Unit 2

Accounting for Material

Concept and techniques

A material is a substance (physical term) that is part of a finished product or is composed of a finished product. In other words, a material is a product that is supplied to a business for the purpose of consuming it in the process of manufacturing or providing services, or for the purpose of converting it into a product. The term "store" is often used as a synonym for material, but store has a broader meaning, not only the raw materials consumed or used in production, but also miscellaneous goods, maintenance stores, processed parts, components. Also includes items such as tools. Jigs, other items, consumables, lubricants, etc. Finished and partially finished products are also often included in the term "store". Materials are also called inventory. The term material / inventory include not only raw materials, but also components; work in process, finished products, and scrap.

Material costs are an important component of the total cost of a product. It accounts for 40% to 80% of the total cost. Percentages may vary from industry to industry. But for the manufacturing sector, material costs are paramount. Inventory is also an important component of working capital. Therefore, it is treated the same as cash. Therefore, analysis and control of material costs is very important.

Purpose of material management system

Material management: The ability to ensure sufficient inventory of goods to meet all requirements without carrying unnecessarily large amounts of inventory.

The purpose of the material management system is to:

1. Make the material available continuously so that the flow of material for production is uninterrupted. Production cannot be postponed due to lack of materials.

2. Purchase the required amount of materials to avoid working capital locks and minimize the risk of surplus or obsolete stores.

3. Make competitive and wise purchases at the most economical prices so that you can reduce material costs.

4. Purchase the right quality material to minimize the waste of material.

5. Acts as an information centre for material knowledge about prices, suppliers, lead times, quality and specifications.

Introduction to purchasing materials:

For manufacturing concerns, there is another purchasing department under the control of the purchasing person. The main function of the purchasing department is to purchase the required amount of materials in time so that the store can provide the production department with a continuous supply of materials and purchase higher quality materials at a reasonable price.

Buyers need to play an important role as they can save or lose a lot of money. He requires good technical knowledge of the industry and some management skills. He also needs to be aware of management policies and sources of concern.

He also needs to be aware of market conditions and have knowledge of suppliers, trusted suppliers, prices and purchasing procedures.

He must keep up with government policies on import and export restrictions and various tariffs and taxes on goods. He must have practical knowledge of the law relating to contracts and the sale of goods so that he can negotiate and enter into contracts on behalf of his employer.

Centralized and Decentralized purchases:

Centralized purchase:

Centralized purchase means the purchase of materials by one specialized department. The purchasing department has personnel with expertise in all aspects of the material. The purchasing department has the authority to make purchases for the entire organization.

In this system, the requirements of the entire organization are confirmed through the creation of purchasing budget, the purchasing department makes purchases according to the accepted principle, and the materials are distributed to each production department according to the requirements.

In most cases, the purchasing department purchases materials based on the requisition form issued by the store. The supplier delivers the material to the Material Receipt section. Individual departments are not allowed to purchase their own materials when centralized purchases are made.

Decentralized purchase:

Decentralized purchases mean that each department can purchase materials according to their needs. Therefore, the authority to make purchases rests with the individual departments.

(A) Advantages of local purchase: If the production unit is far from the body, it is beneficial to have the unit available for purchase locally. You can enjoy the benefits of basic low price and seasonal price, and reduce the cost.

(B) Reduction of transportation costs: By supplying materials locally, transportation costs will be significantly reduced.

(C) Quick resolution of the problem: Disputes caused by refusals, shortages and returns can be resolved easily and quickly.

Advantages of centralized purchase:

From a centralized purchase, you can derive the following benefits:

(A) Benefits of bulk purchase: Because materials are purchased in bulk, trade discount rates are high, credit lines are improved, bargaining power, quantity, and discounts are increased, so materials can be purchased at much lower prices.

(B) Maintaining quality: All purchases are made by the purchasing department, which has expertise in product quality, which helps maintain the quality of the materials and ultimately leads to the production of better quality finished products. Improving product quality ensures that your business is more credible, resulting in higher sales and higher profits.

(C) Reduction of transportation costs: This system purchases materials in bulk, significantly reducing shipping costs. This has a positive impact on the total cost or unit cost of the material. This makes your organization more competitive.

(D) Advantages of specialization: The Purchasing Department has dedicated purchasing personnel to ensure the right purchases from the right type of supplier. This guarantees both quality and price.

(E) You can avoid duplication: All purchases are made by one person, avoiding duplicate purchases.

(F) Planned purchases: You can systematically eliminate the purchase and holding of surplus stores, which enables better space management and easily avoids unnecessary blocks of working capital.

Restriction:

The restrictions on centralized purchases are as follows:

(A) Expensive

The management costs of the purchasing department can be very high, resulting in a solid increase in total costs and defeating the very purpose of costs to reduce costs.

(B) It functions as an obstacle to smooth functioning.

If a production department does not have the materials it needs, it must wait for the purchasing department to purchase it. This delay leads to production outages, which in turn leads to increased costs.

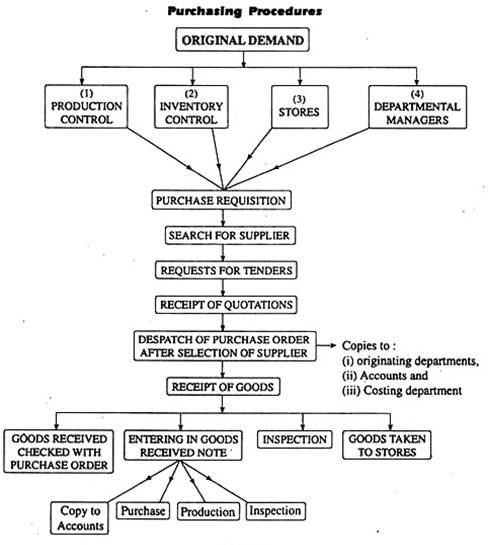

Purchasing routine:

In general, the following routine is used to purchase materials.

(I) Request for purchase. The request is made by the store officer.

(II) Offering bids and quotations for the supply of the required amount of material.

(III) Place an order with a supplier after considering bids and quotations submitted by different suppliers.

(IV) Receipt of material after proper inspection.

(V) Confirm and pass the supplier's payment invoice.

Purchase requisition:

The decision to purchase the material is made by the purchasing department after receiving the purchase request from the authorized department. A purchase request is made from an approved department to the purchasing department in a prescribed form called a purchase request.

Requisitions provide three basic pieces of information that help buyers perform their purchasing functions efficiently.

The information is as follows:

- What materials to buy (purchasing the right quality).

- When to buy (appropriate time).

- Amount to purchase (appropriate quantity).

Purchase requisitions are received by the purchaser from:

(I) Shopkeepers of all standard materials.

(II) Production control department of non-standard materials required for production.

(III) Plant and maintenance engineers for special maintenance and capital investment.

(IV) Head of special items such as office supplies.

The requisition is created three times. Two copies will be sent to the purchasing department, one copy will be retained as proof of approval and the other copy will be returned to the inventor after quoting the order details. Purchasing department. A third copy is kept by the store for office records and future references.

Material specifications or bill of materials:

The requisition contains details and specifications of the materials to purchase. Material specifications are known as bills of material. This starts in the production control department or the plant and maintenance engineer department. The BUI of Material is a complete schedule of materials or parts required for a particular job or work order created by a drafting office.

A bill of materials is created for every job and a copy is sent to the storekeeper.

BOM Benefits:

The following benefits can be obtained in different departments of the BOM.

(I) upon receiving the bill of materials, the purchasing department can place an order with the supplier of choice. Therefore, the bill of materials serves the purpose of the purchase requisition.

(II) The bill of materials allows the store to publish materials.

(III) The bill of materials contains details of the materials used in the job or work order, so the supervisor does not need to prepare detailed material requirements. This saves time and makes it easier to pull out the material.

Purchase time:

Requisitions indicate the date on which the use of the material is required. The storekeeper makes a request to the purchaser as soon as the material reaches the reorder level. Upon receiving the purchase requisition, the purchaser places an order with the supplier with a delivery date.

Delivery times are fixed taking into account the material consumption rate and the minimum level fixed to it.

Purchases are also made when market conditions are good, despite the fact that there is no immediate need for materials for production. In an inflationary economy, we buy materials in bulk in the hope that prices will rise further.

For raw materials such as jute, cotton and sugar cane, quantity, quality and price are used to make bulk purchases during the season. To prevent future price increases, long-term contracts may be entered into with suppliers to purchase materials for a specified period of time and at a specified rate.

However, in doing so, the purchaser must take into account the following factors:

(I) A storage facility for storing quantities.

(II) Financial resources of concern. And

(III) Transportation costs, capital costs, storage costs, etc.

Purchase quantity:

Before placing an order with a supplier, the purchaser must ensure that only the right quantity of stores is purchased. The following factors should be taken into account when determining the purchase quantity:

(I) Material inventory levels must be maintained to meet the requirements of the production sector.

(II) Production is not hindered by a shortage of raw materials.

(III) There should be no excess inventory or material shortage inventory to unnecessarily block working capital. And

(IV) Availability of funds

Purchase order:

Definition:

A purchase order is an agreement between a material buyer and a supplier. It is a requirement from the purchaser to the supplier to supply goods of a specific quantity and quality in accordance with the terms set forth in the contract. It also means the buyer's commitment to deliver and pay for the goods according to the terms and conditions stated on the purchase order.

After carefully determining the purchase quantity, the purchasing department should place an order with the supplier of choice. You need to choose a supplier that can deliver the products you need at a competitive price and at the right time. We are looking for a quote from our supplier.

Quotations received from different suppliers are compared and an acceptable supplier is selected. After completing the above procedure, a purchase order will be issued to the supplier to supply the required quantity of goods at the specified time.

Purchase order i is issued in the prescribed format, produced in quadruples (4 copies), and sent to the next department for reference and coordination.

(I) the first copy will be sent to the supplier.

(II) One copy will be sent to the department that sent the purchase requisition.

(III) One copy will be sent to the store or the internal department of the product.

(IV) One copy will be kept in the purchasing department as a permanent record.

(V) A copy will be sent to your account department.

Purchase procedure:

Purchasing departments need to follow specific steps for efficient purchasing. The purchasing procedure includes the following steps:

(1) Purchase request:

Receive purchase requisitions that you might receive from your store, production control department, or department manager. The amount of material you purchase should be carefully determined.

(2) Supplier search:

Purchasing departments need to find potential suppliers. Care must be taken when choosing the right supplier. Once the supplier has been identified, you will be asked to submit a quote or bid. You need to start bidding and select a supplier considering the conditions stated in the bid.

(3) Purchase order:

Once a supplier is selected, you need to pass the purchase order to the selected supplier. A copy of the purchase order should be sent to the original department, the accounting department, and one copy to the costing department.

(4) Receipt of materials:

The materials you receive must be entered in the receipt note and sent to the inspection department for inspection. After receiving the inspection report, the material is sent to the store and shipped to the manufacturing department.

To better understand the chart in this regard, it is shown below.

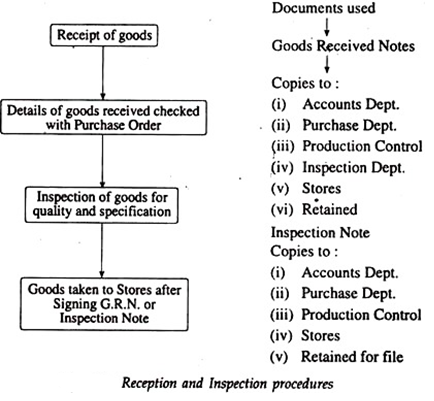

Receipt of goods:

The following chart shows the procedure for receiving and inspecting materials.

The warehousing department is usually located at the entrance of the factory. All carriers of goods are to report to this department. After receiving the delivery note or shipping advice from the supplier, the receiving department must arrange the unloading of the goods.

The receiving office must receive the goods after comparing the quantity, quality, and other details that should have been included in the purchase order. When you receive the item, you should check it by weighing, counting, or inspection.

If there is any damage or missing, you should state that fact on the carrier's copy or Challan. After being satisfied in all respects, the recipient of the goods must sign a copy of the carrier Challan. Next, you need to enter the item details on the receipt (below). The receipt memo is an important document and is required to confirm the supplier's invoice and pass it to payment.

The goods receipt note is prepared with an additional copy distributed as follows:

(I) To the purchasing department to update the purchase record.

(II) To the department that sent the purchase request.

(III) To the accounting and inventory management department.

(IV) To the shop owner. And

(V) Stored in the receiving department for records and future reference.

(VI) Goods receipt note (GRN):

This is a testimony of the goods received according to the purchase order. Otherwise, the supplier will be notified by formal contact. When making adjustments for damaged or defective items, it is customary to send a debit note to the supplier with the value of the damaged or rejected item and the shipping costs for the return.

Confirmation of purchase invoice:

Along with the goods, the supplier sends an invoice containing details of the materials supplied and their price.

The purchaser who receives the material should refer to the following document to verify the accuracy of the details.

(I) Order form.

(II) Receipt notes.

(III) Inspection report.

(IV) Debit notes (if any).

If the invoice is determined to be correct, it will be stamped with a rubber stamp by the responsible authority of the purchasing department and passed to the accounting department for payment. Invoices are now checked by an authorized person in the accounting department to ensure that the calculations are correct.

The invoice will be entered in the purchase diary that will be credited to the supplier's account. Periodically, the purchase journal totals are debited to the general ledger purchase account.

Goods receipt note (GRN) testimony of the goods received according to the purchase order

Key takeaways:

- The main function of the purchasing department is to purchase the required amount of materials.

- Centralized purchase means the purchase of materials by one specialized department.

- Decentralized purchases mean that each department can purchase materials according to their needs.

- From a centralized purchase there are certain benefits.

- A purchase request is made from an approved department to the purchasing department in a prescribed form called a purchase request.

- The requisition contains details and specifications of the materials to purchase.

- Before placing an order with a supplier, the purchaser must ensure that only the right quantity of stores is purchased.

- A material is a substance (physical term) that is part of a finished product or is composed of a finished product.

- The ability to ensure sufficient inventory of goods to meet all requirements without carrying unnecessarily large amounts of inventory.

The important methods to follow in pricing material issuance are: -

1. Actual cost method

2. First-in first-out (FIFO) method

3. Last-in first-out (LIFO) method

4. Maximum first-in first-out method (HIFO) method

5. Simple average cost method

6. Weighted average cost method

7. Periodic average cost method

8. Standard Cost method

9. Exchange cost method

10. Last-in first-out (NIFO) method

11. Base stock method.

1. Actual cost method:

If you purchase a material specifically for a particular job, the actual cost of the material will be charged to that job. Such materials are usually kept separately and published only for that particular job.

2. First-in first-out (FIFO) method:

CIMA defines FIFO as "a method of setting the price of material issuance using the purchase price of the oldest unit in stock." With this method, the materials are issued out of stock in the order in which they were first stocked. It is assumed that the material that opens first is the material that is used first.

Advantage:

(A) Easy to understand and easy to price in question.

(B) It is a good store management practice to ensure that raw materials leave stores in chronological order based on age.

(C) This is an easy method with less administrative costs than other pricing methods.

(D) This inventory valuation method is accepted under standard accounting practices.

(E) Consistent and realistic practices in inventory and finished product valuation.

(F) Inventory is valued at the latest market price, close to the value based on replacement costs.

Cons: Disadvantages:

(A) If confused with other materials purchased at a different price at a later date, it is uncertain whether the material with the longest stock will be used.

(B) If the price of the purchased material fluctuates significantly, there will be more clerical work and errors may occur.

(C) Manufacturing costs are modest in situations where prices are rising.

(D) Inflationary markets tend to lower prices for key issues. The deflationary market tends to set higher prices for these issues.

(E) Generally, it is necessary to adopt multiple prices for the publication of a single document.

(F) This method makes it difficult to compare costs for different jobs when billed for the same material at different prices.

3. Last in first out (LIFO) method:

With this method, the latest purchase is issued first. Issues are priced on the latest batch you receive and will continue to be billed until the new batch you receive arrives in stock. This is a way to set the issue price of a material using the purchase price of the latest unit in stock.

Advantage:

(A) Shares issued at more recent prices represent the current market value based on exchange costs.

(B) Easy to understand and apply.

(C) Product costs tend to be more realistic as material costs are billed at more recent prices.

(D) When the price is rising, the issue pricing will be the more recent current market price.

(E) It tends to show modest profit figures by minimizing unrealized inventory gains and valuing inventory at its pre-price value, providing a hedge against inflation.

Cons: Disadvantages:

(A) Valuation of inventory in this way is not accepted in the creation of financial accounting.

(B) This is an assumption of a cash flow pattern and is not intended to represent the actual physical flow of material from the store.

(C) It may be necessary to adopt multiple prices for one problem.

(D) It becomes difficult to compare costs between jobs.

(E) It involves more clerical work and sometimes the evaluation may go wrong.

(F) During inflation, the valuation of inventory in this way does not represent the current market price.

4. Highest in first out (HIFO) method:

With this method, the most expensive material is published first, regardless of the date of purchase. The basic assumption is that in a fluctuating inflation market, material costs are quickly absorbed into product costs, hedging the risk of inflation. This method is used when the material is in short supply and when you are running a contract with costs. This method is uncommon and is not accepted by standard accounting practices.

5. Simple average cost method:

In this way, all the materials received are merged into the inventory of existing materials and their identities are lost. The simple average price is calculated regardless of the quantity involved. The simple average cost is obtained by dividing the number of batches and adding the various prices paid during the period to the batches purchased. For example, three batches of material received in Rs. 20, rupees 22 and Rs. 24 per unit each.

The simple average price is calculated as follows:

Rs. 20+ rupees 22+ rupees 24/3 batch = Rs. 36/3 batch = 22 rupees per unit

This method takes into account the prices of different batches, but is not common because it does not take into account the quantity purchased in different batches. Use this method when the price is less volatile and the stock price is small.

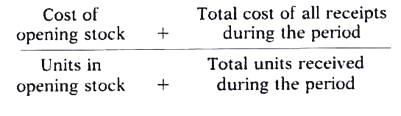

6. Weighted average cost method:

This is a permanent weighted averaging system in which the issue price is recalculated each time after each receipt, taking into account both the total quantity and the total cost when calculating the weighted average price. For example, three batches of material received in a quantity of 2,000 units @ Rs. 25, 2,300 units @ Rupee 26 and 800 units @ Rs. 24.24.

The weighted average price is calculated as follows:

(2,000 units x Rs .25) + (2,300 units x Rs .26) + (800 units x Rs .24) / 2,000 units + 2,300 units + 800 units

= Rs. 25,000+ rupees 20,800 + rupees 22,200 / 3,200 units = rupees 47,000 / 3,200 units = 25.26 per rupee unit

This method tends to smooth out price fluctuations and reduce the number of calculations because each issue is billed at the same price until you receive a new batch of material.

This method is easier than FIFO and LIFO because you do not have to identify each batch individually. However, this method adds more clerical work in calculating the new average price each time you receive a new batch. The calculated issue price rarely represents the actual purchase price.

7. Periodic average cost method:

With this method, instead of recalculating the simple or weighted average cost each time you have a receipt, the average for the entire accounting period is calculated.

The average price of all materials published during the period is calculated as follows:

8. Standard cost method:

In this way, important issues are priced at a given standard issue price. The difference between the actual purchase price and the standard issue price is amortized on the income statement. The standard cost is a predetermined cost set by management before the actual material cost is known, and the standard issue price is used for all issuance to production and valuation of final stock.

Careful setting of standard prices first significantly reduces all clerical work and errors and simplifies inventory recording procedures. Eliminating cost fluctuations due to material price fluctuations makes it easier to compare realistic manufacturing costs. This method is not suitable in situations where prices fluctuate.

9. Exchange fee method:

The replacement cost is the cost of replacing the same material by purchasing it on the pricing date of the material issue. It is different from the actual cost on the purchase date. The exchange price is the exchange price of the material at the time the material is issued or on the valuation date of the end-of-term inventory.

This method is unacceptable to standard accounting practices as it reflects costs that are not actually paid. If the shares are held at exchange costs and are purchased at a lower price for balance sheet purposes, an element of profit that has not yet been realized will be included in the income statement.

This method is advocated by charging the job or process for the market price of the material, making it easier to determine the profitability of the job or process. This method is especially suitable for inflationary trends in material market prices. Without the exact market for a particular material, it is difficult to ascertain the replacement price for a material problem.

10. Next Inn First Out (NIFO) Method:

This method is a variant of the exchange cost method. In this way, the price quoted in the latest purchase order or contract is used for all issuance until a new order is placed.

11. Basic stock method:

With this method, the specified quantity of material is always kept in stock and priced as a buffer or base stock at its original cost. In addition, issuance of materials that exceed the basic stock quantity is priced using one of the above methods.

This method shows how prices fluctuate over time. However, this method is uncommon and makes stock valuation completely unrealistic and is not accepted by standard accounting practices.

Key takeaways:

- Methods to follow in pricing material issuance.

- The simple average cost is obtained by dividing the number of batches and adding the various prices paid during the period to the batches purchased.

- The average price of all materials published during the period.

- The replacement cost is the cost of replacing the same material by purchasing it on the pricing date of the material issue.

Material requirements for production are issued based on material requirements. Output is taken with waste, scrap, rot, and defects. The exact cost of the output can be calculated after considering the loss.

Losses in the form of waste, scrap, putrefaction, and defects are inherent in any manufacturing activity and are unavoidable. These losses can be managed through proper reporting and liability accounting. The standard for each type of loss is fixed. Management needs to take steps to compare performance and manage anomalous losses based on variance.

The different types of material loss are described below:

1. Waste:

Waste is unique to every manufacturing activity. Waste is part of the raw materials lost during the production process and has no recoverable value. Waste is generated invisibly in the form of evaporation or shrinkage. It can also be visibly solid. Examples of visible waste include gas, dust, and worthless residues. Disposal of waste may incur additional costs. Example- Radioactive waste. Losses in the form of waste increase production costs.

Waste management:

Waste reports are prepared on a regular basis. Actual waste is compared to standard waste and corrective actions are taken to manage the anomalous waste.

Accounting for Waste:

Waste has no value. Accounting treatment differs depending on whether the waste is normal or abnormal.

I. Normal waste:

This is an inherent waste during manufacturing. It is in the form of evaporation, deterioration, etc. The total cost of normal waste is distributed to good production units.

II. Abnormal waste:

Abnormal waste is transferred to costing gains / losses A / c to avoid fluctuations in manufacturing costs.

2. Scrap:

Scrap is a residue from a particular manufacturing activity that is usually worth disposable. It can also be a waste material that can earn some income. Examples of scrap are stamping, filing, sawdust, short lengths from woodworking, sprue from casting and moulding processes and contoured materials from "flashes". Scrap can be sold or reused.

Scrap management: Scrap is managed by fixing scrap standards, fixing responsibilities for each department of scrap, and so on. Maintaining proper scrap records and regular reporting can help you manage your scrap. The actual scrap is compared to the standard scrap. If there is too much actual scrap than standard scrap, appropriate action will be taken.

Accounting for Scrap:

(A) Selling price of scrap credited to profit and loss A / c: The selling price is credited to the income statement as other revenue. Production costs include scrap costs. This accounting method is used when the value is negligible.

(B) Selling price recorded in overhead or material costs: The selling price is reduced along with the selling cost of scrap and the net selling price is deducted from the factory overhead or material costs. This method is used when multiple jobs are running at the same time and scrap cannot be separated for each job.

(C) Credit sales to the job or process in which the scrap occurred: The sales amount of the scrap is credited to the associated job or process in which the scrap occurred. This method is used when you can easily identify scrap for a particular job or process.

3. Corruption:

Corruption occurs when a product is damaged beyond modification. The spoilage is disposed of without further treatment. Corruption cost is the cost to the rejection point minus the selling price.

The method of selling spoilage depends on the degree of spoilage. If the degree of damage is small, some of the rot is sold in seconds. The rest may be sold as scrap or treated as waste.

Corruption Management: Corruption is managed through appropriate reporting of the degree of corruption. The standard is fixed as a percentage of production. The actual rot is compared to the standard and the differences are recorded. If the actual corruption exceeds the norm, appropriate measures will be suggested to control it.

Accounting for corruption:

Accounting depends on whether corruption is normal or abnormal. Normal spoilage is production-specific and occurs even under efficient conditions, so it is borne by good production units. Abnormal rot can be avoided under efficient conditions. The cost of abnormal corruption will be charged to the income statement.

4. Defects: It is part of the production that can be fixed and made into a good unit at an additional cost. Defective work is caused by poor quality raw materials, poor planning, and poor finish. Defective units are fixed with additional material, labor and overhead costs and are sold as "First Quality" or "Second Quality".

(A) Defect management: As with any loss, defects are managed with accurate and regular reports. The defective standard has been fixed. The actual defective product is compared with the standard. If the performance exceeds the standard, corrective action is taken to control it.

(B) Defect accounting:

The accounting process depends on the degree of production of defective products. If it is normal for it to be production-specific, it is identified in a particular job. The cost of the correction will be charged to the specific job. If the cost is not tracked in the job, the cost of the fix is treated as factory overhead.

If the defective work is in an unusual situation, the cost of the adjustment will be transferred to the income statement.

5. Obsolete, slow-moving, dormant stocks: These items are part of the inventory. Appropriate and timely action is required on the part of management to prevent over-the-counter losses and prevent working capital lockups.

(A) Obsolete inventory: These are inventories that have been left unused due to changes in product processes, designs, or manufacturing methods. They are generally outdated.

(B) Slow-moving material: It is in stock and has been used for a long time, so it has been idle for a long time.

(C) Dormant strains: It is an in-stock item that has not been used for a considerable period of time. Shopkeepers emphasize such items in regular reports and management either:

- Disposes of them at any price or

- Cleans them up to save store space

Future Items of such materials should be able to pay attention to the purchase.

Key takeaways:

- Material requirements for production are issued based on material requirements. Output is taken with waste, scrap, rot, and defects.

- The exact cost of the output can be calculated after considering the loss.

- Management needs to take steps to compare performance and manage anomalous losses based on variance.

- The different types of material loss are:

- Waste

- Scrap

- Corruption

- Defects

- Obsolete, Slow moving, Dormant Stock.

Most companies are continually trying to improve efficiency. One-way companies analyze efficiency is to look at expenses such as salaries and decide whether to make changes. If a particular payroll calculation is not satisfactory, the company may change its policy.

About labor utilization

Labor costs are usually one of the biggest costs for a company, so most companies want to make sure that labor costs contribute to revenue generation. The direct labor utilization calculation shows what portion of total salary expenditure a company pays for direct work, that is, work directly related to income-generating projects. The remaining salary costs are usually indirect labor costs such as training, marketing, management, paid leave, and taxes.

Calculation

To calculate the direct labor utilization rate of salary, divide the amount of salary paid for direct labor by the total salary cost for the period. For example, if you spend $ 3,000 on salary during a payroll period, of which $ 2,000 is paid directly as labor costs, the direct labor utilization rate for that period is 66.7% ($ 2,000 / $ 3,000 = 66.7).

Interpretation

The direct labor utilization rate of most companies is about 65%. The higher the direct labor utilization rate of a company, the more efficient the company operates. Companies with a large amount of paid training and paid leave have lower rates of direct work than companies with less paid training and paid leave. These taxes have little effect on the interpretation of direct labor utilization, as all companies pay the same percentage of payroll tax.

Things to consider

Many companies directly monitor labor utilization on a monthly basis to assess the efficiency of their business operations. If the company determines that the utilization rate of direct labor is too low, it will make efforts to increase the ratio by reducing indirect labor costs. However, companies may try to reduce indirect labor costs as much as possible, and some of these costs are needed for successful business operations.

Direct and Indirect Labour

Classification of labor costs

Labor costs can be categorized as follows.

1. Direct labor costs

Direct labor costs are part of salary or wages and can be identified and billed by a single unit price of production.

Characteristics of direct labor costs:

Direct labor costs have the following characteristics.

- It has a direct relationship to the product, process, or cost unit.

- It can be measured quantitatively.

- A sufficient amount of material.

2. Indirect labor costs

Even if it occurs directly, it cannot be identified in the production of goods or services. These costs are incurred at the production site. Some cost centers may serve production departments or production activities. These cost centers are responsible for purchasing, engineering, and time management.

3. Manageable labor costs

Labor costs can be managed by managers during production and even when there is no production. Standard hours and hourly rates are fixed and workers can be required to complete a job or order within such time. That way, labor costs can be reduced to some extent.

4. Uncontrollable labor costs

Labor costs that management cannot easily control. Jobs and orders can be completed by a group of workers. The efficiency of such labor groups is inherently different. Workers can maximize their efficiency according to the general environment of the product location. If so, costs cannot be controlled by management.

Direct labor refers to salaries and wages paid to workers who are directly involved in the manufacture of a particular product or the implementation of a service. The work performed must be related to a particular task. In the business of providing services to customers, direct labor is the work performed by workers who provide services directly to customers, such as auditors, lawyers, and consultants.

Wages paid are considered indirect if the work performed is not associated with a particular employee. If you want to track the total costs incurred in a particular project, you need to add direct labor costs as they can make up the majority of the project.

How to measure direct labor

Direct work includes the cost of regular working hours and the cost of overtime hours. This includes related payroll taxes and expenses such as social security, Medicare, unemployment tax and worker employment insurance. Companies must include contributions to the pension plan as well as health insurance costs. Some companies may include employee training and development costs incurred during the hiring process.

When calculating labor costs directly, the company must include all cost items incurred in maintaining and hiring employees. In addition to what you pay your employees, the company must consider the costs of retaining employees, such as payroll tax burdens, insurance premiums, and benefits.

Most companies have standard hourly rates that estimate the expected direct labor costs under normal conditions. For example, suppose you have a direct labor cost of $ 10 per hour to assemble stroller seats, and your company expects to spend 0.5 hours assembling each car seat. If the company produces his 1,000 units, the standard direct labor cost would be $ 5,000 ($ 10 x 0.5 x $ 1,000).

What is Indirect labor?

Indirect labor costs are labor costs that are not directly related to the production of goods or the provision of services. This refers to the wages paid to workers who perform duties that allow others to produce goods and provide services.

Unlike direct labor costs, indirect labor costs are not easily associated with a particular unit. Employees in this group include managers and managers such as supervisors, accountants, security guards, and cleaners.

The workforce is defined as the total workforce and expertise needed to complete a job. It can be divided into direct labor and indirect labor.

Overhead is a category of overhead and refers to employees who directly support overhead in performing their work. It is not directly involved in the service or production process.

Indirect labor cannot be traced back to a particular product or service, so the associated costs cannot be charged to the goods produced or the services provided. This represents the business overhead required to support operational levels.

What is an example of indirect labor?

Imagine you are the owner of a construction company. Consider both direct and indirect work when considering a contract. Direct labor costs are easy to understand. This refers to expenses, including wages and other benefits, incurred by employees directly engaged in projects such as workers, riggers, foreman and pipe fitters.

Indirect work refers to employees who are not involved in planning or construction projects. However, they are involved in running their day-to-day business. This includes human resources, management, accounting, customer service and more.

Examples of indirect labor include:

Computation of Labour cost

How to Calculate Labour Cost: Per Hour, Per Unit, Techniques and Formula

Techniques for managing labor costs can be effectively used by coordinating the activities of various labor-related departments.

(A) Human Resources Department

(B) Engineering and Operations Research Division

(C) Timekeeping department

(D) Payroll department and

(E) Cost accounting department.

The capabilities of these departments in reviewing and managing labor costs are described in detail below.

(A) Human Resources Department:

The Board of Directors has policies regarding recruitment, training, placement, transfer and promotion of employees. The Human Resources Manager of the Human Resources Department must implement these policies. The main functions of this department are recruitment, training, and placement of workers in the right jobs.

The Human Resources department recruits workers when it receives employee placement requests from various departments.

(I) Employee placement request:

This is a document initiated by a department that needs employees. Upon receipt of the job, the Human Resources Department will take action to appoint a worker by receiving the application, scrutinizing the application, interviewing the applicant, and finally selecting the appropriate candidate.

Key takeaways:

- Most companies are continually trying to improve efficiency. One way companies analyze efficiency is to look at expenses such as salaries and decide whether to make changes.

- The direct labor utilization rate of most companies is about 65%.

- The higher the direct labor utilization rate of a company, the more efficient the company operates.

- Even if it occurs directly, it cannot be identified in the production of goods or services.

- Wages paid are considered indirect if the work performed is not associated with a particular employee.

- Indirect labor costs are labor costs that are not directly related to the production of goods or the provision of services.

Labor turnover rate:

Labor turnover can be defined as the number of workers replaced during a particular period relative to the average workforce during the period. This is the number of workers who quit their jobs during the period relative to the average workforce during the period. It is a factor that affects labor efficiency and thus labor costs.

Definition: Turnover can be defined as the overall change in the number of people employed by an entity during a particular time period. This takes into account the number of employees leaving, new subscribers, and the total number of employees listed on salary at the end of a given period.

High turnover rates are considered unfavourable for organizational stability and can even lead to temporary closures and strikes. Therefore, entities take human resources as an integral part of their business. It means the rate of change in the composition of the workforce.

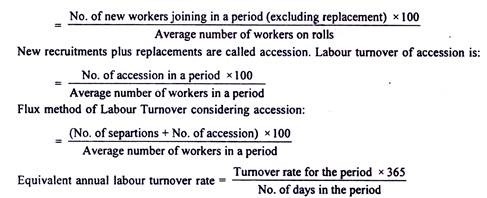

There are three ways to measure it:

- Calculating Labour Turnover by Separation Method

Labour Turnover = No. of workers left or separated during a period / Average number of workers on role during that period x 100

Average No.of. Workers = (No. Of workers at the beginning of the period + No. Of workers at the end of the period) / 2

2. Calculating Labour Turnover by Replacement Method

Labour Turnover = No. of workers replaced during a period / Average number of workers on role during that period x 100

3. Calculating Labour Turnover by Flux Method

Labour Turnover = No. Of workers separated in a period + No. Of workers replaced in the same period) / Average number of workers on role during that period x100

Turnover rate due to new hires: Workers who participate in a business to expand their business do not generate a turnover rate. Some cost activists believe that newly hired workers are responsible for changes in the composition of the workforce. The turnover rate of new workers is as follows.

- A high turnover rate is bad because it indicates that the worker will not stay long. When they go, they bring their experience with them. New workers must be engaged and trained. Aside from the cost of hiring and training new workers, their quality is expected to decline. Therefore, the turnover rate of workers is very costly for employers, but when workers take a break from work or get a job that is not suitable for them, they also lose.

- Both worker turnovers and shifts are costly, but most of the turnover costs usually occur during shifts. Separation is the cause of sales and the exchange continues.

- There is a certain amount of irreducible turnover due to illness, death, retirement, or marriage of female workers. However, research shows that actual sales are unnecessarily high in most industries.

Causes of turnover:

Some of the causes that contribute to high turnover are the disagreement between work and workers, low wages, bad working conditions, bad treatment on the part of employers, or simply the raging nature of workers. Therefore, the cause may be unavoidable.

The avoidable causes of turnover are:

(1) Redundancy due to seasonal fluctuations, material shortages, project completion, etc. The efficiency and foresight of senior management can eliminate sales from these causes.

(2) Boring work

(3) Bad working conditions

(4) Low wages

(5) Unstable employment

(6) There are few opportunities for promotion

(7) Unfair treatment

(8) Labor dispute.

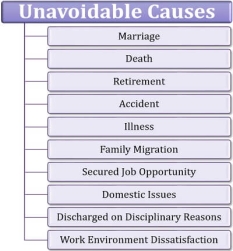

The unavoidable causes are as follows:

(1) Difficulty of housing

(2) Personal improvement

(3) Domestic responsibility

(4) Illness and accident

(5) Leave the district

(6) Discharged because it was judged to be inappropriate

(7) Discharge due to disciplinary action

(8) Retirement

(9) Death.

Employers can significantly reduce worker turnover, thereby saving labor costs.

Labor turnover cost:

It is a good idea to calculate the labor turnover cost individually.

It consists of:

(A) Recruitment costs for additional men engaged due to excessive turnover.

(B) Training costs for additional men engaged. And

(C) Loss due to reduced production quantity and quality due to sales, represented by lack of recovery of hourly wages and fixed costs.

(D) Costs of lost time, wasted, scrap, defective work and tools, and machine damage due to inefficiencies of new employers.

(E) Cost of products lost due to delayed acquisition of new workforce.

(F) Frequency of accidents due to lack of experience of new employees.

Impact on labor turnover

When an employee leaves the organization, it affects the work of some or even the entire entity.

This effect can be both constructive and destructive to the organization. When workers leave the company in groups, the impact is even greater and productivity is reduced.

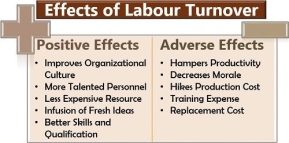

Harmful effects

First, let's talk about the negative effects of turnover within an organization.

- Impede productivity: When an employee quits a job, production is temporarily stopped or slowed down until a new employer joins the organization.

- Demoralization: Colleagues lose motivation when they find that a retired employee is retiring for a better opportunity.

- Increased production costs: During the training or learning phase of a new employee, the cost increases due to reduced productivity and high waste.

- Training Costs: Wages paid to trainees, new employees, and mentors during unproductive training periods are a significant expense to the organization.

- Replenishment Costs: Recruiting new staff to fill the position of retired employees includes advertising, employment, and training costs.

Positive effect

Labor turnover also has several benefits for the organization. This is explained in detail below.

- Improve your organizational culture: Turnover means the entry of new people with different values, ideas and beliefs to enrich your organizational culture.

- More talented people: New hires are more efficient, knowledgeable, sensitive and active than existing employees.

- Cheaper Resources: Due to continuous price increases and promotions, existing workers will cost more than alternative cheap trainees.

- Injecting Fresh Ideas: New resources bring innovative ideas and ways of doing things. This is very beneficial to the organization.

- Better Skills and Qualifications: Evolving courses and skill training allow organizations to acquire new graduates with better abilities.

Types of turnovers

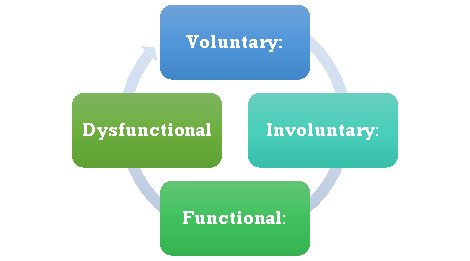

Turnover can be distinguished based on employee spontaneity and its impact on the organization. Below are four basic types of her.

- Voluntary: When an employee voluntarily leaves the organization, that is, when the person resigns from work for some reason, it is called voluntary turnover.

- Involuntary: In the case of involuntary turnover, the worker is excluded from the job by management. It may be due to reasons such as non-compliance with the norms.

- Functional: Being functional means improving the efficiency of your organization.

- Dysfunction: Dysfunctional labor shifts occur when highly efficient and skilled employees quit their jobs by interfering with the overall functioning of the organization.

Strategy to reduce turnover

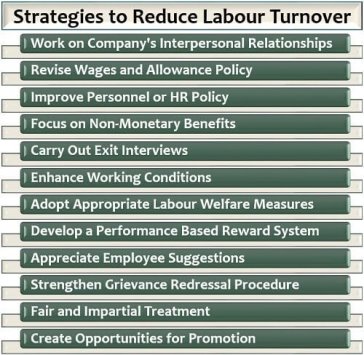

Turnover is an unavoidable aspect of business. However, you can control it by taking timely actions and improving existing HR policies.

Let's look at other ways to reduce the number of exits.

Management must make constant efforts to promote good relationships with healthy employees within the organization. Wage and incentive plans should be reviewed and upgraded annually to ensure fair wages for workers.

Another way is to change your personnel policy according to the guidelines set by government and corporate behavior. In addition to fair wages, we can maintain employee employment by providing a variety of incidental benefits such as insurance, medical facilities and transportation.

Retirement interviews provide a definitive reason for turnover, so do it to get an idea of all the things you need to improve. Workplace facilities such as adequate ventilation, lighting, drinking water and cleanliness must be maintained.

Organizations should not underestimate labor welfare and take appropriate steps to empower their talent. Corporate compensation and compensation planning must be progressive to motivate and evaluate talented employees.

Ground-level employee ideas can prove beneficial to the organization. Therefore, they should be encouraged to share their views. Resolving conflicts and addressing the dissatisfaction and problems of workers in the workplace creates a healthy environment for all.

Managers and supervisors need to be open-minded about their subordinates in order to deepen their ties and understanding. All employees are looking forward to the growth prospects that the organization offers. Therefore, it is very advantageous to give employees the opportunity to be promoted.

Conclusion

Turnover is usually high in private organizations where many workers engage in day-to-day tasks that do not require expertise.

However, skill-based organizations are trying to maintain low turnover rates. This is because if their valuable resources leave the company, they will have to bear the cost of fairly high sales.

Although a small factor, employees tend to stay in the organization for longer if the employee orientation process is prominent.

Key takeaways:

- Labor turnover can be defined as the number of workers replaced during a particular period relative to the average workforce during the period.

- Some of the causes that contribute to high turnover are the disagreement between work and workers, low wages, bad working conditions.

- Employers can significantly reduce worker turnover, thereby saving labor costs.

- When an employee leaves the organization, it affects the work of some or even the entire entity.

- Turnover is usually high in private organizations where many workers engage in day-to-day tasks that do not require expertise

- Management must make constant efforts to promote good relationships with healthy employees within the organization.

- Wage and incentive plans should be reviewed and upgraded annually to ensure fair wages for workers.

- Turnover can be distinguished based on employee spontaneity and its impact on the organization.

- Some of the causes that contribute to high turnover are the disagreement between work and workers, low wages, bad working conditions, bad treatment on the part of employers, or simply the raging nature of workers.

- There is a certain amount of irreducible turnover due to illness, death, retirement, or marriage of female workers.

Idle time

This is usually the difference between the time paid to workers and the time spent on production. The loss of time that an employer faces but does not benefit directly is called ideal time.

Cause of idle time

The causes of idle time can be classified into the following groups:

- According to their control ability.

- Depending on the function

- According to controllability, the causes are:

Normal idle time, including gate-to-work time, lunch breaks, breaks, tea time, loot setting time, and machine adjustment time.

Abnormal idle time due to failure, shortage, known availability of raw materials, neglect of strike or lockout.

Depending on the function:

- Productive cause

- Administrative causes

- Economic cause

- The productive causes are:

- Machine failure

- Unused manpower

- Waiting for work

- Power outage

- Waiting for tools / raw materials

- Waiting for instructions

2) The following are the ideal primes caused by the administrator:

- Inadequate planning

- Delayed or inappropriate instructions

- Unused capacity due to administrative decision

3) The idle time caused by economic causes is as follows:

- Lack of demand

- Lockouts and strikes

- Non-dismissal of off-season workers

Idle time control

- The ideal time is caused by a normal or abnormal cause and needs it appropriate planning to avoid these causes.

- Idle time can be eliminated or minimized by performing the following steps:

Production should be properly planned

Machine maintenance required

Effective use of manpower

Materials to buy in time

All idle time managers need to be identified and corrective action taken.

Handling of idle time

The idle time that is not available remains merged into the job or automatic transfer that the worker was hiring. Normal idle time is reserved for work overhead exercises, which are categorized according to cause and assigned to individual transfer numbers.

Abnormal idle time is usually heavy, takes a long time, and is included in the profit and loss account when it is adjusted to the costing profit or loss account or when the accounts are consolidated.

Over time

If a person works longer than normal working hours, the extra time the person worked is known as overtime. The cause of two factors, normal costs and additional costs, is known as overtime costs. The rate of overtime is higher than twice the normal rate.

It's a win-win situation for both the organization and the employees, as the organization has optimal capabilities and the company needs additional capabilities for people and machines, which are fully utilized. Employees are in the form of overtime pay.

Causes of overtime

It may be caused by the following circumstances:

- To work for the seasonal rush

- For the time lost due to unreasonable conditions

- To complete the work according to the customer's request

- To work for policy making, for example, when there is a shortage of workers and there is extra pressure from existing workers.

Overtime treatment

Treatment of overtime pays in cost accounting, if overtime is done according to the customer's wishes, the full amount of overtime, including freedom of overtime, must be charged directly to the work.

This is due to the pressure of common work to increase insurance production, and overtime may need to be charged for common overheads.

If the cause is the negligence or delay of a worker in a particular department, the relevant department may be charged.

If the cause is an uncontrollable situation that may be charged to the costing P & L account.

Disadvantages of overtime

- Labor costs will be higher

- It also reduces productivity

- At what time in the middle of the night, the cost of lighting, which is electricity, increases?

- It affects the health of customers

- Leads to fatigue

- Improves productivity

- The number of defective products is increasing

- Workers may be disappointed when work is unevenly distributed.

Procedures for managing overtime

- Overtime should be approved after investigating the reason

- Overtime must be in the relevant department.

- If overtime is a normal function, consider hiring more men.

- Overtime is due to a lack of plants, machinery, or other resources, and the steps to be taken to increase the number of machinery.

- Machines can be used if possible to fix caps for each category of overtime.

Methods of wage payment-time and piece rates; Incentive schemes.

Everything you need to know about how to pay wages! The success of an organization depends heavily on the efficiency of labor, which is significantly affected by the amount of wages paid to them. In many cases, management is of the opinion that the benefits of concern can only be maximized by lowering the wage rate paid to workers. However, this view is incorrect.

Low-wage workers are usually inefficient, leading to wasted materials, reduced economic use of tools, frequent machine failures, lost time, resulting in higher production costs, reasonable and fair. It should be remembered that the wages allowed will ultimately lead to a more economical use of machinery, tools, materials, and time.

Therefore, the importance of wage payment methods should not be underestimated.

Some of the wage payment methods are:

1. Time rate planning

2. Partial rate planning

3. Balanced or debt method.

1. Hourly rate plan:

This is the oldest and most common way to fix wages. Under this system, workers are paid at a rate of 1 hour, 1 day, 1 week, 2 weeks, 1 month, or other fixed period, depending on the work done over a period of time.

The important point is that the production of workers is not taken into account when determining wages. You will be paid a flat rate as soon as the contract expires.

Advantages and disadvantages of Hourly wage plans

Merit

i. It's easy because you can easily calculate how much a worker has earned.

Ii. Since there is no time limit for performing work, workers may not finish their work in a hurry and pay attention to the quality of their work.

Iii. All workers hired to do a particular type of work receive the same wages, avoiding malice and jealousy between them.

Iv. The slow and stable pace of the workers eliminates the rough handling of machines, which is a clear advantage for employers.

v. It is the only system that can be beneficially used when the production of individual workers or groups of employees cannot be easily measured.

Vi. Daily or hourly wages provide workers with a regular and stable income, and the budget can be adjusted accordingly.

Vii. This system is favoured by organized workers because it provides solidarity between specific classes of workers.

Viii. Hourly wage contracts are based on integrity and mutual trust between the parties and therefore require less administrative attention than others.

Demerit:

i. The fact that men have different abilities and that better workers do not have the incentive to work harder and better if everyone is paid equally is not taken into account. Therefore, they are reduced to the level of the most inefficient craftsmen.

Ii. Labor costs for certain jobs are not fixed. This puts the authorities in a difficult position in estimating the price of a particular work. There is always the potential for systematic avoidance of work by workers, as workers do not have a specific requirement to complete their work within a certain period of time.

Iii. This system allows many to work in jobs where he has neither taste nor ability, when he may mark him in other jobs.

Iv. Employers do not know how much work each worker puts in, so they cannot adequately assess the total wage spending to create a particular job.

v. The lack of records of individual workers' achievements makes it difficult for employers to determine his relative efficiency for promotion purposes.

2. Peace rate system:

Under this system, workers are paid according to the amount of work completed or the number of units completed, regardless of how long it takes to work, and the rate for each unit is settled in advance. This does not mean that the worker can take any time to complete the rate at which each unit is prepaid, regardless of how long it takes to perform the task. This does not mean that workers can take time to complete their work at any time. This is because if his performance far exceeds the time expected by the employer, the overhead of each item will increase.

It has the indirect implication that workers should not exceed the average time. If he consistently spends more time than average, he does it at the risk of losing his job.

In this plan, a worker working on a given machine under given conditions will be paid in exact proportion to his physical production. He is paid for a direct promotion to his output, and the actual amount paid per unit of service is approximately equal to the limit of his service in supporting the production of that output. This system is commonly used for repetitive nature jobs where tasks can be easily measured, inspected, and counted.

It is particularly well suited for standardized processes and appeals to skilled and efficient workers who can maximize their capabilities and increase their bottom line. In the textile industry weaving and spinning, local growing in mines, leaf picking in plantations, and in the shoe industry, this system is very useful.

However, it is difficult to apply when different shifts are employed in the same job, such as in the gas and electrical industries, or when different grades of workers are employed in different unmeasurable services.

Advantages and disadvantages of peace rate system:

Merit

I. It pays the craftsman according to his efficiency as reflected in the amount of work found by him. It satisfies hard-working and efficient workers, as he thinks his efficiency will be fully rewarded.

Ii. Supervision costs are not that heavy. Because workers know that their wages depend on the amount of work they do, they are less likely to waste time.

Iii. Direct labor costs per unit of production are constant and constant, making it easier to calculate costs when filling out bids and quotes.

Iv. Not only will production and wages increase, but production methods will also improve. This is because workers demand defect-free materials and machines in perfect working conditions.

v. The total unit cost of production is reduced at higher output because the fixed overhead can be distributed to more units.

Demerit:

I. This system is not particularly favoured by workers, although it benefits workers as well as business owners. The main reason for this is that the fixed piece rate by the employer is not scientifically based. In most cases, he determines the rate by empirical law and finds that on average workers get higher wages compared to the wages of workers doing the same job on a daily basis. Burden workers to reduce rates.

Nevertheless, the goose must be killed. Without it, the employer is extravagant in his job. Will continue to pay for, so he will curb the growing ambitions of his men. "

Ii. Workers want to work at tremendous speeds, so they generally consume more power, overuse machines, and don't try to avoid wasting materials. As a result, production costs are high and profits are low.

Iii. Workers' enthusiasm for increased production is likely to reduce the quality of their work. This zeal affects their health and can lead to reduced efficiency.

Iv. It encourages soldiers.

v. If you work too fast, your plants and machines can wear out and be replaced frequently.

Vi. Trade unions often oppose this system. Because it fosters competition among workers and puts their solidarity in labor disputes at risk.

3. Balance or debt method:

This is a mixture of time and peace rate. Workers are guaranteed hourly or daily rates at different peace rates. If the worker's income calculated at the peace rate exceeds the amount he would have earned if paid on an hourly basis, he would get a balance, a credit for excess peace rate income that exceeds the time rate income. ..

If his peace rate earnings are equal to his time rate earnings, then the overpayment issue does not occur.

If the peace rate revenue is less than the time rate revenue, he will be paid based on the time rate. However, the excess paid to him will be carried over as debt to him and will be recovered from the future piecework balance of overtime income. This system assumes that the time and peace rate are fixed on a scientific basis.

How to pay wages-time and partial wages (advantages, disadvantages, and suitability)

1. Hourly wage:

This is the oldest and most commonly used standard for labor compensation. In this way, employees are paid based on working hours, that is, hourly, weekly, monthly, or other fixed time periods, regardless of the amount of work done. The important point is that employees are paid a flat rate as soon as the contract time expires. And his work is not taken into account.

Hourly wage payments are actually found in these industries and in jobs where the quality of the goods produced is very important. For example, a work of art whose production speed is beyond the control of the employee, is automatic in production, or is difficult to measure the work done by the employee, such as clerical, managerial, or supervisory. This system is very simple and easy to follow.

Merit:

The hourly wage system has the following advantages.

(I) it is the simplest system to calculate wages because it is very easy to check the time spent on work. The cost of the uptime wage system is negligible.

(II) There is no time limit to complete the work, so you can maintain the quality of the product with special care.

(III) Workers do not have to rush to complete their work, avoiding speeding and consequent equipment damage. Therefore, there is no rough handling.

(IV) If production is not standardized, it will not be possible to accurately measure worker productivity. In such situations, Shin is the best system for paying wages.

(V) All workers doing a particular type of work receive the same wages under this system. Therefore, there is no reason for malice or jealousy among the members of the group.

(VI) It gives workers a sense of security. If you are temporarily inefficient due to injury or illness, don't be afraid to cut your wages. This system is suitable in case of unavoidable interruption of work.

(VII) This system promotes industrial peace for the following reasons: Trade unions support it and allow it for the benefit of workers, as it makes no distinction in the class of workers.

Cons: Disadvantages:

This system has some drawbacks. The main drawbacks are:

(I) the system does not distinguish between efficient and inefficient workers, and honest workers and sharkers. Wages are paid to all according to the time spent on work. It demoralizes competent workers.

(II) There is a lack of incentives for workers to increase productivity because there is no provision for compensation for extra efforts. Therefore, it does not provide a positive incentive for the worker to demonstrate his abilities by improving his efficiency and giving him better performance.

(III) Jobs tend to be loose because there is no specific time limit to complete the job.

(IV) This system suppresses superior workers because they are paid the same wages as inferior workers. They are refraining from producing better results.

(V) Continuous and rigorous supervision is required to maintain the quality and quantity of work and thereby reduce production costs.

(VI) Employers determine if it is difficult to calculate labor and production costs due to the large fluctuations in production and costs in this system.

Compatibility:

After considering the strengths and weaknesses of the hourly wage system, we can conclude that this system is suitable for the following situations:

The quality of work is the first consideration

- Inevitable interruptions and delays in work or output

- Production is done on a small scale so that effective supervision is possible.

- Workers are learning work,

- The nature of work changes frequently,

- The work is not standardized and the output is beyond the control of the operator.

- Professional skills are required to carry out the work.

- It is not possible to measure the production of workers easily or accurately. And

- It is considered to be the only practical method.

2. Peace wage:

This is the second oldest way to pay wages. In this way, the amount of work is the basis for paying wages, not the time spent on work. A fixed rate for generating units of output is agreed and paid.

Workers are paid a fixed fee for each work produced or completed, which is typically developed based on an analysis of previous performance and the establishment of average performance based on specific skill criteria.

Workers' income can be calculated based on the following formula: "WE = NR" where WE are the worker's income, N is the number of pieces produced, and R is the rate per piece.

Merit:

This system has several advantages.

(I) It is very easy to calculate wages under this system.

(II) The cost of supervision is not so heavy as strict supervision is not required as the workers themselves are interested in raising production to get higher wages.

(III) Since the labor force per unit of cost is constant, the production cost and the cost per unit can be easily calculated and estimated.

(IV) Increased productivity and productivity due to the great motivational effect of financial incentives.

(V) There is greater cooperation from workers to avoid interruptions in work. They take great care to prevent machine and workplace breakdowns.

(VI) Workers themselves can improve labor arrangements and production methods. Workers demand flawless materials and machines in perfect operation.

(VII) Fixed overhead can be distributed to more units, resulting in lower production costs with larger production volumes.

(VIII) Good workers are encouraged to put more effort and work harder.

Cons: Disadvantages:

Among the main drawbacks of this system, the following are important:

(I) too much emphasis is placed on production at the expense of product quality.

(II) Workers are in a hurry to finish their work, which often results in tool and equipment breakage, material waste, machine overwork, and increased power consumption.

(III) Excessive enthusiasm causes the work to be done at the highest speed possible, which puts a heavy burden on the operator and causes excessive fatigue. They compromise their health and efficiency. It may cause an accident

(IV) Increasing income has reduced the regularity of workers' attendance and has a negative impact on employee morale.

(V) Workers feel uneasy because they earn wages based on their output. If efficiency drops temporarily due to health conditions, wages will be lost during that period.

(VI) Trade unions oppose this system because the peace rate is not fixed on a scientific basis. Political, too, this system undermines trade unions because workers cannot spend time on union activities.

(VII) This system fosters jealousy, suspicion and unhealthy competition among workers, thereby endangering trade union solidarity in labor disputes.

(VIII) Production planning and management prevent workers from earning more income and become hostile to their attitudes.

(IX) Workers may need to lose wages if the production process is interrupted for reasons beyond their control, such as power outages or the availability of materials.

(X) This system is complicated because it requires a lot of time and effort to develop and maintain. It's also expensive. You need an up-to-date record of each worker's output. In addition, standards are needed and more time studies are needed.

Compatibility:

This system is suitable for the following cases:

The work has a standardized and repetitive character

Output units can be easily measured, inspected, and counted.

This system is very useful in the textile industry (weaving and spinning), mining (coal procurement), and plantations (leaf picking). However, it is difficult to apply when using different shifts for the same task.

Key takeaways:

- Labor turnover can be defined as the number of workers replaced during a particular period relative to the average workforce during the period.

- Some of the causes that contribute to high turnover are the disagreement between work and workers, low wages, bad working conditions.

- Employers can significantly reduce worker turnover, thereby saving labor costs.

- It is a good idea to calculate the labor turnover cost individually

- If a person works longer than normal working hours, the extra time the person worked is known as overtime.

- The loss of time that an employer faces but does not benefit directly is called ideal time.

- The idle time that is not available remains merged into the job or automatic transfer that the worker was hiring.

- It should be remembered that the wages allowed will ultimately lead to a more economical use of machinery, tools, materials, and time.

- Peace rate system has indirect implication that workers should not exceed the average time.

- If his peace rate earnings are equal to his time rate earnings, then the overpayment issue does not occur.

Incentive schemes

Compensation is the sum of the employee's financial income. It consists of income based on working hours or piece work and includes other financial incentives.

Incentives are the stimulation of effort and effectiveness by providing financial or additional equipment.

Incentives are monetary or non-monetary. Financial incentives include wage payments, premiums, bonuses, prizes, and return on investment that exceed the wages paid to hourly workers. Non-monetary incentives include providing the right facilities and background conditions to get the full benefits of personnel for all grades, including promotion plans and training schemes.

Benefits of incentives: -

- To increase production.

- Improve or at least maintain product quality.

- To reduce production costs.

- Increase employee morale, increase efficiency, and ultimately satisfy

Wage level:

In general, the wages a worker receives depends on the supply and demand of that working class.

The following factors should be considered when determining compensation in a particular industry:

The impact of compensation levels on the country's economy.

- Wages paid to employees of similar organizations in the region.

- Employer's ability to pay.

- Employee needs for living standards

Incentive system factors:

Production: --If you are more productive, your production costs will be lower and your employer will ultimately benefit significantly.

Impact on workers: -The wage system should be clear and simple. It must be able to obtain maximum cooperation and should not increase labor turnover.

Fixed Overhead Incidence: --You need to consider the fixed overhead incurred rate for production. As production increases, variable costs per unit remain the same, but fixed costs per unit decrease. Therefore, the increased production efficiency lowers the total cost of production.

Principles applicable to all incentive schemes:

- Compensation must be associated with the efforts involved and must be fair to both employers and employees.

- The scheme is clearly defined and needs to be fully understood by the worker. It needs to provide valuable and achievable goals.