Unit - 5

Working capital

Working capital is the part of total capital. It is used for carrying out regular business operations. In other words, it is the amount of funds used for financing the day-to-day operations or activities.

The funds invested in current assets such as stock of materials, work-in- progress, investments, bills receivables, sundry debtors, bank balance, etc., are known as working capital or short term capital.

The success of any organization depends upon the efficient management of working capital.

There are two concepts of working capital viz. Quantitative and qualitative. Some people also define the two concepts as gross concept and net concept.

According to quantitative concept, the amount of working capital refers to ‘total of current assets’. Current assets are considered to be gross working capital in this concept.

The qualitative concept gives an idea regarding source of financing capital. According to qualitative concept the amount of working capital refers to “excess of current assets over current liabilities.

Definition

“Working Capital is the excess of C.A. Over current liabilities.”

According to Shubin, “working capital is the amount of funds necessary to cover the cost of operating the enterprise. Working capital in a going concern is a revolving fund, it consists of cash receipts from sales which are used to cover the cost of current operations”.

There are two concepts of working capital viz. Quantitative and qualitative. Some people also define the two concepts as gross concept and net concept.

According to quantitative concept, the amount of working capital refers to ‘total of current assets’. Current assets are considered to be gross working capital in this concept.

The qualitative concept gives an idea regarding source of financing capital. According to qualitative concept the amount of working capital refers to “excess of current assets over current liabilities.

Types of working capital

According to the needs of business, the working capital may be classified into following two basis:

1) On the basis of periodicity

2) On the basis of concept

On the basis of periodicity:

The requirements of working capital are continuous. More working capital is required in a particular season or the peck period of business activity. On the basis of periodicity working capital can be divided under two categories as under:

1. Permanent working capital

2. Variable working capital

(a) Permanent working capital: This type of working capital is known as Fixed Working Capital. Permanent working capital means the part of working capital which is permanently locked up in the current assets to carry out the business smoothly. The minimum amount of current assets which is required to conduct the business smoothly during the year is called permanent working capital.

For example, investments required to maintain the minimum stock of raw materials or to cash balance. The amount of permanent working capital depends upon the size and growth of company. Fixed working capital can further be divided into two categories as under:

1. Regular Working capital:

Minimum amount of working capital required to keep the primary circulation. Some amount of cash is necessary for the payment of wages, salaries etc.

2. Reserve Margin Working capital:

Additional working capital may also be required for contingencies that may arise any time. The reserve working capital is the excess of capital over the needs of the regular working capital is kept aside as reserve for contingencies, such as strike, business depression etc.

(b) Variable or Temporary Working Capital:

The term variable working capital refers that the level of working capital is temporary and fluctuating. Variable working capital may change from one asset to another and changes with the increase or decrease in the volume of business.

The variable working capital may also be subdivided into following two sub-groups.

1. Seasonal Variable Working capital:

Seasonal working capital is the additional amount which is required during the active business seasons of the year. Raw materials like raw-cotton or jute or sugarcane are purchased in particular season. The industry has to borrow funds for short period. It is particularly suited to a business of a seasonal nature. In short, seasonal working capital is required to meet the seasonal liquidity of the business.

2. Special variable working capital:

Additional working capital may also be needed to provide additional current assets to meet the unexpected events or special operations such as extensive marketing campaigns or carrying of special job etc.

On the basis of concept:

On the basis of concept working capital is divided into two categories as under:

(A) Gross Working Capital:

Gross working capital refers to total investment in current assets. The current assets employed in business give the idea about the utilization of working capital and idea about the economic position of the company. Gross working capital concepts is popular and acceptable concept in the field of finance.

(B) Net Working Capital:

Net working capital means current assets minus current liabilities. The difference between current assets and current liabilities is called the net working capital. If the net working capital is positive, business is able to meet its current liabilities. Net working capital concept provides the measurement for determining the creditworthiness of company.

Components of working capital

There are two components of working capital, viz., Current Assets and Current Liabilities.

- Current Assets: Current assets are those assets which can be converted into cash in the normal course of business within a short period-say a maximum of one year. They are also called floating or circulating assets because they cannot be put to constant use. They are meant for resale or produced for the purpose of sale i.e., converting them into cash. In brief, the list of current assets comprises of:

- Cash in hand and bank balances, 2. Bills Receivables, 3. Sundry Debtors (less provision for bad debts), 4. Short-term loans and advances, 5. Inventories of stocks, as: (a) Raw material, (b) Work-in-process, (c) Stores and spares, (d) Finished goods, 6. Temporary Investments of surplus funds, 7. Prepaid Expenses. 8. Accrued Incomes.

- Current Liabilities: Current liabilities are those liabilities which are intended to be paid in the ordinary course of business within a short period of normally one accounting year out of the current assets or the income of the business. Examples of current liabilities are: Bills Payable, Sundry Creditors or Accounts Payable, 3. Accrued or Outstanding Expenses, 4. Short-term loans, advances and deposits, 5. Dividends Payable, 6. Bank Overdraft, 7. Provision for taxation.

Key takeaways

Working capital is the part of total capital. It is used for carrying out regular business operations

A company’s operating cycle usually consists of three primary actions; purchasing resources, producing the product, and selling the product. These actions create funds flows that are both unsynchronized since cash disbursements typically take place before cash proceeds.

Example: Payments for store purchases takes place before the collection of receivables. They are unsure because prospect sales and costs, which produce the particular receipts and disbursements, cannot be forecasted with total exactness. If the firm is to uphold a cash balance to pay the bills as they come outstanding. In addition, the corporation must invest in inventories to fill customer orders punctually. And, finally, the company invests in accounts receivable to extend credit to its consumers.

Operating cycle = Inventory alteration period + Receivables alteration period

The inventory conversion period is the extent of time required to manufacture and sell the product

It is defined as under:

Standard inventory

Inventory change period =Cost of sales/365

The payables delay period is the length of time the firm is able to reschedule payment on its various resource purchases. Equation is used to calculate the payables delay period:

Accounts due + Salaries, benefits, and Payroll taxes due

Payables delay period = (Cost of sales + Selling, general and executive expense) /365

Finally, the cash exchange cycle represents the net time gap between the collections of cash proceeds from product sales and the cash payments for the company’s different resource purchases.

It is calculated as follows: Cash conversion cycle = Operating cycle – Payable delay period

The following factor determine the amount of working capital

- Nature of Companies: The composition of an asset is a function of the size of a business and the companies to which it belongs. Small companies have smaller proportions of cash, receivables and inventory than large corporation. This difference becomes more marked in large corporations. A public utility, for example, mostly employs fixed assets in its operations, while a merchandising department depends generally on inventory and receivable. Needs for working capital are thus determined by the nature of an enterprise.

- Demand of Creditors: Creditors are interested in the security of loans. They want their obligations to be sufficiently covered. They want the amount of security in assets which are greater than the liability.

- Cash Requirements: Cash is one of the current assets which are essential for the successful operations of the production cycle. A minimum level of cash is always required to keep the operations going. Adequate cash is also required to maintain good credit relation.

- Nature and Size of Business: The working capital requirements of a firm are basically influenced by the nature of its business. Trading and financial firms have a very less investment in fixed assets, but require a large sum of money to be invested in working capital. Retail stores, for example, must carry large stocks of a variety of goods to satisfy the varied and continues demand of their customers. Some manufacturing business, such as tobacco manufacturing and construction firms also have to invest substantially in working capital and a nominal amount in the fixed assets.

- Time: The level of working capital depends upon the time required to manufacturing goods. If the time is longer, the size of working capital is great. Moreover, the amount of working capital depends upon inventory turnover and the unit cost of the goods that are sold. The greater this cost, the bigger is the amount of working capital.

- Volume of Sales: This is the most important factor affecting the size and components of working capital. A firm maintains current assets because they are needed to support the operational activities which result in sales. They volume of sales and the size of the working capital are directly related to each other. As the volume of sales increase, there is an increase in the investment of working capital-in the cost of operations, in inventories and receivables.

- Terms of Purchases and Sales: If the credit terms of purchases are more favourable and those of sales liberal, less cash will be invested in inventory. With more favourable credit terms, working capital requirements can be reduced. A firm gets more time for payment to creditors or suppliers. A firm which enjoys greater credit with banks needs less working capital.

- Business Cycle: Business expands during periods of prosperity and declines during the period of depression. Consequently, more working capital required during periods of prosperity and less during the periods of depression.

- Production Cycle: The time taken to convert raw materials into finished products is referred to as the production cycle or operating cycle. The longer the production cycle, the greater is the requirements of the working capital. An utmost care should be taken to shorten the period of the production cycle in order to minimize working capital requirements.

- Liquidity and Profitability: If a firm desires to take a greater risk for bigger gains or losses, it reduces the size of its working capital in relation to its sales. If it is interested in improving its liquidity, it increases the level of its working capital. However, this policy is likely to result in a reduction of the sales volume, and therefore, of profitability. A firm, therefore, should choose between liquidity and profitability and decide about its working capital requirements accordingly.

- Seasonal Fluctuations: Seasonal fluctuations in sales affect the level of variable working capital. Often, the demand for products may be of a seasonal nature. Yet inventories have got to be purchased during certain seasons only. The size of the working capital in one period may, therefore, be bigger than that in another.

Working capital management

The term ‘working capital management’ primarily refers to the efforts of the management towards effective management of current assets and current liabilities. Working capital is nothing but the difference between the current assets and current liabilities. In other words, an efficient working capital management means ensuring sufficient liquidity in the business to be able to satisfy short-term expenses and debts.

Concept of Working Capital:

1. Balance Sheet Concept

2. Operating Cycle Concept

Balance Sheet Concept

It is represented by the excess of current assets over current liabilities and is the amount normally available to finance current operations.

Under Balance Sheet Concept working capital may be described as

(a). Gross Concept [Total Current asset]

(b). Net Concept [Total Current asset- Total current liabilities]

Operating cycle concept

A company’s operating cycle typically consists of three primary activities; purchasing resources, producing the product, and distributing (selling) the product. These activities create funds flows and cash disbursements usually take place before cash receipts.

Estimation of working capital

Two components of capital are current assets and current liabilities. Estimation of the amount of current and current liabilities to maintain a certain level of operation is not an easy task. The lack of working capital disrupts the smooth production process, and excess working capital increases costs. Here we describe the estimation of working capital in case of trading and manufacturing concerns.

The following procedure should be employed to estimate working capital for manufacturing concerns:

(a) Expected production per week or per month.

(b) Determination of costs for each element, namely material, labour and overhead, as well as profit per unit;

(c) Calculation of the amount blocked for each week/month for each element of cost and profit;

(d) Determination of the operating cycle by estimating the raw material retention period. Processing time, storage period of finished products, debt collection period. The period of payment of creditor it takes time lag in pay and overhead payments.

(e) Determining the net block period. This is the period during which each element of the cost remains blocked. For example, if the raw material remains in the store for 2 weeks after purchase, the processing time is 2 weeks, the finished product remains in stock, 3 weeks if the credit period extended to the debtor is extended for 4 weeks, and the payment for the material is made for 2 weeks after purchase, the net block period is as follows: [(2+ 2 + 3 + 4) – (2)] = 9 a few weeks.

(f) Obtain the working capital requirements for each element of the cost by multiplying the net block period calculated in step (e) and the amount blocked for each element of the cost according to step (c).

(g) Get the total amount of working capital, if any, by summing up the costs and all the amounts calculated for each element of the desired cash.

Key takeaways

Estimation of the amount of current and current liabilities to maintain a certain level of operation is not an easy task. The lack of working capital disrupts the smooth production process, and excess working capital increases costs. Here we describe the estimation of working capital in case of trading and manufacturing concerns.

Working Capital Management (WCM) is the management of short-term financial requirements of an organization. This includes maintaining the optimal balance of working capital components such as receivables, inventory and payables and using the cash efficiently for day-to-day operations. Long term funds are required to create production facilities through the purchase of fixed assets such as plant & machinery, solid background, building, furniture, etc. Investments in these assets represent that piece of a firm’s capital which is blanked out on permanent or fixed earth and is called fixed capital. Funds are also needed for short-term purposes for the purchase of crude material, payment of wages and other expenses. It is also known as revolving or circulating capital or short-term capital. Efficient working capital management increases firms’ free cash flow, which in turn increases the firms’ growth opportunities and turn back to shareholders. Even though firms traditionally are focused on long term capital budgeting and capital structure, the recent trend is that many companies across different industries focus on working capital management efficiency.

The management of working capital by managing the proportions of the working capital management components is important to the financial health of businesses from all industries. To reduce accounts receivable, a firm may have strict collections policies and limited sales credits to its customers. This would increase cash inflow. However, the strict collection policies and lesser sales credits would lead to lost sales thus reducing the profits. Maximizing account payables by having longer credits from the suppliers also has the opportunity of taking poor quality fabrics from a provider that would finally bear on the profitability.

Construction is an essential part of any country’s infrastructure and industrial development. The Indian construction sector is an inbuilt component of the economic system and a conduit for a significant portion of India’s development investment. Forecasting working capital along with cash requirements is essential for all construction contractors during the tendering stage since cash flow at the beginning of the project is a major cause of construction companies’ failure. In the contracting business, construction firms are generally more concerned with short-term financial strategies than longer-term ones. Working capital management is the central issue of all short-term financial concerns. Every business needs adequate liquid resources in order to maintain day to day cash flows.

A Contractor needs enough cash to by wages and salaries as they fall due and to pay creditors if it is to keep its workforce and ensure its supplies. Sufficient liquidity must be preserved in order to ensure the survival of business in the long term as well. Even a profitable business may fail if it does not have adequate cash flows to meet its liabilities as they fall due. Therefore, when a business makes an investment decision, they must not only consider the financial outlay involved with acquiring the new machine or the new building, etc. but must also take account of the additional current assets that are usually involved with any expansion of activity.

In the working capital analysis, the direction of change over a period of time is of crucial importance. Not only that, analysis of working capital trends provides a base to judge whether the practice and prevailing policy of the management with regard to working capital is good enough or improvement is to be made in managing the working capital funds.

Inventory management techniques

Inventory constitutes an important item in the working capital of many business concerns. Net working capital is the difference between current assets and current liabilities. Inventory is a major item of current assets. The term inventory refers to the stocks of the product a firm is offering for sale and the components that make up the product. Inventory is stores of goods and stocks. This includes raw materials, work-in-process and finished goods. Raw materials consist of those units or input which are used to manufacture goods that require further processing to become finished goods. Finished goods are products ready for sale. The classification of inventory and the levels of the components vary from organization to organization depending upon the nature of business. For example, steel is a finished product for a steel industry, but raw material for an automobile manufacturer. Thus, inventory may be defined as “Stock of goods that is held for future use”. Since inventory constitute about 50 to 60 percent of current assets, the management of inventories is crucial to successful Working Capital Management. Working capital requirements are influenced by inventory holding. Hence, there is a need for effective and efficient management of inventory A good inventory management is important to the successful operations of the most of the organizations, unfortunately the importance of inventory is not always appreciated by top management. This may be due to a failure to recognize the link between inventory and achievement of organizational goals or due to ignorance of the impact that inventory can have on costs and profits. Inventory management refers to an optimum investment in inventory. It should neither be too low to affect the production adversely nor too high to block the funds unnecessarily. Excess investment in inventory is unprofitable for the business. Both excess and inadequate investment in inventory is not desirable. The firm should operate within the two danger points. The purpose of inventory management is to determine and maintain the optimum level of inventory investment. Techniques and Tools of Inventory Control:

Figure: Techniques of inventory control

- Economic Order Quantity

The economic order quantity (EOQ) refers to the ideal order quantity a company should purchase in order to minimize its inventory costs, such as holding costs, shortage costs, and order costs. EOQ is necessarily used in inventory management, which is the oversight of the ordering, storing, and use of a company's inventory. Inventory management is tasked with calculating the number of units a company should add to its inventory with each batch order to reduce the total costs of its inventory.

Formula for EOQ

a = Annual consumption

b = Buying cost per order

c = Cost per unit

s = Storage cost (It include inventory carrying cost)

2. Fixing Levels of Material

(a) Minimum Level

This represents the quantity which must be maintained in hand at all times. If stocks are less than the minimum level, then the work will stop due to shortage of materials. Following factors are taken into account while deciding minimum stock level:

(i) Lead Time:

A purchasing firm requires some time to process the order and time is also required by the supplier/vendor to execute the order. The time taken in processing the order and then executing it is known as lead time. It is essential to maintain some inventory during this period to meet production requirements.

(ii) Rate of Consumption:

It is the average consumption of materials items in the industry. The rate of consumption will be decided on the basis of past experience and production plans.

(iii) Nature of Material:

The nature of material also affects the minimum level. If a material is required only against special orders of the customer, then minimum stock will not be required for such materials. Wheldon has given the following formula for calculating minimum stock level:

Minimum stock Level = Re-ordering Level – (Normal Consumption x Normal Reorder Period)

(iv) Re-ordering Level:

When the quantity of materials reaches a certain level then fresh order is sent to procure materials again. The order is sent before the materials reach minimum stock level.

(b) Maximum Level

It is the quantity of materials beyond which a firm should not exceed its stocks. If the quantity exceeds maximum level limit, then it will be termed as overstocking. A firm avoids overstocking because it will result in high material costs. Overstocking will lead to the requirement of more capital, more space for storing the materials, and more charges of losses from obsolescence. Maximum stock level will depend upon the following factors:

1. The availability of capital for the purchase of materials in the firm.

2. The maximum requirements of materials at any point of time.

3. The availability of space for storing the materials as inventory.

4. The rate of consumption of materials during lead time.

5. The cost of maintaining the stores.

6. The possibility of fluctuations in prices of various materials.

7. The nature of materials. If the materials are perishable in nature, then they cannot be stored for long periods.

8. Availability of materials. If the materials are available only during seasons, then they will have to be stored for the future period.

9. Restrictions imposed by the government. Sometimes, government fixes the maximum quantity of materials which a concern can store. The limit fixed by the government will become the deciding factor and maximum level cannot be fixed more than that limit.

10. The possibility of changes in fashions will also affect the maximum level.

It is calculated as-

Maximum Stock Level = Reordering Level + Reordering Quantity – (Minimum Consumption x Minimum Reordering period)

(c) Danger Level

It is the level below which stocks should not fall in any case. If danger level approaches, then immediate steps should be taken to replenish the stocks even if more cost is incurred in arranging the materials. Danger level can be determined with the following formula:

Danger Level = Average Consumption x Maximum reorder period for emergency purchases.

3. ABC Inventory Control

ABC method of inventory control involves a system that controls inventory and is used for materials and throughout the distribution management. It is also known as selective inventory control or SIC. ABC analysis is a method in which inventory is divided into three categories, i.e. A, B, and C in descending value. The items in the A category have the highest value, B category items are of lower value than A, and C category items have the lowest value.

Need for Prioritizing Inventory

Item A:

In the ABC model of inventory control, items categorized under A are goods that register the highest value in terms of annual consumption. It is interesting to note that the top 70 to 80 percent of the yearly consumption value of the company comes from only about 10 to 20 percent of the total inventory items. Hence, it is crucial to prioritize these items.

Item B:

These are items that have a medium consumption value. These amounts to about 30 percent of the total inventory in a company which accounts for about 15 to 20 percent of annual consumption value.

Item C:

The items placed in this category have the lowest consumption value and account for less than 5 percent of the annual consumption value that comes from about 50 percent of the total inventory items.

4. Perpetual Inventory System

A perpetual inventory system is an inventory management method that records when stock is sold or received in real-time through the use of an inventory management system that automates the process. A perpetual inventory system will record changes in inventory at the time of the transaction. A perpetual inventory system works by updating inventory counts continuously as goods are bought and sold. This inventory accounting method provides a more accurate and efficient way to account for inventory than a periodic inventory system. Here is a step-by-step overview of how this type of inventory system works.

5. VED classification.

VED analysis is an inventory management technique that classifies inventory based on its functional importance. It categorizes stock under three heads based on its importance and necessity for an organization for production or any of its other activities. VED analysis stands for Vital, Essential, and Desirable.

- V-Vital category

As the name suggests, the category “Vital” includes inventory, which is necessary for production or any other process in an organization. The shortage of items under this category can severely hamper or disrupt the proper functioning of operations. Hence, continuous checking, evaluation, and replenishment happen for such stocks. If any of such inventories are unavailable, the entire production chain may stop. Also, a missing essential component may be of need at the time of a breakdown. Therefore, order for such inventory should be before-hand. Proper checks should be put in place by the management to ensure the continuous availability of items under the “vital” category.

- E- Essential category

The essential category includes inventory, which is next to being vital. These, too, are very important for any organization because they may lead to a stoppage of production or hamper some other process. But the loss due to their unavailability may be temporary, or it might be possible to repair the stock item or part.

The management should ensure optimum availability and maintenance of inventory under the “Essential” category too. The unavailability of inventory under this category should not cause any stoppage or delays.

- D- Desirable category

The desirable category of inventory is the least important among the three, and their unavailability may result in minor stoppages in production or other processes. Moreover, the easy replenishment of such shortages is possible in a short duration of time.

6. Just-In-Time

Just in time is a form of inventory management that requires working closely with suppliers so that raw materials arrive as production is scheduled to begin, but no sooner. The goal is to have the minimum amount of inventory on hand to meet demand.

7. FSN Analysis

FSN stands for fast-moving, slow-moving and non-moving items. The basis of FSN analysis is to derive vital data to help guide inventory management decisions. These may include where products should be placed in the warehouse. For example, fast-moving items could be placed in a location that is easily accessible.

- Fast-moving inventory

Fast-moving inventory comprises of inventory, which moves in and out of stock fastest and most often. Therefore, these goods have the highest replenishment rate. Items in this category generally comprise less than 20% of the total inventory.

- Slow-moving inventory

Items in this category move slower, and hence, their replenishment is also slower. This category comprises of around 35% of the total inventory in an organization.

- Non- moving inventory

The last category of this analysis is the least moving portion of the inventory and also includes the dead stock. Replenishment of such inventory may or may not take place at all after utilization. This category can go as high as 55%-60% of the total inventory in organizations.

8. Inventory Turnover Ratio

Inventory turnover is a financial ratio showing how many times a company has sold and replaced inventory during a given period. A company can then divide the days in the period by the inventory turnover formula to calculate the days it takes to sell the inventory on hand. Calculating inventory turnover can help businesses make better decisions on pricing, manufacturing, marketing, and purchasing new inventory.

Key takeaways

The term inventory refers to the stocks of the product a firm is offering for sale and the components that make up the product.

Financing resources of working capital

Short-term financing is aimed to meet the demand of current assets and pay the current liabilities of the organization. In other words, it helps in minimizing the gap between current assets and current liabilities. There are different means to raise capital from the market for small duration. Various agencies, such as commercial banks, co-operative banks, financial institutions, and NABARD provide the financial assistance to organizations.

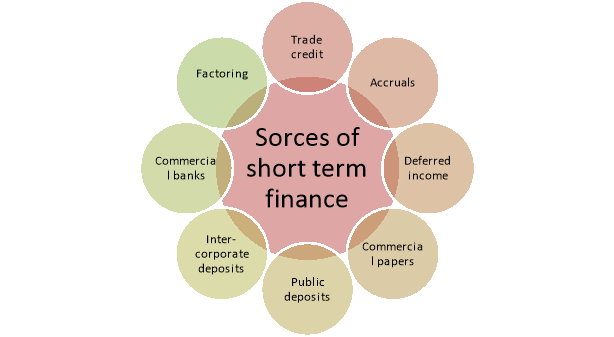

Figure: Sources of short term finance

1. Trade Credit:

Trade credit refers to the credit extended by the supplier of goods or services to his/her customer in the normal course of business. It occupies a very important position in short-term financing due to the competition. Almost all the traders and manufacturers are required to extend credit facility (a portion), without which there is no business. Trade credit is a spontaneous source of finance that arises in the normal business transactions without specific negotiation, (automatic source of finance).

2. Accruals:

Accrued expenses are those expenses which the company owes to the other, but not yet due and not yet paid the amount. Accruals represent a liability that a firm has to pay for the services or goods, it has received. It is spontaneous and interest-free source of financing. Salaries and wages, interest and taxes are the major constituents of accruals. Salaries and wages are usually paid on monthly and weekly base, respectively. The amounts of salaries and wages are owed but not yet paid and shown them as accrued salaries and wages on the balance sheet at the end of the financial year. The longer the time lag in–payment of these expenses, the greater is the amount of funds provided by the employees. Similarly, interest and tax are accruals, as source of short-term finance. Tax will be paid on earnings.

3. Deferred Income:

Deferred income is income received in advance by the firm for supply of goods or services in future period. This income increases the firm’s liquidity and constitutes an important source of short-term finance. These payments are not showed as revenue till the supply of goods or services, but showed in the balance sheet as income received in advance.

Advance payment can be demanded by firms which are having monopoly power, great demand for its products and services and if the firm is manufacturing a special product on a special order.

4. Commercial Papers (CPs):

Commercial paper represents a short-term unsecured promissory note issued by firms that have a fairly high credit (standing) rating. It was first introduced in the USA and it is an important money market instrument. In India, Reserve Bank of India introduced CP on the recommendations of the Vaghul Working Group on Money Market. CP is a source of short-term finance to only large firms with sound financial position.

5. Public Deposits:

Public deposits or term deposits are in the nature of unsecured deposits, are solicited by the firms (both large and small) from general public primarily for the purpose of financing their working capital requirements.

6. Inter-Corporate Deposits (ICDs):

A deposit made by one firm with another firm is known as Inter-Corporate Deposit (ICD). Generally, these deposits are made for a period up to six months.

Such deposits may be of three types:

(a) Call Deposits:

These deposits are those expected to be payable on call/on just one day notice. But, in actual practice, the lender has to wait for at least 2 or 3 days to get back the amount. Inter-corporate deposits generally have 12 per cent interest per annum.

(b) Three Months Deposits:

These deposits are more popular among companies for investing the surplus funds. The borrower takes this type of deposits for meeting short-term cash inadequacy. The interest rate on these types of deposits is around 14 per cent per annum.

(c) Six months Deposits:

Inter-corporate deposits are made for a maximum period of six months. These types of deposits are usually given to ‘A’ category borrowers only and they carry an interest rate of around 16 per cent per annum.

7. Commercial Banks:

Commercial banks are the major source of working capital finance to industries and commerce. Granting loan to business is one of their primary functions. Getting bank loan is not an easy task since the lending bank may ask a number of questions about the prospective borrower’s financial position and its plans for the future.

At the same time the bank will want to monitor borrower’s business progress. But there is a good side to this, that is borrower’s share price tends to rise, because investor knows that convincing banks is very difficult. The different types or forms of loans are:

(i) Loans,

(ii) Overdrafts,

(iii) Cash credits,

(iv) Purchasing or discounting of bills and

(v) Letter of Credit.

8. Factoring:

Factoring is one of the sources of working capital. Banks have been given more freedom of borrowing and lending both internally and externally and facilitated the free functioning in lending and investment operations. From 1994, banks are allowed to enter directly leasing, hire purchasing and factoring services, instead through their subsidiaries. In other words, banks are free to enter or exit in any field depending on their profitability, but subject to some RBI guidelines. Banks provide working capital finance through financing receivables, which is known as “factoring”. A “Factor” is a financial institution, which renders services relating to the management and financing of sundry debtors that arises from credit sales.

Key takeaways

Short-term financing is aimed to meet the demand of current assets and pay the current liabilities of the organization. In other words, it helps in minimizing the gap between current assets and current liabilities.

References:

- Engineering Economics Management, Dr. Vilas Kulkarni and Hardik Bavishi, S. Chand Publication

- Laws for Engineers, Vandana Bhatt and Pinky Vyas, Pro Care Publisher

- Indian Economy, Gaurav Datt and Ashwani Mahajan, S. Chand Publication

- Industrial Organization & Engineering Economics, T. R. Banga and S. C. Sharma, Khanna Publisher