Unit 2

Foreign Exchange

2.1.1 Meaning

The foreign exchange Market is a market where the buyers and sellers are involved within the sale and purchase of foreign currencies. In other words, a market where the currencies of various countries are bought and sold is named a foreign exchange market. The structure of the foreign exchange market constitutes central banks, commercial banks, brokers, exporters and importers, immigrants, investors, tourists. These are the main players of the foreign market.

Currencies are always traded in pairs; therefore the "value" of 1 of the currencies in that pair is relative to the worth of the opposite. This determines what proportion of country A's currency country B can purchase, and the other way around. Establishing this relationship (price) for the global markets is that the main function of the foreign exchange market. This also greatly enhances liquidity in all other financial markets, which is essential to overall stability. The foreign exchange market is an over-the-counter (OTC) marketplace that determines the rate of exchange for global currencies. It is, by far, the most important financial market in the world and is comprised of a worldwide network of monetary centres that transact 24 hours daily, closing only on the weekends. Currencies are always traded in pairs, therefore the "value" of 1 of the currencies therein pair is relative to the value of the opposite.

The following are the key points:

• The foreign exchange (also referred to as FX or FOREX) market is a global marketplace for exchanging national currencies against each other.

• Because of the worldwide reach of trade, commerce, and finance, FOREX markets tend to be the most important and most liquid asset markets within the world.

• Currencies trade against one another as exchange rate pairs. For instance, EUR/USD.

• FOREX markets exist as spot (cash) markets also as derivatives markets offering forwards, futures, options, and currency swaps.

• Market participants use FOREX to hedge against international currency and rate of interest risk, to speculate on geopolitical events, and to diversify portfolios, among several other reasons.

2.1.2 Functions

1. Transfer Function: the essential and the most visible function of exchange market is the transfer of funds (foreign currency) from one country to a different for the settlement of payments. It basically includes the conversion of 1 currency to another, wherein the role of FOREX is to transfer the purchasing power from one country to another.

For example, if the exporter of India import goods from the USA and the payment is to be made in dollars, then the conversion of the rupee to the dollar are going to be facilitated by FOREX. The transfer function is performed through a use of credit instruments, like bank drafts, bills of foreign exchange, and telephone transfers.

2. Credit Function: FOREX provides a short-term credit to the importers so on facilitate the smooth flow of products and services from country to country. An importer can use credit to finance the foreign purchases. Like an Indian company wants to get the machinery from the USA, pays for the purchase by issuing a bill of exchange within the exchange market, essentially with a three-month maturity.

3. Hedging Function: The third function of a foreign exchange market is to hedge foreign exchange risks. The parties to the exchange are often scared of the fluctuations in the exchange rates, i.e., the worth of 1 currency in terms of another. The change in the rate of exchange may end in a gain or loss to the party concerned.

Thus, because of this reason the FOREX provides the services for hedging the anticipated or actual claims/liabilities in exchange for the forward contracts. A forward contract is typically a three-month contract to buy or sell the exchange for another currency at a fixed date within the future at a price agreed upon today. Thus, no money is exchanged at the time of the contract.

There are several dealers within the foreign exchange markets, the foremost important amongst them are the banks. The banks have their branches in several countries through which the exchange is facilitated; such service of a bank is named as Exchange Banks.

2.1.3 Structure

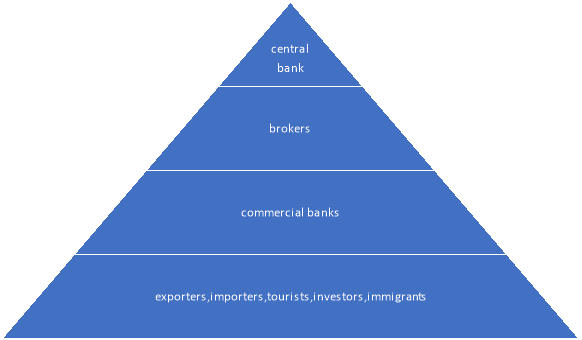

The structure of the foreign exchange market constitutes central banks, commercial banks, brokers, exporters and importers, immigrants, investors, tourists. These are the main players of the foreign market; their position and place are shown within the figure below-

At the bottom of a pyramid are the actual buyers and sellers of the foreign currencies- exporters, importers, tourist, investors, and immigrants. They're actual users of the currencies and approach commercial banks to buy it.

The commercial banks are the second most significant organ of the foreign exchange market. The banks dealing in exchange play a task of “market makers”, within the sense that they quote on a routine the foreign exchange rates for buying and selling of the foreign currencies. Also, they function as clearing houses, thereby helping in wiping out the difference between the demand for and therefore the supply of currencies. These banks buy the currencies from the brokers and sell it to the buyers.

The third layer of a pyramid constitutes the foreign exchange brokers. These brokers function as a link between the central bank and therefore the commercial banks and also between the actual buyers and commercial banks. They're the main source of market information. These are the persons who don't themselves buy the foreign currency, but rather strike a deal between the buyer and therefore the seller on a commission basis.

The central bank of any country is that the apex body within the organization of the exchange market. They work because the lender of the last resort and therefore the custodian of foreign exchange of the country. The central bank has the power to regulate and control the foreign exchange market so on assures that it works within the orderly fashion. One among the main functions of the central bank is to stop the aggressive fluctuations within the foreign exchange market, if necessary, by direct intervention. Intervention within the form of selling the currency when it's overvalued and buying it when it tends to be undervalued.

2.1.4 Euro Dollar Market

By Euro-dollar is meant all U.S. Dollar deposits in banks outside the United States, including the foreign branches of U.S. Banks. A Euro-dollar is, however, not a special type of dollar. It bears the same exchange rate as an ordinary U.S. Dollar has in terms of other currencies.

Euro-dollar transactions are conducted by banks not resident within the us. For example, when an American citizen deposits (lends) his funds with a U.S. Bank in London, which can again be wont to make advances to a business enterprise within the U.S., then such transactions are stated as Euro-dollar transactions. All Euro-dollar transactions are, however, unsecured credit.

Euro-dollars have inherited existence on account of the Regulation issued by the Board of Governors of the U.S. Federal Reserve System, which doesn't permit the banks to pay interest to the depositors above a certain limit.

As such, banks outside the us tend to expand their dollar business by offering higher deposit rates and charging lower lending rates, as compared to the banks inside the U.S. Increase or decrease within the potential for Euro-dollar holdings, however, depends, directly upon U.S. Deficits and surplus, respectively.

EURO-DOLLAR MARKET:

Euro-dollar market is that the creation of the international bankers. It's simply a short-term market facilitating banks’ borrowings and lending’s of U.S. Dollars. The Euro-dollar market is principally located in Europe and basically deals in U.S. Dollars.

But, during a wider sense, Euro-dollar market is confined to the external lending and borrowing of the world’s most vital convertible currencies like dollar, pound, sterling, Swiss franc, French franc, deutsche mark and therefore the Netherlands guilder.

In short, the term Euro-dollar is used as a common term to include the external markets in all the major convertible currencies.

Euro-dollar operations are unique in character, since the transactions in each currency are made outside the country where that currency originates.

The Euro-dollar market attracts funds by offering high rates of interest, greater flexibility of maturities and a wider range of investment qualities.

Though Euro-dollar market is wholly unofficial in character, it's become an indispensable a part of the international monetary system. It's one of the largest markets for short-term funds.

FEATURES OF THE EURO –DOLLAR MARKET

The Euro-dollar market has the subsequent characteristics:

1. It's emerged as a truly international short-term money market.

2. It's unofficial but profound.

3. It's free.

4. It's competitive.

5. It's a more flexible capital market.

Original customers of the Euro-dollar market were the business firms in Europe and therefore the far east which found Euro-dollars a cheaper way of financing their imports from the us, since the lending rates of dollars within the Euro-dollar market were relatively less.

The Euro-dollar market has two facts:

(i) it's a market which accepts dollar deposits from the non-banking public and gives credit in dollars to the needy non-banking public.

(ii) It’s an inter-bank market in which the commercial banks can adjust their foreign currency position through inter-bank lending and borrowing.

The existence of Euro-dollar market during a country, however, depends on the freedom given to the commercial banks to hold, borrow and lend foreign currencies — especially dollars — and to exchange them at fixed official rate of exchange.

BENEFITS OF THE EURO-DOLLAR MARKET:

Following benefits seem to have accrued to the countries involved within the Euro-dollar market:

1. It’s provided a truly international short-term capital market, owing to a high degree of mobility of the Euro-dollars.

2. Euro-dollars are useful for the financing of foreign trade.

3. It's enabled the financial institutions to have greater flexibility in adjusting their cash and liquidity positions.

4. Its enabled importers and exporters to borrow dollars for financing trade, at cheaper rates than otherwise obtainable.

5. It helped in reducing the profit margins between deposit rates and lending rates.

6. It's enhanced the quantum of funds available for arbitrage.

7. Its enabled monetary authorities with inadequate reserves to extend their reserves by borrowing Euro-dollar deposits.

8. It's enlarged the facilities available for short-term investment.

9. It's caused the levels of national interest rates more like international influences.

EFFECTS OF EURO DOLLAR MARKET ON INTERNATIONAL FINANCIAL SYSTEM:

1. The position of dollar has been strengthened temporarily, since its operations of borrowing of dollars have become more profitable rather than its holdings.

2. It facilitates the financing of balance of payments surpluses and deficits. Especially, countries having deficit balance of payments tend to borrow funds from the Euro-dollar market, thereby lightening the pressure on their foreign exchange reserves.

3. Its promoted international monetary cooperation.

4. Over the last decade, the expansion of Euro-dollar has helped in easing of the world liquidity problem.

SHORTCOMINGS OF THE EURO-DOLLAR MARKET:

The major drawbacks of the Euro-dollar market could also be mentioned as under:

1. It may lead banks and business firms to overtrade.

2. It may weaken discipline within the banking communities.

3. It involves a grave danger of sudden large- scale withdrawal of credits to a country.

4. It rendered official monetary policies less effective for the countries involved.

In fact, the Euro-dollar market has created two major problems for an individual country dealing in it. Firstly, there's the danger of over-extension of the dollar credit by domestic banks of the country; consequently, high demand pressure on the official foreign exchange may take place.

Secondly, the Euro-dollar market appears as another channel for the short-term international capital movement for the country, so that the country’s volume of outflow or inflow capital may increase which can again endanger the foreign exchange reserves and therefore the effectiveness of domestic economic policies.

It has destabilisation effect. It increases the pressure on rate of exchange and official foreign exchange reserves. This might require additional liquidity. If such additional reserves aren't provided, it may endanger existence of the present gold exchange standard.

Above all, the Euro-dollar market has caused the growth of semi-independent international interest rates, on which there are often no effective control by one country or an institution.

2.2.1 Meaning of Foreign Exchange Rate

Foreign Exchange Rate is defined as the price of the domestic currency with respect to another currency. The purpose of foreign exchange is to compare one currency with another for showing their relative values.

Foreign exchange rate can also be said to be the rate at which one currency is exchanged with another or it can be said as the price of one currency that is stated in terms of another currency.

Exchange rates of a currency can be either fixed or floating. Fixed exchange rate is determined by the central bank of the country while the floating rate is determined by the dynamics of market demand and supply.

2.2.2 Fixed and Flexible Exchange Rate- Merits and Demerits

Under inconvertible paper money standard, there are often two sorts of exchange rates -— fixed and flexible. Under this monetary system of the International monetary fund (IMF), fixed or stable exchange rates are referred to as pegged exchange rates or par values.

In fact, IMF was established with the object of stabilising the rates of exchange, with proper safeguards for adjustments whenever necessary. On the opposite hand, free or flexible exchange rates are left uninterrupted by the monetary authorities to be determined by the forces of demand and supply in the foreign exchange market.

Thus, flexible exchange rates are determined by the conditions of demand for and provide of exchange and are perfectly free to fluctuate consistent with the changes in the demand or supply forces, if there are not any restrictions on buying and selling in the foreign exchange market.

The free or floating rate is allowed to hunt its own level, as no par of exchange is fixed. Sometimes when a currency is floated a former fixed par no longer applies, and therefore the government also doesn't care to enforce it.

Under the system of fixed pars, as adopted by the IMF member nations, the rate of exchange is decided by the govt and enforced either by pegging operation, or by resorting to some sort of exchange control and sometimes by a healthy combination of both these methods.

Under the pegging operation, the govt fixes an official par of exchange and tries to enforce it through central bank or a sort of exchange stabilisation fund which enters foreign exchange market and buy its currency when the market rate falls below the required level and sell it when the rate rises above a specific mark.

This system of pegged rates of exchange is government propped up. There is, however, one major defect in this system that if the market rate of exchange features a consistent tendency to decline, pegging operations would be very expensive, because it would cause a heavy reduction in the exchange reserves of the country concerned.

Recently, therefore, it's been held by many whom the IMF’s system of adjustable stable exchange rates isn't desirable which free or fluctuating exchange rates would be more helpful in adjusting prevailing rates of exchange to their true value.

It is a highly debatable question on whether the fixed rate of exchange system is good or the fluctuating rate of exchange is better.

Difference between Fixed and flexible Exchange Rate

A study of economic history shows that three different rate of exchange systems are prevailing in the world economy. The first rate of exchange system, popularly called Gold Standard prevailed over 1879-1934 period with the exception of war I years.

Under the gold standard, currencies of various countries were tied to gold (that is, the value of currency of every country was fixed in terms of an exact quantity of gold). With this the rate of exchange between different countries got automatically fixed.

Thus, the gold standard represented fixed rate of exchange system. As explained above, from the end of World War II to 1971, another fixed rate of exchange system, generally referred to as Bretton Woods System prevailed. Under this the US dollar was tied to an exact quantity of gold and therefore the currencies of other countries were tied to dollar or in some countries directly to gold.

However, in 1971 thanks to large and persist deficit in balance of payments of the United States. Bretton Woods system also broke down. Since then, the flexible or what's also called floating rate of exchange system has been existing but even during this flexible or floating exchange rates the govt (or the Central Bank) of the countries intervenes to keep the international value of their currencies (i.e., exchanges rate) within certain limits.

Therefore, even in the post 1971 period, the rate of exchange system isn't purely flexible and has therefore been called Managed Float System.

Merits of Fixed Exchange Rate System – (a) Fixed exchange rate prevents the member countries from the economic fluctuation which can weaken the economic policies.

(b) It promotes capital movements. Fixed exchange rate system attracts foreign capital because a stable currency does not involve any uncertainties about exchange rate that may cause capital loss.

Demerits of Fixed Exchange Rate System –

(a) It creates a barrier on achieving the objective of free markets.

(b) Under this system, countries with deficits in balance of payment uses their stock of gold and foreign currencies to solve the problem. This can further create serious problem for them. They may be forced to devalue their currency. On the other hand, countries with surplus in balance of payments will face the problem of inflation.

Merits of Flexible Exchange Rate System

(a) It eliminates the problem of overvaluation or undervaluation of currencies, Deficit or surplus in balance of payments is automatically corrected under this system.

(b) It frees the government from problem of balance of payments. Demerits of Flexible Exchange Rate System

The main demerits of flexible exchange rate are as follows:

(a) It creates situations of instability and uncertainty. Wide fluctuations in exchange rate are possible. This hampers foreign trade and capital movements between countries.

(b) The uncertainty caused by currency fluctuations can discourage international trade and investments.

2.2.3 Determination of Foreign Exchange Rate: Purchasing Power Parity Theory

The purchasing power parity theory was propounded by Professor Gustav Cassel of Sweden. According to this theory, rate of exchange between two countries depends upon the relative purchasing power of their respective currencies. One popular macroeconomic analysis metric to compare economic productivity and standards of living between countries is purchasing power parity (PPP). PPP is an economic theory that compares different countries' currencies through a "basket of goods" approach. According to this concept, two currencies are in equilibrium—known as the currencies being at par—when a basket of goods is priced the same in both countries, taking into account the exchange rates.

Meaning: The theory aims to determine the adjustments needed to be made in the exchange rates of two currencies to make them at par with the purchasing power of each other. In other words, the expenditure on a similar commodity must be same in both currencies when accounted for exchange rate. The purchasing power of each currency is determined in the process.

Description: Purchasing power parity is used worldwide to compare the income levels in different countries. PPP thus makes it easy to understand and interpret the data of each country.

Example: Let's say that a pair of shoes costs Rs 2500 in India. Then it should cost $50 in America when the exchange rate is 50 between the dollar and the rupee.

Suppose in the USA one $ purchases a given collection of commodities. In India, same collection of goods costs 60 rupees. Then rate of exchange will tend to be $ 1 = 60 rupees. Now, suppose the price levels in the two countries remain the same but somehow exchange rate moves to $1=61 rupees.

This means that one US$ can purchase commodities worth more than 46 rupees. It will pay people to convert dollars into rupees at this rate, ($1 = Rs. 61), purchase the given collection of commodities in India for 60 rupees and sell them in U.S.A. For one dollar again, making a profit of 1 rupee per dollar worth of transactions.

This will create a large demand for rupees in the USA while supply thereof will be less because very few people would export commodities from USA to India. The value of the rupee in terms of the dollar will move up until it will reach $1 = 60 rupees. At that point, imports from India will not give abnormal profits. $ 1 = 60 rupees and is called the purchasing power parity between the two countries.

Thus, while the value of the unit of one currency in terms of another currency is determined at any particular time by the market conditions of demand and supply, in the long run the exchange rate is determined by the relative values of the two currencies as indicated by their respective purchasing powers over goods and services.

In other words, the rate of exchange tends to rest at the point which expresses equality between the respective purchasing powers of the two currencies. This point is called the purchasing power parity. Thus, under a system of autonomous paper standards the external value of a currency is said to depend ultimately on the domestic purchasing power of that currency relative to that of another currency. In other words, exchange rates, under such a system, tend to be determined by the relative purchasing power parities of different currencies in different countries.

In the above example, if prices in India get doubled, prices in the USA remaining the same, the value of the rupee will be exactly halved. The new parity will be $ 1 = 120 rupees. This is because now 120 rupees will buy the same collection of commodities in India which 60 rupees did before. We suppose that prices in the USA remain as before. But if prices in both countries get doubled, there will be no change in the parity.

In actual practice, however, the parity will be modified by the cost of transporting goods (including duties etc.) from one country to another.

References:

1. Dr.D.M.Mithani – International Economics (Himalaya Publishing house ltd)

2. Bo Sodersten, Geoffirey Reed, International Economics (3rd Edition) Publisher Red Globe Press

3. Z.M.Jhingan : International Economics (Vrinda Publication)

4. Robert Feenstra, Alan M Taylor, International Trade (5th Edition) Publisher Worth

5. Dr.Mrs.NirmalBhalerao&S.S.M.Desai – International Economics (Himalaya Publishing house ltd)

Unit 2

Foreign Exchange

2.1.1 Meaning

The foreign exchange Market is a market where the buyers and sellers are involved within the sale and purchase of foreign currencies. In other words, a market where the currencies of various countries are bought and sold is named a foreign exchange market. The structure of the foreign exchange market constitutes central banks, commercial banks, brokers, exporters and importers, immigrants, investors, tourists. These are the main players of the foreign market.

Currencies are always traded in pairs; therefore the "value" of 1 of the currencies in that pair is relative to the worth of the opposite. This determines what proportion of country A's currency country B can purchase, and the other way around. Establishing this relationship (price) for the global markets is that the main function of the foreign exchange market. This also greatly enhances liquidity in all other financial markets, which is essential to overall stability. The foreign exchange market is an over-the-counter (OTC) marketplace that determines the rate of exchange for global currencies. It is, by far, the most important financial market in the world and is comprised of a worldwide network of monetary centres that transact 24 hours daily, closing only on the weekends. Currencies are always traded in pairs, therefore the "value" of 1 of the currencies therein pair is relative to the value of the opposite.

The following are the key points:

• The foreign exchange (also referred to as FX or FOREX) market is a global marketplace for exchanging national currencies against each other.

• Because of the worldwide reach of trade, commerce, and finance, FOREX markets tend to be the most important and most liquid asset markets within the world.

• Currencies trade against one another as exchange rate pairs. For instance, EUR/USD.

• FOREX markets exist as spot (cash) markets also as derivatives markets offering forwards, futures, options, and currency swaps.

• Market participants use FOREX to hedge against international currency and rate of interest risk, to speculate on geopolitical events, and to diversify portfolios, among several other reasons.

2.1.2 Functions

1. Transfer Function: the essential and the most visible function of exchange market is the transfer of funds (foreign currency) from one country to a different for the settlement of payments. It basically includes the conversion of 1 currency to another, wherein the role of FOREX is to transfer the purchasing power from one country to another.

For example, if the exporter of India import goods from the USA and the payment is to be made in dollars, then the conversion of the rupee to the dollar are going to be facilitated by FOREX. The transfer function is performed through a use of credit instruments, like bank drafts, bills of foreign exchange, and telephone transfers.

2. Credit Function: FOREX provides a short-term credit to the importers so on facilitate the smooth flow of products and services from country to country. An importer can use credit to finance the foreign purchases. Like an Indian company wants to get the machinery from the USA, pays for the purchase by issuing a bill of exchange within the exchange market, essentially with a three-month maturity.

3. Hedging Function: The third function of a foreign exchange market is to hedge foreign exchange risks. The parties to the exchange are often scared of the fluctuations in the exchange rates, i.e., the worth of 1 currency in terms of another. The change in the rate of exchange may end in a gain or loss to the party concerned.

Thus, because of this reason the FOREX provides the services for hedging the anticipated or actual claims/liabilities in exchange for the forward contracts. A forward contract is typically a three-month contract to buy or sell the exchange for another currency at a fixed date within the future at a price agreed upon today. Thus, no money is exchanged at the time of the contract.

There are several dealers within the foreign exchange markets, the foremost important amongst them are the banks. The banks have their branches in several countries through which the exchange is facilitated; such service of a bank is named as Exchange Banks.

2.1.3 Structure

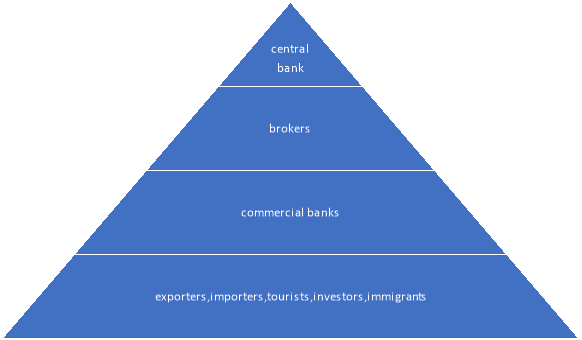

The structure of the foreign exchange market constitutes central banks, commercial banks, brokers, exporters and importers, immigrants, investors, tourists. These are the main players of the foreign market; their position and place are shown within the figure below-

At the bottom of a pyramid are the actual buyers and sellers of the foreign currencies- exporters, importers, tourist, investors, and immigrants. They're actual users of the currencies and approach commercial banks to buy it.

The commercial banks are the second most significant organ of the foreign exchange market. The banks dealing in exchange play a task of “market makers”, within the sense that they quote on a routine the foreign exchange rates for buying and selling of the foreign currencies. Also, they function as clearing houses, thereby helping in wiping out the difference between the demand for and therefore the supply of currencies. These banks buy the currencies from the brokers and sell it to the buyers.

The third layer of a pyramid constitutes the foreign exchange brokers. These brokers function as a link between the central bank and therefore the commercial banks and also between the actual buyers and commercial banks. They're the main source of market information. These are the persons who don't themselves buy the foreign currency, but rather strike a deal between the buyer and therefore the seller on a commission basis.

The central bank of any country is that the apex body within the organization of the exchange market. They work because the lender of the last resort and therefore the custodian of foreign exchange of the country. The central bank has the power to regulate and control the foreign exchange market so on assures that it works within the orderly fashion. One among the main functions of the central bank is to stop the aggressive fluctuations within the foreign exchange market, if necessary, by direct intervention. Intervention within the form of selling the currency when it's overvalued and buying it when it tends to be undervalued.

2.1.4 Euro Dollar Market

By Euro-dollar is meant all U.S. Dollar deposits in banks outside the United States, including the foreign branches of U.S. Banks. A Euro-dollar is, however, not a special type of dollar. It bears the same exchange rate as an ordinary U.S. Dollar has in terms of other currencies.

Euro-dollar transactions are conducted by banks not resident within the us. For example, when an American citizen deposits (lends) his funds with a U.S. Bank in London, which can again be wont to make advances to a business enterprise within the U.S., then such transactions are stated as Euro-dollar transactions. All Euro-dollar transactions are, however, unsecured credit.

Euro-dollars have inherited existence on account of the Regulation issued by the Board of Governors of the U.S. Federal Reserve System, which doesn't permit the banks to pay interest to the depositors above a certain limit.

As such, banks outside the us tend to expand their dollar business by offering higher deposit rates and charging lower lending rates, as compared to the banks inside the U.S. Increase or decrease within the potential for Euro-dollar holdings, however, depends, directly upon U.S. Deficits and surplus, respectively.

EURO-DOLLAR MARKET:

Euro-dollar market is that the creation of the international bankers. It's simply a short-term market facilitating banks’ borrowings and lending’s of U.S. Dollars. The Euro-dollar market is principally located in Europe and basically deals in U.S. Dollars.

But, during a wider sense, Euro-dollar market is confined to the external lending and borrowing of the world’s most vital convertible currencies like dollar, pound, sterling, Swiss franc, French franc, deutsche mark and therefore the Netherlands guilder.

In short, the term Euro-dollar is used as a common term to include the external markets in all the major convertible currencies.

Euro-dollar operations are unique in character, since the transactions in each currency are made outside the country where that currency originates.

The Euro-dollar market attracts funds by offering high rates of interest, greater flexibility of maturities and a wider range of investment qualities.

Though Euro-dollar market is wholly unofficial in character, it's become an indispensable a part of the international monetary system. It's one of the largest markets for short-term funds.

FEATURES OF THE EURO –DOLLAR MARKET

The Euro-dollar market has the subsequent characteristics:

1. It's emerged as a truly international short-term money market.

2. It's unofficial but profound.

3. It's free.

4. It's competitive.

5. It's a more flexible capital market.

Original customers of the Euro-dollar market were the business firms in Europe and therefore the far east which found Euro-dollars a cheaper way of financing their imports from the us, since the lending rates of dollars within the Euro-dollar market were relatively less.

The Euro-dollar market has two facts:

(i) it's a market which accepts dollar deposits from the non-banking public and gives credit in dollars to the needy non-banking public.

(ii) It’s an inter-bank market in which the commercial banks can adjust their foreign currency position through inter-bank lending and borrowing.

The existence of Euro-dollar market during a country, however, depends on the freedom given to the commercial banks to hold, borrow and lend foreign currencies — especially dollars — and to exchange them at fixed official rate of exchange.

BENEFITS OF THE EURO-DOLLAR MARKET:

Following benefits seem to have accrued to the countries involved within the Euro-dollar market:

1. It’s provided a truly international short-term capital market, owing to a high degree of mobility of the Euro-dollars.

2. Euro-dollars are useful for the financing of foreign trade.

3. It's enabled the financial institutions to have greater flexibility in adjusting their cash and liquidity positions.

4. Its enabled importers and exporters to borrow dollars for financing trade, at cheaper rates than otherwise obtainable.

5. It helped in reducing the profit margins between deposit rates and lending rates.

6. It's enhanced the quantum of funds available for arbitrage.

7. Its enabled monetary authorities with inadequate reserves to extend their reserves by borrowing Euro-dollar deposits.

8. It's enlarged the facilities available for short-term investment.

9. It's caused the levels of national interest rates more like international influences.

EFFECTS OF EURO DOLLAR MARKET ON INTERNATIONAL FINANCIAL SYSTEM:

1. The position of dollar has been strengthened temporarily, since its operations of borrowing of dollars have become more profitable rather than its holdings.

2. It facilitates the financing of balance of payments surpluses and deficits. Especially, countries having deficit balance of payments tend to borrow funds from the Euro-dollar market, thereby lightening the pressure on their foreign exchange reserves.

3. Its promoted international monetary cooperation.

4. Over the last decade, the expansion of Euro-dollar has helped in easing of the world liquidity problem.

SHORTCOMINGS OF THE EURO-DOLLAR MARKET:

The major drawbacks of the Euro-dollar market could also be mentioned as under:

1. It may lead banks and business firms to overtrade.

2. It may weaken discipline within the banking communities.

3. It involves a grave danger of sudden large- scale withdrawal of credits to a country.

4. It rendered official monetary policies less effective for the countries involved.

In fact, the Euro-dollar market has created two major problems for an individual country dealing in it. Firstly, there's the danger of over-extension of the dollar credit by domestic banks of the country; consequently, high demand pressure on the official foreign exchange may take place.

Secondly, the Euro-dollar market appears as another channel for the short-term international capital movement for the country, so that the country’s volume of outflow or inflow capital may increase which can again endanger the foreign exchange reserves and therefore the effectiveness of domestic economic policies.

It has destabilisation effect. It increases the pressure on rate of exchange and official foreign exchange reserves. This might require additional liquidity. If such additional reserves aren't provided, it may endanger existence of the present gold exchange standard.

Above all, the Euro-dollar market has caused the growth of semi-independent international interest rates, on which there are often no effective control by one country or an institution.

2.2.1 Meaning of Foreign Exchange Rate

Foreign Exchange Rate is defined as the price of the domestic currency with respect to another currency. The purpose of foreign exchange is to compare one currency with another for showing their relative values.

Foreign exchange rate can also be said to be the rate at which one currency is exchanged with another or it can be said as the price of one currency that is stated in terms of another currency.

Exchange rates of a currency can be either fixed or floating. Fixed exchange rate is determined by the central bank of the country while the floating rate is determined by the dynamics of market demand and supply.

2.2.2 Fixed and Flexible Exchange Rate- Merits and Demerits

Under inconvertible paper money standard, there are often two sorts of exchange rates -— fixed and flexible. Under this monetary system of the International monetary fund (IMF), fixed or stable exchange rates are referred to as pegged exchange rates or par values.

In fact, IMF was established with the object of stabilising the rates of exchange, with proper safeguards for adjustments whenever necessary. On the opposite hand, free or flexible exchange rates are left uninterrupted by the monetary authorities to be determined by the forces of demand and supply in the foreign exchange market.

Thus, flexible exchange rates are determined by the conditions of demand for and provide of exchange and are perfectly free to fluctuate consistent with the changes in the demand or supply forces, if there are not any restrictions on buying and selling in the foreign exchange market.

The free or floating rate is allowed to hunt its own level, as no par of exchange is fixed. Sometimes when a currency is floated a former fixed par no longer applies, and therefore the government also doesn't care to enforce it.

Under the system of fixed pars, as adopted by the IMF member nations, the rate of exchange is decided by the govt and enforced either by pegging operation, or by resorting to some sort of exchange control and sometimes by a healthy combination of both these methods.

Under the pegging operation, the govt fixes an official par of exchange and tries to enforce it through central bank or a sort of exchange stabilisation fund which enters foreign exchange market and buy its currency when the market rate falls below the required level and sell it when the rate rises above a specific mark.

This system of pegged rates of exchange is government propped up. There is, however, one major defect in this system that if the market rate of exchange features a consistent tendency to decline, pegging operations would be very expensive, because it would cause a heavy reduction in the exchange reserves of the country concerned.

Recently, therefore, it's been held by many whom the IMF’s system of adjustable stable exchange rates isn't desirable which free or fluctuating exchange rates would be more helpful in adjusting prevailing rates of exchange to their true value.

It is a highly debatable question on whether the fixed rate of exchange system is good or the fluctuating rate of exchange is better.

Difference between Fixed and flexible Exchange Rate

A study of economic history shows that three different rate of exchange systems are prevailing in the world economy. The first rate of exchange system, popularly called Gold Standard prevailed over 1879-1934 period with the exception of war I years.

Under the gold standard, currencies of various countries were tied to gold (that is, the value of currency of every country was fixed in terms of an exact quantity of gold). With this the rate of exchange between different countries got automatically fixed.

Thus, the gold standard represented fixed rate of exchange system. As explained above, from the end of World War II to 1971, another fixed rate of exchange system, generally referred to as Bretton Woods System prevailed. Under this the US dollar was tied to an exact quantity of gold and therefore the currencies of other countries were tied to dollar or in some countries directly to gold.

However, in 1971 thanks to large and persist deficit in balance of payments of the United States. Bretton Woods system also broke down. Since then, the flexible or what's also called floating rate of exchange system has been existing but even during this flexible or floating exchange rates the govt (or the Central Bank) of the countries intervenes to keep the international value of their currencies (i.e., exchanges rate) within certain limits.

Therefore, even in the post 1971 period, the rate of exchange system isn't purely flexible and has therefore been called Managed Float System.

Merits of Fixed Exchange Rate System – (a) Fixed exchange rate prevents the member countries from the economic fluctuation which can weaken the economic policies.

(b) It promotes capital movements. Fixed exchange rate system attracts foreign capital because a stable currency does not involve any uncertainties about exchange rate that may cause capital loss.

Demerits of Fixed Exchange Rate System –

(a) It creates a barrier on achieving the objective of free markets.

(b) Under this system, countries with deficits in balance of payment uses their stock of gold and foreign currencies to solve the problem. This can further create serious problem for them. They may be forced to devalue their currency. On the other hand, countries with surplus in balance of payments will face the problem of inflation.

Merits of Flexible Exchange Rate System

(a) It eliminates the problem of overvaluation or undervaluation of currencies, Deficit or surplus in balance of payments is automatically corrected under this system.

(b) It frees the government from problem of balance of payments. Demerits of Flexible Exchange Rate System

The main demerits of flexible exchange rate are as follows:

(a) It creates situations of instability and uncertainty. Wide fluctuations in exchange rate are possible. This hampers foreign trade and capital movements between countries.

(b) The uncertainty caused by currency fluctuations can discourage international trade and investments.

2.2.3 Determination of Foreign Exchange Rate: Purchasing Power Parity Theory

The purchasing power parity theory was propounded by Professor Gustav Cassel of Sweden. According to this theory, rate of exchange between two countries depends upon the relative purchasing power of their respective currencies. One popular macroeconomic analysis metric to compare economic productivity and standards of living between countries is purchasing power parity (PPP). PPP is an economic theory that compares different countries' currencies through a "basket of goods" approach. According to this concept, two currencies are in equilibrium—known as the currencies being at par—when a basket of goods is priced the same in both countries, taking into account the exchange rates.

Meaning: The theory aims to determine the adjustments needed to be made in the exchange rates of two currencies to make them at par with the purchasing power of each other. In other words, the expenditure on a similar commodity must be same in both currencies when accounted for exchange rate. The purchasing power of each currency is determined in the process.

Description: Purchasing power parity is used worldwide to compare the income levels in different countries. PPP thus makes it easy to understand and interpret the data of each country.

Example: Let's say that a pair of shoes costs Rs 2500 in India. Then it should cost $50 in America when the exchange rate is 50 between the dollar and the rupee.

Suppose in the USA one $ purchases a given collection of commodities. In India, same collection of goods costs 60 rupees. Then rate of exchange will tend to be $ 1 = 60 rupees. Now, suppose the price levels in the two countries remain the same but somehow exchange rate moves to $1=61 rupees.

This means that one US$ can purchase commodities worth more than 46 rupees. It will pay people to convert dollars into rupees at this rate, ($1 = Rs. 61), purchase the given collection of commodities in India for 60 rupees and sell them in U.S.A. For one dollar again, making a profit of 1 rupee per dollar worth of transactions.

This will create a large demand for rupees in the USA while supply thereof will be less because very few people would export commodities from USA to India. The value of the rupee in terms of the dollar will move up until it will reach $1 = 60 rupees. At that point, imports from India will not give abnormal profits. $ 1 = 60 rupees and is called the purchasing power parity between the two countries.

Thus, while the value of the unit of one currency in terms of another currency is determined at any particular time by the market conditions of demand and supply, in the long run the exchange rate is determined by the relative values of the two currencies as indicated by their respective purchasing powers over goods and services.

In other words, the rate of exchange tends to rest at the point which expresses equality between the respective purchasing powers of the two currencies. This point is called the purchasing power parity. Thus, under a system of autonomous paper standards the external value of a currency is said to depend ultimately on the domestic purchasing power of that currency relative to that of another currency. In other words, exchange rates, under such a system, tend to be determined by the relative purchasing power parities of different currencies in different countries.

In the above example, if prices in India get doubled, prices in the USA remaining the same, the value of the rupee will be exactly halved. The new parity will be $ 1 = 120 rupees. This is because now 120 rupees will buy the same collection of commodities in India which 60 rupees did before. We suppose that prices in the USA remain as before. But if prices in both countries get doubled, there will be no change in the parity.

In actual practice, however, the parity will be modified by the cost of transporting goods (including duties etc.) from one country to another.

References:

1. Dr.D.M.Mithani – International Economics (Himalaya Publishing house ltd)

2. Bo Sodersten, Geoffirey Reed, International Economics (3rd Edition) Publisher Red Globe Press

3. Z.M.Jhingan : International Economics (Vrinda Publication)

4. Robert Feenstra, Alan M Taylor, International Trade (5th Edition) Publisher Worth

5. Dr.Mrs.NirmalBhalerao&S.S.M.Desai – International Economics (Himalaya Publishing house ltd)

Unit 2

Foreign Exchange

2.1.1 Meaning

The foreign exchange Market is a market where the buyers and sellers are involved within the sale and purchase of foreign currencies. In other words, a market where the currencies of various countries are bought and sold is named a foreign exchange market. The structure of the foreign exchange market constitutes central banks, commercial banks, brokers, exporters and importers, immigrants, investors, tourists. These are the main players of the foreign market.

Currencies are always traded in pairs; therefore the "value" of 1 of the currencies in that pair is relative to the worth of the opposite. This determines what proportion of country A's currency country B can purchase, and the other way around. Establishing this relationship (price) for the global markets is that the main function of the foreign exchange market. This also greatly enhances liquidity in all other financial markets, which is essential to overall stability. The foreign exchange market is an over-the-counter (OTC) marketplace that determines the rate of exchange for global currencies. It is, by far, the most important financial market in the world and is comprised of a worldwide network of monetary centres that transact 24 hours daily, closing only on the weekends. Currencies are always traded in pairs, therefore the "value" of 1 of the currencies therein pair is relative to the value of the opposite.

The following are the key points:

• The foreign exchange (also referred to as FX or FOREX) market is a global marketplace for exchanging national currencies against each other.

• Because of the worldwide reach of trade, commerce, and finance, FOREX markets tend to be the most important and most liquid asset markets within the world.

• Currencies trade against one another as exchange rate pairs. For instance, EUR/USD.

• FOREX markets exist as spot (cash) markets also as derivatives markets offering forwards, futures, options, and currency swaps.

• Market participants use FOREX to hedge against international currency and rate of interest risk, to speculate on geopolitical events, and to diversify portfolios, among several other reasons.

2.1.2 Functions

1. Transfer Function: the essential and the most visible function of exchange market is the transfer of funds (foreign currency) from one country to a different for the settlement of payments. It basically includes the conversion of 1 currency to another, wherein the role of FOREX is to transfer the purchasing power from one country to another.

For example, if the exporter of India import goods from the USA and the payment is to be made in dollars, then the conversion of the rupee to the dollar are going to be facilitated by FOREX. The transfer function is performed through a use of credit instruments, like bank drafts, bills of foreign exchange, and telephone transfers.

2. Credit Function: FOREX provides a short-term credit to the importers so on facilitate the smooth flow of products and services from country to country. An importer can use credit to finance the foreign purchases. Like an Indian company wants to get the machinery from the USA, pays for the purchase by issuing a bill of exchange within the exchange market, essentially with a three-month maturity.

3. Hedging Function: The third function of a foreign exchange market is to hedge foreign exchange risks. The parties to the exchange are often scared of the fluctuations in the exchange rates, i.e., the worth of 1 currency in terms of another. The change in the rate of exchange may end in a gain or loss to the party concerned.

Thus, because of this reason the FOREX provides the services for hedging the anticipated or actual claims/liabilities in exchange for the forward contracts. A forward contract is typically a three-month contract to buy or sell the exchange for another currency at a fixed date within the future at a price agreed upon today. Thus, no money is exchanged at the time of the contract.

There are several dealers within the foreign exchange markets, the foremost important amongst them are the banks. The banks have their branches in several countries through which the exchange is facilitated; such service of a bank is named as Exchange Banks.

2.1.3 Structure

The structure of the foreign exchange market constitutes central banks, commercial banks, brokers, exporters and importers, immigrants, investors, tourists. These are the main players of the foreign market; their position and place are shown within the figure below-

At the bottom of a pyramid are the actual buyers and sellers of the foreign currencies- exporters, importers, tourist, investors, and immigrants. They're actual users of the currencies and approach commercial banks to buy it.

The commercial banks are the second most significant organ of the foreign exchange market. The banks dealing in exchange play a task of “market makers”, within the sense that they quote on a routine the foreign exchange rates for buying and selling of the foreign currencies. Also, they function as clearing houses, thereby helping in wiping out the difference between the demand for and therefore the supply of currencies. These banks buy the currencies from the brokers and sell it to the buyers.

The third layer of a pyramid constitutes the foreign exchange brokers. These brokers function as a link between the central bank and therefore the commercial banks and also between the actual buyers and commercial banks. They're the main source of market information. These are the persons who don't themselves buy the foreign currency, but rather strike a deal between the buyer and therefore the seller on a commission basis.

The central bank of any country is that the apex body within the organization of the exchange market. They work because the lender of the last resort and therefore the custodian of foreign exchange of the country. The central bank has the power to regulate and control the foreign exchange market so on assures that it works within the orderly fashion. One among the main functions of the central bank is to stop the aggressive fluctuations within the foreign exchange market, if necessary, by direct intervention. Intervention within the form of selling the currency when it's overvalued and buying it when it tends to be undervalued.

2.1.4 Euro Dollar Market

By Euro-dollar is meant all U.S. Dollar deposits in banks outside the United States, including the foreign branches of U.S. Banks. A Euro-dollar is, however, not a special type of dollar. It bears the same exchange rate as an ordinary U.S. Dollar has in terms of other currencies.

Euro-dollar transactions are conducted by banks not resident within the us. For example, when an American citizen deposits (lends) his funds with a U.S. Bank in London, which can again be wont to make advances to a business enterprise within the U.S., then such transactions are stated as Euro-dollar transactions. All Euro-dollar transactions are, however, unsecured credit.

Euro-dollars have inherited existence on account of the Regulation issued by the Board of Governors of the U.S. Federal Reserve System, which doesn't permit the banks to pay interest to the depositors above a certain limit.

As such, banks outside the us tend to expand their dollar business by offering higher deposit rates and charging lower lending rates, as compared to the banks inside the U.S. Increase or decrease within the potential for Euro-dollar holdings, however, depends, directly upon U.S. Deficits and surplus, respectively.

EURO-DOLLAR MARKET:

Euro-dollar market is that the creation of the international bankers. It's simply a short-term market facilitating banks’ borrowings and lending’s of U.S. Dollars. The Euro-dollar market is principally located in Europe and basically deals in U.S. Dollars.

But, during a wider sense, Euro-dollar market is confined to the external lending and borrowing of the world’s most vital convertible currencies like dollar, pound, sterling, Swiss franc, French franc, deutsche mark and therefore the Netherlands guilder.

In short, the term Euro-dollar is used as a common term to include the external markets in all the major convertible currencies.

Euro-dollar operations are unique in character, since the transactions in each currency are made outside the country where that currency originates.

The Euro-dollar market attracts funds by offering high rates of interest, greater flexibility of maturities and a wider range of investment qualities.

Though Euro-dollar market is wholly unofficial in character, it's become an indispensable a part of the international monetary system. It's one of the largest markets for short-term funds.

FEATURES OF THE EURO –DOLLAR MARKET

The Euro-dollar market has the subsequent characteristics:

1. It's emerged as a truly international short-term money market.

2. It's unofficial but profound.

3. It's free.

4. It's competitive.

5. It's a more flexible capital market.

Original customers of the Euro-dollar market were the business firms in Europe and therefore the far east which found Euro-dollars a cheaper way of financing their imports from the us, since the lending rates of dollars within the Euro-dollar market were relatively less.

The Euro-dollar market has two facts:

(i) it's a market which accepts dollar deposits from the non-banking public and gives credit in dollars to the needy non-banking public.

(ii) It’s an inter-bank market in which the commercial banks can adjust their foreign currency position through inter-bank lending and borrowing.

The existence of Euro-dollar market during a country, however, depends on the freedom given to the commercial banks to hold, borrow and lend foreign currencies — especially dollars — and to exchange them at fixed official rate of exchange.

BENEFITS OF THE EURO-DOLLAR MARKET:

Following benefits seem to have accrued to the countries involved within the Euro-dollar market:

1. It’s provided a truly international short-term capital market, owing to a high degree of mobility of the Euro-dollars.

2. Euro-dollars are useful for the financing of foreign trade.

3. It's enabled the financial institutions to have greater flexibility in adjusting their cash and liquidity positions.

4. Its enabled importers and exporters to borrow dollars for financing trade, at cheaper rates than otherwise obtainable.

5. It helped in reducing the profit margins between deposit rates and lending rates.

6. It's enhanced the quantum of funds available for arbitrage.

7. Its enabled monetary authorities with inadequate reserves to extend their reserves by borrowing Euro-dollar deposits.

8. It's enlarged the facilities available for short-term investment.

9. It's caused the levels of national interest rates more like international influences.

EFFECTS OF EURO DOLLAR MARKET ON INTERNATIONAL FINANCIAL SYSTEM:

1. The position of dollar has been strengthened temporarily, since its operations of borrowing of dollars have become more profitable rather than its holdings.

2. It facilitates the financing of balance of payments surpluses and deficits. Especially, countries having deficit balance of payments tend to borrow funds from the Euro-dollar market, thereby lightening the pressure on their foreign exchange reserves.

3. Its promoted international monetary cooperation.

4. Over the last decade, the expansion of Euro-dollar has helped in easing of the world liquidity problem.

SHORTCOMINGS OF THE EURO-DOLLAR MARKET:

The major drawbacks of the Euro-dollar market could also be mentioned as under:

1. It may lead banks and business firms to overtrade.

2. It may weaken discipline within the banking communities.

3. It involves a grave danger of sudden large- scale withdrawal of credits to a country.

4. It rendered official monetary policies less effective for the countries involved.

In fact, the Euro-dollar market has created two major problems for an individual country dealing in it. Firstly, there's the danger of over-extension of the dollar credit by domestic banks of the country; consequently, high demand pressure on the official foreign exchange may take place.

Secondly, the Euro-dollar market appears as another channel for the short-term international capital movement for the country, so that the country’s volume of outflow or inflow capital may increase which can again endanger the foreign exchange reserves and therefore the effectiveness of domestic economic policies.

It has destabilisation effect. It increases the pressure on rate of exchange and official foreign exchange reserves. This might require additional liquidity. If such additional reserves aren't provided, it may endanger existence of the present gold exchange standard.

Above all, the Euro-dollar market has caused the growth of semi-independent international interest rates, on which there are often no effective control by one country or an institution.

2.2.1 Meaning of Foreign Exchange Rate

Foreign Exchange Rate is defined as the price of the domestic currency with respect to another currency. The purpose of foreign exchange is to compare one currency with another for showing their relative values.

Foreign exchange rate can also be said to be the rate at which one currency is exchanged with another or it can be said as the price of one currency that is stated in terms of another currency.

Exchange rates of a currency can be either fixed or floating. Fixed exchange rate is determined by the central bank of the country while the floating rate is determined by the dynamics of market demand and supply.

2.2.2 Fixed and Flexible Exchange Rate- Merits and Demerits

Under inconvertible paper money standard, there are often two sorts of exchange rates -— fixed and flexible. Under this monetary system of the International monetary fund (IMF), fixed or stable exchange rates are referred to as pegged exchange rates or par values.

In fact, IMF was established with the object of stabilising the rates of exchange, with proper safeguards for adjustments whenever necessary. On the opposite hand, free or flexible exchange rates are left uninterrupted by the monetary authorities to be determined by the forces of demand and supply in the foreign exchange market.

Thus, flexible exchange rates are determined by the conditions of demand for and provide of exchange and are perfectly free to fluctuate consistent with the changes in the demand or supply forces, if there are not any restrictions on buying and selling in the foreign exchange market.

The free or floating rate is allowed to hunt its own level, as no par of exchange is fixed. Sometimes when a currency is floated a former fixed par no longer applies, and therefore the government also doesn't care to enforce it.

Under the system of fixed pars, as adopted by the IMF member nations, the rate of exchange is decided by the govt and enforced either by pegging operation, or by resorting to some sort of exchange control and sometimes by a healthy combination of both these methods.

Under the pegging operation, the govt fixes an official par of exchange and tries to enforce it through central bank or a sort of exchange stabilisation fund which enters foreign exchange market and buy its currency when the market rate falls below the required level and sell it when the rate rises above a specific mark.

This system of pegged rates of exchange is government propped up. There is, however, one major defect in this system that if the market rate of exchange features a consistent tendency to decline, pegging operations would be very expensive, because it would cause a heavy reduction in the exchange reserves of the country concerned.

Recently, therefore, it's been held by many whom the IMF’s system of adjustable stable exchange rates isn't desirable which free or fluctuating exchange rates would be more helpful in adjusting prevailing rates of exchange to their true value.

It is a highly debatable question on whether the fixed rate of exchange system is good or the fluctuating rate of exchange is better.

Difference between Fixed and flexible Exchange Rate

A study of economic history shows that three different rate of exchange systems are prevailing in the world economy. The first rate of exchange system, popularly called Gold Standard prevailed over 1879-1934 period with the exception of war I years.

Under the gold standard, currencies of various countries were tied to gold (that is, the value of currency of every country was fixed in terms of an exact quantity of gold). With this the rate of exchange between different countries got automatically fixed.

Thus, the gold standard represented fixed rate of exchange system. As explained above, from the end of World War II to 1971, another fixed rate of exchange system, generally referred to as Bretton Woods System prevailed. Under this the US dollar was tied to an exact quantity of gold and therefore the currencies of other countries were tied to dollar or in some countries directly to gold.

However, in 1971 thanks to large and persist deficit in balance of payments of the United States. Bretton Woods system also broke down. Since then, the flexible or what's also called floating rate of exchange system has been existing but even during this flexible or floating exchange rates the govt (or the Central Bank) of the countries intervenes to keep the international value of their currencies (i.e., exchanges rate) within certain limits.

Therefore, even in the post 1971 period, the rate of exchange system isn't purely flexible and has therefore been called Managed Float System.

Merits of Fixed Exchange Rate System – (a) Fixed exchange rate prevents the member countries from the economic fluctuation which can weaken the economic policies.

(b) It promotes capital movements. Fixed exchange rate system attracts foreign capital because a stable currency does not involve any uncertainties about exchange rate that may cause capital loss.

Demerits of Fixed Exchange Rate System –

(a) It creates a barrier on achieving the objective of free markets.

(b) Under this system, countries with deficits in balance of payment uses their stock of gold and foreign currencies to solve the problem. This can further create serious problem for them. They may be forced to devalue their currency. On the other hand, countries with surplus in balance of payments will face the problem of inflation.

Merits of Flexible Exchange Rate System

(a) It eliminates the problem of overvaluation or undervaluation of currencies, Deficit or surplus in balance of payments is automatically corrected under this system.

(b) It frees the government from problem of balance of payments. Demerits of Flexible Exchange Rate System

The main demerits of flexible exchange rate are as follows:

(a) It creates situations of instability and uncertainty. Wide fluctuations in exchange rate are possible. This hampers foreign trade and capital movements between countries.

(b) The uncertainty caused by currency fluctuations can discourage international trade and investments.

2.2.3 Determination of Foreign Exchange Rate: Purchasing Power Parity Theory

The purchasing power parity theory was propounded by Professor Gustav Cassel of Sweden. According to this theory, rate of exchange between two countries depends upon the relative purchasing power of their respective currencies. One popular macroeconomic analysis metric to compare economic productivity and standards of living between countries is purchasing power parity (PPP). PPP is an economic theory that compares different countries' currencies through a "basket of goods" approach. According to this concept, two currencies are in equilibrium—known as the currencies being at par—when a basket of goods is priced the same in both countries, taking into account the exchange rates.

Meaning: The theory aims to determine the adjustments needed to be made in the exchange rates of two currencies to make them at par with the purchasing power of each other. In other words, the expenditure on a similar commodity must be same in both currencies when accounted for exchange rate. The purchasing power of each currency is determined in the process.

Description: Purchasing power parity is used worldwide to compare the income levels in different countries. PPP thus makes it easy to understand and interpret the data of each country.

Example: Let's say that a pair of shoes costs Rs 2500 in India. Then it should cost $50 in America when the exchange rate is 50 between the dollar and the rupee.

Suppose in the USA one $ purchases a given collection of commodities. In India, same collection of goods costs 60 rupees. Then rate of exchange will tend to be $ 1 = 60 rupees. Now, suppose the price levels in the two countries remain the same but somehow exchange rate moves to $1=61 rupees.

This means that one US$ can purchase commodities worth more than 46 rupees. It will pay people to convert dollars into rupees at this rate, ($1 = Rs. 61), purchase the given collection of commodities in India for 60 rupees and sell them in U.S.A. For one dollar again, making a profit of 1 rupee per dollar worth of transactions.

This will create a large demand for rupees in the USA while supply thereof will be less because very few people would export commodities from USA to India. The value of the rupee in terms of the dollar will move up until it will reach $1 = 60 rupees. At that point, imports from India will not give abnormal profits. $ 1 = 60 rupees and is called the purchasing power parity between the two countries.

Thus, while the value of the unit of one currency in terms of another currency is determined at any particular time by the market conditions of demand and supply, in the long run the exchange rate is determined by the relative values of the two currencies as indicated by their respective purchasing powers over goods and services.

In other words, the rate of exchange tends to rest at the point which expresses equality between the respective purchasing powers of the two currencies. This point is called the purchasing power parity. Thus, under a system of autonomous paper standards the external value of a currency is said to depend ultimately on the domestic purchasing power of that currency relative to that of another currency. In other words, exchange rates, under such a system, tend to be determined by the relative purchasing power parities of different currencies in different countries.

In the above example, if prices in India get doubled, prices in the USA remaining the same, the value of the rupee will be exactly halved. The new parity will be $ 1 = 120 rupees. This is because now 120 rupees will buy the same collection of commodities in India which 60 rupees did before. We suppose that prices in the USA remain as before. But if prices in both countries get doubled, there will be no change in the parity.

In actual practice, however, the parity will be modified by the cost of transporting goods (including duties etc.) from one country to another.

References:

1. Dr.D.M.Mithani – International Economics (Himalaya Publishing house ltd)

2. Bo Sodersten, Geoffirey Reed, International Economics (3rd Edition) Publisher Red Globe Press

3. Z.M.Jhingan : International Economics (Vrinda Publication)

4. Robert Feenstra, Alan M Taylor, International Trade (5th Edition) Publisher Worth

5. Dr.Mrs.NirmalBhalerao&S.S.M.Desai – International Economics (Himalaya Publishing house ltd)