UNIT 1

INTRODUCTION

Modern business needs information about activities to be planned for the future. A major function of management is decision- making. It requires selection of an optimal course of action from among a set of alternatives. Costing techniques play an important role in gathering and analyzing revenue and cost data. It also helps to control business results and to make a proper appraisal of the performance of persons working in an organisation. Cost accounting also helps in acquiring Plant and Machinery, adding or dropping product, make or buy decision, special pricing of products and replacement of assets.

Evolution of Cost Accounting

The widespread interest in the subject of cost accounting could be said to have developed with Industrial Revolution which started in 1760. As mechanization, simplification, standardization and mass production followed in the wake of factory system, costing had to keep pace with these developments. Until the 18th century, cost accounting was in the domain of the engineer. Its integration with financial accounting began when accountants started to audit the cost records. Under the influence of financial accountant, cost accounting came to be viewed almost exclusively as a means of inventory valuation and profit measurement. It has grown only in the 20th century as an independent discipline.

Cost accounting has found to be of assistance to management, in compiling and providing requisite statistical data. It has developed rapidly and assisted management in providing valuable information to take appropriate decision in time. Cost Accounting throws light on the excessive waste of materials, inefficient labour operations, idle machinery and many other similar factors, which are responsible for reduction in the profit of the business activities. Managements found that cost accounting could render valuable assistance in planning, controlling and coordinating theactivities.

Definitions

Costing:

The institute of Cost & Management Accountants (ICMA) London has defined costing as the ascertainment of costs, costing includes techniques and processes of ascertaining costs.

Cost Accountancy:

The Institute of Cost and Management Accountants (ICMA) London has defined Cost Accountancy as the “application of costing and cost accounting principles, methods and techniques to the science, art and practice of cost control and ascertainment of profitability as well as presentation of information for the purpose of management decision making”. Accordingly Cost Accountancy includes costing, cost accounting, budgetary control, cost control and cost audit. Cost accounting refers to the process of determining and accounting the cost of some particular product or activity. It also includes classification, analysis and infers production of costs.

Cost Accounting:

The I.C.M.A. London defines Cost Accounting as “the process of accounting for cost from the point at which expenditure is incurred or committed to the establishment of its ultimate relationship with cost centers and cost units”.

In practice, costing, cost accounting and cost accountancy are often used interchangeably. Costing refers to ascertainment of costs, accumulation and measurement of cost of activities, processes, products or services. Cost data are used to prepare the statement of cost or cost sheet. Cost Accounting is a specialized branch of accounting which assists management to control costs and to create an awareness of the importance of cost to wells- being of the business organization. Systematic and useful cost data and reports are required to manage the business to achieve its objectives.

Cost Centre:

Cost Centre is a location, person or an asset for which costs can be ascertained and used for the purpose of cost control. It is an organizational segment or area of activity used to accumulate costs. Different types of cost centers used in a manufacturing organization are personal cost canters, impersonal cost centers, operation cost centers and process centers.

Cost Units:

A cost unit is a unit of quantity of product or service in relation to which cost may be ascertained. There should be a unit of activity for proper ascertainment of cost. Every organization has a unit of its own for measurement of raw materials, and finished products. Once the unit of activity is decided it becomes a cost unit for the cost accountant. The cost units should be suitable to the organization. The following are the examples of cost units in different industries :-

Nature of Industry Cost Unit

Cement Tonne

Cable Metre

Power Kilowatt/ hour

Hospital Per bed

The cost accounting objectives are normally used to denote activities for which costs are required to be determined separately. The activities may be function, organizational sub-division, contract or other work unit for which data are required. There is direct relationship among information needs of management, cost accounting objectives and techniques and tools used for analysis in cost accounting. Thus, cost accounting has the following objectives-

- To determine product costs.

- To facilitate planning and controlling of regular business activities.

- To supply information for short and long run decisions.

Importance of Cost Accounting

Cost Accounting is very important for a commercial organization. It is also useful for any other organization. It helps management in different fields one of such fields is presentation of information in the most useful manner. Cost Accounting is used to measure, analyze or estimate the costs. Profitability and Performance of individual products, departments and other segments of an organization, for either internal or external or both and to report to the interested parties. Cost Accounting concerns itself with the synthesis and analysis of costs. Its purpose in the modern days is to help management in the twin functions of decision- making and control. Thus, Cost Accounting is not simply cost finding but it is advising management, planning and control of organization and business operations. The Companies Act also provides that certain companies have to maintain cost accounting records and accounts and conduct the audit of cost accounts.

Advantages of Cost Accounting

A cost accounting system when installed will result in the following:-

- Cost Accounting reveals areas where materials were used excessively, labour operated inefficiently and expenses incurred exorbitantly.

- It suggests cost reduction programme. A continuous cost jointly with technical personnel seeking areas for effecting cost reduction brings beneficial results.

- Cost account locates the specific causes for the variations in profit. It points out the losing product or operations. It indicates reasons for loss and suggests remedial measures in time.

- It provides suitable data to management to select best alternatives. It may be to decide whether to buy or make a part, to operate Machine X or Y, to accept or reject an order below cost.

- Cost accounts give actual cost for price fixation. True demand and supply play vital role in fixing price. But cost is an essential guide here.

- It provides vital data to till in tenders. Tenders filled in with the help of marginal costing technique are successful.

- Standard costing and budgetary control aid maximum efficiency.

- Cost comparison helps cost control. Such comparison may be between different periods of the same department or comparable operations of different units.

- Cost data are useful to outside agencies like Government, Tribunals, etc., for taking decisions on tariff regulations, settlement of disputes, variations in wage levels etc.

- It provides idle capacity cost to assist overcoming capacity utilization crises.

- Marginal costing technique helps to take suitable short-term decisions in times of trade depression.

- Cost Accounting lays down cost centers and responsibility centers which ensure proper organizational structure.

- Cost accounting provides for perpetual inventory system. This enables inventory control and preparation of short-term profit and loss accounts.

- Cost of closing stock of raw materials, work in progress and finished products are readily available in cost records.

All organizations will not get all the advantages listed above. However, an efficiently operated costing system with full support from management can reap most of them.

Cost Accounting is a close follower of financial accounting. It is not independent of financial accounting. Though there are common grounds between the two, the important differences are given below:-

- Reporting: The major objective of financial accounting is external reporting whereas the focus of cost accounting has been essentially internal i.e. management.

- Flexibility: Financial accounting is mostly historical or after the event while cost accounting is much more flexible and open minded and includes in both retrospective and anticipatory calculations.

- Nature: Financial accounting classifies records, presents and interprets in terms of money transactions whereas cost accounting classifies, records, presents and interprets in a significant manner the material, labour and overhead costs involved in manufacturing and selling each product.

- Financial accounting uses Generally Accepted Accounting Principles while recording, classifying summarizing and reputing business transactions whereas cost accounting is not bound to use GAAP and it can use any technique or practice which generates useful information.

- Time Span: Financial accounting data are developed for a definite period, usually a year, half year or a quarter, but cost accounting reports and statements can be prepared whenever needed.

- Accounting Method: Financial Accounting follows the double – entry system for recording, classifying and summarizing business transactions. The data under Cost Accounting can be gathered for small or large segments or activities of an organisation and monetary as well as other measures can be used for different activities in the organisation.

Cost concepts

Cost represents a sacrifice, a foregoing or a release of something of value. It is reckoned in money and usually appears as payment of money. It is money outlay for productive factors.

Costs are expenditure incurred in doing something. Costing is the process of determining the cost of doing something i.e. cost of manufacturing an article, rendering service or performing a function.

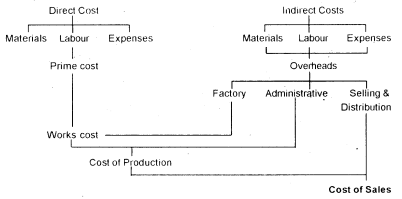

Cost is composed of three elements- material, labour and expenses or overheads. Each of these costs can be further classified as (a) Direct and (b) Indirect.

Direct costs are costs which can be easily identified with a particular Product, Process or Department. Indirect costs refer to costs which cannot be conveniently identified with a particular product. Process or Department. Indirect costs are common costs like rent, repairs salaries, which are incurred for the benefit of a number of cost units or cost centers.

Cost classification

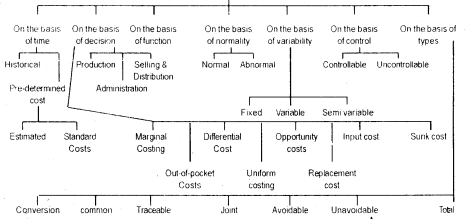

Cost items are analyzed or grouped according to their common characteristics which is some independent factor. There are many objectives of cost classifications depending on the requirements of management. The different cost classifications are as follows:-

Cost Classification by Elements:

The constituent elements of costs are broadly classified into three distinct elements i.e. materials, labour and expenses. These three elements of cost can be further grouped into direct and indirect categories. Direct materials refer to the cost of materials which are conveniently and economically traceable to specific units of output. For example: Raw cotton in textiles, crude oil in making diesel. The indirect materials refer to materials that are needed for the completion of the product but whose consumption with regard to the product is either so small or so complex that it would not be appropriate to treat it as a direct material. For example: stationery lubricants, cotton waste etc.

Cost Classification by Function:

A business organisation has to perform several functions such as Manufacturing, Administration, Selling and Distributing and Research and Development. Functional classification of cost implies that the business performs many functions for which costs are incurred. Expenses or Costs are usually classified by function and grouped under the headings of Manufacturing, Selling and Administrative costs in measuring net income.

Manufacturing costs are all check costs incurred to manufacture the products and to bring them to a saleable condition. This includes direct material, direct labour and indirect manufacturing costs or overheads. Administration costs are incurred for formulation of policy, directing the organisation and controlling the activities excluding the cost of research, development, production, selling and distribution. These costs include salary of executives, office, staff, office rent, stationery, postage etc. Selling costs include the cost of creating and stimulating demand and getting customers. For example: advertisement, salary and commission to salesmen, packing. Distribution costs include the cost of warehouse, freight, cartage etc.

Research and Development costs are incurred in the process of finding out new ideas, new processes by experiments or other means of putting the results of such experiments on a commercial basis. Functional classification of cost is important because it provides an opportunity to the management to evaluate the efficiency of departments performing different functions in an organisation.

Cost Classification by variability:

Cost can be classified as (i) fixed (ii) variable and (iii) semi - fixed or semi variable in terms of their variability or changes in cost behaviour in relation to changes in output or activity or volume of production. Activity may be indicated in any form such as units of output, hours worked, sales, etc. The separation of costs into variable and fixed categories is the most difficult part of the costing operation. Certain costs are easily identifiable as variable or fixed while other costs can be segregated only after careful consideration of their nature and an examination of their behaviour.

Fixed costs:

Fixed cost is a cost which does not change in total for a given time period despite wide fluctuations in output or volume of activity. These costs must be met by the organisation irrespective of the volume level. These costs are also known as capacity costs, period costs or stand - by costs; for example, rent, property taxes, supervisor’s salary, advertising, insurance etc.

Variable costs:

Variable costs are those costs which vary directly and proportionately with the output. There is a constant ratio between the change in the cost and the change in the level of output. Direct materials and labour are the examples of variable costs. Thus, all these costs which tend to vary directly with variations in volume of output are variable costs. However, it must be remembered that variable costs remain the same or approximately the same in amount per unit of production regardless of increase or decrease in volume.

Semi variable or semi fixed costs:

There is another group of costs in between the fixed and variable costs. It is semi variable or semi fixed costs. These costs vary in some degree with volume but not in direct proportion. Such costs are fixed only in relation to specified constant conditions. Semi fixed costs are those costs which remain constant upto a certain level of output after which they become variable. For example: maintenance of building, depreciation of plant, supervisor’s salary, telephone expenses etc.

Composition of Elements of Costs:

A manufacturing organisation converts raw materials into finished products. For that it employs labour and provides other facilities. While compiling production cost, amount spent on all these are to be ascertained. For this purpose, cost are primarily classified into various elements. This classification is required for accounting and control.

The elements of cost are

(i) Direct material

(ii) Direct labour

(iii) Direct expenses and

(iv) Overhead expenses.

The following chart depicts the broad headings of costs and this acts as the basis for preparing a Cost sheet.

Elements of cost

Elements of cost

Materials Labour OtherExpenses

Direct Indirect Direct Indirect Direct Indirect

Overheads

Factory Administrative Selling &Distribution

Break up of cost sheet

Classification of Cost

Prime Cost:

The aggregate of Direct material cost, Direct labour and Direct expenses is termed as Prime Cost. Direct costs are traceable to products or jobs.

Direct materials

It includes cost of materials consumed in the production process which can be directly allocated to the cost center. Direct material can be identified and charged to the finished product.

Examples:

- Material specially purchased for a specific job or process.

- Materials passing from one process to another.

- Consumption of materials or components manufactured in the same factory.

- Primary packing materials.

- Freight, insurance and other transport costs, import duty, octroi duty, carriage inward, cost of storage and handling are treated as direct costs of the materials consumed.

In certain cases direct materials are used in small quantities and it will not be feasible to ascertain their costs and allocate them directly. For instance, nails used in the manufacture of chairs and tables, glue used in the manufacture of toys. In such cases cost of the total quantity consumed for the period will be treated as Indirect costs.

Direct Labour

This includes the number of wages which can be easily identified and directly charged to the product. These are the costs for converting raw material into finished products. Wages paid to workers for operating Lathe machines, Drilling machines etc. in a Tool room are direct wages.

Direct Expenses

This includes expenses other than materials and labour which can be easily identified with a particular product or process. For example: Excise duty expenses. Indirect costs cannot be easily identified with a particular products or process.

Indirect materials

Materials which cannot be traced as part of the finished products are known as Indirect materials.

Examples:

- Consumable stores such as lubricants, cotton wastes, tools etc.

- Materials of insignificant value not worthwhile to ascertain the cost separately, for charging directly such as nails (for making chair) glues (for making toys). These materials can be apportioned to or absorbed by cost centers or cost units arbitrarily.

Indirect labour:

Indirect labour is the cost which cannot be directly charged or identified to the finished product. Indirect labour is apportioned to or absorbed by cost centers or cost units suitably.

Examples:

- Salary to Store- keeper

- Wages to Time – keeper

Indirect Expenses:

These are general expenses not incurred for any particular product or service and not chargeable to the products directly.

Examples:

- Rent, Rates and Insurance of Factory

- Power, lighting, heating, repairs, telephone expense, printing and stationery.

Overheads can be sub-divided into following main groups.

Factory or Works Overheads: Also known as manufacturing or production overheads it consists of all costs of indirect materials, indirect labour and other indirect expenses which are incurred in the factory.

Examples: Factory rent and insurance. Depreciation of Factory building and machinery.

Office or Administration overheads: All indirect costs incurred by the office for administration and management of an enterprise.

Examples: Rent, rates, taxes and insurance of office buildings, audit fees, director’s fees.

Selling and Distribution overheads: These are indirect costs in relation to marketing and sale.

Examples: Advertising, salary and commission of sales agents, travelling expenses of salesmen.

Cost sheet is a statement prepared to present the detailed costs of total output during a period. It provides information relating to cost per unit at different stages of total cost of production. The preparation of cost sheet is one of the important and primary function of cost accounting. Cost sheet is not an account. There is a prescribed form for preparation of cost sheet. A cost sheet is a statement of cost prepared for a given period of time in such a manner that it indicates various elements of cost as clearly as possible. A cost sheet is useful in ascertaining the total cost of production per unit, formulation of production plan, fixing up the selling price and minimizes the production cost. Sometimes standard cost data are provided to facilitate comparison with the actual cost increased. The preparation of the cost sheet requires understanding of the treatment of the following items:-

Stock of raw materials: The opening and closing stock of raw materials are to be adjusted with purchase of Raw materials in order to determine the value of raw materials consumed for the output produced. Carriage/Freight inward and Octroi on purchase etc. also to be added to purchases. This is a part of Prime Cost.

Stock of Work in Process: The value of stock of work in process is a part of Factory cost and therefore, it should be adjusted with factory overheads. Sale of scrap should be deducted from the factory overheads in order to determine the total factory cost.

Stock of Finished goods: Finished goods cover the products on which factory work has been completed. It is the cost of completed production. The opening and closing values of finished goods are to be adjusted with the total cost of production in order to arrive at cost of sales.

Expenses excluded from cost sheet:

There are certain expenses /costs which do not form a part of cost sheet. Some of these expenses are an apportionment of profit. Examples of these expenses are -

- Dividend to shareholders

- Income Tax

- Interest on loan

- Donations paid

- Capital expenditure

- Capital loss on sale of assets.

- Commission to Partners / Managing Director

- Discount on issue of shares/ debentures

- Underwriting commission.

- Writing of goodwill/ bad debts

- Provision for Taxation, Bad Debts or any kind of Fund or reserves.

Specimen of Cost Sheet

Cost Sheet for the period

(Production ------ Units)

Particulars | Total Cost Rs. | Cost Per Unit Rs. |

Direct Materials Raw Materials Opening stock Materials : Add : Purchases Add : Carriage /FreightInwards Less :Closingstock Cost of materials consumed Direct Labour Direct Expenses

Prime cost Factory overheads Add: Work in Progress (Opening ) Less : Work in Progress (Closing )

Works /Factory cost Add: Office and administrative expenses

Cost of Production (of goods produced)

Add: Op. Stock of finished goods Less closing of finished goods

Cost of production (of goods sold) Add: Selling & Distribution expenses

Cost of Sales Add: Profit (Loss) Sales |

|

|

Elements of Total Cost

Costs are classified under different heads which represent the successive stages through which the cost flow.

Prime Cost

Prime cost is the basic cost of any product. It comprises of those expenses which could be traced directly to it. The prime cost consists of cost of direct materials, direct labour and direct expenses. Direct expenses include special expenses which can be identified with product or job and are charged directly to the product as part of the prime cost. For example cost of hiring special plant or machinery, cost of special moulds, design or patterns, Architect’s fees, Royalties, License fees etc.

Works cost:

Works cost of a Product consists of prime cost plus the portion of works or factory expenses chargeable against the Production. Works or factory expenses include indirect materials indirect labour and indirect expenses. Indirect materials refer to those materials that are needed for the completion of the product but the consumption of these materials is either so small or complex that it would not be appropriate to treat it as direct materials. These are supplies that cannot be conveniently and economically charged to a specific unit of output. For example, lubricants, cotton waste, works stationery etc.

Indirect labour is that labour which does not affect the construction or the composition of the finished product. This is the labour cost of production related activities that cannot be associated with or conveniently traced to specific product through physical observation. For example, Foremen’s salary and salary of employees engaged in maintenance or service work. Indirect expenses cover all expenditure incurred by the manufacturer from the time of production to its completion as delivery to customer by way of rate of product. Any expense that cannot be allocated but which can be apportioned to or absorbed by the cost centers/ cost units are known as indirect expenses. These expenses are incurred for the benefit of more than one product, job or activity and therefore, must be apportioned by appropriate bases to the various functions or products. For example, lighting and heating, maintenance factory manager’s salary, watch and ward department’s salary etc.

Cost of Production:

Cost of Production consists of works cost plus an additional amount of office and administrative expenses. It includes all expenses connected with the managerial functions such as planning, organizing, directing, coordinating and controlling the operations of the manufacturing business. For example, office rent, salary, lighting, stationery, repairs and maintenance and depreciation of office building, audit fees, legal expenses.

Cost of Sales:

Cost of sales consists of cost of production plus proportionate selling and distribution expenses of the product. Selling expenses include the expenses incurred for creating demand for the product such as advertisement, salaries of salesmen, selling expenses and show room expenses. Distribution expenses are those expenses incurred in connection with the delivery of goods to the customers such as packing, carriage outwards, warehouse expenses.

A costing system is an established set of procedures, rules, cost records, etc., for the purpose of achieving specified objective at minimum cost. It forms the basis for future operations.

Steps for installation of a costing system

Objectives to be achieved:

The first step is to clear the objectives of the costing system so that a thrust is given to that aspect. If the main objective is to improve the marketing then the costing system should give more attention to marketing aspect, if the emphasis is to expand production of products then that area should be cared well. The objective is to get information for decision making, planning and control.

Study the Product:

The study of the product is very essential. The type of costing system to be used is determined by the nature of the product. For example if the product requires high costs on materials then the costing system will give main emphasis on pricing, storing, issuing and controlling of material cost. On the other hand, if the product requires high labour cost then efficient system of time-recording and wage payment will be essential and the same will be true of overhead cost too.

Study the organization

The costing system should be designed to meet the requirements of the organization. It is necessary to study the nature, size and layout of the organization. The factors to be considered are as follows

- Size of the organization and the size of the departments.

- The physical layout of the organization.

- The different levels of management.

- The extent of decentralization of authority.

- The nature of authority relationships.

Deciding the Structure of Cost Accounts:

The next step in the process of installing a costing system is to take decision about the structure of cost accounts. The details of a suitable costing system should be worked out. The structure of cost accounts should be simple and in accordance with the natural production process.

Selecting the Cost Rates:

The next step is to determine the cost rates and the allocation of various expenses among different products. The following points should be considered

- Classification of costs into direct and indirect costs.

- Grouping of indirect costs (overheads) into production, administration, selling and distribution etc.

- Methods of pricing issues.

- Treatment of wastes of all types.

- Absorption of overheads.

- Calculation of overhead rates.

Introduction of the system

After completion of the above steps, the costing system may be formally introduced. The success of the costing system will depend upon its proper implementation. Its implementation will be done with the full co-operation of employees in the organization. If required, the system should be gradually introduced instead of implementing it in full.

A Follow-up:

The last step is to take the follow up. A follow-up of the system is essential to make it practicable and useful. The weaknesses and deficiencies may be realized when a system is put into actual practice. While collecting cost information from various sources there may be some delays in supplying information.

A cost accountant is responsible for increasing profits and reduction of the company's financial waste. Duties of cost accountant include determining actual cost, scrutinizing associated expenses, analyzing profitability and preparing the company budget. Cost Accountants are required to work closely with management, to effectively achieve financial objectives.

Cost accounting is a form of management accounting and is used to understand the fixed and variable costs associated with producing and delivering the goods and services produced by an organization.

Cost accountants who determine the costs associated with providing a service or manufacturing a product by analyzing expenses within the supply chain. They measure and record actual costs such as labour, shipping, production and administration, both across a function and at a unit level, to determine the true cost of bringing goods and services to market. Cost accountants help to plan, budget and monitor performance, set standard unit costs and recommend appropriate cost-saving opportunities. The role is important in determining where a company is spending money as well as which products, departments or services are most profitable.

Key responsibilities

Responsibilities will vary which include:

- Collecting and validating data to determine both fixed and variable costs of business activity such as rent, raw material purchases, inventory and labour

- To determine effects on cost, analyze changes in product design, raw materials, manufacturing methods or services provided,

- Analyzing actual manufacturing costs and preparing periodic reports comparing standard costs to actual production costs

- Recording cost information for use in controlling expenditures

- Cost-saving options are recommended

- To ensure accuracy performing ongoing reconciliations of various cost reports against software systems

- Providing management with reports specifying and comparing factors affecting prices and profitability of products or services

- Initiating the month-end closing and reporting processes, which they in turn submit to management

- Performing physical inventory inspections and monitoring inventory management information systems