Unit 3

Computation of tax liability

Computation of total income and tax liability of an individual

According to section 2(45) total income means the total amount of income referred to in section 5, computed in the manner laid down in this Act. Section 5 of the act provides scope of total Income-

(1) Subject to the provisions of this Act, the total income of any previous year of a person who is a resident includes all income from whatever source derived which-

(a) is received or is deemed to be received in India in such year by or on behalf of such person; or

(b) accrues or arises or is deemed to accrue or arise to him in India during such year; or

(c) accrues or arises to him outside India during such year:

Provided that, in the case of a person not ordinarily resident in India within the meaning of sub-section (6) of section 6, the income which accrues or arises to him outside India shall not be so included unless it is derived from a business controlled in or a profession set up in India.

(2) Subject to the provisions of this Act, the total income of any previous year of a person who is a non-resident includes all income from whatever source derived which—

(a) is received or is deemed to be received in India in such year by or on behalf of such person; or

(b) accrues or arises or is deemed to accrue or arise to him in India during such year.

The stepwise procedure for computation of total income and tax liability of an individual are stated below-

Step 1: Compute the income of an individual under 5 heads of income on the basis of his residential status.

Step 2: Income of any other person, if includible u/ss 60 to 64, will be included under respective heads.

Step 3: Set off of the losses if permissible, while aggregating the income under 5 heads of income.

Step 4: Carry forward and set off of the losses of past years, if permissible, from such income.

Step 5: The income computed under Steps 1 to 4 is known as Gross Total Income from which deductions under sections 80C to 80U (Chapter VIA) will be allowed. However, no deduction under these sections will be allowed from short-term capital gain covered under section 111A, any long-term capital gain and winning of lotteries etc., though these incomes are part of gross total income.

Step 6: The balance income after allowing the deductions is known as total income which will be rounded off to the nearest Rs. 10.

Step 7: Compute tax on such Total Income at the prescribed rates of tax.

Step 8: Allow rebate of maximum Rs. 2,500 under section 87A in case of resident individual having total income upto Rs. 3,50,000. For details see below.

Step 9: Add surcharge @ 10% on total income exceeding Rs. 50,00,000 and upto Rs. 1 crore and 15% of such income tax in case of an individual having a total income exceeding Rs. 1 crore.

Step 10: Add education cess @ 2% and SHEC @ 1% on the tax (including surcharge if applicable).

Step 11: Allow relief under section 89, if any.

Step 12: Deduct the TDS, advance tax paid for the relevant assessment year and double taxation relief under section 90, 90A or 91. The balance is the net tax payable which will be rounded of nearest ten rupees and must be paid as self-assessment tax before submitting the return of income.

Aggregation of income

Aggregated income of the assessee includes the following incomes:

Income of the assessee

Deemed Incomes

Clubbing of Incomes

Share of a member in the income of (a) Association of persons (AOP) or (b) Body of individuals (BOI)

Deemed incomes

There are certain such incomes or amounts which apparently are not the income of the assessee even then they are deemed to be the income of the assessee under the various provisions of the Income Tax Act. Such incomes are added to the income of assessee and are called 'Deemed Incomes'. Such deemed incomes or amounts are as under:

- Cash Credits (Section 68)

Any amount credited in the books of accounts of assessee in the previous year for which assessee does not offer satisfactory explanation regarding nature and source of such credit, to the assessing officer then such credited amount may be added to the income of assessee and tax may be charged on it. Share application money, share capital, security premium reserve etc. if found credited in the accounts of closely held company, then it will be deemed unexplained unless it is explained to the satisfaction of assessing officer by the resident person in whose name such credit is recorded in the books of such company. However, if such explanation does not satisfy the Assessing Officer (A.O.), the amount so credited shall be deemed to be the income of the company in whose account such amount was found credited. This is to be noted that, this provision is not applicable, if the sum is recorded in the name of a Venture Capital Fund or a Venture Capital Company. The unexplained income shall be taxable @ 60% + surcharge (if applicable) + 4% Health and Education Cess (HEC).

2. Unexplained Investments (Section 69)

If in the relevant previous year, the assessee has made investments which are not recorded in the books of accounts, if any maintained by him for any source of income, and the assessee offers no explanation about the nature and source of money invested or the explanation offered by him is not satisfactory in the opinion of the Assessing Officer, the value of the investments may be deemed to be the income of the assessee for such previous year and tax will be imposed on such income.

3. Unexplained Money etc. (Section 69 A)

If in any financial year, the assessee is found to be the owner of any money, bullion, jewellery or other valuable article which is not recorded in the books of accounts, if any, maintained by him for any source of income and the assessee offers no explanation about the nature and source of acquisition of money, bullion, jewellery and other valuable article or the explanation offered by him is not in the opinion of Assessing Officer satisfactory, the money and the value of the bullion, jewellery, or other valuable article may be deemed to be the income of the assessee for such financial year and will be included in his total income and then, tax will be imposed on it.

4. Investment Amount etc not Fully Disclosed in the Books of Accounts (Section 69 B)

If in any financial year, the assesse has made investments or is found to be the owner of any bullion jewellery, or other valuable article and the Assessing Officer finds that the amount expanded on making such investments or in acquiring such bullion, Jewellery or other valuable articles exceeds the amount recorded in this behalf in the books of accounts maintained by the assessee for any source of income and the assessee offers no explanation about such excess amount or the explanation offered by him is not, in the opinion of the Assessing Officer is satisfactory, the excess amount may be deemed to be the income of the assessee for such financial year, in which the investment has been taken and the assessee is being found to be the owner of the investment and such income will be included in his total income and tax will be imposed.

5. Unexplained Expenditure etc. (Section 69 C)

If in any financial year, an assessee has incurred any expenditure and the assessee is unable to give a satisfactory explanation about the source of money for such expenditure or part thereof, then such expenditure is deemed to be his income for that financial year and added to his total income and then tax will be imposed. Such unexplained expenditure which is deemed to be the income of the assessee shall not be allowed as a deduction under any head of income.

6. Amount Borrowed or Repaid on Hundi (Section 69 D)

Amount borrowed on hundis and its repayment must be made by Account Payee Cheque otherwise amount of such borrowing or amount repaid shall be treated as the income of the person borrowing or repaying the amount for the previous year in which such transaction is made. Repayment of the amount shall include the amount of interest on the amount borrowed. It must be noted that if any amount borrowed on a Hundi and which has been deemed as income, it shall not be deemed as income again when such amount is repaid.

7. Taxation of Deemed Incomes

Incomes falling under Sections (68, 69, 69 A, 69B, 69C and 69D) as deemed incomes shall be charged to tax @ 30% plus (Surcharge and Cess as applicable). In the aforesaid Section, no deduction in respect of any expenditure or allowance or set off of any loss shall be allowed to the assessee in computing deemed income.

Clubbing of incomes

According to these provisions to the extent of transfer of income to the other person or to the extent of income earned by such person on such transfers shall be included in the total income of the assessee. Such inclusion of income of other person in the income of the assessee is called ‘Clubbing of Income’. Provisions of Clubbing of Income are as under:

1. Transfer of Income without Transfer of Assets

If an income earned through an asset is transferred by a person to another person without transferring the ownership of the asset, the income from such asset shall be deemed to be the income of the transferor and shall be included in his total income.

2. Revocable Transfer of Assets (Section 61)

Where a revocable transfer is made of an asset by one person to another person, any income arising or derived from such assets shall be deemed to be the income of the transferor and shall be included in his total income. A transfer shall be deemed to be revocable if

i)It contains any provision for the retransfer directly or indirectly of the whole or any part of the income or assets to the transferor, or

Ii) It (Transfer) in any way, give the transferor a right to reassume power directly or indirectly over the whole or any part of the income or assets.

Transfer includes any settlement, trust, covenant, agreement or arrangement (Sec. 63).

3.Salary, Commission, Fees, or Any Other Remuneration to the Spouse (Section 64)

In computing the total income of an individual, there shall be included all such income as arises directly or indirectly to the spouse of such individual by way of salary, commission, fees or any other form of remuneration whether in cash or in kind from a concern in which such individual has a substantial interest. However, these provisions will not apply on the income of such spouse who possesses Technical or Professional Qualifications and the income is solely attributable to the application of his or her Technical or Professional knowledge and experience. In case of a company, an individual is considered as deemed to have substantial interest, if he beneficially has atleast 20% equity shares along with his relatives at any time during the previous year. The shares must carry voting rights. In any other case (where the concern is not a company), the individual along with his relatives is entitled to at least 20% of the profits of the concern at any time during the previous year. If both spouse has substantial interest in a concern and both are in receipt of remuneration from such concern, the remuneration shall be clubbed in the income of that spouse (husband or wife) whose total income is higher excluding such remuneration. Spouse means husband or wife and the clubbing is limited to the incomes of salary, commission, fees or any other remuneration received by the spouse, directly or indirectly and in cash or kind.

4. Income from Assets Transferred to Spouse [Section 64 (1) iv]

Where an individual transfers his asset (excluding house property) directly or indirectly, to his spouse, any income from such asset is deemed to be the income of the transferor. However, these provisions will not apply in the following circumstances:

i) If the transfer is made for adequate consideration.

Ii) If the transfer is made under an agreement between the spouses to live apart. Such separation may be judicial or voluntary. In the cases, where the consideration is not adequate, proportionate income shall be included in the income of the transferor. The income from house property transferred to spouse shall be taxed under the head 'Income from House Property' in the hands of transferor and not in the hands of transferee.

5. Income from Assets Transferred to Daughter-in-law (Son's wife) [Section 64 (1) (vi)]

Income arising from transfer of an asset by an individual directly or indirectly on or after the 1st day of June 1973 without adequate consideration to son's wife (daughter-in-law) is included in the total income of the transferor.

6. Income from Assets Transferred to a Person or Association of Persons for the Benefit of Spouse [Section 64 (1) (vii)]

Income arising from transfer of an asset directly or indirectly by an individual without adequate consideration to a person or Association of Persons for the immediate or deferred benefit of his or her spouse shall be included in the total income of the transferor to the extent it is for the benefit of the spouse.

7. Income from Assets Transferred to a Person or Association of Persons for the Benefit of Son's Wife [Section 64 (1) (viii)]

Income arising from transfer of an asset after 31.05.1973, directly or indirectly by an individual without adequate consideration to a person or Association of Persons for the immediate or deferred benefit of son's wife, shall be included in the total income of the transferor to the extent it is for the benefit of the son's wife.

8. Income to the Spouse or Son's wife from investment of Transferred Asset

Where the individual has transferred any asset or assets directly or indirectly to the spouse or son's wife and such assets are invested by the transferee.

a) In any business, such investment being not in the nature of contribution of capital as a partner in a firm or for being admitted to the benefits of partnership in a firm, the amount as calculated in the following manner shall be included in the total income of the transferor =

Value of the asset transferred by the Transferor on the 1st day of previous Year/ Total Investment in the business by the transfer as on the 1st day of previous year × Income from the business to the transferee

b) In any business, such investment in the nature of contribution of capital

As a partner in a firm, the amount as calculated in the following manner,

Shall be included in the total income of the transferor =

Such capital contribution of the transferee as on 1st day of previous year/ Total capital contribution of the transferee as on 1st day of previous year × Total Income received by the transferee from the firm

Income of a minor child

Every income of a minor child not being a minor child suffering from any, disability of the nature specified in Section 80 U shall be included (clubbed) in the income of his/her parent. Income includes both which arises or accrues to the minor. However, the following incomes shall not be included in the total income of parent:

a) Income as arises or accrues to the minor child on account of any manual work done by him; or

b) Income as arises or accrues to the minor child from any activity involving application of his skill, talent or specialized knowledge and experience.

Rules of clubbing of a minor's income in the income of parent are as under:

a) Where the marriage of his (minor's) parent subsists, income shall be clubbed in the income of that parent whose total income (excluding the income of minor child) is greater, for example, if in the previous year, exclusive income of mother is Rs 6,00,000 and father’s income is Rs 7,00,000 (without adding minor’s income in both the cases), and the minor’s income in the previous year is Rs 2,00,000, then, minor’s income shall be included in the income of the father because his exclusive income is greater.

b) Where the marriage of his parent does not subsist, the income of the minor child shall be included (clubbed) in the minor child in the income of that parent who maintains the minor child in the previous year.

Where any income of minor is once included in the total income of either parent, any such income arising in any succeeding year shall not be included in the total income of the other parent unless the Assessing Officer is satisfied and gives approval for doing so. If a minor child's income is included in the total income of an individual (any parent), such individual shall be entitled to the following exemption in respect of each minor child separately:

The income of the minor child so included

Or

Rs. 1,500 (Whichever is less)

Income from converted property

If an individual who is a member of H.U.F. Converts any asset owned by him into asset of HUF without adequate consideration after 31.12.1969, then the income from such asset shall be deemed to be the income of the individual and not of the H.U.F. And shall be included in the total income of the transferor (individual). If such converted property is partitioned subsequently, the income earned/received from such converted property or transferred property as is received by the spouse of the transferor, shall be deemed to be the income of the transferor and shall be included in his total income.

Income from the accretion to assets

Income arising to the transferee from the property transferred without consideration to him is taxable in the hands of the transferor. However, if an income arises from accretion of such property or from accumulated income of such property to the transferee, it will not be included in the total income of the transferor and shall be taxable in the hands of the transferee.

Clubbing of negative incomes (losses)

Losses are also called Negative Incomes. Since incomes of other persons (transferee) may be clubbed in the income of transferor, the negative incomes or losses shall be taken into account in computing the income of transferor for such purpose. Thus, it may be concluded that for the purpose of clubbing provision income includes, loss also.

Benami Transaction:

When a person enters into a transaction in the name of a person other than the real person, it is called Benami Transaction and the person in whose name the transaction is made is called Benamidar. The purpose of such transaction used to avoid tax. If the Assessing Officer considers that a particular transaction is Benami, then, he may treat income of such Benami Transaction as the income of real person and it is taxed in the hands of real person.

Cross Transactions/Transfers:

Cross Transfers are the transfers which are intimately connected by agreement so as to form part of a single transaction, and each transfer constitutes consideration for the other. In such cross transfers, income shall be clubbed in the hands of deemed transferor and the provisions of Section 64 will be applicable.

Aggregation of income

Section 2 (45) describes Total Income for which an assessee is chargeable to tax and which is computed as per the provisions and the manners prescribed in the Act. It means, that the Total Income of an assessee includes all such incomes which are chargeable to tax however, there are circumstances in which such income are also included in assessee's Total Income, on which income tax is not payable. The Procedure of including such incomes in an assessee's Total Income, on which income tax is not payable, is termed as 'Aggregation of Income'. According to Section 66 of the Act, in computing the total income of an assessee, there shall be included all income on which no income tax is payable.' According to Section 86 of the Act, share of an assessee in the income of an association of persons (AOP) or Body of Individuals (BOI) is such income. Rules for inclusion of its share are as under:

1) If an assessee is a member of Association of Persons (AOP) or Body of Individuals (BOI), the share of assessee in AOP or BOI shall be included in his total income, However, if the AOP or BOI is liable to pay tax on its total income, the assessee shall be entitled to rebate of such income tax on such share of income including any remuneration at the average rate of income tax.

2) Where the assessee is a member of AOP or BOI but such AOP or BOI is not liable to pay tax on its total income, the assessee shall not be entitled to rebate of income tax on his share of income from such AOP or BOI. It means the assessee will pay tax on such income.

3) If the total income of AOP or BOI is chargeable to tax at the maximum marginal rate or any higher rate, under any of the provision of this act, the share income of the member assessee of such AOP or BOI shall not be included in his Total Income. In such case, the assessee's share of income from AOP or BOI shall be exempt from tax.

Key Takeaways

• There are certain such incomes or amounts which apparently are not the income of the assessee even then they are deemed to be the income of the assessee under the various provisions of the income tax act. Such incomes are added to the income of assessee and are called 'deemed incomes'.

Set off losses

An assessee may have various sources of income under any head of income but this is not necessary that in a previous year all these sources will generate income only. In fact, there may be a condition in which one or more source of income may generate losses while some other source of income may generate profit or gains under the same head of income. Since assessee is taxed on the net income, such losses are made good (Adjusted) against the gains or profits of other sources. This adjustment of losses is called 'Setting off of Losses'. Similarly, there may be profit under one head of income and loss in another head of income. This loss of one head can also be set off (Adjusted) against the profits/gains of another head.

Following are the provisions of Income Tax Act relating to set off of Losses:

- Inter Source Adjustment (Set off) (Section 70)

Where the net result for any assessment year in respect of any source falling under any head of income is a loss, the assessee shall be entitled to have the amount of such loss set off against the income from any other source under the same head. This is called Inter-Source Adjustment. For example, if an assessee has four house properties. Three of them yield net taxable income, but from the fourth there is net loss. The assessee can set-off the loss of one house property against the income of the remaining house properties. Similarly, if an assessee has four businesses of different nature in a particular year, from two businesses there is a taxable profit and from remaining two businesses there is loss. The loss of these two businesses can be set off against the profits of the other two businesses.

2. Inter Head Adjustment (Set off) (Section 71)

Where in respect of any assessment year the net result of the computation under any head of income is a loss, the assessee shall be entitled to have the amount of such loss, set-off against his income, if any, assessable under any other head of income.

3. Non-Speculation Business

General Business includes any non-speculation business. Any loss from business (except speculation business) or profession is eligible to be set-off against any other income falling under the same head or any other head including income from speculation business but excluding income under the head 'Salaries'. Losses of illegal business cannot be set-off against profits of a legal business. However, such losses (illegal losses) can be set off against profits of illegal business. Losses of discontinued business can also be set-off.

4. Set-off of Losses of Speculation Business [Section 73(1)]

Losses related with speculation business can be set off only from profits and gains (if any) of another similar business (i.e. speculation business) carried on by the assessee and not against the income of any other head.

5. Set off of Losses of Specified Business [Section 73A] (w.e.f. AY 2010-11)

Any loss computed in respect of any specified business referred to in Section 35 AD shall not be set off except against profits and gains, if any, of any other specified business. It cannot be set off from the income of any other business.

6. Set off of Losses under the Head Capital Gains

Capital Losses can be (a) Short-term and (b) Long-term.

i) Short-term capital Loss can be set off from any capital Gain i.e. Short term gain or Long-term gain.

Ii) Long-term capital Loss can only be set off against Long-term Capital Gains.

7. Set-off of Losses from Owning and Maintaining Race Horses [Section 74A (3)]

The amount of the loss incurred by the assessee in the activity of owning and maintaining race horses in any assessment year shall be set off only against income of same activity (i.e. owning and maintaining race horses). This type of loss cannot be set off against the income from any other source.

8. Set off of Losses of Lottery, Betting, Gambling, Crossword Puzzles or Card Games etc

These losses are not allowed to be set off against any income including winnings of lotteries, crossword puzzles, races, card games etc.

9. Set off of Losses of Partnership Firm

Where the assessee is a firm, its losses can be set off from its own (firm's) income. The rules of setting off losses shall be the same as they (rules) apply in case of non – firm assessee and explained earlier. No partner can set off his share of loss in the firm against his/her personal income.

10. Set off of Losses of Association of Persons (AOP) or Body of Individuals (BOI)

Losses of AOP or BOI can be set off from their own income. The rules for setting off of losses shall be the same as they apply in case of general assessee. Members of AOP or BOI cannot set off their share of loss in the losses of AOP or BOI, from their personal income.

Carry forward losses

All losses cannot be carried forward for setting off in succeeding years. Only following specified losses are allowed to be carried forward and set off in succeeding assessment year/years:

1. Loss from House Property [Section 71(B)]

Loss under the head 'Income from House Property' can be set off against any other head of income subject to a maximum Rs. 2 Lakhs for any assessment year and any unabsorbed portion of such loss can be carried forward to be set off against the income only under the 'Income from House Property' in maximum subsequent 8 assessment years.

2. Losses of General Business [Section 72]

It is not possible to set off full amount of losses of general business in the same previous year, such 'Not Set off Losses' can be carried forward and set off against the profits of subsequent year or years subject to following provisions:

• Such 'Not Set off Losses' can be carried forward and set off only against the profits under the head 'Profits and Gains of Business or Profession' Thus, if 'Not Set off Losses' are carried forward and set off in subsequent years, such losses cannot be set off against any other head of income except business or profession income.

• Such 'Not Set off Losses' can also be set off against incomes’ (not falling under the head ‘Profits and Gains of Business or Profession’) which arises due to a Business Activity.

• Such 'Not Set off Losses' shall be carried forward maximum for 8 assessment years immediately succeeding the assessment year for which the loss was first computed.

• The assessee who owns the business at the time when it (business) suffered losses is entitled to carry forward such losses. Thus, if the business is transferred to a new owner, then the new owner cannot carry forward 'Not Set off Losses.'

• Not set off Losses can be carried forward and set off against profits or gains of business or profession even if the business in which loss incurred has been discontinued.

• Brought forward losses of a specified business (referred to in Section 35 AD) can be set off in the subsequent years against the income of any specified business.

• If a business undertaking is discontinued because of losses due to natural calamities like floods, cyclones etc, but later on revived within 3 years thereafter, the unabsorbed losses of such undertaking shall be carried forward and set off against the profits of the revived business or any other business for maximum upto 8 years as reckoned from the year in which the business is restarted.

• Such loses cannot carried forward and set off unless the details of such losses are furnished in the income tax return filed by the assessee under the provisions of Section 139. However, delay in submission of return may be condoned if new conditions are satisfied.

3. Accumulated Losses and Unabsorbed Depreciation

In addition to business losses (a) unabsorbed depreciation, (b) unabsorbed capital expenditure on scientific research and (c) unabsorbed expenditure on family planning can also be carried forward indefinitely although as per Income Tax Law these are not business losses. These losses can be set off against the income under any head except salaries in the following order:

i) Current year's depreciation

Ii) Current year capital expenditure on scientific research and current year expenditure on family planning to the extent allowed.

Iii) Brought forward business or profession losses [Section 71(1)]

Iv) Unabsorbed depreciation [Section 32(2)]

v) Unabsorbed capital expenditure on scientific research [Section 35(4)]

Vi) Unabsorbed expenditure on family planning [Section 21(1) (9)]

It is necessary that the details of all such losses must be given in the return of income and the return must be filed before due date u/s 139 (1) otherwise the loss cannot be carried forward. The rules for carry forward and set off unabsorbed depreciation and accumulated losses in different situations are as under:

a) In certain cases of Amalgamation [ Section 72A]

As per Section 72 A(1), where there has been an amalgamation of a company

(i) owning an industrial undertaking or a ship or a hotel with another company or,

(ii) a banking company amalgamates with a specific bank or

(iii) one or more public sector company or companies engaged in the business of operation of aircraft amalgamates with one or more public sector company or companies engaged in similar business, the accumulated loss and the unabsorbed depreciation of the amalgamating company for the previous year in which the amalgamation was effected can be carried forward. Thus, subject to certain conditions for set off, the amalgamated company shall be eligible to carry forward and set off the loss and unabsorbed depreciation of the amalgamating company. If the prescribed conditions u/s 72(i) are not complied with, the set off and carry forward shall not be allowed to the company, eligible for doing so.

b) In certain cases of Demerger [ Section 72A]

U/s 72 A(4) in case of a demerger of an undertaking, the accumulated loss and the allowance for unabsorbed depreciation of the demerged company shall be allowed to be carried forward and set off in the hands of resulting company. Such accumulated losses and unabsorbed depreciation transferred by the demerged company to the resulting company can be carried forward and set off by the resulting company.

c) In cases of succession of a firm or a proprietary concern by company:

As per provisions of Section 72 A (6), where a firm or a proprietary concern is succeeded by the company which fulfills the prescribed conditions, the accumulated loss and the unabsorbed depreciation of predecessor firm or proprietary concern shall be deemed to be the loss or allowance for depreciation of the successor company for the previous year in which business reorganization was effected and other provisions of set off and carry forward of loss and unabsorbed depreciation shall apply accordingly.

d) In cases of succession of a private company or an unlisted public company by a Limited Liability Partnership (LPP):

Under the provisions of Section 72 A(6A), due to reorganization of business, a private company or unlisted public company is succeeded by a Limited Liability Partnership fulfilling the conditions laid down in Section 47 (xiii) (b), the accumulated loss and the unabsorbed depreciation of the predecessor company shall be deemed to be the loss and the unabsorbed depreciation of the predecessor company, shall be deemed to be the loss or allowance for depreciation of the successor Limited Liability Partnership of the previous year in which the such succession has taken place, other provisions of set off and carry forward of loss and depreciation shall apply accordingly.

e) In cases of scheme of amalgamation of Banking Company in certain cases [ Section 72AA]

Under the provisions of Section 72 AA, if there has been an amalgamation of Banking Company with any other Banking Institution, under a scheme sanctioned and brought into force. Other provisions of this Act relating to set off and carry forward of loss and allowance for depreciation shall apply accordingly.

f) In cases of Business Reorganization of Co-operative Banks

[Section 72AB]

Under the provisions of Section 72 AB, if two cooperative Banks have an amalgamation, then, the accumulated loss and unabsorbed depreciation of the predecessor Co-operative Bank can be set off and carry forward by the successor co-operative Bank. All other provisions of the Act relating to set-off and carry forward of the losses and unabsorbed depreciation shall apply accordingly.

4.Loss of Speculation business [Section 73]

Where it is not possible to fully set off losses of speculation business against the profits of another speculation business in the same year then 'Not Set off Losses' can be carried forward for the purpose of setting off such losses from the profits of speculation business. However, such carry forward of 'Not Set off Losses' can be made for a maximum period of 4 assessment years immediately succeeding the assessment year for which the loss was first computed.

5. Losses of Specified Business [Section 73A]

According to Section 73 A, for any assessment year if any loss computed in respect of Specified Business has not been wholly set off against any other Specified Business in the same assessment year then 'Not set off' such losses can be carried forward in the following assessment year, and

i) It shall be set off against the profits and gains, if any, of any Specified Business carried on by him assessable for the assessment year.

Ii) If the loss cannot the wholly so set off, the amount of loss ‘not so set off’ shall be carried forward to the following assessment year and so on till it is fully set off out of profits of any Specified Business.

6. Capital Losses [Section 74]

a) 'Not Set off' Short Term Capital Loss of a previous year many be carried forward to be set off against the Capital Gains (whether Long-term Capital Gain or Short-term Capital Gain) arising in eight (8) subsequent years immediately succeeding the assessment year for which the loss was first computed.

b) 'Not Set off' Long-Term Capital Loss of a previous year may be carried forward to be set off against the Long-Term Capital Gains, arising in subsequent eight (8) years immediately succeeding the assessment year for which the loss was first computed.

7. Losses on Account of Owning and Maintaining Race Horses [Section 74A]

'Not Set Off' Losses from the activity of Owning and Maintaining Race Horses may be carried forward for maximum 4 assessment years immediately succeeding the assessment year in which such loss was first computed. Such 'Not Set off Losses' can be carried forward but are allowed to be set off from the profits of owning and Maintaining Race Horses only subject to the condition that such activities must have been continued till the losses are carried forward. If such activities related to race horses are discontinued, losses of such discontinued, losses of such discontinued business cannot be carried forward.

8. Losses of Firms

Partners of the firm share the profits of the firm and it is exempt in their hands but losses of the firm are not shared among the partners. The law related to set off and carry forward of losses of firms are broadly same as already discussed in the previous pages, however, some main points are given as under:

a) The firm can only set off and carry forward and set off its own losses and not the partners.

b) Firm's "Not Set Off" business losses can be carried forward for 8 assessment years and set off against business income of subsequent years.

c) Unabsorbed Depreciation, Capital Expenditure on Scientific Research and Family Planning are allowed to be carried forward for being set off in the subsequent assessment years and there is no time limit prescribed for such carry forward.

9. Losses of Firm in Case of Change in Constitution [Section 78 (1)]

It there is a change in the constitution of the firm due to retirement or death of a partner, on insolvent of one or more partner, on admission of one or more partners in the firm, or on change in the profit sharing ratio of the partners, then, under above of the any situation and if there is any loss to deceased partner, it cannot be carried forward.

10. Losses in Case of Change in succession of Firm [Section 78 (2)]

Losses of a firm related to pre-succession period cannot be carried forward and set off by successor in the post succession period.

11. Losses in Case of Change in Succession in Business by Inheritance

If the succession has occurred due to inheritance, losses of a firm related to pre-succession period can be carried forward and set off by the successor against the profits of post-succession period.

12. Losses in Case of Certain Companies [Section 79]

i) If there is a change in the shareholders of a company (in which there is no substantial interest of the public in general) in the previous year, then losses incurred in any prior to the previous year shall be carried forward and set off against the income of previous year provided that shareholders having 51% voting rights should be old shareholders on the last day of the year or years in which the loss was incurred and the change should be in minority shareholding only.

Ii) In the case of a company, not being a company in which the public are substantially interested but being an eligible start-up as referred to in Section 80-IAC, the loss incurred in any year prior to the previous year shall be carried forward and set off against the income for the previous year, if all the shareholders of such company who held shares carrying voting power on the last day of the year or years in which the loss was incurred:-

a) Continue to hold those shares on the last day of such previous year; and

b) Such loss has been incurred during the period of seven years beginning from the year in which such company is incorporated.

This provision shall not apply in the following cases:

i) The death of a shareholder.

Ii) On account of transfer of shares by way of gift to any relative of the shareholders making such gift.

13. Losses of Lottery, Crossword Puzzles, Gambling, Betting etc

These losses cannot be carried forward; however, they can be set off in the same year in which they occur against the incomes of the similar sources.

14. Losses in Case of Association of Persons (AOP) or Body of Individuals (BOI)

Losses of AOP or BOI shall be set off and carry forward by the AOP or BOI itself. It will not be apportioned among members. In other words, rules regarding set off and carry forward of losses of AOP or BOI are the same as are applicable in case of a firm assessee.

15. Loss Arising in Case of Bonus Stripping [Section 94 (8)]

Bonus stripping is a situation when purchase or sale of units of a listed company is transacted in a manner, which would result in short term capital loss that can be adjusted against any other capital gains. In Bonus Stripping, shareholders acquire units before the company makes any bonus issue. Once the company issues bonus units, the investors sell the original units which they had held earlier. This can result in to short term capital loss. Later, after one year they dispose the bonus units. This situation enables the shareholders to enjoy two fold benefits.

i) Short-term capital loss for the sale of original units can be set off against any capital gains.

Ii) Benefit of concessional rate of tax at the rate of 10% can be availed on the long-term gains made on the same of the bonus unit.

To prevent the practice of Bonus Stripping Section 94 (8) has been inserted. According to the said Section [94 (8)], if an investor sells or transfers all or any of the original units within a period of 9 months after record date (date on which bonus units is allotted), while continuing to hold all or any of the bonus units, then the loss, if any arising from such transfer shall be ignored for the purpose of calculating income chargeable to tax and the amount of the loss so ignored shall be deemed to be the cost of purchase or acquisition of additional units (bonus units). Thus, the shareholders will not be allowed to book the above mentioned loss on original units against other capital gains.

16. Return of Losses

No loss can be carried forward and set off unless it is determined in pursuance of a return filed as per provisions of Section 139(3) before the Assessing Officer within the time limits prescribed or within the extended time permitted. If the return of loss is filed after the allowed time limit or prescribed time limit, the delay may be condoned, if certain conditions are satisfied.

17. Order of Set Off

If the assessee is entitled to claim depreciation, capital expenditure etc. and carried forward business losses, the order of set off will be as under:

i) Current year depreciation [Section 32 (1)]

Ii) Current year capital expenditure on scientific research and family planning to the extent allowed.

Iii) Brought forward business or profession losses [Section 72(1)]

Iv) Unabsorbed Depreciation [Section 32 (2)]

v) Unabsorbed Capital expenditure on scientific research [Section 35 (4)]

Vi) Unabsorbed expenditure on family planning [Section 36 (i) (ix)]

Key Takeaways

- An assessee may have various sources of income under any head of income but this is not necessary that in a previous year all these sources will generate income only.

Deductions to be made in Computing Total Income [Sections 80A to 80U (Chapter VIA)]

The aggregate of income computed under each head, after giving effect to the provisions for clubbing of income and set off of losses, is known as "Gross Total Income". In computing the total income of an assessee, certain deductions are permissible under sections 80C to 80U from Gross Total Income.

These deductions are however not allowed from the following incomes although these incomes are part of Gross Total Income:

- Long-term capital gains.

- Short-term capital gain on transfer of equity shares and units of equity oriented fund through a recognised stock exchange i.e. short-term capital gain covered under section 111A.

- Winnings of lotteries, races, etc.

- Incomes referred to in sections 115A, 115AB, 115AC, 115ACA, 115AD and 115D.

These deductions are of two types:

- Deductions on account of certain payments and investments covered under sections 80C to 80GGC.

- Deductions on account of certain incomes which are already included under Gross Total Income covered under sections 80-IA to 80U.

Basic Rules of Deductions [Sections 80A/80AB/80AC]

- Deductions cannot exceed Gross Total Income [Section 80A(2)]:

The aggregate amount of deductions under sections 80C to 80U i.e., under Chapter VI-A shall not, in any case, exceed the "Gross Total Income" (exclusive of long-term capital gains, short-term capital gain covered under section 111A, winnings of lotteries, crossword, puzzles, etc. and income referred to in sections 115A to 115AD and 115D) of the assessee. Therefore, the total income after deductions will either be positive or nil. It cannot be negative due to deductions. If the "Gross total income" is negative or nil, no deduction can be permitted under this Chapter.

2. Deduction not allowed to members if allowed to AOP/BOI [Section 80A(3)]:

If a deduction is allowed under the above sections to the AOP or BOI then deductions for the same payment/income will not be allowed to the members of the AOP/BOI. [Section 80A(3)].

3. Double deduction not allowed and deduction cannot exceed the profit of the particular undertaking or unit or enterprise, etc. [Section 80A(4)]:

Notwithstanding anything to the contrary contained in section 10AA or in any provisions of this Chapter under the heading "C.—Deductions in respect of certain incomes" (i.e. deductions under sections 80-IA to 80RRB), where, in the case of an assessee, any amount of profits and gains of an undertaking or unit or enterprise or eligible business is claimed and allowed as a deduction under any of those provisions for any assessment year, deduction in respect of, and to the extent of, such profits and gains shall not be allowed under any other provisions of this Act for such assessment year and shall in no case exceed the profits and gains of such undertaking or unit or enterprise or eligible business, as the case may be.

4. Deduction allowed only when it is claimed by the assessee [Section 80A(5)]:

Where the assessee fails to make a claim in his return of income for any deduction under section 10AA or under any provision of this Chapter under the heading "C.—Deductions in respect of certain incomes" (i.e. sections 80-IA to 80RRB), no deduction shall be allowed to him thereunder.

5. Profit or gain to be recomputed if inter unit or inter business transfer is not at market value [Section 80A(6)]

6. Assessee's duty to place relevant material:

If an assessee approaches a statutory authority for obtaining a concession under the taxing statute, he should in fairness place all the material before the said authority and be also in a position to satisfy the said authority that he was entitled to obtain the concession.

7. Deduction to be allowed in respect of net income included in Gross Total Income [Section 80-AB]:

Where any deduction is required to be made or allowed under any section in respect of any income then for the purpose of computing the deduction under that section, the net income computed in accordance with the provisions of the Income-tax Act (before making any deduction under this chapter i.e. Chapter VIA) shall alone be regarded as the income received by the assessee and which is included in his Gross Total Income. [Section 80AB].

8. Benefits of certain deductions not to be allowed in cases where return is not filed within the specified time limit [Section 80AC]:

Where in computing the total income of an assessee, any deduction is admissible under section 80-IA or section 80-IAB or section 80-IB or section 80-IC or section 80-ID or section 80-IE, no such deduction shall be allowed to him unless he furnishes a return of his income for such assessment year on or before the due date specified under section 139(1).

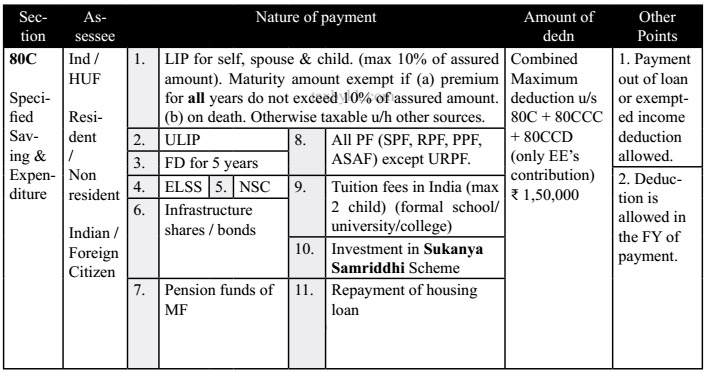

Section 80C (Specified Saving & Expenditure)

Section 80CCC (Annuity Scheme or any other Pension Plan)

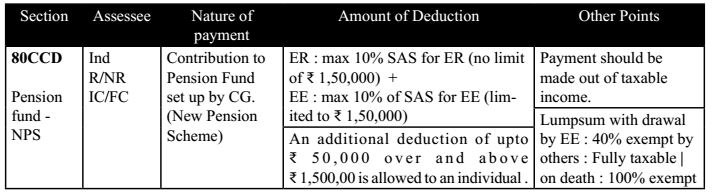

Section 80CCD (New Pension Scheme-NPS)

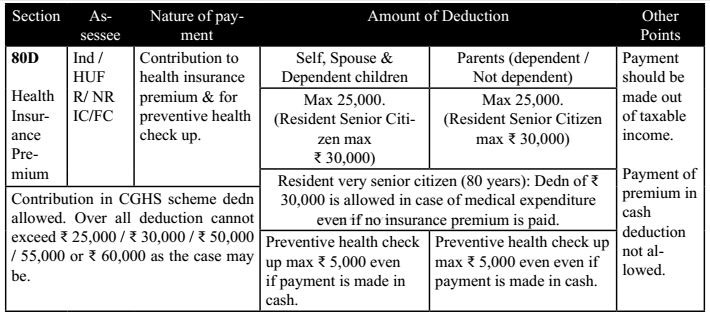

Section 80D (Health Insurance Premium & Health Check Up)

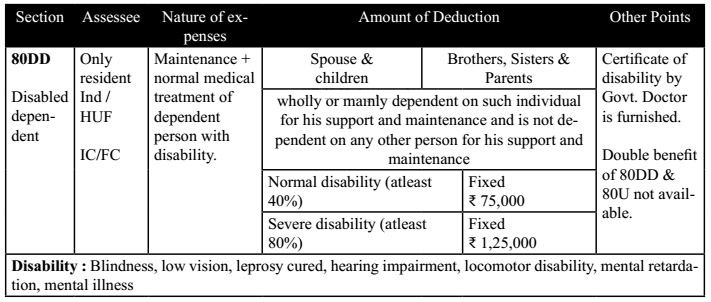

Section 80DD (Disabled Dependent)

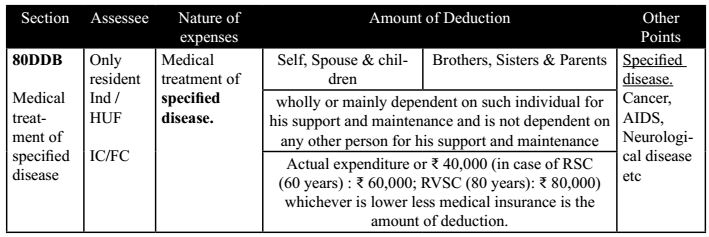

Section 80DDB (Medical Treatment of Specified Disease)

Section 80U (Assessee himself is Disabled)

Section 80E (Interest on Higher Education Loan after +2)

Section 80EE (Interest on Housing Loan)

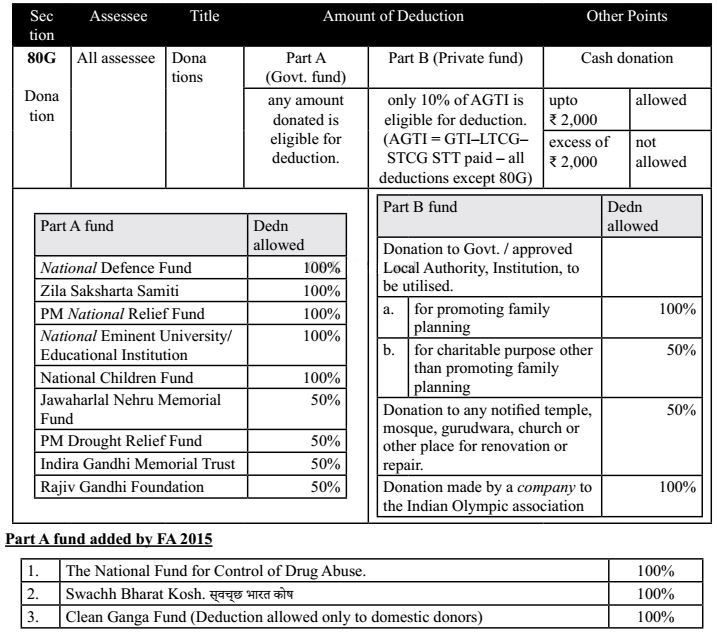

Section 80G (Donations)

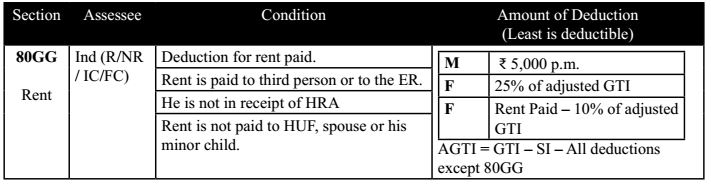

Section 80GG (Rent Paid)

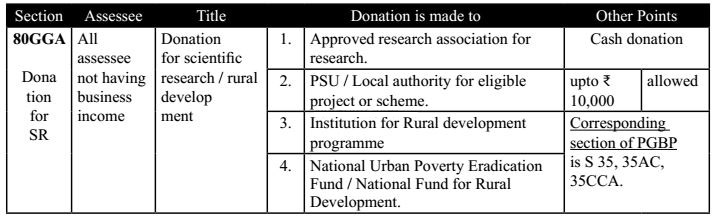

Section 80GGA (Donation for Scientific Research / Rural Development)

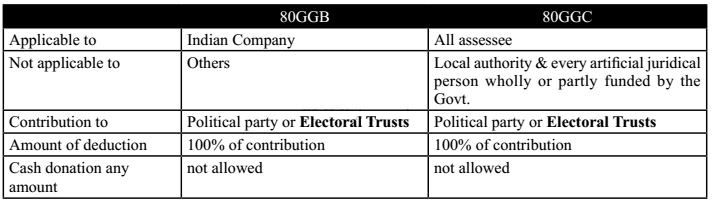

Section 80GGB & GGC

Section 80JJA (Profit from Bio Degradable Wastes)

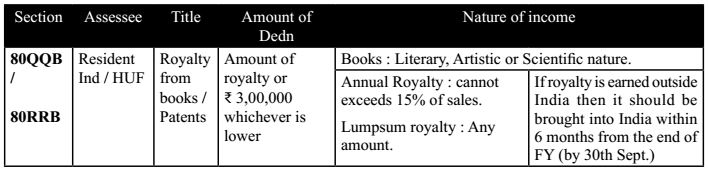

Section 80QQB / 80RRB (Royalty from Books / Patents)

Section 80TTA (Interest on Saving A/c)

References:

1. Singhanai V.K.: Student’s Guide to Income Tax; Taxmann, Delhi.

2. Prasad, Bhagwati: Income Tax Law & practice: Wiley Publication, New Delhi.

3. Dinker Pagare: Income Tax Law and Practice; Sultan Chand & Sons, New Delhi.

4. Girish Ahuja and Ravi Gupta; Systematic approach to income tax; Sahitya Bhawan Publications, New Delhi.

5. Chandra Mahesh and Shukla D.C.: Income Tax Law and Practice; Pragati Publications, New Delhi.