UNIT I

Introduction to Management Accounting

Meaning of Management Accounting:

The term management accounting consists of two phrases, "management" and "accounting". It is a study of the management aspects of accounting. This is a tool in the hands of management to make decisions. The focus of management accounting is to redesign accounting in a way that helps managers formulate policies and control their execution.

Management accounting has a recent origin. The term was first used in 1950 by a team of accountants who visited the United States under the auspices of the British-American Council on Productivity. The costing term did not mention the term "management accounting" before this research group visited. Fierce competition, large-scale production, dynamic development of technology, and the complexity of modern business have led to the development of management accounting-to solve many problems. Management accounting provides management with information to use as a basis for decision making.

J. Bati is used to describe management accounting as "accounting methods, systems, and techniques that, combined with special knowledge and capabilities, support management's mission to maximize profits or minimize losses. It is defined as "term".

Nature of Management Accounting

Management accounting is the latest division of accounting, but it may be considered partly science and partly art. It is the science of "quantification and summarization" of accounting data and the art of "interpretation".

Management accounting draws conclusions through the collection, processing, and objective analysis of data. Therefore, it relies on "progress and problem objectification and quantification". From this point of view, management accounting can be regarded as science.

However, management accounting also includes human judgment, impulses, whims, and prejudices, as evidenced by the inferences and conclusions drawn from the interpretation and analysis of data. The deduction must not be exactly scientific. The management accountant's personal judgment can have a significant impact on interpretation and deductions. From this point of view, management accounting can be regarded as an art.

As with all other social sciences, we can conclude that management accounting is partly science and partly art.

Characteristics of Management Accounting:

The purpose of management accounting is to record, analyze and present financial data to management. This helps you plan and execute your business systematically and effectively. The main features of management accounting are as follows.

(1) Provision of financial information: The main focus of management accounting is to provide management with financial information. Information is provided in a manner suitable for different levels of management for policy review and decision making.

(2) Analysis of cause and effect: Financial accounting is limited to displaying the income statement and balance sheet. Management accounting analyzes the causes and effects of the facts and numbers. If there is a loss, the cause of the loss is investigated. If there is a profit, the variables that affect the profit are also analyzed. Compare your profits with spending, sales, capital used, etc. and draw appropriate conclusions about the impact of these items on your profits.

(3) Use of special techniques and concepts: Controlling makes accounting data more useful and manageable using special techniques such as standard costing, budgeting, marginal costing, cash flows, cash flows, ratio analysis, and liability accounting. Each of these techniques or concepts is a tool that serves a specific purpose, such as analysing and interpreting data or establishing control over operations.

(4) Use of special techniques and concepts: Management accounting uses special techniques such as standard cost accounting, budget management, marginal cost accounting, cash flow, cash flow, ratio analysis, and liability accounting to collect accounting data. It is more useful and useful for management. .. Each of these techniques or concepts is a tool that serves a specific purpose, such as analyzing and interpreting data or establishing control over operations.

(4) Decision-making: The main purpose of management accounting is to provide relevant information to management and make various important decisions. Historical information provides the basis for predicting future impacts, developing alternatives, and making decisions to select the most beneficial course of action.

(5) There is no set practice: Financial accounting has various established principles and rules in the creation of financial accounting. There are no such fixed rules in management accounting. The tools or techniques applied by management accounting are the same, but the application of these techniques varies from concern to concern and situation to situation.

The interpretation of the analysed data depends on the person who uses it. The conclusions drawn from the application of the method depend on the intelligence and experience of the management account. The presentation of information depends on the requirements of your concern. All concern was applying the technology to meet that need.

(6) Achievement of purpose: Management accounting helps you achieve your company's goals. Based on historical information, adjust for future changes in predicates and set goals. The actual performance is recorded. A comparison is made between the actual result and the given result. If the performance deviates from the prescribed result, corrective action will be taken to achieve the predicted purpose. This is possible with the help of standard costing and budgetary management accounting techniques.

(7) Improvement of efficiency: The purpose of accounting is to provide information to improve efficiency. You can improve departmental or departmental efficiency by fixing goals or goals for a specific time period. Compare the actual performance with the target performance. The positive deviation is reviewed. Negative deviations are investigated to determine the cause. The methods and means of addressing the cause are analysed and the goal is achieved. The process of modifying and achieving goals leads to a gradual improvement in overall efficiency.

(8) Forecast: Management accounting is involved in decision making for future implementations. This includes future forecasts and forecasts. This helps you plan and set goals.

(9) Providing information, not decisions: Management accounting provides financial information, not decisions. Therefore, management accounting is said to depend on management efficiency in utilizing information and making effective decisions.

Scope of Management Accounting

The management accountant provides management with information related to business operations, both financial and non-financial. It is useful for short-term and long-term decisions. They require accounting knowledge and other studies such as management, industrial engineering, strategic management, and business economics in work and reporting.

The scope of management accounting is to support the following:

- Effective performance measurement

- Cost management

- Budget plan

- Pricing, and

- Decision making by management.

The management accountant uses historical data and quotes to provide information. This helps you perform your day-to-day operations, plan your future operations, and develop your overall business strategy.

Duties of management accountant

The scope of duties of a management accountant depends on the needs of management. Here, we will explain five of them.

- Capital budget

- Product costing

- Margin analysis

- Constraint analysis

- Trend analysis

Capital budget

Management accounting uses some standard capital budget measures for decision making. The internal rate of return (IRR) and net present value (NPV) methods are two examples. These methods help you make long-term investment decisions such as buying new machines, replacing old machines, new factories, or acquiring companies. Usually, the management accountant reviews the proposal, decides if it is the best investment option, and finds the right way to fund the purchase. It also outlines revenue and timeframes so management can predict future economic returns.

To determine the source of investment funds, you need to create details about each source (debt, capital, or retained earnings). In addition, the management objectives of the capital structure are important considerations in deciding on appropriate financing.

Product costing

The management accountant determines the actual cost of the product or service. Costs fall into several groups, including variable costs, fixed costs, direct costs, and overhead costs. You then calculate these costs and assign them to your products using several methods, such as full costing or variable costing.

Product costing is essential for planning different business strategies. Management uses this information to make product pricing and promotional budget decisions.

Margin analysis

Margin analysis includes analysis of additional profits from increased production. In this case, the management accountant determines the best point between production, sales, revenue, and profit.

You may use break-even analysis to calculate the contribution margin of your sales structure. Its purpose is to determine the amount of units whose revenue is equal to its cost. This information will help you determine the price of your product or service.

Constraint analysis

The management accountant analyses the constraints that can occur in the operation of the company, from the production process to sales. Then identify the cause of the problem and calculate its impact on your company's revenue, profits, and cash flow. Since various fields are involved, technical knowledge is required.

Trend analysis

This includes reviewing operational cost trends and investigating anomalous variants or deviations. Accountants use the information from the previous period to calculate and forecast future financial and operational information, including:

- Selling price

- Sales volume

- Advertising budget

- Get Capital investment

- Cash flow

Objectives and Functions of Management Accounting:

The main purpose of management accounting is to enable managers to perform their functions efficiently. The main functions of management are planning, organization, direction, and control. Management accounting helps managers perform these functions effectively.

(1) Presentation of data: Traditional income statements and balance sheets are not decision-making analyses. Controlling modifies and rearranges data according to the decision-making requirements of various methods.

(2) Support for planning and forecasting: Controlling helps you manage your planning process through budgetary and standard costing techniques. Forecasting is widely used in budgeting and setting standards.

(3) Help with organizing: Organization is related to the establishment of relationships between various individuals within a company. This includes delegating authority and modifying responsibilities. Management accounting aims to help managers organize through the establishment of cost centers, profit centers, responsibility centers, budget reserves and more. AH These activities help set up an effective organizational framework.

(4) Decision making: Management accounting provides comparative data for analysis and interpretation for effective decision making and policy making.

(5) Report to managers at various levels: One of the main objectives of management accounting is to keep management informed about the performance, plan compliance, and progress of different sections of the organization. Top management needs feedback on its planning policies and program implementation. Even mid-career executives and junior executives need data for day-to-day operational decisions. Management accountants create regular and frequent reports and send them in time to meet the needs of managers at all levels.

(6) Communication of management policy: Management accounting effectively communicates management policies to individuals for proper implementation.

(7) Effective management: Standard costing and budgeting are an integral part of management accounting. These techniques set goals, compare budgets with real-world will criteria, evaluate performance, and control deviations.

(8) Incorporation of non-financial information: Management accounting considers both financial and non-financial information to develop alternative behavioral policies that lead to effective and accurate decision making.

(9) Adjustment: The goals of the various departments are communicated to them, and their performance is sometimes reported to management. This ongoing report helps management coordinate various activities to improve overall performance.

(10) Motivate employees: Budgets, standards, and other programmers are actually implemented by employees. The main purpose of management accounting is to set goals in the form of budgets, standards, and programmers in a way that encourages employees to reach them. This is usually achieved by making goals feasible and providing appropriate financial and non-monetary incentives to achieve them.

Limitations of Management Accounting:

Like other areas, management accounting has its own limitations. It is considered an essential tool for business decision making, but its recent origins and some external factors limit its effectiveness. These factors are explained below.

(1) Reliance on basic records: Management accounting rarely maintains basic and key records of operations, expenses, and income. It gets all primary data from financial accounting, costing, and other related records. Therefore, the accuracy and reliability of the conclusions drawn by Management Accounting is limited by the reliability of its data source, and is plagued by some limitations of financial accounting and costing.

(2) Personal bias: The analysis and interpretation of financial information depends on the capabilities of the analyst and interpreter. Some areas of management accounting require the use of personal judgment and discretion. An individual's personal "prejudice" and "bias" can affect the objectivity and effectiveness of conclusions and recommendations.

(3) Management accounting is just a tool: Management accounting cannot be considered an alternative or alternative to management. The management accountant acts as an advisor and facilitator for management decision making. Actual decisions, their implementation and follow-up actions are a privilege of management.

(4) Management accounting provides only data: The main function of management accounting is to provide data to management in the form of "alternatives". Management can make the right choices, or even discard them all. Therefore, management accounting "only gives notice, cannot prescribe."

(5) Wide range: The scope of management accounting is very broad and extensively based. We use information from a variety of disciplines such as financial accounting, economics, statistics, costing, and engineering. Consider the financial and non-monetary transactions of the company. The limits of knowledge and experience of managed accountants in these diverse disciplines can compromise the reliability and reliability of data.

(6) Resistance to change: The introduction of management accounting involves setting up an organization and fundamental changes to traditional accounting practices. Stakeholders are convinced of the need for such changes and can resist such changes unless they are convinced.

(7) Costly to install: The introduction of management accounting can be very costly due to the elaborate organization and numerous changes in procedures, formats and rules required. As a result, SMEs may not be able to afford the cost. Only large organizations can afford to maintain and assist management accounting as a department.

(8) Evolutionary stage: Management accents have a recent academic origin and are still in development. Therefore, the concept is fluid, the technology is still evolving, and the analytical tools are incomplete. There are some experts who are sceptical about the usefulness of management accounting because of such important restrictions.

Most of the above limitations can be overcome with decisive efforts on the part of management and skilled management accountants.

Importance of Management Accounting:

Management accounting has immeasurable value and usefulness for the management of any company, and has been considered essential, especially for large organizations with complex management tasks. The importance of management accounting can be listed below.

(1) Improvement of efficiency: Management accounting greatly contributes to improving the operational efficiency of a company. Budgets, standards, reports, etc. usually increase the level of performance.

(2) Effective planning: Through the "decision-making data" provided by management accounting, policy development and operational planning become more effective.

(3) Performance evaluation: Performance evaluation of employees, departments, etc. is facilitated by management accounting based on difference analysis and management ratio.

(4) Maximizing profits: Management accounting helps in profit planning to pursue profit-optimizing decisions.

(5) Reliability: Tools used in management accounting typically make the data provided for management accurate and reliable.

(6) Elimination of waste: Standard costs, budgets, cost control methods, etc. contribute to the elimination of waste and the production of defective products.

(7) Effective communication: Regular and systematic reporting ensures a continuous flow of operational information to different levels of administrators.

(8) Employee morale: Employee morale can be created and maintained through achievable standards, practical budgets, and incentive schemes.

9) Management and coordination: Managing costs and adjustments in efforts in different segments of your organization can be achieved through performance reports, variance analysis, follow-up actions, and more.

The greatest advantage of management accounting is its advisory role in helping managers makes the best possible decisions on a daily basis on everyday issues and important policy issues.

The tools and techniques used in Management Accounting are described below:

(1) Financial policy and accounting: All business concerns are planned for their sources of funding. The use of a particular source of funding depends on the service costs of that source of funding, the terms of repayment in the case of borrowing, and so on. The amount of stock capital raised and the legal definition of repayment will be taken into account. The capital structure, that is, the ratio of equity capital to borrowings, must be determined to have an optimal capital structure. Management accounting provides a capital budgeting method for financial planning.

(2) Analysis of financial statements: Analyzing financial statements is a means of classifying and presenting data in a way that is useful to management. The importance of the information provided is explained in non-technical languages in the form of ratio analysis, cash flow, and cash flow methods.

(3) Acquisition cost accounting: Expenses are recorded after they are incurred to compare with a given goal to assess performance.

(4) Budget management: Budgets are used as a tool for planning and management. Expenditures and income are predetermined. Performance is compared to the budget, revealing deviations and who is responsible for them. Corrective actions will be initiated to eliminate future negative deviations.

(5) Standard costing: In standard costing, systematic analysis predetermines costs. The actual cost is compared to the standard. Analyse the differences to identify the cause and take steps to eliminate the differences and increase efficiency. Standard costing is commonly used in conjunction with budgetary control to effectively manage operations.

(6) Marginal cost: At marginal cost, product costs are divided into fixed and variable parts. Variable costs are used for decision making, but fixed costs are treated as period costs charged in the income statement. Marginal costs help management make a variety of important decisions.

(7) Other tools for management accounting are as follows.

(A) Decision accounting: Here, alternatives are evaluated for choice in the decision-making situation.

(B) Revaluation accounting: This applies to the exchange of fixed assets whose prices rise over time. Here we are addressing the impact of inflation on fixed assets.

(C) Management accounting: Controlled accounting uses internal checks, internal audits and statutory audits.

(8) Management information system: An important function of management accounting is reporting. This feature has been improved in consideration with the development of electronic data processing systems. In modern enterprises, the process of making information available for management is integrated and computer-based, known as the "Management Information System" (MIS).

6. Installation of management accounting system: Installing the Controlling System involves the following steps:

(1) Organization manual: The first step is to prepare your organization's manual. This manual clearly demonstrates the obligations and responsibilities of managers at each level and the horizontal and vertical relationships between key personnel.

(2) Creating various forms and reports: The second step in the installation process is to design the execution of various reports. The purpose is to minimize and simplify their underscores to avoid "bureaucratization".

(3) Necessary staffing: You need to hire and train the staff needed to deploy the system.

(4) Account classification: Treasury and cost accounts should be categorized, limited, and integrated as much as possible to meet management accounting requirements.

(5) Establishment of cost center: Investment centers, profit centers, cost centers, and budget centers must be clearly configured to collect and analyze information in their respective contexts.

(6) Introduction of management accounting method: Various methods of management accounting are introduced based on the needs and feasibility of the company.

(7) Provision of usage of "operations research" (O.R) method: As businesses operate in a changing economic, political and social environment, they face new challenges every day.

7. Management accounting organization: The organization of the management accounting system depends on the scale of business, the nature of the business, the nature of the organization, and so on. A minor concern is that the Treasurer is directly under the owner. A major concern is that management accounting may be assigned to financial managers.

Concerns about establishing a department will have a different management organization. The role of management accountant is emphasized by Anderson, and Schmidt management accounting is of particular concern. When it comes to the issue of collaboration with everything else, no other functional element across the organization has the necessary relationships with so many different departments.

Management accounts relate to different levels of managers, supervisors, and operators in all sections of business operations.

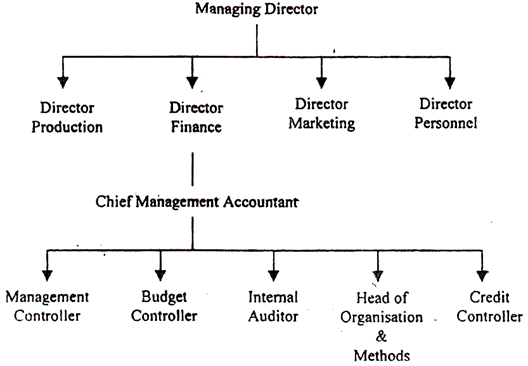

An organizational chart for a large-scale concern is given below:

In the organizational chart, the director's finances are placed above the Chief Accountant. All functions such as budgeting, auditing, O & M, and credit management are under the control of the Chief Accountant.

Role of Accounting: Management Accounting Vs. Financial Accounting

What is financial accounting?

Financial accounting is the accounting department involved in summarizing, recording, and reporting financial transactions that arise from business concerns over a period of time. Financial accounting is used to create various financial statements that companies can use to show financial performance to different users of financial information such as creditors, investors, customers, and suppliers.

What is Management accounting?

Management accounting is the latest division of accounting, but it may be considered partly science and partly art. It is the science of "quantification and summarization" of accounting data and the art of "interpretation".

Management accounting draws conclusions through the collection, processing, and objective analysis of data. Therefore, it relies on "progress and problem objectification and quantification". From this point of view, management accounting can be regarded as science.

However, management accounting also includes human judgment, impulses, whims, and prejudices, as evidenced by the inferences and conclusions drawn from the interpretation and analysis of data. The deduction must not be exactly scientific. The management accountant's personal judgment can have a significant impact on interpretation and deductions. From this point of view, management accounting can be regarded as an art.

Points of Difference | Financial Accounting | Management Accounting |

Aim | The main purpose is to provide information to outside parties. External parties include creditors, investors and customers. Therefore, it is primarily intended to help investors make informed decisions.

| Here, the purpose is different from financial accounting. Management accounting information is generally intended for management to make informed business decisions. |

Regulatory requirements | This is a mandatory requirement for all public authorities by the government. Therefore, they are governed by the Accounting Standards Board, the Companies Act and the Government.

| It is at the discretion of the management. There are no mandatory requirements, but institutions such as CIMA and ICWAI still offer several frameworks and formats. |

Governing principles | Financial accounting reports are based on generally accepted accounting principles (GAAP). This GAAP depends on countries that have more or less the same functionality.

| There is no standard basis for preparing a management accounting report. Therefore, they are created based on the requirements of the management team. |

Time horizon | The period of financial accounting is "past". Usually one fiscal year. | There is no specific period, but the main focus is on the future. |

Reporting beneficiaries | It is prepared for external or external parties. External parties such as shareholders, suppliers, customers, governments and banks. | Reports produced under management accounting are useful to insiders such as CEOs, directors, promoters, and senior management. |

Outputs | The financial accounting report consists of an income statement, a balance sheet, and a cash flow statement.

| Controlling reports are monthly, weekly, or yearly analysis of products, regions, features, and so on. |

Relevance and precision of data | Financial accounting data is 100% verifiable and accurate. Therefore, everything has evidence to support it. | Management accounting data is not always 100% verifiable. Therefore, the data must be relevant, timely, and logical. For example, no one can fully predict sales. |

Independent audit | In most countries, independent audits of financial accounting reports are required. For example, in the United States, certified accountants perform such audits, and in India, certified accountants (CAs) carry out such audits. | There are no special requirements for independent audits. However, management can take the initiative in conducting independent audits at its discretion for efficient and effective management. |

Confidentiality | The financial accounting report is a publicly available report and is for the general public. Therefore, there are no confidentiality issues. | Management accounting statements are for management purposes, and the confidentiality of the statement is an important concern. That's because they contain business secrets. |

Segment reporting | It has to do with the whole business and is an end in itself. Therefore, some accounting standards in some countries require companies to produce segment reports in a defined format. | On the other hand, it pertains to a particular area or segment for their analysis. Therefore, a segment can be a product line, region, manufacturing unit, and so on. |

Perspective | It has a historical perspective. | It has a futuristic perspective. |

Nature of information input | The information required for a financial accounting report is financial in nature. | Both financial and non-financial information is used to create Controlling reports. |

References:

- Https://openstax.org/books/principles-managerial-accounting/pages/1-2-distinguish-between-financial-and-managerial-accounting#:~:text=Managerial%20accountants%20regularly%20calculate%20and,reporting%20what%20has%20already%20happened.

- Https://en.wikipedia.org/wiki/Management_accounting

- Https://accountlearning.com/tools-and-techniques-of-management-accounting/

Books:

Cost Accountant: Thomson Reuters. 2011. Retrieved November 12, 2011.

Institute of Management Accounting Archived 2007-12-07 at the Wayback Machine