UNIT II

Direction

Directing is one of the most important functions of management. The plans may be the best feasible ones; the activities may be systematically organized, the staff may be highly efficient, but the organization will not succeed if there is no proper direction.

Direction involves not only instructing people what to do, but also ensuring that they know what is expected of them. The manager should help, motivate and guide his subordinates to improve their skills. Most of all, directing involves development of high morale in the subordinates.

IMPORTANT FEATURES/CHARACTERISTICS OF DIRECTION

1. Directing Initiates Action:

Other functions prepare a base or setting of action, i. e., how action has to be carried on the directing initiate or start action.

By giving directions or instructions the managers get the work started in the organisation.

2. Continuing Function:

Directing is a continuous process. A manager cannot just rest after issuing orders and instructions. He has to continuously guide, supervise and motivate his subordinates. He must continuously take steps to make sure that orders and instructions are carried out properly.

3. Directing takes place at every level:

Directing is a pervasive function as it is performed by managers at all levels and in all locations. Every manager has to supervise, guide, motivate and communicate with his subordinate to get things done. However, the time spent in directing is comparatively more at operational level of management. Directing takes place wherever superior subordinate relation exists.

4. Directing flows From Top to Bottom:

Directions are given by managers to their subordinates. Every manager can direct his immediate subordinate and take directions from immediate boss. Directing starts from top level and flows to lower level.

5. Performance Oriented:

Directing is a performance oriented function. The main motive of directing is bringing efficiency in performance. Directing converts plans into performance. Performance is the essence of directing. Directing functions direct the performance of individuals towards achievement of organisational goal.

6. Human Element:

Directing function involves study and molding of human behaviour. It improves interpersonal and intergroup relationship. It motivates employees to work with their best ability.

IMPORTANCE OF DIRECTING:

1) Facilitates innovation: Proper directions facilitate innovation in the Organization. Due to effective directions, employees may be motivated to come up with innovative ideas, plans and policies.

2) Corporate image: Proper directions help to improve corporate image. Due to effective directions, there can be better performance of the employees. The better performance of the employees can help to develop goodwill in the market.

3) Team work: Directing develops team spirit in the Organization. It is the team work that brings success to the Organization. Due to effective directions of the superior, the subordinates work as a team.

4) Optimum use of resources: Directing facilitates optimum use of resources. Through effective directions, the manager can make optimum use of resources such as:

5) Motivation: Directing facilitates motivation of employees in the Organization. The manager can motivate the subordinates to perform effectively through effective communication and leading. The manager may enhance the motivational level of the subordinates by providing them monetary and non-monetary incentives.

6) Reduce absenteeism: Proper directing helps to reduce absenteeism. For e.g. if a lecturer gives proper directions to the students, then the absenteeism on the part of the students may be reduced considerably.

7) Reduction in wastages: Effective directions help to reduce wastages of resources. The subordinates would make every possible effort to minimize or avoid wastages of resources, wherever possible.

8) Higher efficiency: Proper directing can facilitate higher efficiency in the Organization. Efficiency is the ratio of returns to cost. Due to effective directions, there can be higher returns at reduced costs.

9) Initiates Action: Directing function is a point from where the action starts, subordinates understand their jobs and do according to the instructions given. Whatever plans are made can be implanted only when the actual work starts, the direction becomes beneficial.

PRINCIPLES OF EFFECTIVE DIRECTION:

Effective direction results in greater contribution of subordinates to organization goals. The directing functions of management are often effective only certain well accepted principles are followed.

The following are the essential principles of effective direction:

1. Harmony of Objectives:

It is a vital function of management to make the people realize the objectives of the group and direct their efforts towards the achievement of their objectives. The interest of the group should prevail over individual interest. The principle implies harmony of personal interest and common interest. Effective direction fosters the sense of belongingness among all subordinates in such how that they always identify themselves with the enterprise and tune their goals with those of the enterprise.

2. Unity of Command:

This principle states that one person should receive orders from just one superior, in other words, one person should be accountable to just one boss. If one person is under quite one boss then there can be contradictory orders and the subordinate fails to understand whose order to be followed. In the absence of unity of command, the authority is undermined, discipline weakened, loyalty divided and confusion and delays are caused.

3. Unity of Direction:

To have effective direction, there should be one head and one plan for a group of activities having similar objectives. In other words, each group of activities having the same objectives must have one plan of action and must be under the control of 1 supervisor.

4. Direct Supervision:

The directing function of management becomes more effective if the superior maintains direct personal contact with his subordinates. Direct supervision infuses a way of participation among subordinates that encourages them to place in their best to realize the organizational goals and develop an efficient system of feed-back of information.

5. Participative or Democratic Management:

The function of directing becomes more effective if participative or democratic type of management is followed. According to this principle, the superior must act consistent with the mutual consent and the decisions reached after consulting the subordinates. It provides necessary motivation to the workers by ensuring their participation and acceptance of work methods.

6. Effective Communication:

To have effective direction, it's very essential to have an effective communication system which provides for free flow of ideas, information, suggestions, complaints and grievances.

7. Follow-up:

In order to make direction effective, a manager has got to continuously direct, guide, motivate and lead his subordinates. A manager has not only to issue orders and directions but also to follow-up the performance so on ensure that work is being performed as desired. He should intelligently oversee his subordinates at work and proper them whenever they go wrong.

LIMITATIONS OF DIRECTING

ELEMENTS OF DIRECTION:

Directing is a vital function of management. It’s rightly called the heart of management process as it is concerned with initiating action. It consists of all those activities which are concerned with influencing, guiding or supervising the subordinates in their job.

The main aspects or elements of direction are as follows:

1. Issuing Orders and Instructions;

2. Leadership;

3. Communication;

4. Motivation;

5. Supervision; and

6. Co-ordination.

1. Issuing Orders and Instructions:

A manager is required to issue variety of orders to his subordinates to initiate, modify or halt any action. He’s also required to guide and instruct workers in performance of their task towards the achievement of desired goals. Instructions are important in directing subordinates. Orders and instructions reflect the decisions of managers.

A good order or instruction should have the subsequent characteristics:

(a) It should be simple, unambiguous and clear.

(b) It should be brief but complete.

(c) It should be reasonable and enforceable.

(d) It should be convincing and acceptable.

(e) It should invoke co-operation.

(f) It should be compatible with the objectives of the organization.

(g) It should “be in written form as far as possible.

(h) It should be protected by follow-up action.

2. Leadership:

Leadership is “the process by which an executive or manager imaginatively directs/guides and influences the work of others in choosing and attaining specified goals by mediating between the individual and organization in such a manner that both will get maximum satisfaction.” it's the ability to build up confidence and zeal among people and to create an urge in them to be led. To be a successful leader a manager must process the qualities of foresight, drive, initiative, self-confidence and private integrity. Different situations may demand differing types of leadership viz., autocratic leadership, democratic leadership and free-rein leadership.

Elements of Direction —the Management in Action:

3. Communication:

Communication constitutes a really important element of directing. It’s said to be the amount one problem of management today. Communication is that the means by which the behaviour of the subordinates is modified and alters is affected in their action.

The word communication has been derived from the Latin word ‘Communis’ which suggests ‘common’. Thus, communication means sharing of ideas in common. The essence of communication is getting the receiver and therefore the sender tuned together for a specific message. Communication refers to the exchange of ideas, feelings, emotions, knowledge and information between two or more persons.

In management ideas, objectives, orders, appeals, observations, instructions, suggestions etc. need to be exchanged among the managerial personnel and their subordinates operating at different levels of the organization for the purpose of planning and executing the business policies. Directing will mainly depend on the effectiveness of communication. In case the orders and instructions aren't properly conveyed then these might not be properly implemented.

4. Motivation:

It is a vital element of directing function. Motivation encourages persons to offer their best performance and help in reaching enterprise goals. It’s the degree of readiness for undertaking assigned task and doing it in the best possible way. Directing function tries to make best use of varied factors of production available within the organization. This will be achieved only employees co-operate during this task. Efforts should be made to form employees contribute their maximum.

5. Supervision:

It consists of the process and technique involved in issuing instructions and confirming that operations are carried as originally planned. Supervision may be a continuing activity and performed at every level of activity. It’s inevitable at every level of management for putting the managerial plans and policies into action. During a way supervision is a kind of control as the supervisor is meant to take corrective measures if the work isn't in line with the plan.

6. Co-ordination:

Co-ordination is an orderly arrangement of group effort to provide unity of action in pursuit of common purpose. The aim of directing is to get various activities coordinated for achieving common goals. Co-ordination involves the integration of varied parts of the organization. So as to attain goals of an enterprise, both physical also as mental co-ordination should be secured. Co-ordination is a part of directing exercise and helps in synchronization of varied efforts.

Coordination is the function of management which ensures that different departments and groups work in sync. Therefore, there is unity of action among the employees, groups, and departments.

It also brings harmony in carrying out the different tasks and activities to achieve the organization’s objectives efficiently. Coordination is an important aspect of any group effort. When an individual is working, there is no need for coordination.

Therefore, we can say that the coordination function is an orderly arrangement of efforts providing unity of action in pursuance of a common goal. In an organization, all the departments must operate a part of a cohesive unit to optimize performance.

Coordination implies synchronization of various efforts of different departments to reduce conflict. Multiple departments usually perform the work for which an organization exists.

Therefore, synchronization between them is essential. Lacking coordination, departments might work in different directions or at different timings, creating chaos.

Features of coordination

Coordination is the integration, unification, synchronization of the efforts of the departments to provide unity of action for pursuing common goals. A force that binds all the other functions of management.

The management of an organization endeavors to achieve optimum coordination through its basic functions of planning, organizing, staffing, directing, and controlling.

Therefore, coordination is not a separate function of management because management is successful only if it can achieve harmony between different employees and departments. Here are some important features of coordination:

Limitations of Coordination

Key Takeaways

In an organization, the efficient coordination of internal and external components help in reducing the complexities (both internal and external). Therefore, the organization experiences an increase in productivity, easier integration of micro and macro level organizational dynamics, a better connection of roles among intra-organizational and inter-organizational groups as well as building trust among competing groups, and defining organizational tasks. Coordination is primarily of two types – internal coordination and external coordination as described below.

Internal Coordination

Internal coordination is all about establishing a relationship between all the managers, executives, departments, divisions, branches, and employees or workers. These relationships are established with a view to coordinate the activities of the organization. Internal coordination has two groups:

Vertical coordination – In vertical coordination, a superior authority coordinates his work with that of his subordinates and vice versa. For example, a sales manager will coordinate his tasks with his sales supervisors. On the other hand, all sales supervisors ensure that they work in sync with the sales manager.

Horizontal coordination – In horizontal coordination, employees of the same status establish a relationship between them for better performance. For example, the coordination between department heads, or supervisors, or co-workers, etc.

In other words, in internal coordination, an employee either reports vertically to the supervisor and/or the subordinates and horizontally to the colleagues and/or co-workers.

External Coordination

As the name suggests, external coordination is all about establishing a relationship between the employees of the organization and people outside it.

These relationships are established with a view to having a better understanding of outsiders like market agencies, public, competitors, customers, government agencies, financial institutions, etc.

Usually, organizations entrust a Public Relations Officer (PRO) with the responsibility of establishing cordial relationships between the employees of the organization and outsiders.

Control is a primary goal-oriented function of management in an organisation. It is a process of comparing the actual performance with the set standards of the company to ensure that activities are performed according to the plans and if not then taking corrective action.

Every manager needs to monitor and evaluate the activities of his subordinates. It helps in taking corrective actions by the manager in the given timeline to avoid contingency or company’s loss.

Controlling is performed at the lower, middle and upper levels of the management.

Features of Controlling

Controlling and planning are interrelated for controlling gives an important input into the next planning cycle. Controlling is a backwards-looking function which brings the management cycle back to the planning function. Planning is a forward-looking process as it deals with the forecasts about the future conditions.

Importance of Control:

The control function helps management in various ways. It guides the ‘management in achieving pre-determined goals. The efficiency of various functions is also ensured by the control process. The shortcomings in various fields are also reported for taking corrective measures.

1. Basis for Future Action:

Control provides basis for future action. The continuous flow of information about projects keeps the long range planning on the right track. It helps in taking corrective action in future if the performance is not up to the mark. It also enables management to avoid repetition of past mistakes.

2. Facilitates Decision-making:

Whenever there is deviation between standard and actual performance the controls will help in deciding the future course of action. A decision about follow up action is also facilitated.

3. Facilitates Decentralization:

Decentralization of authority is necessary in big enterprise. The management cannot delegate authority without ensuring proper controls. The targets or goals of various departments are used as a control technique. If the work is going on satisfactorily then top management should not worry. The ‘management by exception’ enables top management to concentrate on policy formulation. Various control techniques like budgeting, cost control, pre action approvals allow decentralization without losing control over activities.

4. Facilitates Co-ordination:

Control helps in coordination of activities through unity of action. Every manager will try to co-ordinate the activities of his subordinates in order to achieve departmental goals. Similarly, chief executive will co-ordinate the functioning of various departments. The controls will act as checks on the performance and proper results will be achieved only when activities are coordinated.

5. Helps in Improving Efficiency:

The control system helps in improving organizational efficiency. Various control devices act as motivators to managers. The performance of every person is regularly monitored and any deficiency is corrected at the earliest.

6. Psychological Pressure:

Controls put psychological pressure on persons in the organization. Everybody knows that his performance is regularly evaluated and he will try to improve upon his previous work. The rewards and punishments are also linked with performance. The employees will always be under pressure to improve upon their work. Since performance measurement is one of the important tools of control it ensures that every person tries to maximize his contribution.

Limitations of Control:

Though control is essential for better performance and maintenance of good standards, there are certain limitations also.

Some of the limitations are discussed as such:

1. Influence of External Factors:

There may be an effective control system but external factors which are not in the ambit of management may have adverse effect on the working. These factors may be government policy, technological changes, change in fashion, etc. The influence of these factors cannot be checked by the control system in the organization.

2. Expensive:

The control system involves huge expenditure on its exercise. The performance of each and every person in the organization will have to be measured and reported to higher authorities. This requires a number of persons to be employed for this purpose. If the performance cannot be quantitatively measured then it will be observed by the superiors. The exercise of control requires both time and effort.

3. Lack of Satisfactory Standards:

The performance of certain activities involving human behaviour cannot be fixed in terms of quantities. It is difficult to fix standards for activities like public relations, management development, human relations, research, etc. The evaluation of work of persons engaged in these activities will be difficult.

4. Opposition from Subordinates:

The effectiveness of control process will depend upon its acceptability by subordinates. Since control interferes with the individual actions and thinking of subordinates they will oppose it. It may also increase the pressure of work on subordinates because their performance is regularly monitored and evaluated. These factors are responsible for the opposition of controls by subordinates.

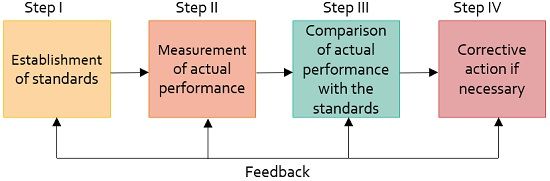

Process of Controlling

Control process involves the following steps as shown in the figure:

|

Key Takeaways

A good control system must be simple and easily understandable so that all the managers can apply it effectively. Complicated control techniques fail to communicate the meaning of control data to the managers.

2. Objectivity:

The standards of performance should be objective and specific, quantified and verifiable. They should be based on the facts so that control is acceptable and workable.

3. Promptness:

The control system should provide information soon enough so that the managers can detect and report the deviations promptly and necessary corrective actions may be taken in proper time. Corrective measures are of no value if those are taken too late.

4. Economy:

The control system must justify the expenses involved. In other words, anticipated earnings from it should be greater than the expected costs in its working. A small organisation cannot use the expensive control technique applied in large enterprises.

5. Flexibility:

Internal goals and strategies must be responsive to the changes in the environment and the control system should be flexible enough to adapt the changing conditions or unforeseen situations. It should be adaptable to the new developments. Flexibility in control system can be introduced by making alternative plans.

6. Accuracy:

The control system should encourage accurate information in order to detect deviations. The technique of control used should be appropriate to the work being controlled.

7. Suitability:

Control must reflect the needs and nature of the activities of the organisation, the control system should focus on achieving the organisational goals.

8. Forward-looking Nature:

The control system must be directed towards the future. It must pay attention on how the future actions can be conformed with the plans adopted.

9. Focus on Strategic Points:

The control system should focus attention on strategic or critical deviations. Only exceptional deviations require the attention of the managers.

10. Motivating:

A good control system should pay due attention to the human factor, It should be designed to secure positive action from the workers. Self-control tends to be motivated. Direct contact between the controller and the controlled also helps in making the control system motivational.

Key Takeaways

Control is a fundamental managerial function. Managerial control regulates the organizational activities. It compares the actual performance and expected organizational standards and goals. For deviation in performance between the actual and expected performance, it ensures that necessary corrective action is taken.

There are various techniques of managerial control which can be classified into two broad categories namely-

Traditional Techniques of Managerial Control

Traditional techniques are those which have been used by the companies for a long time now. These include:

1. Personal Observation:

This is the most traditional method of control. Personal observation is one of those techniques which enables the manager to collect the information as first-hand information.

It also creates a phenomenon of psychological pressure on the employees to perform in such a manner so as to achieve well their objectives as they are aware that they are being observed personally on their job. However, it is a very time-consuming exercise & cannot effectively be used for all kinds of jobs.

2. Statistical Reports:

Statistical reports can be defined as an overall analysis of reports and data which is used in the form of averages, percentage, ratios, correlation, etc., present useful information to the managers regarding the performance of the organization in various areas.

This type of useful information when presented in the various forms like charts, graphs, tables, etc., enables the managers to read them more easily & allow a comparison to be made with performance in previous periods & also with the benchmarks.

3. Break-even Analysis:

Breakeven analysis is a technique used by managers to study the relationship between costs, volume & profits. It determines the overall picture of probable profit & losses at different levels of activity while analyzing the overall position.

The sales volume at which there is no profit, no loss is known as the breakeven point. There is no profit or no loss. Breakeven point can be calculated with the help of the following formula:

Breakeven point = Fixed Costs/Selling price per unit – variable costs per unit

4. Budgetary Control:

Budgetary control can be defined as such technique of managerial control in which all operations which are necessary to be performed are executed in such a manner so as to perform and plan in advance in the form of budgets & actual results are compared with budgetary standards.

Therefore, the budget can be defined as a quantitative statement prepared for a definite future period of time for the purpose of obtaining a given objective. It is also a statement which reflects the policy of that particular period. The common types of budgets used by an organization.

Some of the types of budgets prepared by an organisation are as follows,

Modern Techniques of Managerial Control

Modern techniques of controlling are those which are of recent origin & are comparatively new in management literature. These techniques provide a refreshingly new thinking on the ways in which various aspects of an organization can be controlled. These include:

1. Return on Investment

Return on investment (ROI) can be defined as one of the important and useful techniques. It provides the basics and guides for measuring whether or not invested capital has been used effectively for generating a reasonable amount of return. ROI can be used to measure the overall performance of an organization or of its individual departments or divisions. It can be calculated as under-

Net income before or after tax may be used for making comparisons. Total investment includes both working as well as fixed capital invested in the business.

2. Ratio Analysis

The most commonly used ratios used by organizations can be classified into the following categories:

3. Responsibility Accounting

Responsibility accounting can be defined as a system of accounting in which overall involvement of different sections, divisions & departments of an organization are set up as ‘Responsibility centers’. The head of the center is responsible for achieving the target set for his center. Responsibility centers may be of the following types:

4. Management Audit

Management audit refers to a systematic appraisal of the overall performance of the management of an organization. The purpose is to review the efficiency &n effectiveness of management & to improve its performance in future periods.

5. PERT & CPM

PERT (programmed evaluation & review technique) & CPM (critical path method) are important network techniques useful in planning & controlling. These techniques, therefore, help in performing various functions of management like planning; scheduling & implementing time-bound projects involving the performance of a variety of complex, diverse & interrelated activities.

Therefore, these techniques are so interrelated and deal with such factors as time scheduling & resources allocation for these activities.

Planning and controlling are inter-related to each other. Planning sets the goals for the organization and controlling ensures their accomplishment. Planning decides the control process and controlling provides sound basis for planning. In reality planning and controlling are both dependent on each other. In the words of M.C. Niles, “Control is an aspect and projection of planning, where as planning sets the course, control observes deviations from the course, and initiates action to return to the chosen course or to an appropriately changed one.”

The relationship between planning and control can be explained as follows:

1. Planning Originates Controlling:

In planning the objectives or targets are set in order to achieve these targets control process is needed. So planning precedes control.

2. Controlling Sustains Planning:

Controlling directs the course of planning. Controlling spots the areas where planning is required.

3. Controlling Provides Information for Planning:

In controlling the actual performance is compared to the standards set and records the deviations, if any. The information collected for exercising control is used for planning also.

4. Planning and Controlling are Interrelated:

Planning is the first function of management. The other functions like organizing, staffing, directing etc. are organized for implementing plans. Control records the actual performance and compares it with standards set. In case the performance is less than that of standards set then deviations are ascertained. Proper corrective measures are taken to improve the performance in future. Planning is the first function and control is the last one. Both are dependent upon each other.

5. Planning and Control are Forward Looking:

Planning and control are concerned with the future activities of the business. Planning is always for future and control is also forward looking. No one can control the past, it is the future which can be controlled. Planning and controlling are concerned with the achievement of business goals. Their combined efforts are to reach maximum output with minimum of cost. Both systematic planning and organized controls are essential to achieve the organizational goals.

References-