 are as follows-

a) The 5 different schemes (Focus Product Scheme, Market Linked Focus Product Scheme, Focus Market Scheme, Agri, Infrastructure Incentive Scrip, VKGUY) for rewarding merchandise exports with different kinds of duty scripts have been merged into a single scheme, namely Merchandise Export from India Scheme (MEIS) and there would be no conditionality attached to the scripts issued under the scheme.

b) Rewards for export of notified goods to notified markets under ‘Merchandise Exports from India Scheme (MEIS) shall be payable as percentage of realized FOB value (in free foreign exchange). The debits towards basic customs duty in the transferable reward duty credit scrips would also be allowed adjustment as duty drawback. At present, only the additional duty of customs / excise duty / service tax is allowed adjustment as CENVAT credit or drawback, as per Department of Revenue rules.

2. Service Exports from India Scheme (SEIS)

(a) Served from India Scheme (SFIS) has been replaced with Service Exports from India Scheme (SEIS). SEIS shall apply to ‘Service Providers located in India’ instead of ‘Indian Service Providers’.

(b) The rate of reward under SEIS would be based on net foreign exchange earned. The reward issued as duty credit scrip, would no longer be with actual user condition and will no longer be restricted to usage for specified types of goods but be freely transferable and usable for all types of goods and service tax debits on procurement of services / goods. Debits would be eligible for CENVAT credit or drawback.

3. Chapter -3 Incentives (MEIS & SEIS) to be available for SEZs

It is now proposed to extend Chapter -3 Incentives (MEIS & SEIS) to units located in SEZs also.

4. Duty credit scrips to be freely transferable and usable for payment of custom duty, excise duty and service tax.

(a) All scrips issued under MEIS and SEIS and the goods imported against these scrips would be fully transferable.

(b) Scrips issued under Exports from India Schemes can be used for the following:-

(i) Payment of customs duty for import of inputs / goods including capital goods, except items listed in Appendix 3A.

(ii) Payment of excise duty on domestic procurement of inputs or goods, including capital goods as per DoR notification.

5. Status Holders

(a) Business leaders who have excelled in international trade and have successfully contributed to country’s foreign trade are proposed to be recognized as Status Holders and given special treatment and privileges to facilitate their trade transactions, in order to reduce their transaction costs and time.

(b) The nomenclature of Export House, Star Export House, Trading House, Star Trading House, Premier Trading House certificate has been changed to One, Two, Three, Four, Five Star Export House.

5. Boost to "MAKE IN INDIA"

Reduced Export Obligation (EO) for domestic procurement under EPCG scheme:

a) Specific Export Obligation under EPCG scheme, in case capital goods are procured from indigenous manufacturers, which is currently 90% of the normal export obligation (6 times at the duty saved amount) has been reduced to 75%, in order to promote domestic capital goods manufacturing industry.

b) Higher level of rewards under MEIS for export items with high domestic content and value addition.

6. Trade facilitation & ease of doing business

Online filing of documents/ applications and Paperless trade in 24x7 environments:

a) DGFT already provides facility of Online filing of various applications under FTP by the exporters/importers. However, certain documents like Certificates issued by Chartered Accountants/ Company Secretary / Cost Accountant etc. have to be filed in physical forms only. In order to move further towards paperless processing of reward schemes, it has been decided to develop an online procedure to upload digitally signed documents by Chartered Accountant / Company Secretary / Cost Accountant. In the new system, it will be possible to upload online documents like annexure attached to ANF 3B, ANF 3C and ANF 3D, which are at present signed by these signatories and submitted physically.

b) As a measure of ease of doing business, landing documents of export consignment as proofs for notified market can be digitally uploaded in the following manner:-

(i) Any exporter may upload the scanned copy of Bill of Entry under his digital signature.

(ii) Status holders falling in the category of Three Star, Four Star or Five Star Export House may upload scanned copies of documents.

7. Online inter-ministerial consultations:

It is proposed to have online inter-ministerial consultations for approval of export of SCOMET items, Norms fixation, Import Authorisations, Export Authorisation, in a phased manner, with the objective to reduce time for approval. As a result, there would not be any need to submit hard copies of documents for these purposes by the exporters.

8. Forthcoming e-Governance Initiatives

(a) DGFT is currently working on the following EDI initiatives:

(i) Message exchange for transmission of export reward scrips from DGFT to Customs.

(ii) Message exchange for transmission of Bills of Entry (import details) from Customs to DGFT.

(iii) Online issuance of Export Obligation Discharge Certificate (EODC).

(iv) Message exchange with Ministry of Corporate Affairs for CIN & DIN.

(v) Message exchange with CBDT for PAN.

(vi) Facility to pay application fee using debit card / credit card.

(vii) Open API for submission of IEC application.

(viii) Mobile applications for FTP

9. Other initiatives

New initiatives for EOUs, EHTPs and STPs

(a) EOUs, EHTPs, STPs have been allowed to share infrastructural facilities among themselves. This will enable units to utilize their infrastructural facilities in an optimum way and avoid duplication of efforts and cost to create separate infrastructural facilities in different units.

(b) Inter unit transfer of goods and services have been allowed among EOUs, EHTPs, STPs, and BTPs. This will facilitate group of those units which source inputs centrally in order to obtain bulk discount. This will reduce cost of transportation, other logistic costs and result in maintaining effective supply chain.

(c) EOUs have been allowed facility to set up Warehouses near the port of export. This will help in reducing lead time for delivery of goods and will also address the issue of un-predictability of supply orders.

(d) STP units, EHTP units, software EOUs have been allowed the facility to use all duty free equipment/goods for training purposes. This will help these units in developing skills of their employees.

Key takeaways-

1) Industrial policy is formulated to control and regulate the industrial sectors of the country. It also aims to promote small scale industries of the country.

Regulation of foreign investment at the international level is scarce. Hundreds of bilateral and multilateral treaties attempt to regulate that behaviour, either exclusively or in combination with other matters, typically trade relations. The provisions of these treaties apply equally to the treatment of investment by nationals of either party in the territory of the other party or parties. The regulatory measures of foreign investment in India are-

Restrictive policies in the first group are expressed in strict controls over the entry and establishment of foreign investment, the levels of capital which foreign investors are permitted to invest and a myriad of performance requirements. Under such controls, the admission of foreign investment is typically subject to various “screening” procedures, licensing requirements and several approvals by the host state’s central and local authorities. The procedures are frequently cumbersome and based on rules that are vaguely formulated, allowing for significant measure of administrative discretion. Transfer of capital and earnings is subject to general currency controls and the employment of foreign labour is tightly restricted. Performance requirements usually include minimum local inputs, export ratios and/or local employment ratios. The legal approach to attracting foreign investments in certain sectors is incentive-based. Statutes of this kind emphasize fiscal (tax exemption) or other incentives to attract and channel foreign investments to certain areas or predefined sectors of the national economy. Such approaches have been proven to distort global flows of foreign investment, while bringing little or no benefits to the economic development of the host country.

2. Regulation in Outward-Looking Economies

The foreign investment statutes in this group of countries reflect market-oriented approaches to foreign investment, allowing in principle for open admission of foreign investment, subject to specified exceptions. In some of these statutes, the exceptions have been framed in broad terms to assure protection of the host state’s fundamental interests such as national security, public order, protection of the environment, public health and the like. In other statutes, the exceptions have been listed in so-called “negative lists” of areas of the national economy where the foreign investment is either absolutely prohibited or only partially permitted under specified circumstances. Some statutes also provide for a one-stop shop where all approvals required, including for tax exemptions, are obtained through one agency.

3) Bilateral investment treaties

The first modern bilateral investment treaty (BIT) was concluded in 1959 between Germany and Pakistan. Over the decades that followed an increasing number of European countries concluded such treaties with developing countries. By the mid- to late-1980s, BITs came to be universally accepted instruments for the promotion and legal protection of foreign investments. BITs are no longer concluded exclusively between capital-exporting and capital-importing countries; an increasing number of them began to be concluded among developing, normally capital-importing countries (and transition economy countries). The consolidation of certain core provisions in BITs points to what may be called the “first generation” of BITs. The greatly expanded treaty practice since the late1980s, however, has led to refinement in the drafting of BIT provisions and in some cases to their reformulation as instruments of investment liberalization policies.

Key takeaways-

1) Regulation of foreign investment at the international level is scarce. Hundreds of bilateral and multilateral treaties attempt to regulate that behaviour, either exclusively or in combination with other matters, typically trade relations. The provisions of these treaties apply equally to the treatment of investment by nationals of either party in the territory of the other party or parties.

References-