UNIT – 5

Market

MARKET:

In the ordinary sense, the market refers to a place where buyers and sellers meet for the purpose of exchange of goods. However, in economics the term market does not refer to a particular place such. In economics, the term market refers to, ‘An arrangement in which buyers and sellers come in close contact with each other directly or indirectly, to buy or sell goods.’

Following are the features of market:-

1) It does not refer to a particular place. It refers to an arrangement which facilitate transaction between buyers and sellers of goods.

2) The supply from sellers and demand from buyers are the two important forces in market.

3) The exchange of a commodity takes place at a particular price in the market.

4) The price is determined by the forces of demand and supply in the market.

5) The market can be small or large. It can be local, national or international.

6) There may be different markets for a specific commodity. Therefore, there may be different prices in different markets for the same commodity.

7) A market brings together potential buyers and potential sellers of a particular commodity.

TYPES OF MARKET:

The market structure is generally classified on the basis of competition among the sellers. Thus, we have the following types of markets:

1) Perfect competition 2) Monopoly 3) Monopolistic competition

4) Oligopoly 5) Duopoly 6) Pure competition

In this chapter we have to learn about perfect competition, monopoly & monopolistic competition.

1) Perfect competition:

Perfect competition refers to ‘A market structure in which there are large number of buyers and sellers with a single uniforms price for the product which is determined by the forces of demand & supply.’ The price prevailing in perfect competition market is equilibrium price.

Features of perfect competition:-

1) Large number of seller / seller are price takers: There are many potential sellers selling their commodity in the market. Their number is so large that a single seller cannot influence the market price because each seller sells a small fraction of total market supply. The price of the product is determined on the basis of market demand and market supply of the commodity which is accepted by the firms, thus seller is a price taker and not a price maker.

2) Large number of buyers: There are many buyers in the market. A single buyer cannot influence the price of the commodity because individual demand is a small fraction of total market demand.

3) Homogeneous product: The product sold in the market is homogeneous, i.e. identical in quality and size. There is no difference between the products. The products are perfect substitutes for each other.

4) Free entry and exit: There is freedom for new firms or sellers to enter into the market or industry. There is no legal, economic or any type of restrictions. Similarly, the seller is free to leave the market on industry.

5) Perfect knowledge: The seller and buyers have perfect knowledge about the market such as price, demand and supply. This will prevent the buyer from paying higher price than the market price. Similarly, sellers cannot change a different price than the prevailing market price.

6) Perfect mobility of factors of production: Factors of production are freely mobile from one firm to another or from one place to another. This ensures freedom of entry and exit firms. This also ensure that the factors cost are the same for all firms.

7) No transport cost: It is assumed that there are no transport costs. As a result, there is no possibility of changing a higher price on the behalf of transport costs.

8) Non intervention by the government: It is assumed that government does not interfere in the working of the market economy. Price is determined freely according to demand and supply conditions of the market.

9) Single Price: In Perfect Competition all units of a commodity have uniforms or a single price. It is determined by the forces of demand and supply.

*PURE COMPETITION:

According to Prof. Chamberlin, there is said t be ‘Pure competition’ when the first three condition of perfect competition i.e. large number of buyers and sellers, homogenous product & free entry and exit of firm are fulfilled. When monopoly is absent because the first three conditions are fulfilled but the other conditions like perfect knowledge, perfect mobility, absence of transport cost or no Govt. Interference are not fulfilled, then the competition would be ‘PURE’ and not ‘PERFECT’.

Key Points: Large Sellers & Buyers, Same Product Perfect Knowledge, Free entry & exits, mobility, Transport, No Intervention by government, Single Price. |

Price determination under Perfect competition:

The equilibrium price refers to that price at which the demand and supply of a commodity are in equilibrium (equal). In other words Quantity demanded is equal to Quantity supplied. Once equilibrium price is reached there is no tendency for the price to move upward or downwards.

According to Marshall both Demand and Supply are essential in determination equilibrium price. Like the two blades of a scissor that cut piece of paper, demand and supply are important part in determining equilibrium price. Both the blades are useless when they are applied individually. Thus demand and supply are equally important in determining equilibrium price.

This can be explained with the help of following table:

Price (Rs.) | Quantity Demanded (Units) | Quantity Supplied (Units) | Market Condition | Pressure on Price |

5 | 120 | 40 | Shortage | Upward |

10 | 100 | 60 | Shortage | Upward |

15 | 80 | 80 | Equilibrium | Neutral |

20 | 60 | 100 | Surplus | Downward |

25 | 40 | 120 | Surplus | Downward |

In the above table there is Price, Quantity demanded, Quantity supplied, Market condition and change in price. When the price is Rs. 5 Quantity demanded 120 units and quantity supplied 40 units, there is a shortage and pressure on the price is upward (rises). This conditions same at price of Rs. 10. When price is Rs.20 Quantity demanded is 60 units and Quantity supplied is 100 units, there is surplus in the market and pressure on price is downward (decrease). This condition same at price of Rs.25. When the price is Rs. 15 the quantity demanded is equal to the quantity supplied. It is equilibrium price. At this price the market is cleaned, that is neither surplus nor shortage in the market. At the equilibrium price demanded is equal to supply.

2) Monopoly:

The term Monopoly is derived from Greek words, Mono which means Single & Poly which means Selling.

Monopoly refers to a market situation in which there is only a single seller. The firm does not face any competition from any rival. Seller as there is no close substitute for the product. It is opposite of perfect competition. In monopoly the sellers try to control both the price and output. Therefore, In monopoly the seller is price maker. Following are the features of monopoly:

1) Single seller: There are no competitions. Production and supply are controlled by monopolist. He is the Price maker. There is no close substitute for the product of monopolist.

2) No close substitute: There are no close substitutes for the product, so the buyers have no alternative or choice. They have to either buy the product or go without it.

3) No entry: In monopoly there are many restrictions for entry. Thus, other products or firm are not allowed to enter the market. Thus, the monopolist has complete hold over the supply.

4) Price maker: The entire market supply can be controlled by monopolist. He can determine the price of his product. Hence he is a price maker in the market.

5) No distinction between firm & Industry: Since there is only one seller in monopoly, the firm itself is the industry. There is no distinction between the firm and Industry.

6) Super normal Profit: The monopolist always wants to earn supernormal profit. His decision regarding the price and the level of output are guided by the profit maximization motive. Thus, sometimes at price, he supplies the product as per the demand and sometimes he controls the supply of the product and sells the product at high prices.

7) Price discrimination: This implies charging p different prices for the same product to different buyers. The monopolist succeeds in increasing his profit by adopting the technique of price.

8) Control over the market supply: The monopolist has complete hold over the market supply. He is a sole producer of the commodity. Therefore entry barriers such as natural, economic, technological or legal do not allow competitors to enter the market.

Key Points: - Single Seller, No close substitute, No free entry & exits, Price maker, Super normal profit, Price discrimination, Control over supply. |

Types of Monopoly:

1) Natural Monopoly: A natural monopoly arises when a particular natural resources is located or available only in particular locality or region. Hence the producers in that region who control the supply of that resources would enjoy a monopoly in the product which requires that natural resources.

2) Legal Monopoly: It arises due to legal protection given to the producer in the form of patents, trademarks, copy rights, etc. The law prevents the potential competitors for producing identical products.

3) Voluntary Monopoly: When number of big business companies acquire monopoly through voluntary agreement, business firms join together through cartels, syndicates etc.. They are called joint monopolies. Merger and amalgamation may also lead to monopoly. E.g. OPEC (Oil Producing and Exporting countries). This is also known as Joint Monopoly.

4) Simple Monopoly: In simple monopoly the firm has monopoly power over a product or service, but it changes a uniform price to all the buyers.

5) Discriminating Monopoly: In discrimination monopoly, the firm change different prices to different buyers or in different markets for the same product. There is no fixed policy for sale of goods. Policies are changes as per the Market conditions, consumers, etc.

6) State or social Monopoly: When the government owns and controls the production of a goods or services it is called state or social monopoly.

7) Private Monopoly: Private monopoly refers to sole ownership of the supply of goods or services by the private firm or individual. The main objective of private monopoly is profit maximization, for e.g. Tata group and Reliance group

Key points: - Natural, Legal, Voluntary, Simple, discriminating, Social Private. |

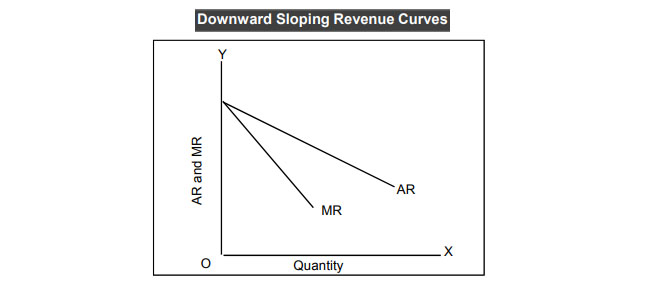

Price curves under a Monopoly

A monopolistic firm is a price-maker, not a price-taker. Therefore, a monopolist can increase or decrease the price. Also, when the price changes, the average revenue, and marginal revenue changes too. Take a look at the table below:

Quantity Sold | Price per unit | Total Revenue | Average Revenue | Marginal revenue |

1 | 6 | 6 | 6 | 6 |

2 | 5 | 10 | 5 | 4 |

3 | 4 | 12 | 4 | 2 |

4 | 3 | 12 | 3 | 0 |

5 | 2 | 10 | 2 | -2 |

6 | 1 | 6 | 1 | -4 |

Let’s look at the revenue curves now:

As you can see in the figure above, both the revenue curves (Average Revenue and Marginal Revenue) are sloping downwards. This is because of the decrease in price. If a monopolist wants to increase his sales, then he must reduce the price of his product to induce:

- The existing buyers to purchase more

- New buyers to enter the market

Hence, the demand conditions for his product are different than those in a competitive market. In fact, the monopolist faces demand conditions similar to the industry as a whole.

Therefore, he faces a negatively sloped demand curve for his product. In the long-run, the demand curve can shift in its slope as well as location. Unfortunately, there is no theoretical basis for determining the direction and extent of this shift.

Talking about the cost of production, a monopolist faces similar conditions that a single firm faces in a competitive market. He is not the sole buyer of the inputs but only one of the many in the market. Therefore, he has no control over the prices of the inputs that he uses.

Role of time element in determination of price are given below:

Time plays an important role in the theory of volume, i.e., price determination because supply and demand conditions are affected by time.

Price during the short-period can be higher or lower than the cost of production, but in the long-period price will have a tendency to be equal to the cost of production.

The relative importance of supply on demand in the determination of price depends upon the time given to supply to adjust itself to demand.

To study the relative importance of supply or demand in price determination, Prof. Marshall has divided time element-into three categories:

(a) Very short period or market period.

(b) Short period.

(c) Long period.

.

(a) Very short period (determination of market price):

Market period is a time period which is too short to increase production of the commodity in response to an increase in demand. In this period the supply cannot be more than existing stock of the commodity.

The supply of perishable goods is perfectly inelastic during market period. But non-perishable goods (durable goods) can be stored.:

Therefore, the supply curve of non-perishable goods above reserve price has a positive scope at first but becomes perfectly inelastic after some price level.

The reserve price y depends upon-(i) cost of storing, (ii) future expected price, (iii) future cost of production, and (iv) seller’s need for cash we will discuss the determination of market price by taking a perishable commodity and determination of market price is illustrated.

DD is the original demand curve and SS the market period supply curve. The demand curve DD (perfectly inelastic) cuts the supply curve SS at point E. Point E, is the equilibrium point and equilibrium price is determined at OP, level.

Increase in demand shifts the demand curve to D,D and the price also increased to OP,. Decrease in demand shifts the demand curve downward to D2D2 and the price too falls to OP It is, thus, clear that in market period price fluctuates with change in demand conditions.

(b) Price determination is short period:

In the short period fixed factors of production remain unchanged, i.e., productive capacity remains unchanged.

However, in the short period supply can be affected by changing the quantity of variable factors.

In other words, during the short period supply can be increased to some extent only by an intensive use of the existing productive capacity.

Therefore, the supply curve in the short-run slopes positively, but the supply curve is less elastic. Determination of price in the short-run is illustrated.

SS is the market period supply curve and SRS is short-run supply curve. The original demand curve DD cuts both the supply curves at E, point and thus OP, price is determined.

Increase in demand shifts the demand curve upward to the right to D,D,. Now with the increase in demand the market price (in market period) rises at once to OP3 because supply remains fixed. But in the short-run supply increases. Therefore, in the short-run price will cuts the SRS curve. If demand decreases opposite will happen.

(c) Price determination in long period (Normal Price):

In the long period there is enough time for the supply to adjust fully to the changes in demand.

In the long period all factors are variable. Present firms can increase on decrease the size of their plants (productive capacity).

The new firms can enter the industry and old firms can leave the market. Therefore, long-period supply curve has a positive slope and is more elastic than short period supply curve.

The shape of supply curve of the industry depends upon the nature of the laws of returns applicable to the industry. Price determination in the long period is illustrated.

DD is the original demand curve and LS is the long period supply curve of the industry. Demand curve DD and supply curve LS both intersect each other at E point and OP price is determined.

This price will be equal to minimum average cost (AC) of production because in the long period firms under perfect competition can only earn normal profits. Suppose these are permanent increase in demand.

With the increase in demand, the demand curve shifts to D1,D1. As a result of increase in demand the price in the market period and short period will rise.

Due to increase in price present firms will earn above normal profit. Therefore, new firms will enter into market in the long period.

As a result of it supply will increase in the long period. In the long period price will be determined at OP1, level because at this price demand curve D1 D2 cuts the LS curve at E2 point.

Price OP1, is greater than previous price OP1, because the industry is an increasing cost industry. This new higher price will also be equal to minimum average cost of production

3) MonopolISTIC COMPETITION:

It is a market structure in which a large number of firms produce and sell products that are differentiated but close substitutes of each other. Monopolistic competition is a mixture of perfect competition degree of monopoly power. Following are the features of Monopolistic competition:

1) Large number of sellers: In a monopolistic competition market there is a large number of sellers. Hence no single seller can control the market supply. Each seller follow his own course is independent.

2) Product differentiation: The most important feature of Monopolistic competition is the product differentiation. Each seller will try hard to make an identity for his brand. Though the products are close substitutes, they will differ from each other in many ways. Differentiation will be clearly evident in the form of brand name. Besides the trademark or brand name, a product is differentiated in terms of colour, size, design, taste, etc. These features can be seen in textile, soap and in many other products.

3) Close substitutes: Though there are many sellers in the market, products sold by the sellers are close substitutes. Garment market is goods example for this situation.

4) Selling cost: Firms in a monopolistic competition promotes sales by incurring selling cost. Selling cost includes all types of costs incurred to promote sales. Selling cost is usually incurred in the form of advertisements, exhibitions, gifts, free samples & so on. Selling cost is incurred to influence consumer’s demand and promotes sales.

5) Nature of Demand curve: An individual firm can sell more products by reducing the price and therefore the demand curve downward sloping. Demand for the produce will be elastic.

6) Free entry & exit: A firm is free to produce a product which is usually a close substitute for the existing products. There is no restriction from the Government or through any business. Similarly there is no restriction for leaving the market for any reasons. In the long run, free entry and exit ensures that the firm earns only normal profit.

7) Concept of group: Chamberlin introduced the concept of group as the substitutes for industry concept. The firm producing identical product, are clubbed together in one industry under perfect competition. However, in the Monopolistic Competition the products are differentiated. All the firms producing close substitutes are taken together in a ‘group concept’. For example – group of firms producing medicines, cement, etc.

Pricing Under Monopolistic Competition

Monopolistic competition is a market structure which has elements of both monopoly and competitive markets.

Essentially a monopolistic competitive market provides freedom of entry and exit, but sellers can differentiate their products. They can set prices because they have an inelastic demand curve.

However, since there is freedom of entry, supernormal profits may encourage more firms to enter the market leading to normal profits in the long term.

The diagram for a monopolistic competition is the same as for a monopoly in the short run.

Supernormal profit encourages new firms to enter in the long run. This reduces existing demand for existing firms and leads to normal profit.

The efficiency of firms in monopolistic competition

Key features of a Monopolistic Competitive Industry

- There are many firms.

- Freedom of entry and exit.

- Firms manufacture differentiated goods.

- Firms have price inelastic demand, therefore, they are price makers because the good is highly differentiated.

- They earn normal profits in the long run but could make supernormal profits in the short term.

- Dynamic efficiency is possible as firms have excess profit to invest in research and development.

- In a monopolistic competitive industry, this is possible the firm does face competitive pressures to cut cost and provide better products.

Examples of Monopolistic Competition

- Restaurants – Generally restaurants compete on quality and as much as the price of food. Product differentiation is a key element of the restaurant business. There are relatively low barriers to entry in opening a new restaurant.

- Saloon-A service which provides a reputation to firms for the quality of their hair-cutting.

- Fashion Industry-In cloths industry, designer label clothes are about the brand and product differentiation.

- TV programmes – Around the world globalization has increased the diversity of television programmes from network. Consumers can choose programs between domestic channels and also imports from other countries such as Netflix.

Questions

- What is market.

- Explain concept of perfect competition.

- Explain concept of Monopoly.

- Explain concept of monopolistic competition.

- Explain types of Monop[oly.

- Explain process of Price determination.