UNIT I

BASIC CONCEPTS

Income concept

While the Income Tax Act does not define the term income, Section 2 (24) of the Act describes the various receipts contained under the income range.

Section 4 of the Income Tax Act, 1961, is the charging section of the law. Therefore, in this section:

Head of income

Income falls under 5 major heads under Section 14 of the act

Agricultural income is rent or income in cash or in kind derived from the land, which is used for agricultural purposes and the land must be located in India. Income from agriculture should be produced by the cultivator or the beneficiary of the spot rent of its agricultural products, which is suitable for incorporating it into the market.

The income should be obtained from the sale by the cultivator or the rental recipient of its products produced or received by him and cannot carry out any process other than the process of adapting it to the market.

Casual income means an income which is casual in nature, i.e., which is unplanned, uncertain, accidental, sudden income which occurs just by chance and the person cannot depend upon it to produce income in future.

Example: Winning from lotteries, gambling, betting, etc.,

Apart from these, any incomes which are unanticipated and non-recurring in nature are called Casual incomes.

Similarly, capital gains, receipt from a business or an occupation and one-time benefits like bonus given to employees are not casual incomes.

As per Income Tax Act: Casual incomes upto Rs. 5000/- were exempt from tax but at present all casual incomes are subject to tax at 30% plus education cess (including surcharge, if any). They are treated as income from other sources and are taxable u/s 56 of Income Tax Act.

Assessment Year is the year in which one file income tax returns of the year prior to it (i.e. Financial Year). It is the year in which the income that one has earned in the financial year that is just ended is evaluated.

E.g. For Financial Year 2014-15 the Assessment Year will be 2015-16.

As per the Income Tax law the income earned in current year is taxable in the next year. The year in which income is earned is known as the previous year.

In layman language the current financial year is known as the previous year. The financial year starts from 1st April and end on 31st March of the next year.

For Instance, for the salary income earned from 1 April 2017 - 31st March 2018 .The previous year would be 2017-18.

All the assessee’s are required to follow the financial year( April 1 to March 31) as previous year for all types of incomes. In case, of a newly set-up business/profession or first job then your first previous year may be less than 12 months. Though from subsequent years your previous year will always be your financial year.

What are the five heads of income?

As per section 14 of the Income Tax Act, income is classified into the following categories known as Heads of Income.

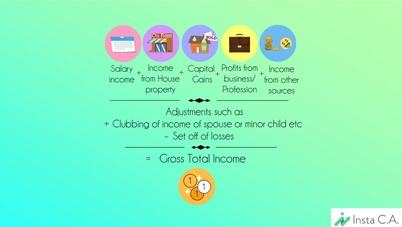

What is Gross Total Income?

Gross total income (GTI) is the sum of incomes computed under the five headsof income i.e. salary, house property, business or profession, capital gain and other sources after applying clubbing provisions and making adjustments of set off and carry forward of losses.

GTI = Salary Income + House Property Income + Business or Profession Income + Capital Gains + Other Sources Income + Clubbing of Income - Set-off of Losses

What are the types of Gross Total income (GTI)?

Gross total income is to be categorized in 2 parts

Other GTI includes:

Person [Section 2(31)]: Definition under Income Tax Act

Person includes:

The word person is a very wide term and embraces in itself the following :

Individual. It refers to a natural human being whether male or female, minor or major.

Hindu Undivided Family. It is a relationship created due to operation of Hindu Law. The manager of HUF is called “Karta” and its members are called ‘Coparceners’.

Company. It is an artificial person registered under Indian Companies Act 1956 or any other law.

Firm. It is an entity which comes into existence as a result of partnership agreement between persons to share profits of the business carried on by all or any one of them. Though, a partnership firm does not have a separate legal entity, yet it has been regarded as a separate entity under Income Tax Act. Under Income Tax Act, 1961, a partnership firm can be of the following two types

Association of Persons or Body of Individuals, Co-operative societies, MARKFED, NAFED etc. are the examples of such persons. When persons combine togather to carry on a joint enterprise and they do not constitute partnership under the ambit of law, they are assessable as an association of persons. Receiving income jointly is not the only feature of an association of persons. There must be common purpose, and common action to achieve common purpose i.e. to earn income. An AOP. can have firms, companies, associations and individuals as its members.

A body of individuals (BOl) cannot have non-individuals as its members. Only natural human beings can be members of a body of individuals. Whether a particular group is AOP or BOl is a question of fact to be decided in each case separately.

Local Authority: Municipality, Panchayat, Cantonment Board, Port Trust etc. are called local authorities.

Artificial Juridical Person: A public corporation established under special Act of legislature and a body having juristic personality of its own are known to be Artificial Juridical Persons. Universities are an important example of this category.

Tax Evasion in India

There are many methods that people use to evade paying taxes in India that range from false tax return and smuggling to fake documents and bribery. The penalties for this are high, from 100% to 300% of the tax for undisclosed income.

What is Tax Evasion?

Tax evasion is illegal action in which a individual or company to avoid paying tax liability. It involves hiding or false income, without proof of inflating deductions, not reporting cash transaction etc. Tax evasion is serious offense comes under criminal charges and substantial penalties.

Rooting for taxes is never an easy thing because most people question that concept of giving away part of their earning to a government but the fact is that taxes are an important source of income for the government. This is the money that is invested in various development projects that are meant to improve the company's situation. But the country has been facing a massive problem with tax evasion. People who should be paying taxes have found ways not to pay them and, as a result, it may be said that the income of the country has been suffering. So let's take a look at what are the ways in which people are avoiding taxes and what are the penalties for it.

Common Methods of Tax Evasion

There are two aspects of not paying taxes when they are due. The first is tax avoidance and the other tax evasion. The difference between the two is that tax avoidance is basically finding a loophole that exempts you from paying taxes and is not strictly illegal, while evasion is not paying the taxes when they are actually due, which is absolutely illegal. These are some of the ways in which people may avoid/evade taxes.

This is the simplest way in which someone may evade taxes. They simply won't pay it to the government, not even when the dues are called for. A person engaged in this sort of tax evasion won't, willingly or unwillingly, pay the tax before or after the due date.

When certain goods move from one location to another, across international or state borders, a tax or charge may be payable in order to move the goods. However, some individuals may move these goods in surreptitious ways in order to avoid paying those taxes that evading the tax altogether.

In some cases, when an individual files taxes, they may submit false or incorrect information in order to either lessen the tax that they are supposed to pay or not pay it at all. This is also tax evasion since the complete information is not provided and they may actually be paying less than what they should.

The taxes that are payable by an individual or an organisation may be decided on the financial dealing that have taken place during the assessment year. If false financial documents or accounts books are submitted, ones that show incomes less than what was actually earned, the tax may come down.

The government may have provided certain exemptions and privileges to certain strata or members of society in order to ensure they have a bit more financial freedom to progress. In some cases, members who actually don't qualify for such privileges will get documents created to support their claim of being a part of that group thus claiming exemptions where they are not suited.

It could be said that this is one of the most common methods of tax evasion. In this case, individual just won't report any income that they receive during a financial year. Not having reported any income, they don't pay any tax thus successfully evading tax all together. The simplest example of this would be a landlord who has kept tenants but has not informed the authorities that he has rented the house and is actually receiving an income from it.

There may be a situation where there a certain amount due in taxes which the individual may not be willing to pay. In such a case he or she may actually offer a bribe to officials to not make them pay the tax and to make it 'disappear'.

We have all heard tales of Swiss bank accounts. Offshore accounts are accounts maintained outside the country and information about the dealing in these accounts is not disclosed to the income tax department thereby evading any and all taxes due on that wealth.

Penalties for Tax Evasion:

There are various penalties that the income tax department can impose on anyone who is found guilty of evading or avoiding taxes. These penalties can also apply to companies that either fail to report and pay their own taxes or fail to deduct taxes at source when they are supposed to.

Some of these may be:

Collecting 100% to 300% of the tax when income is not disclosed.

In case of a failure to pay the tax due, the assessing officer may impose a penalty amount but it cannot exceed the amount due in taxes.

If an individual fails to file tax statements within the time allotted then a penalty of Rs. 200 per day may be charged for every day that the statements are not filed.

In case someone has concealed details of their income or any fringe benefits that are taxable, the penalty can range from 100% to 300% of the tax amount due.

In case a person or a company fails to maintain their accounts properly as directed by section 44AA, a penalty of Rs. 25,000 may be levied.

If a company fails to get itself audited or fails to provide a report of said audit, then a penalty of Rs. 1.5 lakhs or 0.5% of the sales turnover, whichever is less, may be charged.

If a report from an accountant is not provided as directed then a fine of Rs. 1 lakh may be levied.

In case an organisation fails to deduct tax where it is supposed to while making payments then the penalty could be payment of the tax due.

These are just some of the penalties that can be levied by the Income Tax department and, in some cases, it can be a hefty sum to pay, so best thing to do is to ensure that all taxes are paid when they are due.

Tax Avoidance:

Tax avoidance is an act of using legal methods to minimize tax liability. In other words, it is an act of using tax regime in a single territory for one’s personal benefits to decrease one’s tax burden. Although Tax avoidance is a legal method, it is not advisable as it could be used for one’s own advantage to reduce the amount of tax that is payable. Tax avoidance is an activity of taking unfair advantage of the shortcomings in the tax rules by finding new ways to avoid the payment of taxes that are within the limits of the law. Tax avoidance can be done by adjusting the accounts in such a manner that there will be no violation of tax rules. Tax avoidance is lawful but in some cases it could come in the category of crime.

Tax Planning:

Tax planning is process of analyzing one’s financial situation in the most efficient manner. Through tax planning one can reduce one’s tax liability. It involves planning one’s income in a legal manner to avail various exemptions and deductions. Under Section 80C, one can avail tax deduction if specific investments are made for a specific period up to a limit of Rs 1, 50,000. The most popular ways of saving tax are investing in PPF accounts, National Saving Certificate, Fixed Deposit, Mutual Funds and Provident Funds. Tax planning involves applying various advantageous provisions which are legal and entitles the assesse to avail the benefit of deductions, credits, concessions, rebates and exemptions. Or we can say that Tax planning is an art in which there is a logical planning of one’s financial affairs in such a manner that benefits the assesse with all the eligible provisions of the taxation law. Tax planning is an honest approach of applying the provisions which comes within the framework of taxation law.

Features and differences between Tax evasion, Tax avoidance and Tax Planning:

1. Nature: Tax planning and Tax avoidance is legal whereas Tax evasion is illegal

2. Attributes: Tax planning is moral. Tax avoidance is immoral. Tax evasion is illegal and objectionable.

3. Motive: Tax planning is the method of saving tax .However tax avoidance is dodging of tax. Tax evasion is an act of concealing tax.

4. Consequences: Tax avoidance leads to the deferment of tax liability. Tax evasion leads to penalty or imprisonment.

5. Objective: The objective of Tax avoidance is to reduce tax liability by applying the script of law whereas Tax evasion is done to reduce tax liability by exercising unfair means. Tax planning is done to reduce the liability of tax by applying the provision and moral of law.

6. Permissible: Tax planning and Tax avoidance are permissible whereas Tax evasion is not permissible.

Tax liability of an individual can be reduced through 3 different methods- Tax Planning, Tax avoidance and Tax evasion. All the methods are different and interchangeable.

Tax planning and Tax avoidance are the legal ways to reduce tax liabilities but Tax avoidance is not advisable as it manipulates the law for one’s own benefit. Whereas tax planning is an ideal method.

Key Takeaways:

The charging section, Section 15 states that, salary is taxable on “due” or “paid” basis whichever is earlier. That is, if it is due, it is included in taxable salary, irrespective of whether it is paid or not, and if it is paid, it is taxable, irrespective of whether it is due or not. Therefore, it is only logical to note that if it has already been taxed on due basis, the same cannot be taxed again when it is paid. Similarly, if a salary which was paid in advance, if it has already been taxed in the year of payment, it cannot subsequently be taxed when it becomes due.

Advance salary is taxable; however, an advance against Salary is essentially a loan which will be recovered later from the employee and therefore that isn’t taxable.

Salary, if earned in India, is deemed to accrue / arise in India, even if it is paid outside India.

Section -5 of Income Tax Act, 1961 provides Scope of total Income in case of of person who is a resident, in the case of a person not ordinarily resident in India and person who is a non-resident which includes. Income can be Income from any source which (a) is received or is deemed to be received in India in such year by or on behalf of such person; or (b) accrues or arises or is deemed to accrue or arise to him in India during such year; or (c) accrues or arises to him outside India during such year.

Table explaining Scope of total Income under section 5 of Income Tax Act, 1961

Sr. No | Particulars | Resident Ordinary Resident (ROR) | Resident Not Ordinary Resident (RNOR) – 5(1) | Non Resident (NR)– 5(2) |

1 | Income received in India | Taxed | Taxed | Taxed |

2 | Income Deemed to be receive in India | Taxed | Taxed | Taxed |

3 | Income accrues or arises in India | Taxed | Taxed | Taxed |

4 | Income deemed to accrues or arises in India | Taxed | Taxed | Taxed |

5 | Income accrues or arises outside India | Taxed | NO | NO |

6 | Income accrues or arises outside India from business/profession controlled/set up in India | Taxed | Taxed | NO |

7 | Income Other than Above (No Relation In India) | Taxed | NO | NO |

Note-

Explanation 1 & 2:-

Income accruing or arising outside India shall not be deemed to be received in India within the meaning of this section by reason only of the fact that it is taken into account in a balance sheet prepared in India.

Income which has been included in the total income of a person on the basis that it has accrued or arisen or is deemed to have accrued or arisen to him shall not again be so included on the basis that it is received or deemed to be received by him in India.

Key Takeaways:

The Income Tax Act, 1961, (Act) to consolidate and amend the law relating to income tax. However, not everyone is liable to pay taxes on income under the Act. The Act makes certain exceptions and exempts certain kind and extent of income from taxation. As per Section 2(31) of the Act, defines the term “Person” for whom we will assess the income. Further, those who are liable to pay tax and whose incomes are assessed under the Act are known as “Assessees” and the same has been defined under section 2(7) of the Act. Also, for determining the tax liability of the Assessees, the same has been further categorise on the basis of Residential Status.

Residential status is a term coined under Income Tax Act, 1961, and has nothing to do with nationality or domicile of a person. An Indian, who is a citizen of India can be non-resident for Income-tax purposes, whereas an American who is a citizen of America can be resident of India for Income-tax purposes, as per the Income Tax Act, 1961. Residential status of a person depends upon the territorial connections of the person with this country, i.e., for how many days he has physically stayed in India in any particular Financial Year.

Further it is to be note that the residential status of different types of persons viz an individual, a firm, a company etc is determined differently. Here, we have discussed about how the residential status of an individual taxpayer can be determined for the Previous Year i.e 2019-2020 or Assessment Year 2020-2021.

Determining the Residential Status of an Individual

Under the Act, Residential Status of an individual is either Resident of India or Non-Resident of India. The first thing that needs to be kept in mind is that the residential status is determined with respect to the previous financial year – hence, an individual may be a resident in one year and a non-resident in the next year.

As per Section 6(a) of the Act which mandates that an individual is said to be resident of India in any previous year, if he satisfy any of the following primary conditions, otherwise the person become Non-Resident of India, if an individual-

i. Is in India in previous year for 182 days or more; or

ii. Is in India in previous year for 60 days or more and 365 days or more in the immediate 4 preceding Financial Year.

Further Act provides certain exemption to following persons to comply only clause (i) to become resident in India:

a. Citizen of India who leaves India for taking up employment outside India;

b. Indian Citizen who leaves India as a member of the crew of Indian Ship;

c. Citizen of India or to a person of Indian origin who visit India;

Further, Clause (a) of Section 6 of the Act, a Resident of India can be termed as Resident-Ordinary Resident of India, if an individual satisfy all the following two conditions, otherwise he can be termed as Resident-Not Ordinary Resident of India, if

i. An individual is a resident in India for 2 years out of 10 previous years preceding current financial year; and

ii. An individual is in India for 730 days or more in 7 previous years preceding current financial year.

Amendment have also been made vide Finance Act, 2020, From F.Y. 2020-21, a citizen of India or a person of Indian origin who leaves India for employment outside India during the year will be a resident and ordinarily resident if he stays in India for an aggregate period of 182 days or more. However, this condition will apply only if his total income (other than foreign sources) exceeds Rs 15 lakhs.

The Finance Act, 2020, has also introduced the concept of “Deemed Resident” whereby all such citizen of India who are not taxable in any other country by reason of residence or domicile or any other criteria of similar nature and such individuals have income exceeding Rs. 15 lakhs from sources in India and from business controlled from India or Profession set up in India. With effect From F.Y. 2020-202 1 deemed resident will be a resident and ordinarily resident in India.

Tax Incidence in India

A Resident Ordinary Resident is subject to tax on his global income in India. Resident Not Ordinary Resident and Non-Residents are generally subject to tax in India only in respect of India source income that is, income received, accruing or arising in India or deemed to be received, accrued or arisen in India.

Salary received in India or for services provided in India, rental income from a house property in India, capital gains on sale of assets in India — be it shares or house property, income from fixed deposits or savings bank account in India are instances of income which would be taxed in the hands of not just tax residents of India, but also Resident Not Ordinary Resident and Non-Residents.

Conclusion

In order to enjoy tax benefits through Non-Resident Status, individuals visiting India on a business trip should not stay for more than 181 days during one previous business year and their total stay in the previous four years should not exceed more than 364 days.

If individuals, having been in India for more than 365 days during four years preceding the relevant previous year, and stay for more than 60 days in the previous year, they should plan their visit to India in such a manner that their total stay in India falls under two previous years. Such persons can come to India any time in the first week of February and stay till May 29.

Key Takeaways:

Various categories of income are exempt from income tax under section 10. The assessee has to establish that his case clearly and squarely falls within the ambit of the said provisions of the act.

1. Agriculture Income:

We can still consider India is the country mostly depending upon the agriculture and income generated from the activities of agriculture. Agriculture income shall be excluded from the assessee total income (section 10, (1)) however, it shall be taken for considering rate to tax non-agriculture income.

2. Share Of Profit From A Firm:

A partners share in the total income of the firm is totally exempted from the total income of the hands of the partner because firm is separately assess as such. However, any salary interest commission paid or payable to the partner which was deductible from the total income of the firm shall be included in the income of the partners total income as his business.

3. Leave Travel Concession:

If an employee goes on travel (on leave) with his family and traveling cost is reimbursed by the employer, then such reimbursement is fully exempted. But some provisions for it was as bellow;

1) Journey may be performed during service or after retirement.

2) Employer may be present or former.

3) Journey must be performed to any place within India.

4) In case, journey was performed to various places together, then exemption is limited to the extent of cost of journey from the place of origin to the farthest point reached, by the shortest route.

5) Employee may or may not be a citizen of India.

6) Stay cost is not exempt.

4. Allowance Or Perquisite Paid Outside India [Sec. 10(7)]:

Any allowance or perquisite paid outside India by the Government to a citizen of India for Rendering Services Outside India.

5. Death-Cum-Retirement-Gratuity [Sec. 10(10)]:

Gratuity is a retirement benefit given by the employer to the employee in consideration of past services. Sec. 10(10) deals with the exemptions from gratuity income. Such exemption can be claimed by a salaried assessee. Gratuity received by an assessee other than employee shall not be eligible for exemption u/s 10(10). E.g. Gratuity received by an agent of LIC of India is not eligible for exemption u/s 10(10) as agents are not employees of LIC of India.

6. Compensation For Any Disaster [Sec. 10(10bc)]:

Any amount received or receivable from the Central Government or a State Government or a local authority by an individual or his legal heir by way of compensation on account of any disaster, except the amount received or receivable to the extent such individual or his legal heir has been allowed a deduction under this Act on account of any loss or damage caused by such disaster.

7. Sum Received Under A Life Insurance Policy [Sec. 10(10d)]:

Any sum received under a life insurance policy including bonus on such policy is wholly exempt from tax. However, exemption is not available on – 1. any sum received u/s 80DD (3) or u/s 80DDA (3); or 2. any sum received under a Keyman insurance policy; or 3. any sum received under an insurance policy issued on or after 1-4-20121 in respect of which the premium payable for any of the years during the term of the policy exceeds 10%2 of the actual capital sum assured.

8. Payment from National Pension Trust [Sec. 10(12a) & 10(12b)]:

Any payment from the National Pension Scheme Trust to an assessee on closure of his account or on his opting out of the pension scheme referred to in sec. 80CCD, to the extent it does not exceed 60% of the total amount payable to him at the time of such closure or his opting out of the scheme [Sec. 10(12A)] Any payment from the National Pension System Trust to an employee under the pension scheme referred to in sec. 80CCD, on partial withdrawal made out of his account in accordance with the terms and conditions, specified under the Pension Fund Regulatory and Development Authority Act, 2013, to the extent it does not exceed 25% of the amount of contributions made by him [Sec. 10(12B)]

9. Payment from Approved Superannuation Fund [Sec. 10(13)]:

Any payment from an approved superannuation fund made – • on the death of a beneficiary; or • to an employee in lieu of or in commutation of an annuity on his retirement at or after a specified age or on his becoming incapacitated prior to such retirement; or • by way of refund of contributions on the death of a beneficiary; or • by way of refund of contributions to an employee on his leaving the service (otherwise than by retirement at or after a specified age or on his becoming incapacitated prior to such retirement) to the extent to which such payment does not exceed the contributions made prior to 1-4-1962 and any interest thereon by way of transfer to the account of the employee under a pension scheme referred to in sec. 80CCD and notified by the Central Government.

10. Income of Mutual Fund [Sec. 10(23D)]:

Any income of – a. A Mutual Fund registered under the Securities and Exchange Board of India Act, 1992 or regulation made thereunder; b. A Mutual Fund set up by a public sector bank or a public financial institution or authorised by the Reserve Bank of India and subject to certain notified conditions.

11. Income of Business Trust [Sec 10(23FC)]:

Any income of a business trust by way of a) interest received or receivable from a special purpose vehicle; or b) dividend referred to in sec. 115-O(7) “Special purpose vehicle” means an Indian company in which the business trust holds controlling interest and any specific percentage of shareholding or interest, as may be required by the regulations under which such trust is granted registration.

12. Income of Specified Boards [Sec. 10(29A)]:

Any income accruing or arising to The Coffee Board; The Rubber Board; The Tea Board; The Tobacco Board; The Marine Products Export Development Authority; The Coir Board; The Agricultural and Processed Food Products Export Development Authority and The Spices Board.

13. Subsidy Received From Tea Board [Sec. 10(30)]:

Any subsidy received from or through the Tea Board under any scheme for replantation or replacement of tea bushes or for rejuvenation or consolidation of areas used for cultivation of tea as the Central Government may specify, is exempt.

14. Awards and Rewards [Sec. 10(17A)].

Any payment made, whether in cash or in kind – a. in pursuance of any award instituted in the public interest by the Central Government or any State Government or by any other approved body; or b. as a reward by the Central Government or any State Government for approved purposes.

15. Income of Scientific Research Association [Sec. 10(21)]:

Any income of a scientific research association [being approved for the purpose of Sec. 35(1)(ii)] or research association which has its object, undertaking research in social science or statistical research [being approved and notified for the purpose of Sec. 35(1)(iii)], is exempt provided such association— a. applies its income, or accumulates it for application, wholly and exclusively to the objects for which it is established; and b. invest or deposit its funds in specified investments.

16. Expenditure Related To Exempted Income [Sec. 14A]:

For the purposes of computing the total income, no deduction shall be allowed in respect of expenditure incurred by the assessee in relation to income, which does not form part of the total income under this Act. Where the AO is not satisfied with the correctness of the claim of such expenditure by assessee, he can determine the disallowable expenditure in accordance with the method prescribed by the CBDT.

Deductions under chapter VI A-

Basic Rules

2. Limit of deduction: The aggregate amount of deduction under chapter VIA cannot exceed Gross Total Income of the assessee excluding -

3. Deduction must be claimed: Deduction under chapter VIA shall be available only if the assessee claims for it.

4. Double deduction not permissible: Where deduction under any section of chapter VIA has been claimed then the same shall not qualify for deduction in any other section.

Deduction under Section 80C-

Applicable to: An Individual or a Hindu Undivided Family (whether resident or non-resident)

Condition to be satisfied: Assessee has made a deposit or an investment in any one or more of the listed items (as given below) during the previous year.

Various options under 80C:

Maximum Premium allowed is 20% of Sum Assured

2. Investment/Contribution in Public Provident Fund (PPF)

3. Investment in National Savings Certificate (NSC)- VIII or IX issue

4. Contribution for participating in the Unit-linked Insurance Plan (ULIP) of Unit Trust of India (UTI) or ULIP of LIC Mutual fund u/s 10(23D) formerly known as Dhanraksha 1989.

5. Sum paid to effect or keep in force a contract for notified annuity plan of the LIC or any other insurer.

6. Subscription to notified units of a specified Mutual fund u/s 10(23D)/ administrator or the specified company as referred in sec. 2 of UTI (ELSS, 2005).

7. Any sum paid as subscription to Home Loan Account Scheme or notified pension fund of the National Housing Bank.

8. Any sum paid as subscription to a notified deposit scheme of Public sector companies or Any authority constituted in India for the purpose of satisfying the need for housing accommodation or for the purpose of planning, development or improvement of cities, towns, villages or for both.

9. Repayment of Principal amount of Housing Loan.

10. Investment in Debentures/Equity shares of a Public Financial Institution.

11. Subscription to units of any mutual fund u/s 10(23D) provided amount of subscription to such units is subscribed only in the eligible issue of capital.

12. Investment as term deposit for a period of 5 years or more with a scheduled bank.

13. Notified Bonds issued by the National Bank for Agriculture and Rural Development (NABARD).

14. Senior Citizens Savings Scheme Rules, 2004.

15. 5 year time deposit in an account under the Post Office Time Deposit Rules, 1981.

Deductions only for Individuals:

Quantum of Deduction:

Deduction under this section shall be minimum of the following:

● Aggregate of the eligible contributions, expenditure or investments (discussed above)

● Rs 1,50,000

Deduction under Section 80CCC-

Contribution to Pension Fund of LIC or any other insurer

Applicable to: An individual (irrespective of residential status or citizenship of the individual)

Condition to be satisfied:

1. Amount paid under an annuity plan: During the previous year, assessee has paid or deposited a sum under an annuity plan of the Life Insurance Corporation of India (LIC) or any other insurer for receiving pension from the fund referred to in Sec. 10(23AAB).

2. Payment out of taxable income: The amount must be paid out of income which is chargeable to tax. However, it is not necessary that such income relates to current year.

Quantum of deduction

Minimum of the following -

a) Amount deposited; or

b) Rs 1,50,000 .

Other Points

a) Treatment of Interest or Bonus accrued: Interest or bonus accrued or credited as per the scheme to the assessee’s account shall not be eligible for deduction.

b) Withdrawal from such fund [Sec. 80CCC(2)]: Any amount received by the assessee or his nominee as pension; or on surrender of such annuity is taxable in the hands of recipient in the year of receipt.

Note: Interest or bonus received from such fund shall also be taxable.

c) Deduction u/s 80C [Sec.80CCC(3)]: Deduction u/s 80C will not be available for the amount paid or deposited and for which deduction has been claimed u/s 80CCC.

Deduction under Section 80CCD-

Contribution to Pension Fund of Central Government (New Pension System or Atal Pension Yojna).

Applicable to: An individual

Condition to be satisfied

During the previous years, the assessee has paid or deposited any amount in his account under a pension scheme notified by the Central Government (New Pension System and Atal Pension Yojna).

Quantum of Deduction

Deduction u/s 80CCD(1)

A. In case of salaried individual

Lower of the following Rs

● Amount so paid or deposited ***

● 10% of his salary in the previous year ***

***

Add: The whole of the contribution made by the employer to such

account to the maximum of 10% of his salary1 in the previous year. ***

Amount of Deduction ***

B. In case of other individual

Lower of the following

● Amount so paid or deposited

● 20% of his gross total income in the previous year

Additional Deduction u/s 80CCD(1B)

Lower of the following shall also be eligible for deduction Rs

● Contribution to the scheme by any individual [Other than amount

claimed and allowed as deduction u/s 80CCD(1)] ***

● Rs 50,000

*Salary means Basic + DA

Deduction under Section 80CCE-

The aggregate amount of deductions under section 80C, section 80CCC and section 80CCD [other than deduction in respect of employer’s contribution and additional deduction u/s 80CCD(1B)] shall not exceed Rs 1,50,000.

Deduction under Section 80D-

Medical Insurance Premium

Applicable to: An individual or an HUF (irrespective of residential status or citizenship)

Conditions to be satisfied

| ||

Nature of Payment | Expenditure for | Quantum of Deduction |

Medical Insurance Premium or Contribution to Central Govt Health Scheme or Preventive Health Check up | For Individual: Himself/ Herself or Spouse or dependent children

For HUF: Any member | Lower of : Amount actually spent, or Rs. 25,000 pa

(Where the person, for whom such premium (not for payment made for preventive health check up) is paid, is a senior citizen, then maximum limit of deduction shall be increased to Rs 50,000 instead of Rs 25,000) |

|

|

|

2. Individual/HUF | ||

Nature of Payment | Expenditure for | Quantum of Deduction |

Medical Insurance Premium or Preventive Health Check up | Parents (whether dependent or not) | Lower of : Amount actually spent, or Rs. 25,000 pa

(Where the person, for whom such premium (not for payment made for preventive health check up) is paid, is a senior citizen, then maximum limit of deduction shall be increased to Rs 50,000 instead of Rs 25,000) |

Note: The deduction for payment made for preventive health check up (for self, spouse, dependent children and parents) for category 1 & 2 does not exceed in the aggregate Rs 5,000 subject to overall limit of Rs 25,000/- or Rs 50,000/- | ||

3. Individual/HUF | ||

Nature of Payment | Expenditure for | Quantum of Deduction |

Amount paid on account of medical expenditure provided mediclaim insurance is not paid on the health of such person | Expenditure incurred for any of the following person who is a senior citizen: In case of Individual a. Himself/herself, spouse; or b. dependent children; or c. Either or both of the parents In case of HUF Any member of the family | Lower of : Medical Expenditure incurred, or Rs. 50,000 pa |

2. Mode of payment: The premium or medical expenditure must be paid by any mode other than cash. However, payment shall be made by any mode, including cash, in respect of any sum paid on account of preventive health check-up.

Deduction under Section 80E-

Interest on Educational Loan

Applicable to: An Individual (irrespective of residential status and citizenship of the individual).

Conditions to be satisfied

1. Loan from specified institution: The assessee had taken a loan from -

2. Purpose of loan: The loan must have been taken for the purpose of pursuing higher education of himself/herself or for any other following persons:

a. Spouse

b. Children (dependent or not); or

c. the student for whom the individual is the legal guardian

“Higher education” means any course of study pursued after passing the Senior Secondary Examination or its equivalent from any school, board or university recognised by the Central Government or State Government or local authority or by any other authority authorised by the Central Government or State Government or local authority to do so

3. Payment of interest: The assessee pays interest on such loan.

Quantum of deduction: Amount paid during the year by way of payment of interest.

Maximum permissible period for which deduction is available

Deduction under this section shall be allowed for the initial assessment year and 7 assessment years immediately succeeding the initial assessment year* or until interest is paid by the assessee in full, whichever is earlier.

*Initial Assessment Year means the assessment year relevant to the previous year, in which the assessee starts repaying the loan or interest thereon.

Taxpoint

■ The deduction is available for a maximum period of 8 consecutive years.

■ The period starts from the year in which the assessee starts paying the interest on such loan.

Deduction under Section 80DD & Section 80 U

Deduction in respect of Handicapped/Disabled Person

Applicable to: A resident individual (irrespective of citizenship) or a resident HUF

Section 80DD Maintenance of Dependent Disabled Relative | Section 80U Deduction for Disabled Assessee |

| |

Dependent Relative of Assessee | Assessee himself |

Relative means: Individual- Spouse, children, parents, brothers and sisters of the individual HUF – Any member of HUF |

|

2. Condition | |

1. Assessee incurred medical expenses and other expenses for maintenance of Disabled relative. 2. Medical Certificate is furnished with return of income | - |

3. Quantum of Deduction- Same for 80DD & 80U | |

Disability from 40% to 79% - Rs 75,000 Disability of 80% and above(Severe Disability) - Rs 1,25,000

Note: Deduction under section 80DD is irrespective of the amount spent on maintenance of disable dependent relative. | |

Deduction under Section 80TTA-

Applicable to: An individual (other than senior citizen covered u/s 80TTB) or a Hindu Undivided Family.

Conditions to be satisfied

Gross total income of an assessee includes any income by way of interest on deposits (not being time deposits) in a savings account with:

Quantum of deduction

Minimum of the following

a. Interest on such deposits in saving account

b. Rs 10,000

Note: As per Notification No. 32/2011 dated 03-06-2011, interest on Post Office Saving Bank is exempt u/s 10(15(i) to the extent of the interest of Rs 3,500 (in case of single account) and Rs 7,000 (in case of joint account)

Deduction under Section 80TTB-

Applicable to: Senior Citizen

Conditions to be satisfied

Gross total income of an assessee includes any income by way of interest on deposits (not being time deposits) in a savings account with:

Quantum of deduction

Minimum of the following

a. Interest on such deposits in saving account

b. Rs 50,000

Note: Where such income is derived from any deposit held by, or on behalf of, a firm, an association of persons or a body of individuals, no deduction shall be allowed.

Key Takeaways:

References: