• Purchase order acknowledgements (POAs)

Fully integrated EDI solutions will connect to:

Comparison of in-house vs. outsourced EDI

Five reasons to implement associate degree EDI resolution

1. Processes take too long to cleanly complete.

2. Prices of inaccuracies square measure setting out to add up.

3. Inventory surpluses and stockouts happen frequently.

When points of sale, ecommerce order submission, fulfillment processes, shipment tracking and other systems don’t communicate together, it increases the chances of miscommunication and inventory problems. To manually reconcile all of the information makes forecasting extremely labor intensive and prone to miscalculations. With an integrated EDI solution, ecommerce platforms, accounting, ERP and other business solutions can communicate with each other, enabling the most accurate transmission, collection and analysis of data.

4. Trading partners are becoming impatient.

With the speed of the retail supply chain accelerating, retailers, distributors, vendors, 3PLs and other organizations need to be on the same page. Links in the supply chain that rely on legacy systems and outdated processes can slow down the whole network. Some retailers and brands won’t even consider working with a partner that doesn’t have EDI. The improved efficiency, accuracy and automation that EDI offers an organization can help retain trading partners and secure new opportunities. It can also help businesses obtain value from new trading relationships faster with standardized, streamlined onboarding.

5. Resource limitations have been reached.

As a business grows, resources such as inventory, staffing, space allocation and other needs grow as well. Often organizations run into bottlenecks that hinder the pace of expansion. EDI can add agility, elasticity and scalability to existing assets. With information and forecasting ability, EDI enables tighter management of inventory, staffing, warehouse operations and other assets. When manual data entry requirements are reduced or eliminated, employees that previously performed these tasks can be retrained and redeployed to other positions that help the business perform and grow.

Key Takeaway

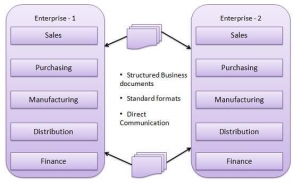

- EDI stands for Electronic Data Interchange. EDI combines a system and processes to give businesses the ability to exchange documents and transactions between trading partners in a standard electronic format. For example, a retailer can send a purchase order (PO) to a vendor digitally through EDI, rather than send a paper document or fax.

- EDI automation can reduce or eliminate paper documents, while also ensuring no transactions get lost in the shuffle. EDI vastly diminishes or eliminates manual data entry and processing needs, as well as the costly human errors that come with it. EDI also serves as a line of defense against improper documentation and fraud.

EDI stands for Electronic Data Interchange. EDI is an electronic way of transferring business documents in an organization internally, between its various departments or externally with suppliers, customers, or any subsidiaries. In EDI, paper documents are replaced with electronic documents such as word documents, spreadsheets, etc.

|

Fig 1 - EDI

Following are the few important documents used in EDI −

- Invoices

- Purchase orders

- Shipping Requests

- Acknowledgement

- Business Correspondence letters

- Financial information letters

Following are the steps in an EDI System.

- A program generates a file that contains the processed document.

- The document is converted into an agreed standard format.

- The file containing the document is sent electronically on the network.

- The trading partner receives the file.

- An acknowledgement document is generated and sent to the originating organization.

Following are the advantages of having an EDI system.

- Reduction in data entry errors.− Chances of errors are much less while using a computer for data entry.

- Shorter processing life cycle− Orders can be processed as soon as they are entered into the system. It reduces the processing time of the transfer documents.

- Electronic form of data− it is quite easy to transfer or share the data, as it is present in electronic format.

- Reduction in paperwork−As a lot of paper documents are replaced with electronic documents, there is a huge reduction in paperwork.

- Cost Effective−As time is saved and orders are processed very effectively, EDI proves to be highly cost effective.

- Standard Means of communication− EDI enforces standards on the content of data and its format which leads to clearer communication.

Key takeaway

- EDI stands for Electronic Data Interchange. EDI is an electronic way of transferring business documents in an organization internally, between its various departments or externally with suppliers, customers, or any subsidiaries. In EDI, paper documents are replaced with electronic documents such as word documents, spreadsheets, etc.

Electronic Data Interchange (EDI) is the electronic interchange of business information using a standardized format; a process which allows one company to send information to another company electronically rather than with paper. Business entities conducting business electronically are called trading partners.

Many business documents can be exchanged using EDI, but the two most common are purchase orders and invoices. At a minimum, EDI replaces the mail preparation and handling associated with traditional business communication. However, the real power of EDI is that it standardizes the information communicated in business documents, which makes possible a "paperless" exchange.

The traditional invoice illustrates what this can mean. Most companies create invoices using a computer system, print a paper copy of the invoice and mail it to the customer. Upon receipt, the customer frequently marks up the invoice and enters it into its own computer system. The entire process is nothing more than the transfer of information from the seller's computer to the customer's computer. EDI makes it possible to minimize or even eliminate the manual steps involved in this transfer.

The process improvements that EDI offers are significant and can be dramatic. For example, consider the difference between the traditional paper purchase order and its electronic counterpart:

|

Key takeaway

- Electronic Data Interchange (EDI) is the electronic interchange of business information using a standardized format; a process which allows one company to send information to another company electronically rather than with paper. Business entities conducting business electronically are called trading partners.

- Many business documents can be exchanged using EDI, but the two most common are purchase orders and invoices. At a minimum, EDI replaces the mail preparation and handling associated with traditional business communication. However, the real power of EDI is that it standardizes the information communicated in business documents, which makes possible a "paperless" exchange.

The electronic payment system has big more and more over the last decades thanks to the growing unfold of internet-based banking and searching. Because the world advances a lot of with technology development, we are able to see the increase of electronic payment systems and payment process devices. As these increase, improve, and supply ever safer on-line payment transactions the proportion of check and money transactions can decrease.

Electronic Payment strategies

One of the foremost in style payment forms on-line square measure credit and debit cards. Besides them, there also are different payment strategies, like bank transfers, electronic wallets, sensible cards or bitcoin notecase (bitcoin is that the most well-liked cryptocurrency).

E-payment strategies may be classified into 2 areas, credit payment systems and money payment systems.

1. Credit Payment System

Credit Card — A variety of the e-payment system which needs the utilization of the cardboard issued by a monetary institute to the cardholder for creating payments on-line or through associate device, while not the utilization of money.

E-wallet — A variety of postpaid account that stores user’s monetary knowledge, like debit and mastercard data to create an internet dealing easier.

Smart card — A plastic card with a micro chip which will be loaded with funds to create transactions; additionally called a chip card.

2. money Payment System

Direct debit — A monetary dealing during which the account holder instructs the bank to gather a selected quantity of cash from his account electronically to pay money for merchandise or services.

E-check — A digital version of associate recent paper check. It’s associate electronic transfer of cash from a checking account, sometimes bank account, while not the utilization of the paper check.

E-cash could be a variety of associate electronic payment system, wherever a particular quantity of cash is keep on a client’s device and created accessible for on-line transactions.

Stored-value card — A card with a particular quantity of cash which will be wont to perform the dealing within the establishment store. A typical example of stored-value cards square measure gift cards.

Pros associated Cons of exploitation an E-payment System

- E-payment systems square measure created to facilitate the acceptance of electronic payments for on-line transactions. With the growing quality of on-line searching, e-payment systems became a requirement for on-line customers — to create searching and banking a lot of convenient. It comes with several edges, such as:

- Reaching a lot of purchasers from everywhere the globe, which ends up in additional sales.

- More effective and economical transactions — It’s as a result of transactions square measure created in seconds (with one-click), while not wasting customer’s time. It comes with speed and ease.

- Convenience. Customers will pay for things on associate e-commerce web site at anytime and anyplace. they merely want a web connected device. As straightforward as that!

- Lower dealing price and attenuated technology prices.

- Expenses management for purchasers, as they'll invariably check their virtual account wherever they'll realize the dealing history.

- Today it’s simple to feature payments to a web site, therefore even a non-technical person could implement it in minutes and begin process on-line payments.

- Payment gateways and payment suppliers provide extremely effective security and anti-fraud tools to create transactions reliable.

- Sounds nice, therefore square measure there any drawbacks?

- E-commerce fraud is growing at half-hour p.a.. If you follow the protection rules, there shouldn’t be such issues, however once a businessperson chooses a payment system that isn't extremely secure, there's a risk of sensitive knowledge breach which can cause fraud.

- The lack of obscurity — for many, it’s not a haul the least bit, however you would like to recollect that a number of your personal knowledge is keep within the info of the payment system.

- The need for net access — As you will guess, if the net affiliation fails, it’s not possible to complete a dealing, get to your on-line account, etc.

- E-commerce, still as m-commerce, is obtaining larger year once year, therefore having associate e-payment system in your on-line store could be a should. It’s straightforward, quick and convenient, therefore why not have one?

- Still, one in every of the foremost in style payment strategies square measure credit and open-end credit payments, however individuals additionally select some alternatives or native payment strategies. If you run an internet business, determine what your target market desires and supply the foremost convenient and relevant e-payment system.

Key takeaway

- The electronic payment system has grown increasingly over the last decades due to the growing spread of internet-based banking and shopping. As the world advances more with technology development, we can see the rise of electronic payment systems and payment processing devices. As these increase, improve, and provide ever more secure online payment transactions the percentage of check and cash transactions will decrease.

What is an electronic funds transfer?

An electronic funds transfer (EFT) is that the electronic transfer of cash over an internet network. Electronic funds transfers may be performed between identical bank and a distinct one, and might be accomplished with many differing types of payment systems. Associate in Nursing newt may be initiated by someone or by an establishment sort of a business and infrequently doesn’t need far more than a checking account in sensible standing.

Deeper definition

An electronic funds transfer may be a wide used methodology for moving funds from one account to a different employing a electronic network. Electronic funds transfers replace paper-based transfers and human intermediaries, however give the client with the convenience of doing her own banking.

Every time a banking client uses her credit or revolving credit, whether or not at a physical location or on-line, she’s partaking in Associate in Nursing electronic funds transfer. Any preauthorized charges, like direct deposits or utility bills, conjointly utilize Associate in Nursing newt.

Certain services use EFTs to make a peer-to-peer payment surroundings. In such a scenario, the sender merely uses Associate in Nursing app or web site to point that she needs to send cash to a recipient. Often, this implies causation cash from a checking account to a different checking account, however it will typically mean transferring it to the service itself, from wherever the recipient will withdraw the funds into her checking account manually.

Electronic funds transfers square measure secured by a private number (PIN) or the login info that unlocks the customer’s on-line banking service. an automatic financial organisation (ACH) processes the payment.

With on-line banking, you'll build your own EFTs. Open saving accounts to urge started.

Electronic funds transfer example

The most widespread kind of electronic funds transfer may be a direct deposit, during which Associate in Nursing worker of an organization preauthorizes her leader to pay her wage directly into her checking account. However, various different electronic funds transfers exist, together with the following:

- ATMs.

- Online peer-to-peer payment apps like PayPal and Venmo.

- Pay-by-phone systems.

- Wire transfers.

- Online or mobile banking.

- Electronic Checks.

There square measure various ways in which of transferring cash from one checking account to account. With the increasing technology, on-line cash transfer has become the simplest means of transferring cash from one bank to a different with none issue. Here square measure 3 major suggests that of transferring cash.

1. NEFT (National Electronic Fund Transfer)

The National Electronic Fund Transfer or NEFT is that the simplest and most likeable kind of cash transfer from one bank to bank.

To make any NEFT dealings, you only would like 2 necessary items of knowledge -- first, account range and second, the IFSC Code of the destination account.

In NEFT, there's no cap on the quantity of cash which will be transferred. However, individual banks could set a limit.

Steps for a NEFT cash transfer

Step 1: visit Fund Transfer tab, and choose 'Transfer to different bank' (NEFT)

Step 2: choose the recipient account and enter the relevant details

Step 3: settle for the (Terms and Conditions)

Step 4: Recheck the main points, if all and complete the method

2. RTGS (Real Time Gross Settlement

A Real Time Gross Settlement or RTGS is sort of like NEFT however the minimum payment and the way it credits to the destination account differs.

If you would like to transfer quite two then you'll use this. there's no higher cap on the quantity.

An RTGS cash transfer happens on a time period basis. The bank of the person to whom the money is transferred gets half-hour to credit it to his/her account.

Steps to create RTGS funds transfer:

Step 1: visit Fund Transfer tab, and choose 'Transfer to different bank' (RTGS)

Step 2: choose the recipient account and enter the relevant details

Step 3: settle for the (Terms and Conditions)

Step 4: Recheck the main points, if all square measure correct, then ensure and complete the method

3. IMPS (Immediate Payment Service)

Immediate Payment Service or IMPs an immediate fund transfer service and it may be used anytime. IMPS may be merely outlined as NEFT+RTGS.

In order to avoid fraud complaints, the cap on dealings limit is ready terribly low. For IMPS transfer, you only ought to apprehend the destination account holder's IMPS id (MMID) and his/her mobile range.

Steps to create IMPS cash transfer:

Step 1:Using your client ID and arcanum into web Banking/Mobile Banking

Step 2: visit Funds Transfer tab (Other Bank Account)

Step 3: choose Debit / open account, mode of transfer as IMPS and beneficiary account

Step 4: Enter the quantity to be transferred and click on Submit

Step 5: Click on the ensure button

Step 6: Recheck all the knowledge and approve the dealings victimization OTP (one time password) received on your registered mobile range

Step 7: And finally, ensure by clicking on the submit button.

Through IMPS, you'll transfer cash 24/7, however RTGS & NEFT may be done solely in operating hours on weekdays + many hours on Saturdays solely. apart from NEFT, RTGS and IMPS, you'll conjointly transfer your cash through UPI and cheque.

1. UPI (Unified Payments Interface):

A Unified Payments Interface may be a time period payment system that enables transactions to be done through any smartphone victimization VPA (Virtual Payment Address).

No checking account detail is required for the money transfer through UPI. solely mobile range or name is decent and therefore the transactions may be done 24/7. UPI-enabled apps enable the transfers up to Rs one large integer.

2. Cheque:

You can transfer cash from your one account to a different account by cheque. you've got to easily draw a stating recipient as your name together with the account range whereby you would like to transfer the quantity together with your signature.

It's done right away at a branch if the transfer is at intervals your bank.

It's done immediately at a branch if the transfer is within your bank.

There is no limit if you want to transfer money from your a/c to another bank a/c, but if you want to withdraw a certain amount, there are restrictions.

Through a cheque, you cannot withdraw more than Rs 50,000 from a non-home branch.

Key takeaway

- An electronic funds transfer (EFT) is the electronic transfer of money over an online network. Electronic funds transfers can be performed between the same bank and a different one, and can be accomplished with several different types of payment systems. An EFT can be initiated by a person or by an institution like a business and often doesn’t require much more than a bank account in good standing.

E-commerce sites use electronic payment, wherever electronic payment refers to paperless financial transactions. Electronic payment has revolutionized the business process by reducing the work, dealing prices, and labor price. Being user friendly and fewer long than manual process, it helps concern to expand its market reach/expansion. Listed below ar a number of the modes of electronic payments −

- Credit Card

- Debit Card

- Smart Card

- E-Money

- Electronic Fund Transfer (EFT)

Credit Card

Payment victimisation mastercard is one in every of commonest mode of electronic payment. mastercard is tiny plastic card with a singular range hooked up with AN account. it's conjointly a magnetic strip embedded in it that is employed to scan mastercard via card readers. once a client purchases a product via mastercard, mastercard establishment bank pays on behalf of the client and client includes a bound fundamental quantity when that he/she pays the mastercard bill. it's typically mastercard monthly payment cycle. Following ar the actors within the mastercard system.

- The card holder − client

- The bourgeois marketer of product UN agency will settle for mastercard payments.

- The card establishment bank − card holder's bank

- The acquirer bank − the merchant's bank

- The card whole for instance , visa or Mastercard.

Credit Card Payment method

Step Description

Step 1 Bank problems and activates a mastercard to the client on his/her request.

Step 2 The client presents the mastercard data to the bourgeois web site or to the bourgeois from whom he/she needs to buy a product/service.

Step 3 Merchant validates the customer's identity by inquiring for approval from the cardboard whole company.

Step 4 Card whole company authenticates the mastercard and pays the dealing by credit. bourgeois keeps the sales slip.

Step 5 Merchant submits the sales slip to acquirer banks and gets the service charges paid to him/her.

Step 6 Acquirer bank requests the cardboard whole company to clear the credit quantity and gets the payment.

Step 7 Now the cardboard whole company asks to clear {the quantity|thequantity|the number} from the establishment bank and therefore the amount gets transferred to the cardboard whole company.

Debit Card

Debit card, like mastercard, could be a tiny plastic card with a singular range mapped with the checking account range. it's needed to own a checking account before obtaining a open-end credit from the bank. the foremost distinction between a open-end credit and a mastercard is that just in case of payment through open-end credit, the number gets subtracted from the card's checking account straightaway and there ought to be adequate balance within the checking account for the dealing to induce completed; whereas just in case of a mastercard dealing, there's no such compulsion.

Debit cards free the client to hold money and cheques. Even merchants settle for a open-end credit promptly. Having a restriction on the number which will be withdrawn during a day employing a open-end credit helps the client to stay a check on his/her disbursement.

Smart Card

Smart card is once more like a mastercard or a open-end credit in look, however it's a little chip embedded in it. it's the capability to store a customer’s work-related and/or personal data. sensible cards are accustomed store cash and therefore the quantity gets subtracted when each dealing.

Smart cards will solely be accessed employing a PIN that each client is allotted with. sensible cards ar secure, as they store data in encrypted format and ar less expensive/provides quicker process. Mondex and Visa money cards ar samples of sensible cards.

E-Money

E-Money transactions visit scenario wherever payment is finished over the network and therefore the quantity gets transferred from one money body to a different money body with none involvement of a middleman. E-money transactions ar quicker, convenient, and saves a great deal of your time.

Online payments done via credit cards, debit cards, or sensible cards ar samples of emoney transactions. Another common example is e-cash. just in case of e-cash, each client and bourgeois have to be compelled to check in with the bank or company issuance e-cash.

Electronic Fund Transfer

It is a really common electronic payment technique to transfer cash from one checking account to a different checking account. Accounts are often within the same bank or completely different banks. Fund transfer are often done victimisation ATM (Automated Teller Machine) or employing a laptop.

Nowadays, internet-based triton is obtaining common. during this case, a client uses the web site provided by the bank, logs in to the bank's web site and registers another checking account. He/she then places asking to transfer specific amount thereto account. Customer's bank transfers the number to different account if it's within the same bank, different wise the transfer request is forwarded to AN ACH (Automated Clearing House) to transfer {the quantity|thequantity|the number} to other account and therefore the amount is subtracted from the customer's account. Once the number is transferred to different account, the client is notified of the fund transfer by the bank.

Key takeaway

- E-commerce sites use electronic payment, where electronic payment refers to paperless monetary transactions. Electronic payment has revolutionized the business processing by reducing the paperwork, transaction costs, and labor cost. Being user friendly and less time-consuming than manual processing, it helps business organization to expand its market reach/expansion. Listed below are some of the modes of electronic payments −

a) Credit Card

b) Debit Card

c) Smart Card

d) E-Money

e) Electronic Fund Transfer (EFT)

The digital token based mostly payment system may be a new sort of electronic payment system that is predicated on electronic tokens instead of e-cheque or e-cash. The electronic tokens square measure generated by the bank or some monetary establishments. therefore {we can|wewill|we square measure able to} say that the electronic tokens square measure cherish the money that are to be created by the bank.

Categories of Electronic Tokens:-

I. money or Real Time:-

In this mode of electronic tokens transactions takes place via the exchange of electronic currency (e-cash).

2. Debit or Prepaid:-

In this electronic payment system the paid facilities square measure provided. It implies that for transactions of data user pay prior to. This technology square measure utilized in positive identification, electronic purses etc.

3. Credit or Postpaid;-

These varieties of electronic token supported the identity of consumers that issue a card, their authentication and verification by a 3rd party. during this system the server demonstrate the purchasers and so verify their identity through the bank. in spite of everything these process the dealing crop up. Example is E-Cheques.

The Digital Token based mostly system have following problems that they're established:-

1. Nature of dealing that instrument is designed:-

In this class, the planning problems with token crop up. it should be designed to handle small payments. it should be designed for typical product. Some tokens square measure designed specifically and different usually. the planning issue involve involvement of parties, purchase interaction and average quantity.

2. means that of Settlement:- The Digital Tokens square measure used once their format should be in money, credit, electronic bill payments etc. Most dealing settlement ways use credit cards whereas different used proxies for values.

3. Approach to Security, namelessness and Authentication:-

Since the electronic token square measure vary from system to system once the business dealing crop up. therefore it's necessary to secure it by intruders and hackers. For this purpose numerous security measures square measure supplied with electronic tokens like the tactic of coding. The coding methodology use the digital signatures of the purchasers for verification and authentication.

4. Risk Factors:-

The electronic tokens is also no-good and if the client have currency on token than no one can settle for it, If the dealing has while between delivery of product and payments to bourgeois then merchant exposes to the chance. therefore it's vital to analysis risk think about electronic payment system.

Key takeaway

- The digital token based payment system is a new form of electronic payment system which is based on electronic tokens rather than e-cheque or e-cash. The electronic tokens are generated by the bank or some financial institutions. Hence we can say that the electronic tokens are equivalent to the cash which are to be made by the bank.

What is a contemporary Payment System?

A modern payment system directly integrates to your purpose of sale and delivers a sturdy payment expertise for each bourgeois and client. It connects merchants to a complete payment scheme, from bourgeois services to link-attached terminal solutions, to hardware procural.

Benefits of a contemporary Payment System

Read on to find out additional regarding the advantages of today’s fashionable payment system.

1. Complete Payment Flexibility

2. Revolutionary valuation

3. Get Paid quicker

4. Secure Payment and POS Integration

5. link-attached terminal Management

6. Lower Operational prices

7. Access to Premium Payment Services

1. Complete Payment Flexibility

In today’s fast retail surroundings, the necessity to fulfill and exceed client expectations is vital to staying relevant amongst your client base. having the ability to just accept all forms and ways of payment will be the distinction between an acquisition and a walk-out. Luckily, a contemporary payment system ensures your business’ ability to just accept all major credit cards, PIN debit, EMV chip, and contactless transactions like credit/debit faucet, Apple Pay, and Samsung Pay. Universal payment acceptance can keep your customers happy, returning, and demonstrate your business’ drive to remain on prime of payment trends.

2. Revolutionary valuation

Although fashionable payment systems cannot cut back interchange rates as set by the mastercard networks, they'll cut back their own process fee mark-ups. Contrary to most, fashionable payment systems don't vie on process rates. Instead, they’re centered on passing through best valuation to ensure their shoppers all-time low per dealing rates on the market.

iQmetrix’s Payment Connect distinguishes itself by providing shoppers with a hybrid Flat Rate and Interchange and valuation model. shoppers access essential bourgeois services for an occasional meet up with transactional value then prime up their payment system with worth superimposed enhancements for one flat rate.

3. Get Paid quicker

You work laborious for your cash, therefore why not get paid even faster? fashionable payment systems run on electronic transactions that ar abundant faster to reconcile, batch, and collect upon over money primarily based systems. Updated system technology and quicker web connections create electronic transactions even speedier. additionally, fashionable payment systems permit merchants to add-on a next day funding choice. Merchants will increase their income by obtaining paid inside twenty four hours when batching.

4. Secure Payment and POS Integration

Although integrated payment (integration between your payment device and your telephone store POS) is changing into additional common, several merchants still use non-integrated payment systems. additionally to being safer than complete payment technology, integration saves you time and cash by pushing the dealing on to the payment terminal rather than having to enter the quantity manually. Integration additionally mechanically updates the invoice once a payment is tendered, permitting you additional accuracy in your accounting and saving you time whereas adaptive at the tip of the night.

5. link-attached terminal Management

Advanced payment systems provide spectacular terminal management code that helps merchants manage all aspects of their payment devices from the comfort of their own workplace. With a time period list of terminal inventory out there on-line, merchants will guarantee they meet PCI compliance commonplace DSS nine.9.1 and monitor device transactions across all retail locations. link-attached terminal solutions permit merchants to find and report payment device problems early for max period of their fleet, whereas security automation options block unknown terminals from getting into your network as an additional fraud hindrance live.

6. Lower Operational prices

Modern payment systems ar invariably seeking ways in which to lower your operational prices. Another profit to integrated payments and advanced terminal management is that the system’s ability to speak seamlessly with multiple payment devices and work stations quickly. Shared payment device management permits the cashier to push a dealing from any digital computer to a shared payment device. By sharing devices across multiple workstations, merchants will effectively save many bucks on the price of buying new terminals.

7. Access to Premium Payment Services

In ancient payment systems, premium services ar valuable or perhaps unobtainable to most merchants. fashionable systems create shifting to EMV, accessing advanced security measures, and change your payment devices a breeze.

iQmetrix’s Payment Connect offers versatile enhancements to make a very strong payments package. a number of the numerous enhancements include:

- Remote EMV computer code updates: a Payment Specialist can mechanically push the most recent computer code unleash to every device remotely.

- Advanced PCI: create PCI compliance easier with personalised PCI steerage.

- Remote Key Injection: create the transition to a replacement processor easier by having your payment devices remotely re-keyed.

With a contemporary payment system in your corner, payments will transition from being a price center to a key competitive advantage for your business. vital time and value savings moreover as advanced practicality like augmented security measures, next-day funding, and premium payment services all facilitate to supply a superior payment expertise for you and your customers.

Key takeaway

- A modern payment system directly integrates to your point of sale and delivers a robust payment experience for both merchant and customer. It connects merchants to a total payment ecosystem, from merchant services to remote terminal solutions, to hardware procurement.

The steps concerned in on-line payment process have considerably reduced the waiting amount and trouble once buying commercials product and services. With new technologies and payment processes, individuals will simply purchase product and one-time services, found out revenant payment, and contour payments that permit sellers to just accept new orders 24/7.

In the past, several ecommerce payment process services were removed from intuitive and infrequently expensive. However, these days there ar dozens of respected corporations pushing easy-to-use on-line payment process systems which will handle mastercard transactions, bank transfers, and period orders at the fraction of the price. whereas there actually isn’t a shortage of payment service suppliers for you to settle on from, however specifically will on-line payment work? Let’s bear the first steps.

Step 1: the customer submits a payment request through his/her cellular phone, pc or mobile payment processor (i.e. SWIPE).

Step 2: The service supplier routes the information via a secure affiliation to the buyer’s bank or mastercard company.

Step 3: The buyer’s bank either approves or declines the dealing supported the buyer’s accessible funds or credit. If approved, the dealing is routed back to the payment supplier to be processed.

Step 4: The payment supplier stores the dealing and send a record to each the vendor and purchaser.

Step 5: the products or services ar sent to the customer and therefore the buyer’s bank sends the funds to the vendor.

All of this could happen in an exceedingly matter of seconds once the customer submits letter of invitation to get.

Having Associate in Nursing understanding of the advantages of on-line payment process and therefore the styles of payments that you simply ar in a position or need to just accept as a replacement business is one amongst the foremost vital steps to tackle as Associate in Nursing ecommerce trafficker. virtually each eCommerce payment process service accepts mastercard payments as a result of it's one amongst the foremost common types of payment. There are eChecks and ACH (bank) transfers, that pull funds directly from the buyer’s personal checking account.

The benefits of efficient on-line payment process steps that drive business success embody international reach, electronic records, advanced fraud protection and secure transactions, easy integration into numerous web site platforms and bank process systems, and easy options. These convenient options can create it easier for shoppers to get your product and services and to stay up with an outsized demand.

Most of the skilled payment process service suppliers will set up their payment services to fit your business desires. Mobile payments comprise one amongst the most recent types of on-line payment process. rather than mistreatment credit cards, a purchaser should merely send a payment request via a text message or a package application that’s coupled to a mastercard or checking account. And whereas there's a priority of eCommerce fraud, supplemental security measures like a security pin helps diminish the possibility of this occurring.

Key takeaway

- The steps involved in online payment processing have significantly reduced the waiting period and hassle when purchasing commercials products and services. With new technologies and payment processes, people can easily purchase products and one-time services, set up recurring payment, and streamline payments that allow sellers to accept new orders 24/7.

- In the past, many ecommerce payment processing services were far from intuitive and often costly. However, today there are dozens of reputable companies pushing easy-to-use online payment processing systems that can handle credit card transactions, bank transfers, and real-time orders at the fraction of the cost. While there certainly isn’t a shortage of payment service providers for you to choose from, how exactly does online payment work? Let’s go through the primary steps.

Security is a necessary a part of any dealing that takes place over the net. Customers can lose his/her religion in e-business if its security is compromised. Following square measure the essential necessities for safe e-payments/transactions −

- Confidentiality − info shouldn't be accessible to Associate in Nursing unauthorized person. It shouldn't be intercepted throughout the transmission.

- Integrity − info shouldn't be altered throughout its transmission over the network.

- Availability − info ought to be obtainable where and whenever needed at intervals a limit specified .

- Authenticity − There ought to be a mechanism to evidence a user before giving him/her Associate in Nursing access to the specified info.

- Non-Repudiability− it's the protection against the denial of order or denial of payment. Once a sender sends a message, the sender shouldn't be able to deny causing the message. Similarly, the recipient of message shouldn't be able to deny the receipt.

- Encryption − info ought to be encrypted and decrypted solely by a certified user.

- Auditability − knowledge ought to be recorded in such how that it may be audited for integrity necessities.

Measures to confirm Security

Major security measures square measure following −

- Encryption − it's a really effective and sensible thanks to safeguard the information being transmitted over the network. Sender of the knowledge encrypts the information employing a cypher and solely the desired receiver will decipher the information victimization an equivalent or a unique cypher.

- Digital Signature − Digital signature ensures the believability of the knowledge. A digital signature is Associate in Nursing e-signature documented through secret writing and watchword.

- Security Certificates − Security certificate could be a distinctive digital id accustomed verify the identity of a personal web site or user.

Security Protocols in web

We will discuss here a number of the popular protocols used over the net to confirm secured on-line transactions.

Secure Socket Layer (SSL)

It is the foremost unremarkably used protocol and is wide used across the business. It meets following security necessities

• Authentication

• Encryption

• Integrity

• Non-reputability

"https://" is to be used for protocol urls with SSL, wherever as "http:/" is to be used for protocol urls while not SSL.

Secure machine-readable text Transfer Protocol (SHTTP)

SHTTP extends the protocol web protocol with public key secret writing, authentication, and digital signature over the net. Secure protocol supports multiple security mechanism, providing security to the end-users. SHTTP works by negotiating secret writing theme varieties used between the shopper and also the server.

Secure Electronic dealing

It is a secure protocol developed by MasterCard and Visa together. on paper, it's the most effective security protocol. it's the subsequent the subsequent

- Card Holder's Digital pocketbook computer code computer code Digital pocketbook permits the cardboard holder to create secure purchases on-line via purpose and click on interface.

- Merchant computer code computer code This computer code helps merchants to speak with potential customers and money establishments during a secure manner.

- Payment entry Server computer code computer code Payment entry provides automatic and customary payment method. It supports the method for merchant's certificate request.

- Certificate Authority computer code computer code This computer code is employed by money establishments to issue digital certificates to card holders and merchants, and to change them to register their account agreements for secure electronic commerce.

Key takeaway

- Security is an essential part of any transaction that takes place over the internet. Customers will lose his/her faith in e-business if its security is compromised. Following are the essential requirements for safe e-payments/transactions −

- Confidentiality− Information should not be accessible to an unauthorized person. It should not be intercepted during the transmission.

- Integrity− Information should not be altered during its transmission over the network.

- Availability− Information should be available wherever and whenever required within a time limit specified.

- Authenticity− There should be a mechanism to authenticate a user before giving him/her an access to the required information.

- Non-Repudiability− It is the protection against the denial of order or denial of payment. Once a sender sends a message, the sender should not be able to deny sending the message. Similarly, the recipient of message should not be able to deny the receipt.

- Encryption− Information should be encrypted and decrypted only by an authorized user.

- Auditability− Data should be recorded in such a way that it can be audited for integrity requirements.

Internet Banking, also known as net-banking or online banking, is an electronic payment system that enables the customer of a bank or a financial institution to make financial or non-financial transactions online via the internet. This service gives online access to almost every banking service, traditionally available through a local branch including fund transfers, deposits, and online bill payments to the customers.

Internet banking can be accessed by any individual who has registered for online banking at the bank, having an active bank account or any financial institution. After registering for online banking facilities, a customer need not visit the bank every time he/she wants to avail a banking service. It is not just convenient but also a secure method of banking. Net banking portals are secured by unique User/Customer IDs and passwords.

Special Features of Internet Banking

Here are some of the best features of internet banking:

- Provides access to financial as well as non-financial banking services

- Facility to check bank balance any time

- Make bill payments and fund transfer to other accounts

- Keep a check on mortgages, loans, savings a/c linked to the bank account

- Safe and secure mode of banking

- Protected with unique ID and password

- Customers can apply for the issuance of a chequebook

- Buy general insurance

- Set-up or cancel automatic recurring payments and standing orders

- Keep a check on investments linked to the bank account

Services Available through the Internet Banking

Once a customer is registered for online banking, he/she can log-in to the respective online banking portal of his/her bank using the issued User-ID and password.

| |||||||||||||||||||||

Advantages of Internet Banking

Given below are some advantages/benefits of Internet Banking available for all the users-

- 24×7 Availability: Internet banking, unlike usual banking hours, is not time-bound. It is available 24×7 throughout the year. Most of the services available online are not time-restricted. Users can check their bank balance, account statements and make fund transfers anytime instantly.

- Convenience of initiating financial transactions: Internet banking is largely preferred because of the convenience that it provides while fund transfer and bill payments. Registered users can use almost all the banking services without having to visit the bank and standing in queues. Financial transactions such as paying bills and transferring funds between accounts can easily be performed anytime as per the convenience of the user.

- Proper Track of Transactions: Acknowledgement slips are provided by the bank after transactions which have a high possibility of getting misplaced. However, with internet banking, it becomes very easy to track the history of all the transactions initiated by the user. Transactions and fund transfers made online are organised in the ‘Transaction History’ section along with other details such as payee’s name, bank account number, the amount paid, the date and time of payment, and remarks.

- Quick and Secure: Net banking users can transfer funds between accounts instantly, especially if the two accounts are held at the same bank. Funds can be transferred via NEFT, RTGS or IMPS as per the user’s convenience. One can also make bill payments, EMI payments, loan and tax payments easily. Moreover, the transactions, as well as the account, are secured with a password and unique User-ID.

- Non-financial Transactions: Besides fund transfer, internet banking allows the users to avail non-financial services such as balance check, account statement check, application for issuance of cheque book, etc.

Types of Fund Transfers using Internet Banking

As we have already discussed, there are three types of fund transfers which can be made using net-banking. Let us understand more-

NEFT

National Electronic Fund Transfer (NEFT) is a payment system which allows one-to-one fund transfer.

- Using NEFT, individuals and corporates can transfer funds electronically from any bank branch to any individual or corporate with an account with any other bank branch in the country

- NEFT service is available 24×7 on internet banking. But, it is a time-restricted service at the bank branch

- Usually, NEFT transfer is successfully completed within 30 minutes. Nonetheless, the time can even stretch to 2-3 hours or might be completed in just 10 minutes

RTGS

Real-Time Gross Settlement (RTGS) is a continuous settlement of funds individually on an order by order basis.

- This payment system ensures that the receiver’s account gets credited with the funds almost immediately and not after a certain duration, as is the case with other payment modes like NEFT

- RTGS transactions are tracked by the RBI, thereby successful transfers are irreversible. This method is majorly used for large value transfers

- The minimum amount to be remitted through RTGS is 2 lakh. There is no cap on the maximum amount for transfer via RTGS

- Like NEFT, RTGS is also available online 24×7

IMPS

Immediate Payment System (IMPS) is another payment method that transfers funds in real-time.

- IMPS is used to transfer funds instantly within banks across India via mobile, internet and ATM, which is not only safe but also economical both in financial and non-financial perspectives

- IMPS is an inexpensive mode of fund transfer. Other fund transfer mediums such as NEFT and RTGS charge significantly higher than IMPS

- It does not require details like account number, IFSC code, etc. Funds can be transferred via IMPS just with the mobile number of the beneficiary

How to Register for Internet Banking?

Every account holder has to register for an online banking service at his/her respective bank to get access. Most of the banks provide a net-banking log-in kit as and when you apply for a new account. To start using net-banking, follow these steps-

- Download the application form from your bank’s official website, fill the same and take out a print. You can also visit the bank directly and fill the application form for net-banking

- Submit the application form at the bank

- After verification, you will receive a unique User ID and password using which you can log-in to internet banking

E-banking or Electronic Banking refers to all the forms of banking services and transactions performed through electronic means. It allows individuals, institutions and businesses to access their accounts, transact business, or obtain information on various financial products and services via a public or private network, including the internet.

Popular Types of E-banking Services in India

- Internet Banking: It is the type of electronic banking service which enables customers to perform several financial and non-financial transactions via the internet. With internet or online banking or net-banking, customers can transfer funds to another bank account, check account balance, view bank statements, pay utility bills, and much more.

- Mobile Banking: This electronic banking system enables customers to perform financial and non-financial transactions via mobile phone. Most of the banks have launched their mobile banking applications available on Google Playstore and Apple App Store. Just like the net-banking portal, customers can use the mobile application to access banking services.

- ATM: Automated Teller Machines (ATM) is one of the most popular types of e-banking. ATMs allow customers to withdraw funds, deposit money, change Debit Card PIN, and other banking services. To make use of an ATM, the user must have a password. Banks charge a nominal fee from the customers on every transaction made after crossing the specified limit of free transactions if the transaction is done from any other bank’s ATM.

- Debit Cards: Almost every person owns a debit card. This card is connected to your bank account and you can go cashless with this card. You can use your debit card for all types of transactions, the transaction amount is debited from your account instantly.

- Deposit and Withdraws (Direct): This service under e-banking offers the customer a facility to approve paychecks regularly to the account. The customer can give the bank an authority to deduct funds from his/her account to pay bills, instalments of any kind, insurance payments, and many more.

- Pay by Phone Systems: This service allows the customer to contact his/her bank to request them for any bill payment or to transfer funds to some other account.

- Point-of-Sale Transfer Terminals: This service allows customers to pay for the purchase through a debit/credit card instantly.

Services Provided through E-banking in India

|

Comparison between Internet Banking and E-Banking

Internet banking and Electronic banking are often confused with each other. Let us compare the two for better understanding:

Definition

Internet banking or online banking or net-banking is a digital payment system which enables customers of a bank or a financial institution to make financial or non-financial transactions online via the internet. On the other hand, E-banking or Electronic Banking refers to all the forms of banking services and transactions performed through electronic means.

Electronic banking or E-banking is a broad category of accessing banking services via electronic means, whereas Internet banking is a part or type of electronic banking. It is also known as electronic funds transfer (EFT) and uses electronic means to transfer funds directly from one account to another.

Types of Services

With internet banking, customers can obtain every banking service, traditionally available through a local branch including fund transfers, deposits, and online bill payments to the customers.

Electronic banking includes various transaction services such as internet banking, mobile banking, telebanking, ATMs, debit cards, and credit cards. Internet banking is one of the latest additions to electronic banking.

How can I use internet banking?

To use internet banking, you must have an operating account in any bank or a financial institution. You need to register for online banking at the bank to obtain a unique ID and password. For that, you can download the net-banking application form from your bank’s net-banking website or visit the bank and fill in the form.

Can I change my internet banking password?

After logging in to the net-banking portal for the first time, all the users must change the password which is issued by the bank. Also, you should change your password at least once every two months.

What precautions should be taken while using internet banking?

While using internet banking, you must make sure of a few things-

- Avoid using public Wi-Fi or use a VPN software

- Use a genuine anti-virus software

- Make sure the operating system of your smartphone or device is updated

- Change your login password at least once in two months

- Avoid logging in to your net-banking portal via mailers

- Do not use public computers to log in to the net-banking portal

What is user ID in net-banking?

Most of the banks provide internet banking ID and password as and when you apply for a new account. If you haven’t received your user ID and password, you need to apply for net-banking at the bank by filling and submitting an application form. After verification, you will receive a unique user ID and password to login to net banking.

Are electronic banking and internet banking the same?

No, electronic banking and internet banking are often confused with each other. However, these are two different services launched by the bank. Electronic banking is a broad term or category which includes various forms of banking services and transactions performed through electronic means such as internet banking, mobile banking, telebanking, ATMs, debit cards, and credit cards. Internet banking is one of the latest additions to electronic banking. Thereby, internet banking is a part of electronic banking.

Key takeaway

- Internet Banking, also known as net-banking or online banking, is an electronic payment system that enables the customer of a bank or a financial institution to make financial or non-financial transactions online via the internet. This service gives online access to almost every banking service, traditionally available through a local branch including fund transfers, deposits, and online bill payments to the customers.

- Internet banking can be accessed by any individual who has registered for online banking at the bank, having an active bank account or any financial institution. After registering for online banking facilities, a customer need not visit the bank every time he/she wants to avail a banking service. It is not just convenient but also a secure method of banking. Net banking portals are secured by unique User/Customer IDs and passwords.

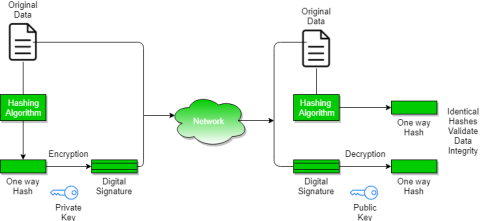

Encryption – method of changing electronic information into another kind, known as cipher text, that can't be simply understood by anyone except the approved parties. This assures information security.

Decryption– method of translating code to information.

- Message is encrypted at the sender's facet exploitation varied coding algorithms and decrypted at the receiver's finish with the assistance of the secret writing algorithms.

- When some message is to be unbroken secure like username, password, etc., coding and secret writing techniques ar wont to assure information security.

Types of coding

1.cruciate Encryption– information is encrypted employing a key and therefore the secret writing is additionally done exploitation identical key.

2.uneven Encryption-Asymmetric Cryptography is additionally called public key cryptography. It uses public and personal keys to code and rewrite information. One key within the try which may be shared with everyone seems to be known as the general public key. the opposite key within the try that is unbroken secret and is just far-famed by the owner is named the personal key. Either of the keys will be wont to code a message; the other key from the one wont to code the message is employed for secret writing.

Public key– Key that is understood to everybody. Ex-public key of A is seven, this data is understood to everybody.

Private key– Key that is just far-famed to the person who's personal key it's.

Authentication-Authentication is any method by that a system verifies the identity of a user UN agency desires to access it.

Non- repudiation– Non-repudiation means that to make sure that a transferred message has been sent and received by the parties claiming to own sent and received the message. Non-repudiation could be a thanks to guarantee that the sender of a message cannot later deny having sent the message which the recipient cannot deny having received the message.

Integrity– to make sure that the message wasn't altered throughout the transmission.

Message digest -The illustration of text within the sort of one string of digits, created employing a formula known as a 1 approach hash perform. Encrypting a message digest with a personal key creates a digital signature that is associate degree electronic means that of authentication..

Digital Signature

A digital signature could be a mathematical technique wont to validate the credibleness and integrity of a message, software package or digital document.

1.Key Generation Algorithms : Digital signature ar electronic signatures, that assures that the message was sent by a specific sender. whereas acting digital transactions credibleness and integrity ought to be assured, otherwise the info will be altered or somebody can even act as if he was the sender and expect a reply.

2.sign language Algorithms: to form a digital signature, sign language algorithms like email programs produce a unidirectional hash of the electronic information that is to be signed. The sign language algorithmic rule then encrypts the hash price exploitation the personal key (signature key). This encrypted hash in conjunction with different data just like the hashing algorithmic rule is that the digital signature. This digital signature is appended with the info and sent to the admirer. the explanation for encrypting the hash rather than the whole message or document is that a hash perform converts any impulsive input into a far shorter mounted length price. this protects time as currently rather than sign language a protracted message a shorter hash price has got to be signed and what is more hashing is far quicker than sign language.

3.Signature Verification Algorithms : admirer receives Digital Signature in conjunction with the info. It then uses Verification algorithmic rule to method on the digital signature and therefore the public key (verification key) and generates some price. It additionally applies identical hash perform on the received information and generates a hash price. Then the hash price and therefore the output of the verification algorithmic rule ar compared. If they each ar equal, then the digital signature is valid else it's invalid.

The steps followed in making digital signature ar :

1. Message digest is computed by applying hash perform on the message then message digest is encrypted exploitation personal key of sender to make the digital signature. (digital signature = coding (private key of sender, message digest) and message digest = message digest algorithm(message)).

2. Digital signature is then transmitted with the message.(message + digital signature is transmitted)

3. Receiver decrypts the digital signature exploitation the general public key of sender.(This assures credibleness,as solely sender has his personal key thus solely sender will code exploitation his personal key which may so be decrypted by sender’s public key).

4. The receiver currently has the message digest.

5. The receiver will reckon the message digest from the message (actual message is distributed with the digital signature).

6. The message digest computed by receiver and therefore the message digest (got by secret writing on digital signature) got to be same for making certain integrity.

Message digest is computed exploitation unidirectional hash perform, i.e. a hash perform during which computation of hash price of a message is simple however computation of the message from hash price of the message is incredibly troublesome.

|

Fig 2 – Message digest

Digital Certificate

Digital certificate is issued by a trusted third party which proves sender's identity to the receiver and receiver’s identity to the sender.

A digital certificate is a certificate issued by a Certificate Authority (CA) to verify the identity of the certificate holder. The CA issues an encrypted digital certificate containing the applicant’s public key and a variety of other identification information. Digital certificate is used to attach public key with a particular individual or an entity.

Digital certificate contains:-

- Name of certificate holder.

- Serial number which is used to uniquely identify a certificate, the individual or the entity identified by the certificate

- Expiration dates.

- Copy of certificate holder's public key.(used for decrypting messages and digital signatures)

- Digital Signature of the certificate issuing authority.

Digital ceritifcate is also sent with the digital signature and the message.

Digital certificate vs digital signature :

Digital signature is used to verify authenticity, integrity, non-repudiation ,i.e. it is assuring that the message is sent by the known user and not modified, while digital certificate is used to verify the identity of the user, maybe sender or receiver. Thus, digital signature and certificate are different kind of things but both are used for security. Most websites use digital certificate to enhance trust of their users.

|

Key takeaway

- Encryption – Process of converting electronic data into another form, called cipher text, which cannot be easily understood by anyone except the authorized parties.This assures data security.

Decryption– Process of translating code to data. - Message is encrypted at the sender's side using various encryption algorithms and decrypted at the receiver's end with the help of the decryption algorithms.

- When some message is to be kept secure like username, password, etc., encryption and decryption techniques are used to assure data security.

Online business is booming, and online shopping statistics say that ecommerce is the way to go for any growing business. You have a product you want to sell or a great business idea.

Building an ecommerce website will strengthen the reputation of your business, help you expand your brand nationally and internationally, and expand your professional network.

In this article, we’ll show you how to build an ecommerce website in 7 steps, quickly and easily, without any special technical skills or experience.

Building an Ecommerce Website in 7 Effortless Steps

- Start with a Strategy

- Choose a Domain and Platform for Your Ecommerce Website

- Decide on Pricing and Set Up Payments

- Design Your Store and Add Products

- Create a Great Checkout Experience

- Market Your Growing Business

- Improve Your Online Sales with Data

If you are just beginning your research, all of the information about ecommerce can feel both complicated and overwhelming.

Building an ecommerce website used to require extensive technical understanding and a dream, but with the massive options for ecommerce platforms, all you need to do is a little research to move your growing business online.

Do you want an online store but don’t want to spend thousands of dollars building an ecommerce website? If the answer is yes, then let’s walk you through the process of building your own store using Selz as an example. Selz is a powerful tool for creating online stores and selling from existing websites.

Follow these steps for building AN ecommerce website:

1. begin with a method

To ensure success whereas building AN ecommerce web site, begin with a sound strategy. Even the only ecommerce platforms have details that require to be excellent for you and your business.

For instance, everybody says that they need wonderful client service, however you’re headed into a world wherever your life might depend upon your ecommerce web site. Don’t you wish 24/7 client support and friendly workers accessible to troubleshoot something which may arise?

It’s vital to anticipate your greatest desires and challenges as your business grows. If you intend to sell physical product, decide however you wish shipping to figure earlier.

If you’re commercialism digital product, have faith in the information measure and delivery choices you’ll would like. commercialism services online? List out specifically what you’ll be commercialism, however you wish to deliver it, and any payment or time limitations.

Building AN Ecommerce Site? arrange for Growth

Think about {the choices|the choices} you wish and also the options you’ll would like for the expansion of your business, and the way those choices can have an effect on your bottom line. Selz offers multiple plans so you simply pay money for the choices {you would like|you would like|you wish} once you need them.

For example, as exciting because it is to make an entire new ecommerce web site if you’re already creating sales through your journal you'll be able to use Selz to infix a button (for one product), a gismo (for multiple products), or an entire store on your journal.

Instead of amusing your customers to an entire new web site, you've got a cheap choice to sell wherever you're and contour the shopping for and payment method.

At the tip of the day, take care to try to your schoolwork so you’re creating the most effective long-run selections for your business. Speaking of long-run, another important strategy whereas building your ecommerce web site is program optimisation (SEO).

Develop a promoting strategy before building AN ecommerce web site, and begin early with SEO, as a result of it will take a year for even the most effective SEO strategy to point out results.

2. Select a site and Platform for Your Ecommerce web site

Is a custom domain essential for your ecommerce website? The short answer is not any. once you register for a free 14-day trial with Selz, you instantly get your own sub-domain, like “mysite.selz.com.”

This may serve for your ecommerce web site desires. However, if you intend to sell a good kind of product and develop or extend your whole, a custom domain is that the thanks to go.

A custom domain offers your ecommerce store:

- A recognizable whole that belongs to you, e.g. mystore.com

- A skilled email address joined to your domain wherever individuals will contact you

- Search engine optimisation (SEO) edges

You can produce a custom domain for your Selz store in exactly many clicks. If you have already got a site name, you'll be able to quickly set up it to your Selz store. If you don’t have a site name however, you'll be able to purchase and set one up right your Selz dashboard.

Your next step is choosing the correct ecommerce platform for your growing business. You ideally need to make AN ecommerce web site on a platform that’s versatile and simple to use. Most little business homeowners don’t need to trouble with hand-coding their web site.

Business homeowners and solo entrepreneurs would like a platform that they'll simply integrate with their existing web site. or else, if you don’t have a web site however, you'll take pleasure in a platform that enables you to make a web site from scratch, in a very few easy steps.

That’s why Selz could be a fashionable selection for several on-line entrepreneurs. It’s designed to assist you produce an expert and trendy ecommerce web site, at a competition-beating worth purpose. Plus, your store may be simply custom, we’ve enclosed a lot of details on it below.

If you’ve already got a web site, you'll be able to simply build AN ecommerce web site by adding obtain buttons or widgets. you'll be able to conjointly infix an easy store directly on your web site.

If victimization WordPress for your web site, Selz features a free WordPress Ecommerce plugin accessible for you to use.

3. Elect evaluation and started Payments

There square measure 3 key aspects of payments as you build AN ecommerce website: however you'll worth your product, however customers square measure progressing to pay you, and the way you're progressing to get those payments into your own checking account.

You may be ranging from scratch or extending your native business on-line. Either way, the net world has completely different expectations for a way you'll place a worth on your product.

There square measure several factors to think about once evaluation your product available on-line including:

- The price of materials per item

- Ecommerce net hosting

- Shipping

- Taxes

- Fees and share per sale deductions from varied organizations, as well as PayPal, credit cards, etc.

- Flexible evaluation, like pay-what-you-wish

Then decide however your ecommerce web site can settle for payments. In several cases, this implies finding a third-party payment processor to act because the intermediary. One very fashionable payment possibility is PayPal. We’ve created it easy for your store to simply accept PayPal payments from your customers, victimization our powerful PayPal feature. Yay! we have a tendency to conjointly supply Selz Pay.

With these payment choices, you'll be able to take payments from anyplace and provides your customers further peace of mind.

Selz offers:

- Secure payment handling

- Integrated SSL

- Acceptance of payments from anyplace

- Payments via PayPal or into your own checking account

- WordPress ecommerce integration

4. Style Your Store and Add product

Next step in building Associate in Nursing ecommerce website, it’s time to style your store. accept what, additionally to your product, you intend to incorporate.

At the terribly least, you'll need to incorporate Associate in Nursing concerning page Associate in Nursingd a contact page as you build an ecommerce web site to assist potential patrons connect with you. you'll be able to conjointly add video and text onto your pages.

When building Associate in Nursing ecommerce website, make certain to incorporate your:

- Photograph: individuals like handling real individuals

- Store name: Selz uses your account name by default, however you'll be able to invariably modification this

- Logo: For stigmatisation and recognition

- Trustmarks and payment logos: These facilitate individuals feel snug looking with you. Selz has these logos inbuilt.

Select a subject matter that represents your whole and permits you to showcase your product within the best lightweight potential. produce classes that square measure logical to your patrons. Learn the maximum amount concerning your ideal client as you'll be able to and style your website with their preferences and ideal user expertise in mind.

Remember that the approach you see your customers won't be the approach that they see themselves, thus notice the simplest way to raise their opinions as you build your website.

Your ecommerce web site is on the brink of be a transactional hub wherever you'll sell to customers and build direct relationships with them. Selz permits you to feature pages, products, blog posts, images, text, videos, and a lot of to your on-line store. this enables you to pique customers’ curiosity and facilitate them feel more leisurely concerning getting product.

Once you’ve given your whole store an expert, polished look with one in every of Selz’s themes, begin building your ecommerce web site at intervals that structure. The drag and drop store builder makes this method intuitive, easy, and effective.

Check out this video to check however our store builder works.

Now it’s time to feature some product to your new ecommerce web site. Here’s however this works with Selz:

- Choose your product kind (physical, digital or service). If you’re giving a video course, it’s price noting that Selz has no information measure or storage limits and you'll be able to transfer files up to a massive 15GB.

- Give your product a reputation and outline

- Set the value and also the quantities on the market purchasable

- Create a preview of your item by uploading a photograph, Associate in Nursing audio file or perhaps a video preview

- Choose from a spread of delivery and evaluation choices, moreover as specifying any variants

It is tempting to hurry through this method, however detain mind that nice product descriptions and clear pictures convert. Be thoughtful and pithy together with your copywriting and make certain your pictures look nice.

5. produce a good Checkout expertise

Shopping cart abandonment is that the plague of on-line sales. In 2017, the Baymard Institute took the typical of thirty seven cart abandonment studies and located that the typical on-line pushcart abandonment rate is over 69%!

Avoid cart abandonment as you build Associate in Nursing ecommerce web site by:

- Enabling customers to get multiple things promptly

- Offering free shipping if you'll be able to, or

- Being terribly clear concerning shipping prices direct (before customers get to the checkout)

- Making certain that you simply optimize your checkout for mobile devices. Selz works on desktops, smartphones, and tablets.

- Sending cart abandonment emails anytime somebody leaves while not finishing their purchase

Don’t forget, the quantity of steps it takes to finish a sale considerably affects your sales conversion rates. check your checkout method till it's excellent and raise your friends and family to check it too.

6. Market Your Growing Business

Once you begin building Associate in Nursing ecommerce web site, you would like to push your product to extend traffic and drive sales.

Many vendors favor to sell from marketplace sites like Etsy or Amazon however notice themselves troubled thanks to high fees and alternative limitations.

After building Associate in Nursing ecommerce {website|web website} you’ll would like a solid promoting conceive to bring the proper customers to your site and to stay their warm-heartedness for come business. Selz helps you with promoting by:

- Offering professional services for business employment, SEO, pay per click advertising and a lot of

- Including inbuilt SEO-optimization for each product. Use the most recent steerage on SEO to assist individuals notice your ecommerce web site, products, and services on-line

- Linking your ecommerce website with Facebook

- Enabling social sharing for your product – it’s a one-click method

- Giving you the choice to form coupons or discounts to drive sales from come customers

- Offering free integration with MailChimp, AWeber, Campaign Monitor and a lot of for email promoting

- Adding customers to your existing email promoting lists thus you'll be able to inform them concerning new offerings

- Include a diary or Associate in Nursing eBook on your website to share participating, relevant content, build trust, and attract new customers

7. Take care of SEO and analytics

Track the performance of your ecommerce web site with Associate in Nursing analytics answer. additionally to the business reportage at intervals Selz dashboard, Selz integrates with Google Analytics in order that you'll be able to gain deeper insight into however your promoting efforts and ecommerce SEO square measure playacting.

This will assist you monitor your website and merchandise pages thus you'll be able to improve them for a lot of sales, reach, and effectiveness.

Building Associate in Nursing Ecommerce web site outline

That’s it. You’re done! You currently have your own on-line store.

Building Associate in Nursing ecommerce web site isn’t for the faint of heart, however it's a chance to stay your business competitive, and to lift awareness and access for your unimaginable product.

Key takeaway

- Online business is booming, and online shopping statistics say that ecommerce is the way to go for any growing business. You have a product you want to sell or a great business idea.

- Building an ecommerce website will strengthen the reputation of your business, help you expand your brand nationally and internationally, and expand your professional network.

- In this article, we’ll show you how to build an ecommerce website in 7 steps, quickly and easily, without any special technical skills or experience.

E- PAYMENT