UNIT I

Accounting Standards issued by ICAI and Inventory Valuation

Concepts:

We know that generally accepted accounting principles (GAAP) aim to bring uniformity and comparability to financial statements. In many places, you'll see that GAAP allows different alternative accounting treatments for an equivalent item. For instance, different stock valuations end in different financial statements.

Such practices can lead the intended user within the wrong direction when making decisions associated with his or her field. Given the issues faced by many accounting users, the necessity to develop common accounting standards has increased.

To this end, the Institute of Chartered Accountants of India (ICAI), which is additionally a member of the International Accounting Standards Committee (IASC), formed the Accounting Standards Committee (ASB) in 1977. ASB needed accounting. After detailed investigation and discussion, a draft was prepared and submitted to ICAI. After proper review, ICAI finalized them and notified them of their use within the financial statements.

Meaning of Accounting Standards:

Accounting standards are written statements consisting of rules and guidelines issued by accounting institutions for the preparation of unified and consistent financial statements and other disclosures that affect different users of accounting information. Is.

Accounting standards set the conditions for accounting policies and practices with codes, guidelines, and adjustments that facilitate the interpretation of things contained in financial statements and even their handling within the books.

Nature of Accounting Standards:

Based on the discussion above, accounting standards are often said to be guides, dictators, service providers, and harmonizers within the field of accounting processes.

(I) Useful as A Guide to Accountants:

Accounting standards serve accountants as a guide to the accounting process. They supply the idea for the account to be prepared. For instance, they supply how to value inventory.

(II) Act as a Dictator:

Accounting standards act as a dictator within the field of accounting. In some areas, like dictators, accountants haven't any choice but to settle on practices aside from those listed in accounting standards. For instance, the income statement must be prepared within the format specified by accounting standards.

(III) Act as a Service Provider:

Accounting standards constitute the scope of accounting by defining specific terms, presenting accounting issues, specifying standards, and explaining numerous disclosures and implementation dates. Therefore, accounting standards are descriptive in nature and act as a service provider.

(IV) Functions as a Harmonizer.

There is no bias in accounting standards and there's uniformity in accounting methods. They remove the consequences of varied accounting practices and policies. Accounting standards often develop and supply solutions to specific accounting problems. Therefore, whenever there's a contradiction within the accounting problem, it's clear that the accounting principle acts as a harmonizer and facilitates the accountant's solution.

Purpose of Accounting Standards:

Previously, accounting was wont to record business transactions of a financial nature. Currently, its main focus is on providing accounting information during the decision-making process.

Accounting Standards are required for the following purposes:

(I) To bring Unity to Accounting Methods:

Accounting standards brings equality to accounting methods by proposing standard treatments for accounting issues. For example, AS-6 (revised edition) describes depreciation accounting methods.

(II) To improve the Reliability of Financial Statements:

Accounting is the language of business. The information provided by accountants is often based solely on the information contained in the financial statements, and many users make various decisions about their field. In this regard, financial statements need to provide a true and fair view of business concerns. Accounting standards bring credibility and credibility to different users.

They also help potential users of the information contained in financial statements with disclosure standards that make it easier for even the layperson to interpret the data. Accounting standards provide a concrete theoretical basis for the accounting process. They provide accounting uniformity, make financial statements for different business units comparable in different years, and again facilitate decision making.

(III) Simplify Accounting Information:

Accounting standards prevent users from reaching misleading conclusions and make financial data easy for everyone. For example, AS-3 (revised edition) clearly classifies cash flows in terms of "sales activities," "investment activities," and "finance activities."

(IV) Prevent fraud and manipulation:

Accounting standards prevent management from manipulating data. By systematizing accounting methods, fraud and operations can be minimized.

(V) Assist Auditors:

Accounting standards set the conditions for accounting policies and practices with codes, guidelines, and adjustments for creating and interpreting the items that appear in financial statements. Therefore, these terms, policies, guidelines, etc. are the basis for auditing the books.

The Characteristics of Accounting Standards:

Classification of Companies

Companies are distinguished and labelled as Level I, Level II, and Level III companies. Accounting standards apply to companies supported this classification and therefore the categories to which they apply.

Level I company

Companies that fall under one or more of the subsequent categories are called Level I companies.

- Companies with listed stock or debt securities, whether in or outside India

- Companies listed on equity or debt securities. Board resolution must be available as evidence Banks, including co-operative banks

- Financial organization

- Companies running insurance business

- All commercial, industrial, and business reporting companies with sales in more than Rs that don't include “other income” within the immediately preceding accounting period supported audited financial statements 50 crore.

- All commercial, industrial, and business reporting companies that borrow quite Rs, including public deposits. 10 chlores at any time during the accounting period

- Any of the above holding companies and subsidiaries at any time during the accounting period

Level II Enterprise

Companies that fall under one or more of the subsequent categories are called Level II companies.

- All commercial, industrial, and business reporting companies whose sales (excluding “other income”) within the last accounting period supported audited financial statements exceed rupees. 400,000 rupees but Rs 5 billion

- All commercial, industrial, and business reporting companies that hold borrowings, including public deposits, have larger Rs. 100 million rupees, but rupees. 10 crores at any time during the accounting period

- Any of the above holding companies and subsidiaries at any time during the accounting period

Level III Companies:

Companies that don't fall into Level I and Level II are considered Level III companies.

Applicability of Accounting Standards

Accounting Standard | Level I | Level II | Level III |

AS 1 Disclosure of Accounting Principles | Yes | Yes | Yes |

AS 2 Valuation of Inventories | Yes | Yes | Yes |

AS 3 Cash Flow Statements | Yes | No | No |

AS 4 Contingencies and Events Occurring after the Balance Sheet Date | Yes | Yes | Yes |

AS 5 Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies | Yes | Yes | Yes |

|

|

|

|

AS 7 Construction Contracts (Revised 2002) | Yes | Yes | Yes |

AS 9 Revenue Recognition | Yes | Yes | Yes |

AS 10 Accounting for Fixed Assets | Yes | Yes | Yes |

AS 11 The Effects of Changes In Foreign Exchange Rates (Revised 2003) | Yes | Yes | Yes |

AS 12 Accounting for Government Grants | Yes | Yes | Yes |

AS 13 Accounting for Investments | Yes | Yes | Yes |

AS 14 Accounting for Amalgamations | Yes | Yes | Yes |

AS 15 Employee Benefits (Revised 2005) | Yes | Yes | Yes |

AS 16 Borrowing Costs | Yes | Yes | Yes |

AS 17 Segment Reporting | Yes | No | No |

AS 18 Related Party Disclosures | Yes | No | No |

AS 19 Leases | Yes | Partial | Partial |

AS 20 Earnings Per Share | Yes | Partial | Partial |

AS 21 Consolidated Financial Statements | Yes | No | No |

AS 22 Accounting for taxes on income | Yes | Yes | Yes |

AS 23 Accounting for Investments in Associates in Consolidated Financial Statements | Yes | No | No |

AS 24 Discontinuing Operations | Yes | No | No |

AS 25 Interim Financial Reporting | Yes | No | No |

AS 26 Intangible Assets | Yes | Yes | Yes |

AS 27 Financial Reporting of Interests in Joint Ventures | Yes | No | No |

AS 28 Impairment of Assets | Yes | Yes | Yes |

AS 29 Provisions, Contingent Liabilities and Contingent Assets | Yes | Partial | Partial |

International Financial Reporting Standards

The field of monetary reporting in India has seen significant changes over the last five years. As trade moves more and more across national borders, so do compliance and reporting requirements. It's becoming increasingly difficult to display an entity's financial statements in accordance with the reporting requirements of all countries during which it exists.

What is IFRS?

International Financial Reporting Standards (IFRS) is an accounting principle issued by the International Accounting Standards Board (IASB) with the aim of providing a standard accounting language for increasing the transparency of the presentation of monetary information.

What is the IASB?

The International Accounting Standards Board (IASB) is an independent body established in 2001 and is solely liable for establishing International Financial Reporting Standards (IFRS). It's a continuation of the International Accounting Standards Committee (IASC), which was previously given responsibility for establishing international accounting standards. The IASB is predicated in London. It also provides the Conceptual Framework for Financial Reporting, published in September 2010, to supply a conceptual understanding and foundation of accounting practices under IFRS.

Components of Monetary Statements under IFRS

A complete set of monetary statements prepared in accordance with IFRS ideally consists of:

- Statement of monetary position at the top of the amount – more commonly referred to as the “balance sheet”

- Earnings report and Other Comprehensive earnings report for the Year – Other comprehensive income includes profit and loss items that aren't recognized within the earnings report to suits other relevant criteria.

Both of those statements are often combined or displayed separately.

- Statement of Changes in Shareholders' Equity – This includes adjustments between the amounts displayed at the start and end of the year.

- Income statement for that period

- Budget notes – Includes summary of serious accounting policies and other explanatory information in accordance with them.

In the following scenarios, the financial statements may include a press release of monetary position for the previous period.

- When a corporation applies accounting policies retroactively.

- When a corporation retroactively adjusts an item during a budget. Or

- When a corporation reclassifies items in financial statements.

List of International Financial Reporting Standards (IFRS)

As already discussed, the quality issued by the IASB is named IFRS. However, its predecessor, the IASC, had already issued certain international standards called International Accounting Standards (IAS). These IAS were issued by the IASC between 1973 and 2001. Both IAS and IFRS are still valid. The standards are as follows:

Standard No. | Standard Title |

IFRS 1 | First-time Adoption of International Financial Reporting Standards |

IFRS 2 | Share-based Payment |

IFRS 3 | Business Combinations |

IFRS 4 | Insurance Contracts |

IFRS 5 | Non-current Assets Held for Sale and Discontinue Operations |

IFRS 6 | Exploration and Evaluation of Mineral Resources |

IFRS 7 | Financial Instruments: Disclosures |

IFRS 8 | Operating Segments |

IFRS 9 | Financial Instruments |

IFRS 10 | Consolidated Financial Statements |

IFRS 11 | Joint Arrangements |

IFRS 12 | Disclosure of Interests in Other Entities |

IFRS 13 | Fair Value Measurement |

IFRS 14 | Regulatory Deferral Accounts |

IFRS 15 | Revenue from Contracts with Customers |

IFRS 16 | Leases |

IFRS 17 | Insurance Contracts |

IAS 1 | Presentation of Financial Statements |

IAS 2 | Inventories |

IAS 7 | Statement of Cash Flows |

IAS 8 | Accounting Policies, Changes in Accounting Estimates and Errors |

IAS 10 | Events after the Reporting Period |

IAS 11 | Construction Contracts |

IAS 12 | Income Taxes |

IAS 16 | Property, Plant, and Equipment |

IAS 17 | Leases |

IAS 18 | Revenue |

IAS 19 | Employee Benefits |

IAS 20 | Accounting for Government Grants and Disclosure of Government Assistance |

IAS 21 | The Effects of Changes in Foreign Exchange Rates |

IAS 23 | Borrowing Costs |

IAS 24 | Related Party Disclosures |

IAS 26 | Accounting and Reporting by Retirement Benefit Plans |

IAS 27 | Separate Financial Statements |

IAS 28 | Investments in Associates and Joint Ventures |

IAS 29 | Financial Reporting in Hyperinflationary Economies |

IAS 32 | Financial Instruments: Presentation |

IAS 33 | Earnings per Share |

IAS 34 | Interim Financial Reporting |

IAS 36 | Impairment of Assets |

IAS 37 | Provisions, Contingent Liabilities, and Contingent Assets |

IAS 38 | Intangible Assets |

IAS 39 | Financial Instruments: Recognition and Measurement |

IAS 40 | Investment Property |

IAS 41 | Agriculture |

Key takeaways:

- Accounting may be a necessary function for deciding, cost planning, and economic performance measurement, no matter the dimensions of the business.

- Professional accountants follow a group of commonly accepted accounting principles (GAAP) when preparing financial statements.

- The Financial Accounting Standards Board (FASB) sets accounting rules for public and personal companies and non-profits within the us.

- The relevant organization, the Governmental Accounting Standards Board (GASB), sets the rules for state and local governments.

- In recent years, the FASB has worked with the International Accounting Standards Board (IASB) to establish compatible standards around the world.

- Accounting standards are a general set of principles, standards, and procedures that define the basis of financial accounting policies and practices.

- Accounting standards apply to the overall financial position of a company, including assets, owners, income, expenses and shareholders' equity.

- Banks, investors and regulators rely on accounting standards to ensure that information about a particular entity is appropriate and accurate.

- International Accounting Standards were replaced by International Financial Reporting Standards (IFRS) in 2001

- Currently, the United States, Japan and China are the only major capital markets with no IFRS obligations.

- Since 2002, US GAAP has been working with the Financial Accounting Standards Board to improve and integrate US GAAP and IFRS.

- Accounting standards have been introduced to improve the quality of financial information reported by companies.

- In the United States, the Financial Accounting Standards Board (FASB) issues generally accepted accounting principles (GAAP).

- GAAP is required for all companies listed in the United States. It is also routinely carried out by private companies.

- The FASB and IASB may work together to publish joint standards on hot topic issues, but for the time being the United States has no intention of switching to IFRS.

- GAAP is a set of generally accepted accounting principles, standards, and procedures that a company and its accountants must follow when preparing financial statements.

- IFRS is a set of international accounting standards that specify how certain types of transactions and other events are reported in financial statements.

- Some accountants consider the methodology to be the main difference between the two systems. GAAP is rule-based and IFRS is principle-based

Benefits:

Accounting is often regarded as the language of business because it conveys the financial position of a company to others. And the same is true here, just as all languages have specific syntax and grammatical rules. In the case of accounting, these rules are accounting standards (AS). They are the accounting and reporting rules and regulatory framework of a country. Let's look at the main purpose of forming these standards.

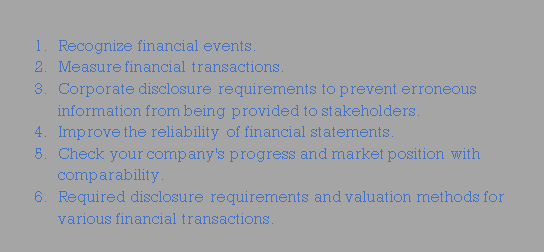

1. The main purpose is to improve the reliability of financial statements. This is because financial statements must be prepared according to standards that users can trust. They know that non-compliance with these standards can have serious consequences for a company.

2. Then there is comparability. By following these criteria, you can make inter-company and intra-company comparisons. This allows you to see the company's progress and its position in the market.

3. We also aim to provide a set of accounting policies that include the required disclosure requirements and various financial transaction valuation methods.

Objectives of Accounting Standards

Accounting is often regarded as the language of business because it conveys the financial position of a company to others. And the same is true here, just as all languages have specific syntax and grammatical rules. In the case of accounting, these rules are accounting standards (AS). They are the accounting and reporting rules and regulatory framework of a country. Let's look at the main purpose of forming these standards.

- The main purpose is to improve the reliability of financial statements. This is because financial statements must be prepared according to standards that users can trust. They know that non-compliance with these standards can have serious consequences for a company.

- Then there is comparability by following these criteria, you can make inter-company and intra-company comparisons. This allows you to see the company's progress and its position in the market.

- It also aims to provide a set of accounting policies that include the required disclosure requirements and various financial transaction valuation methods.

Advantages and Limitations of Accounting Standards

Benefits of AS

Accounting standards are the dominant authority in the accounting world. It ensures that the information provided to potential investors is by no means misleading. Let's take a look at the benefits of AS.

1] Achieve Accounting Unification

Accounting standards provide rules for standard handling and recording of transactions. There is even a standard format for financial statements. These are the steps to achieve a unified accounting method.

2] Improve the Reliability of Financial Statements

The company has many stakeholders, who rely on financial statements for information. Many of these stakeholders make decisions based on the data provided by these financial statements. And there are also potential investors who make investment decisions based on such financial statements.

Therefore, it is imperative that these statements provide a true and fair picture of the company's financial position. Accounting Standards (AS) guarantee this. They make sure that the statement is credible and credible.

3] Prevent Fraud and Accounting Operations

Accounting Standards (AS) set out the accounting principles and methodologies that all entities must follow. One of the consequences is that entity management cannot manipulate financial data. Following these criteria is mandatory, not optional.

Therefore, these standards make it difficult for management to misrepresent financial information. It makes it even harder for them to commit fraud.

4] Supports the Auditor

Currently, accounting standards set out all accounting policies, rules, regulations, etc. in writing. You must follow these policies. Therefore, if the auditor ensures that the policy is followed correctly, he can be confident that the financial statements are true and fair.

5] Comparability

This is another major purpose of accounting standard. All entities in a country follow the same set of criteria, which makes their financial accounting somewhat comparable. Users of financial statements can analyze and compare the financial performance of different companies before making decisions.

You can also compare two statements from the same company in different years. This shows the user the growth curve of the company.

6] Determination of Management Accountability

Accounting standards help measure a company's performance. This helps measure management's ability to increase profitability, maintain the company's solvency, and maintain management's other important financial obligations.

Management also needs to choose accounting policies wisely. Constant changes in accounting policies are confusing to users of these financial statements. It also loses the principles of consistency and comparability.

AS Limits

Accounting standards also have some restrictions. Regulators continue to update standards to limit these restrictions.

1] Difficulty in Choosing Choices

There are alternatives to certain accounting or valuations. For example, stocks can be valued using LIFO, FIFO, weighted average, and so on. Therefore, choosing from these options is a difficult decision for management. AS does not provide guidelines for proper selection.

2] Limited Range

Accounting standards cannot invalidate laws or statutes. They must be assembled within the laws prevailing at the time. It may limit their scope to provide the best policy for the situation.

Key takeaways:

- Accounting Standards (AS) are basic policy documents. Their main purpose is to ensure the transparency, reliability, consistency and comparability of financial statements.

- They do so by standardizing national / economic accounting policies and principles.

- Therefore, transactions of all companies are recorded in a similar manner if they comply with these accounting standards.

- These accounting standards (AS) are issued by accounting institutions or regulatory committees, or directly by governments.

- In India, Indian Accounting Standards are published by the Institute of Chartered Accountants of India (ICAI).

- Accounting is often regarded as the language of business because it conveys the financial position of a company to others.

- And the same is true here, just as all languages have specific syntax and grammatical rules. In the case of accounting, these rules are accounting standards (AS).

- They are the rules and regulatory framework for national accounting and reporting.

Procedures for issue of Accounting Standards Various AS:

Establishment of Accounting Standards Committee:

The Institute of Chartered Accountants of India recognized the need to reconcile the diverse accounting policies and practices currently in use in India and established the Accounting Standards Board (ASB) on April 21, 1977.

Scope and function of the Accounting Standards Board:

The main function of the ASB is to develop accounting standards and ensure that such standards are established by the Indian Institute Council. ASB takes into account applicable laws, customs, usage, and business environment when developing accounting standards.

The Institute is a member of the International Accounting Standards Committee (IASC) and agrees to support the purposes of the IASC. The ASB will take into account the international accounting standards issued by the IASC in developing its accounting standards and will endeavour to integrate them as much as possible in the light of the general circumstances and practices of India.

Accounting standards are issued under the authority of the Board. The ASB is also responsible for disseminating accounting standards and persuading stakeholders to adopt them in the preparation and presentation of financial statements.

The ASB issues guidance notes on accounting standards and describes the issues that arise from them. ASB also reviews accounting standards on a regular basis.

Accounting Standard Issuance Procedure:

Broadly speaking, the following steps are used to develop accounting standards:

- First, the ASB identifies areas where accounting standards may need to be developed.

- The ASB then forms research groups and panels to discuss and study the topic at hand. Such a panel prepares a draft of the standard. Drafts usually include definitions of important terms, the purpose of the criteria, their scope, measurement principles, and representation of the data in the financial statements.

- The ASB then conducts a deliberation on the above draft of the criteria. Changes and corrections will be made as needed.

- The draft will then be circulated to all relevant authorities. This typically includes members of the ICAI and relevant authorities such as the Ministry of Corporate Affairs (DCA), SEBI, CBDT, the State-owned Enterprise Standing Conference (SCPE), and the Comptroller and Auditorium of India. These members and departments are invited to give their comments.

- The ASB then arranges meetings with these representatives to discuss their views and concerns regarding the draft and its provisions.

- The Exposure Draft is then completed and made publicly available for review and comment.

- Review public comments on the Exposure Draft. A final draft is then prepared for ICAI review and review.

- The ICAI Council will then review and consider the final draft of the standard. We may suggest some changes as needed.

- Finally, accounting standards are issued. For non-corporates standards, ICAI issues the standards. Also, if the relevant subject matter relates to a business entity, the central government will issue the standard.

The draft standard proposed includes the following basic points:

- Statement of standards-related concepts and basic accounting principles.

- Definitions of terms used in the standard.

- How accounting principles were applied.

- Labelling and disclosure requirements to comply with the standard.

- The class of company to which the standard applies.

- The date on which the standard takes effect.

After considering the comments received, the draft of the proposed criteria will be finalized by the ASB and submitted to the institute's council.

The Institute's council will review the final draft of the proposed criteria and, if it deems it necessary, consult with ASB to revise the same. Accounting standards for relevant subjects are then issued under the authority of the council.

Accounting Standards by I.C.A.I

The following accounting reports should be considered.

) AS 01 – Disclosure of Accounting Policies.

B) AS 02 – Valuation of Inventories.

C) AS 09 – Revenue Recognition.

Key takeaways:

- The ASB shall determine the broad areas in which accounting standards need to be developed and the "priority" for their choices.

- In developing accounting standards, ASB is supported by research groups organized to consider specific subjects. In the formation of the study group, a wide range of participants such as research institute members will be possible.

- ASB also holds dialogues with representatives of government and public sector projects. Industry and other organizations to confirm their views.

- Based on the work of the study group and dialogue with the organization, an exposure draft of the proposed criteria will be prepared and published for comment by members of the institute and the general public.

AS – 1: Disclosure of Accounting Policies

Accounting Standard (1): Disclosure of Accounting Policy: -AS-1 is on priority. All types involved, such as sole proprietorship, company, AS – 1: Disclosure of Accounting Policies or company, must follow.

Meaning: -Accounting policy refers to specific accounting principles and the way in which they are applied in the preparation and presentation of financial statements (that is, final accounting).

(a) Purpose.

The purpose of disclosing accounting policies is to better and better understand the financial statements. All-important accounting policies should be disclosed in one place to help the reader understand the financial statements. The accounting policy statement is part of the financial statements.

(b) Areas of Policies.

At the time of final accounting preparation, there are many areas where multiple methods of accounting can be followed.

For example.

A) Depreciation Method: -

i) Fixed installment payment method.

Ii) WDV method.

B) Stock Valuation: -

i) FIFO.

Ii) Weighted average.

C) Handling of Expenditures during Construction: -

i) Written.

Ii) Capitalization.

Iii) Postponed.

Iv) Conversion of foreign currency items.

v) Investment valuation.

Vi) Handling of goodwill.

Vii) Handling of retirement benefits.

Viii) Handling of contingent liabilities.

(c) Disclosure of Policies.

In order to better and better understand the financial statements, you must disclose all important accounting policies that you follow in preparing the financial statements. The statement indicating the disclosure of accounting policies is part of the financial statements. We recommend that you disclose all your policies in one place for your understanding.

(d) Disclosure of Change in Policies.

There are changes from one period in the accounting policy to the next period during the preparation of the financial statements, and such changes affect the balance sheet and profit / loss A / c situation from the current period onward. If so, such changes must be disclosed in the financial statements.

Amounts that affect financial statements should be disclosed as much as possible.

Basic Accounting Assumptions: -No specific disclosure is required if you follow the basic accounting assumptions.

(e) Illustrations

a) Handling of spending during construction: -This means that concerns are going to continue the business in the future and there is no intention to close the business.

b) Consistency: -means that the same accounting policy is adhered to from one period to another.

c) Occurrence: -means that financial statements are prepared only in the commercial system. This means that revenues and costs are recorded when they are earned or incurred, not when they are received or paid for.

If you do not follow basic accounting assumptions, you will need to disclose the facts.

Key takeaways:

- Accounting Standard (1): Disclosure of Accounting Policy: -AS-1 is on priority. All

- The purpose of disclosing accounting policies is to better and better understand the financial statements.

- In order to better and better understand the financial statements, you must disclose all important accounting policies that you follow in preparing the financial statements.

- Basic Accounting Assumptions: -No specific disclosure is required if you follow the basic accounting assumptions.

AS – 2: Valuation of Inventories (Stock)

(a) Meaning, Definition.

The purpose of this standard is to formulate how to calculate the cost of a stock and to determine the closing price displayed on the balance sheet.

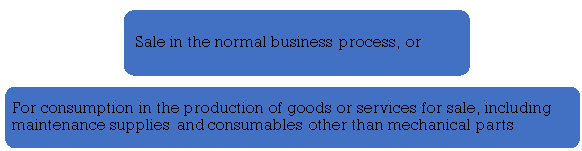

Definition: -AS-2 defines inventory as an asset.

a) Held for sale in the normal business process (finished product).

b) The production process of such sale (raw materials and work in process).

c) In the form of materials or supplies consumed in the production process or provision of services.

Valuation of Inventories

This standard must be applied to the accounting for all inventory except:

(a) Work in progress in the construction business, including directly related service contracts.

(b) Work in progress in the service business (consulting, banks, etc.)

(c) Shares, corporate bonds held as shares and other financial products.

(d) Inventories of livestock, agricultural and forestry products, mineral oils, etc. These inventories are valued at their net feasible value.

Definition

I. The inventory definition includes:

A. It is sold as a normal business, that is, as a finished product.

B. Products in production, that is, in progress.

C. Raw materials (including consumables) consumed during the production process or service provision.

II. Net Realizable Value (NRV):

"Net realizable value is the estimated selling price in a normal business process minus the estimated cost of completing the estimate and the estimated cost of selling."

Valuation of Inventories

Inventories should be valued at cost or net realizable value, whichever is lower. The procedure for valuing inventories is as follows. A. Determine the cost of inventory B. Determine the net realizable value of inventory C. When comparing cost and net realizable value, the lower of the two is considered the value of inventory. Comparisons can be made by item or by group of items. (See the case study at the end of the article) Let's take a closer look at the important items of inventory valuation.

A. Inventory Costs Inventory costs include:

i) Purchase cost

Ii) Conversion cost

Iii) Other costs incurred to return inventory to its current location and condition.

B. Purchase costs When determining purchase costs, you need to consider the following:

i) Inventory purchase costs include customs duties and taxes (excluding those that can be later collected by the tax authorities).

Ii) Inward cargo

Iii) other spending directly from the purchase

Iv) Trade discounts, rebates, tariff drawbacks, and other similar items will be deducted when determining purchase costs.

C. Conversion costs include all costs incurred during the manufacturing process to finish the raw material into a finished product. Conversion costs also include systematic allocation of fixed and variable overhead incurred by the enterprise during the production process. The categories of conversion costs are:

I. Direct cost

All costs directly related to the unit of production, such as direct labor

II. Fixed Overhead

Fixed overhead costs are overhead costs borne by the company regardless of production volume. These are costs that are kept relatively constant regardless of production volume, such as depreciation costs, building maintenance costs, and management costs.

Fixed production overhead allocation is based on the normal capacity of the production facility. These fixed overhead allocations do not result in increased production when production is low or when the plant is idle.

III. Variable Overhead Costs

Variable overhead costs are indirect production costs that change directly with production volume. These are costs incurred based on actual production, such as packaging and indirect labor. D. Other Costs All other costs incurred to bring inventory to its current location and condition. (Example) Design cost incurred for a specific customer's order. If there are by-products during the manufacture of the main product, their costs must be identified individually. If they cannot be identified individually, they can be assigned to the relative selling price of the main product and by-products. Some of the costs that should not be included are:

a. Abnormal waste costs

b. SG & A expenses when not required in the manufacturing process

c. Normal losses incurred during the manufacturing process are allocated to the remaining number of units, and extraordinary losses are treated as expenses.

(b) Applicability.

This standard should be applied to the accounting of inventories other than:

(A) Work in progress under construction contracts, including directly related service contracts (see)

Accounting Standard (AS) 7, Construction Contract);

(B) Work in progress that occurs during the normal business process of the service provider.

(C) Stocks, corporate bonds and other financial instruments traded as sk. And

(D) Inventories of livestock, agricultural and forestry products, mineral oil, ore and gas producers. It is measured at net realizable value according to established practices in these industries.

(c) Measurement of Inventory.

Stocks should be valued at lower cost and net realizable value.

Costs: -Inventory costs include:

a) Purchase cost.

b) Cost of conversion.

c) other costs incurred to return inventory to its current location and condition.

Net Realizable Value (NRV): -Means the estimated selling price in a normal business process minus the estimated cost of completing work in progress and the estimated cost of making a sale.

Purchase Costs: -Purchase costs include purchase prices, customs duties and taxes, inward freight, and other expenses directly attributable to the acquisition. Customs and tax reductions, trade discounts, rebates, and customs refund that companies can collect from tax authorities.

(d) Disclosure in Final Account.

Financial statements must disclose:

a) accounting policies adopted to measure inventory.

b) Cost formula used.

c) Inventory classification, that is, finished products, work in process, raw materials, etc.

Key takeaways:

- The purpose of this standard is to formulate how to calculate the cost of a stock and to determine the closing price displayed on the balance sheet.

- "Net realizable value is the estimated selling price in a normal business process minus the estimated cost of completing the estimate and the estimated cost of selling."

- Inventories should be valued at cost or net realizable value, whichever is lower.

- Fixed overhead costs are overhead costs borne by the company regardless of production volume.

- Variable overhead costs are indirect production costs that change directly with production volume.

AS – 9: Revenue Recognition

Revenue should be measured by the amount charged to the client for the sale of goods or services. However, for agency relationships, revenue should be measured in terms of what is charged as a commission, not the total inflow of cash, accounts receivable, or other consideration. There are some exceptions to the above statement to which special considerations apply:

a) Income from construction contracts

b) Revenue from rental purchases and rental contracts

c) Income from government grants and other similar grants

d) Insurance company revenue from insurance contracts

(a) Meaning and Scope.

Revenue means the total inflow of cash, receivables, or other consideration generated in the course of a company's normal activities, such as:

a) Sale of goods.

b) Service rendering.

c) Use of corporate resources by others, interest, dividends and royalties.

AS 9 Revenue Recognition Applicability

This standard was published by ICAI in 1985 and was recommended only to Level I companies for the first few years, but has been mandated by all other companies since April 1, 1993.

According to ICAI, "A company means a company as defined in Section 3 of the Companies Act 1956."

Level I companies are those with sales of more than 50 chlores in the previous fiscal year. Sales here do not include other income and apply to the holding company and its subsidiaries.

Description

a) Revenue recognition focuses on the timing of revenue recognition in a company's income statement

b) The amount of revenue generated from a transaction is usually determined by an agreement between the parties involved in the transaction.

c) If there are uncertainties regarding the determination of the amount or associated costs, these uncertainties can affect the timing of revenue.

Timing: -Revenue should be recognized at the time of sale of the service offer.

(b) Transactions excluded.

AS 9 does not apply to:

a) Income from construction contracts.

b) Revenue from employment, purchases and rental contracts.

c) Government grants and income from subsidies.

d) Insurer revenue from insurance contracts.

(c) Sale of Goods.

According to AS 9, revenue from the sale of goods is recorded when:

a) The seller has transferred ownership of the goods to the buyer at a price.

b) All significant risks and rewards of ownership have been transferred to the purchaser.

c) The seller does not retain effective control of ownership of the transferred goods.

d) There is no significant uncertainty in the collection of consideration.

(d) Rendering of Services.

Revenue from the service is recorded when the service is run. It is measured in two ways.

a) Completer Service Contract Method: -Revenue is recorded when the contract is completed, that is, when the service is completed.

b) Proper completion method: -Revenue is recorded proportionally, that is, in proportion to the degree of completion of the service under the contract.

(e) Effects of Uncertainties.

Revenues are recorded only if there are no significant uncertainties in the collection of consideration. Revenue recognition is whether the final collection is uncertain.

If there is uncertainty about the recovery of revenue after revenue recognition, it is better to prepare for the uncertainty of recovery

(f) Disclosure.

If revenue recognition is postponed, you must disclose the circumstances that require the postponement.

(g) Illustrations.

- During sale, the buyer gets the title and accepts the claim, but delivery is delayed at the buyer's request

-You need to recognize revenue even though the physical delivery has not been completed.

2. Delivery subject to installation and inspection

-You must not recognize revenue until the customer accepts the delivery and completes the installation and inspection. However, if the installation process is very simple, you need to be aware of your revenue. For example. TV sales may be set up.

3. Sale at the time of approval

-If the goods are officially accepted, rejected, or the time is uncertain, you must not recognize revenue until a reasonable amount of time has passed.

4. Sale under the condition of "refund if not completely satisfied"

-Although it may be appropriate to approve the sale, it may be appropriate to properly prepare for the return based on previous experience.

5. Consignment sales

-Revenue should not be recognized until the item is sold to a third party.

6. Installment sales

-Revenue at the sale price, excluding interest, should be recognized on the date of sale.

7. Special order and shipping

-Revenue from such sales should be recognized when the goods are identified and ready for delivery.

8. If the seller agrees to buy back the same item at a later date

-The sale should not be recognized as this is a monetary arrangement.

9. Subscriptions received for publication

-Revenues received or invoiced must be deferred and recognized in a straight-line manner over time. Alternatively, if the value of the item offered varies from period to period, the revenue should be based on the sales amount of the item offered.

10. I received an advertising fee

-Recognized when the ad is displayed before it is published.

11. The tuition fee received

-Must be recognized during the teaching period

12. Admission fee and membership fee

-Admission is usually capitalized

-If the membership fee only allows the membership fee and all other services or products are paid individually, the membership fee must be recognized upon receipt. If a membership fee qualifies a member for a service or publication provided during the year, it should be systematically and reasonably recognized, taking into account the timing and nature of all services.

13. Sale of show tickets

-You need to be aware of your revenue when an event occurs.

14. Guarantee of sales of agricultural products

-If the sale is guaranteed under a forward contract or government guarantee, the crop can be recognized at a net realizable value, although it does not meet the revenue recognition criteria.

Key takeaways:

- Revenue should be measured by the amount charged to the client for the sale of goods or services.

- According to ICAI, "A company means a company as defined in Section 3 of the Companies Act 1956."

- Revenue means the total inflow of cash, receivables, or other consideration generated in the course of a company's normal activities.

- Revenue from the service is recorded when the service is run.

- Level I companies are those with sales of more than 50 chlores in the previous fiscal year.

Inventory Valuation

Inventory, sometimes referred to as merchandise, refers to the merchandise or materials that a company holds to sell to its customers in the near future.

In other words, these goods and materials serve no other purpose in the business except that they are sold to customers for profit. They are not used to promote produce or business. The sole purpose of these liquid assets is to sell them to customers for profit, but just because an asset is sold does not mean that it is considered inventories. To determine if an asset needs to be accounted for as a commodity, you need to look at three key characteristics of inventory.

First, the assets need to be part of the company's core business. For example, sandwich store delivery trucks are not considered inventories because they have nothing to do with the main business of manufacturing and selling sandwiches. This is considered a sandwich store fixed asset. On the other hand, for car dealers, this truck is considered in stock because it is in the business of selling vehicles.

Second, the asset must be sellable, otherwise it will be immediately available for sale. If you were able to sell some of your business assets, but have never actually been able to sell them, they are not in stock. These are just assets or investments in the company.

Third, the purpose of owning assets must be to sell them to customers. Returning to the sandwich store example, the truck was not intended to be sold to customers. It was purchased to deliver sandwiches and sold when the job could not be accomplished. Car dealers, on the other hand, buy vehicles for resale only. Therefore, trucks are considered in stock for them.

Inventory Type

According to the definition of Inventory, there are different types of inventories, and each has a slightly different accounting treatment. Retailers usually have only one type of merchandise, called merchandise, so it's easiest to explain. We purchase it as a finished product from wholesalers and manufacturers and sell it to our customers.

Manufacturers, on the other hand, have a slightly different definition of inventory because they manufacture their own products for sale to their customers. Therefore, inventory must be considered at all stages of production. The three categories are raw materials, work in process, and finished products. Take a look at each of these categories at Ford's car factory.

Raw Materials – Raw materials are the building blocks of a finished product. Ford buys sheet metal, steel bars and tubes to manufacture car frames and other parts. When they put these materials into production and start cutting bars and forming metal, the raw materials are in process inventory.

Work in Process – Work in process inventory consists of all partially finished products manufactured by the manufacturer. An unfinished car goes down the assembly line and is considered an ongoing car until it is completed.

Finished Product – The finished product sounds exactly like that. These are finished products that can be sold to wholesalers, retailers and even end users. In the case of Ford, they are finished vehicles ready to be sent to the dealer.

Key takeaways:

- Inventory, sometimes referred to as merchandise, refers to the merchandise or materials that a company holds to sell to its customers in the near future.

- In other words, these goods and materials serve no other purpose in the business except that they are sold to customers for profit.

- According to the definition of Inventory, there are different types of inventories, and each has a slightly different accounting treatment.

Cost for Inventory Valuation

Each of these different categories is important and managing them is key to the survival of your business. Warehouse management is one of the most important concepts for any business, especially retailers. They buy goods from manufacturers and resell them to consumers with a small margin, so they need to control their purchases and control the amount of cash bound by the goods.

Inventory valuation is the cost associated with a company's inventory at the end of the reporting period. It forms an important part of cost of sales and can also be used as collateral for loans. This valuation appears as a current asset on the company's balance sheet. Inventory valuation is based on the costs companies incur to take inventory, transform it into a ready-to-sell state, and ship it to the right place of sale. Do not add management or sales costs to inventory costs. The costs that can be included in the inventory valuation are:

a) Direct labor,

b) Direct material,

c) Factory overhead,

d) Freight transportation,

e) Handling,

f) Import tax.

You may need to lower the inventory valuation to the market value of the inventory if it is lower than the recorded cost of the inventory, whichever is lower, the cost or the market rule. There are also very limited situations in which under International Financial Reporting Standards it is permitted to record the cost of inventory at market prices, regardless of the cost of manufacturing the inventory (usually limited to agricultural products).

Inventories must be valued at cost or market value (net realizable value), whichever is lower.

- Inventory valuation is the cost associated with a company's inventory at the end of the reporting period.

- It forms an important part of cost of sales and can also be used as collateral for loans.

- Inventory valuation is based on the costs companies incur to take inventory, transform it into a ready-to-sell state, and ship it to the right place of sale.

- There are also very limited situations in which under International Financial Reporting Standards it is permitted to record the cost of inventory at market prices, regardless of the cost of manufacturing the inventory (usually limited to agricultural products).

Key takeaways:

- Inventory at market prices, regardless of the cost of manufacturing the inventory (usually limited to agricultural products).

- Inventory valuation is based on the costs companies incur to take inventory, transform it into a ready-to-sell state, and ship it to the right place of sale.

- Inventory valuation is the cost associated with a company's inventory at the end of the reporting period.

Inventory systems: Periodic Inventory System, Perpetual Inventory System

An inventory management system is a technology solution that integrates all aspects of an organization's inventory tasks, including shipping, purchasing, receiving, warehousing, turnover, tracking, and reordering. There is some debate about the difference between inventory management and inventory management, but the truth is that a good inventory management system takes a holistic approach to inventory and the organization takes advantage of lean practices throughout the supply chain. It's all about doing it by being able to optimize productivity and efficiency. To meet customer expectations, we have the right inventory in the right place.

That said, there are two types of inventory management systems available today: permanent inventory systems and regular inventory systems. Within these systems, two main types of inventory management systems (barcode systems and radio frequency identification (RFID) systems) are used to support the entire inventory management process.

Main types of Inventory Management System:

1. Permanent Inventory System,

2. Regular Inventory System.

Types of inventory management systems in the inventory management system:

1. Barcode system,

2. Radio frequency identification (RFID) system.

An inventory management system helps you track your inventory and provides you with the data you need to manage and manage your inventory. Whatever type of inventory management system you choose, your company must ensure that it includes a system for identifying inventory items and their information, such as barcode labels and asset tags. A hardware tool for scanning barcode labels or RFID tags. A central database of all inventories, in addition to data analysis, report generation, and demand forecasting capabilities. Inventory labelling, documentation, and reporting processes, along with proven inventory methodologies such as just-in-time, ABC analysis, first-in first-out (FIFO), and last-in first-out (LIFO).

Periodic Inventory System

What is Periodic Inventory?

Periodic Inventory is an accounting stock valuation method that is performed at specified intervals. Companies physically count products at the end of the period and use that information to balance their general ledger. The entity then applies the balance to the start of a new period.

In a regular review inventory system, accounting practices differ from a permanent review system. To calculate the year-end amount of regular inventory, the company performs a physical count of inventory. Organizations use intermediate marker quotes such as monthly and quarterly reports. Accountants do not update general ledger inventory when a company purchases goods for resale. Instead, it will be deducted from your temporary account purchase. Temporary accounts start with zero balance each year. The accountant will delete the balance to another account at the end of the year.

The company makes the necessary adjustments from the purchase of goods to the reverse account in the general ledger. A contra account is the opposite of the general ledger because it offsets the balance of the associated account and appears in the financial statements. Examples of Contra accounts include purchase discounts or purchase returns and allowance accounts. Combine these accounts to get a net purchase.

In a regular inventory management system, companies also keep shipping costs in a separate account from their main inventory account. Track shipping costs associated with your Freight in or Transportation In accounts for in-stock inventory. Ultimately, the cost of this account increases the value of your inventory. In the journal, the account looks like this:

What is a Regular Inventory System?

A regular inventory system is a software system that supports regular inventory acquisition. The company imports the inventory number into the software, performs the first physical review of the item, and then imports the data into the software for adjustment.

These software systems support current inventory management methods. You can use them to get a paper inventory list, import inventory data, order more inventory, and calculate the data needed to adjust inventory for the new period. Companies can export these numbers and reports to accounting software. Companies choose software based on their needs and product requirements.

Catherine Milner and Geoff Relph are co-authors of "Inventory Management: Advanced Methods for Manage Inventory within Business Systems" and "The Inventory Toolkit: Business Systems Solutions." Inventory Matters, Ltd. As owners of, they consult with clients and advise them to choose a software system for inventory management that does proactive work.

Milner explains: "Many companies are trying to implement an inventory management business system that doesn't have the features and requirements they need. The most important thing is to know exactly what you need. Someone sells the system to you. When it comes to, their measure of success may not be the same as the measure of your business's success, whether it's your business, your sales business, or your hosting business. We have a focus, so make sure you are the one that drives the sale. "

Lelf adds: "For example, when you buy a car, you know what you want. A sales person may have a vehicle that doesn't exactly meet your requirements. His job is more than you need. To convince you to sell. When you drive a car, you realize that you can't operate the vehicle effectively. As a buyer, be careful. You need, not an estimate of what you want. You should buy what you want. Whether this is a matter of choice or misunderstanding, it's hardly a problem. It's not a criticism, but it reflects the industry. "

In a recurring system, the software should display the cost of inventory recorded according to the last physical count. It will not be updated based on sales. The company registers purchases made between counts in the purchase account. The software creates journal entries based on transactions from inventory and cost of sales (COGS) accounts to user-defined accounts. Other features of regular inventory management software include:

a) User-defined accounts set up for various combinations of books and subsidiaries.

b) Create a journal entry in the background based on a scheduled script.

c) Custom reports such as journals created today, journals not needed for transactions created today, error reports, and changed transactions.

d) The role of customized software such as principal accountants.

When will the regular inventory system be used?

SMEs with a small number of SKUs use a regular system if they are not concerned about expanding their business over time. Depending on the product and needs, the recurring system can also be used in combination with a permanent system.

Any company can use a recurring system because no additional equipment or coding is required to use the recurring system. Therefore, the cost is low. Implement and maintain. In addition, you can train your staff to provide easy inventory when time is limited or when staff turnover is high. For example, seasonal staff may come and go. You can quickly count the products you are working on, but permanent systems that provide more accurate inventory require staff training on electronic scanners and data entry. Read the Perpetual Inventory Guide to learn more about the Perpetual System and how it provides a more accurate inventory solution.

If you manage your supply chain process, sell some products, and look at the products that flow through your business, you can also use a recurring system. If you need to investigate to identify missing inventory or disproportionate numbers, a regular system will not help. This issue arises as operations grow and become more difficult to actively manage.

Milner describes the regular system as "a simple approach to inventory management that helps those small organizations that have a simple approach to inventory management." These businesses do not always have a clear relationship between raw materials or purchased items and the final product sold. An example of a business that uses a regular system is a food bank. They frequently counted physical inventories to determine final inventory quantities. "

Overview

The recurring inventory system does not track inventory daily. Rather, the organization can know the start and end inventory levels for a particular time period. These types of inventory management systems use physical inventory to track inventory. When the physical inventory is complete, the balance of the purchase account shifts to the inventory account and is adjusted to match the cost of the closing inventory. Organizations can choose whether to calculate the cost of closing inventory using the LIFO or FIFO inventory accounting method or another method.

Note that the starting stock is the ending stock for the previous period.

Benefits of Regular Inventory System

The main advantages of adopting a recurring inventory system are its ease of implementation, its low cost, and the reduction in personnel required to implement it. Adding a regular system to your business takes only a short time. You can collect product data with a simple count of legitimate paper, especially if you only offer a small number of products. In many cases, a basic daytime or weekly count is sufficient for SMEs to properly handle their inventory. This means you don't need expensive and complex equipment, only important information gathering tools such as pens and paper.

However, one of the major drawbacks is that it collects minimal information, usually only the number of individual products. In addition, we do not collect or report this data in "real time". Inventory numbers are updated at different times, not when buying or selling. In fact, if you need to track your product from start to finish or investigate shortages or excesses, you don't have much information to move on. The cause of the problem cannot be quickly identified.

Disadvantages or Drawbacks:

There are some drawbacks to using a Periodic Inventory System.

First, when the physical inventory is completed, normal business activities are almost interrupted. As a result, workers may rush physical counts due to time constraints. Recurring inventory systems typically do not use inventory trackers and therefore cannot maintain inventory continuously, which can lead to more prevalence of errors and fraud. Also, with a regular inventory management system, the intervals between counts are so long that it is more difficult to pinpoint where inventory count discrepancies occur. The effort required for a regular inventory management system is better suited for small businesses.

- Estimated Error: During the period between inventory, you need to estimate the cost of goods sold and the products and quantities available. After completing the physical count, this estimate may be far from the actual cost of goods sold.

- Significant Adjustment: During the period between inventories, there is no way to describe lost, excess, or obsolete merchandise. This can result in significant and costly adjustments after the next physical count. The periodic table is up-to-date only immediately after inventory and accounting events.

- Unable to Scale: Regular systems have some margin because they are based on their ability to track merchandise. However, expanding your business with a regular system takes more time and effort as you grow and add products to your inventory.

Example:

An example of a recurring system would include accounting for the starting inventory and all purchases made during the period as credits. Instead of recording their own sales during the debit period, the company finally performs a physical count and now adjusts the account.

Cost flow assumptions are inventory costing methods in the periodic system that companies use to calculate COGS and final inventory. Starting inventory and purchases are the inputs that an accountant uses to calculate the cost of an item that can be sold. Then apply this number to cost flow assumptions that your company chooses to use, such as FIFO, LIFO, and weighted average.

Perpetual Inventory System

What is a Perpetual Inventory System?

The permanent inventory system uses technology to track and update inventory records each time you receive or sell an item. In a perpetual inventory system, the sale of inventory items increases cost of goods sold (COGS) and is also updated in accounting records to ensure that the number of items in the store or in storage is accurately reflected in the inventory account.

Permanent inventory systems are more robust than regular inventory systems, where companies regularly audit inventory to update inventory information. These audits include regular and regular physical inventory. The main difference between a permanent inventory system and a regular inventory system is that the former has a system that updates inventory information in real time, while the latter uses a more manual process.

Increased use of Perpetual Inventory System

Until now, permanent inventory systems have not been widely used due to the difficulty of recording and processing large amounts of data quickly and accurately.

However, in recent years, technical capabilities have improved, business and accounting practices have improved, inventory tracking systems can now be managed using computers and scanners, and the burden of permanent inventory tracking has been reduced.

A Perpetual Inventory System can be defined as "a system of records maintained by the management department that reflects the physical movement of inventory and the current balance." Therefore, it is a system that checks the balance each time material is received and issued through inventory records to facilitate regular checks and avoid closing the company for inventory. To ensure the accuracy of permanent inventory records (bincards and store ledgers), physical verification of the store is carried out by an ongoing inventory program.

The operation of the Permanent Inventory System is as follows: -

a. Inventory records are maintained and up-to-date transaction postings are made so you always know your current balance.

b. Various sections of the store are taken up by rotation for physical checks. Some items are checked daily, so all items may be checked many times during the year.

c. Stores that have arrived but are awaiting quality inspection are not yet listed in the inventory record, so they will not be confused with regular stores at the time of on-site confirmation.

d. In some cases, after counting, weighing, measuring, or listing, the physical inventory available in the store is properly recorded on the bin card / inventory tag and inventory check sheet.

Do not confuse the permanent inventory system with continuous inventory. Continuous inventory is an important feature of the permanent inventory system. Permanent inventory means a system of inventory records and continuous inventory, and continuous inventory means only physical verification of inventory records with actual inventory.

In continuous inventory, physical verification is done throughout the year. Randomly pick and check 10 to 15 items every day so that you can keep the surprise element of inventory check and check each item many times each year. On the other hand, regular checks are usually done at the end of the year, so the surprise element is missing.

Benefits of Perpetual Inventory System:

a. This system eliminates the need to physically check all inventory and stores at the end of the year.

b. It avoids disruption of the organization's day-to-day activities, including production and dispatch.

c. A reliable and detailed check of the store is maintained.

d. Errors, irregularities, and inventory losses due to other methods are quickly resolved, and the necessary actions minimize future recurrence of such things.

e. The work is done systematically and without rushing too quickly, so the numbers are readily available.

f. Actual inventory can be compared to the maximum and minimum levels allowed so that inventory can be kept within specified limits. The disadvantages of excess inventory are avoided and cannot be capitalized into store materials to exceed the budget.

g. Recorder levels for various items in the store are easily available, facilitating store procurement operations.

h. For monthly or quarterly financial statements such as income statements and balance sheets, inventory numbers are readily available and no physical validation of balances is required.

What is an Inventory Management System?

An inventory management system is a set of hardware and software-based tools that automate the process of inventory tracking. The types of inventories tracked include almost all types of quantifiable merchandise, including food, clothing, books, equipment, and other items that consumers, retailers, or wholesalers may purchase. Can be included.

Modern inventory management systems work almost exclusively using barcode technology. Barcodes were originally developed to automate the grocery checkout process, but they can encode a variety of alphabetic and numeric symbols, making them ideal for encoding products in inventory tracking applications. These systems operate in real time using wireless technology and send information to a central computer system when a transaction occurs.

Which industry uses the Inventory System?

Inventory management systems are used in a variety of applications, all centered around tracking the delivery of goods to customers. The ability to track inventory is very important in retail stores, especially those that sell a large number or variety of merchandise. It is also used to track orders and shipments in the warehouse and to process automatic orders. Other important applications for inventory systems are manufacturing, shipping, and receiving.

Advantages of Inventory Management System

Inventory tracking is essential to ensure quality control in businesses that process consumer goods-centric transactions. In supermarkets, for example, inadequate store inventory management can lead to unknowingly sold-out inventory of important items. The inventory system automatically alerts retailers when it is time to reorder. Inventory tracking is also an important way to automatically track large shipments. For example, if a company ordered 10 pairs of socks for retail, but received only 9 pairs, this is obvious when looking at the contents of the package and it is unlikely that an error will occur. Meanwhile, a wholesaler orders 100,000 pairs of socks and is short of 10,000 pairs. Manually counting each pair of socks can result in an error.

An automated warehouse management system helps minimize the risk of errors. In retail stores, inventory management also helps track the theft of retail goods and provides valuable information about the need for anti-theft systems to prevent store profits and losses.

Barcode Inventory System

How does the Barcode Inventory System work?

The automatic inventory system works by scanning the item's Barcode. Barcode scanners are used to read barcodes, and the information encoded by the barcodes is read by the machine. This information is tracked by a central computer system. For example, a purchase order may contain a list of items that are pulled for packaging and shipping. In this case, the inventory tracking system can perform various functions. Helps workers find items in the warehouse order list, encodes shipping information such as tracking numbers and shipping addresses, removes these purchased items from inventory, and removes the exact number of items in stock can be maintained.

All this data works together to provide the enterprise with real-time inventory tracking information. Inventory management systems make it easy to find and analyze inventory information in real time with a simple database search and are an integral part of any business that moves the supply of goods.

Barcode Stocking Software

Some of the inventory management systems that need to be considered are software. Barcode inventory software is a core component because it has the ability to assist in inventory management in a warehouse or retail environment. The right software for your needs can help streamline your system, update inventory automatically, maintain accuracy, and reduce mistakes. Talk to your inventory specialist to find the right software.

There are many benefits to using barcodes in the inventory management process, including:

- Accurate record of all inventory transactions.

- Eliminate frequent and time-consuming data errors on manual or paper systems.

- Eliminate manual data entry mistakes.

- Scanning ease and speed.

- Automatically update your inventory.

- Record transaction history to easily determine minimum level and reorder quantity.

- Streamline documents and reports.

- Rapid Return on Investment (ROI).

Facilitate the movement of inventory in warehouses, across locations, and from receipt to picking, packing, and shipping.

Facilitate the movement of inventory in warehouses, across locations, and from receipt to picking, packing, and shipping.

Radio Frequency Identification (RFID)

Radio frequency identification (RFID) tags are attached to individual products or product boxes to get radio signals that contain information about the merchandise. Passive tags reflect a sign generated by a reader which will read the tag from about 10 feet away. The active tag contains an influence supply and generates its own signal, which expands the range. When products within the warehouse are tagged, readers can instantly determine inventory on racks on shelves, improving inventory accuracy and control.

Reduction of Inventory Shrinkage

Inventory reduction may be a term used for product identification, storage, shipping errors, and inventory loss caused by theft. Improved inventory tracking with RFID tags reduces errors because the method is fully automated once the tags are attached. Discrepancies are going to be immediately visible to the staff liable for tracking inventory. Companies also reduce the prospect of theft if RFID systems track products and warehouse warehousing management systems track access to warehouses.

Real-Time Inventory Management

Non-RFID inventory management systems believe records of products received and shipped, and regular manual inventory to work out the amount of things available. These numbers are often inaccurate. If all items available have RFID tags and a reader is found near each rack on the shelf, the amount of things available is that the actual number supported the amount of things on the shelf at that point. Is displayed as. Therefore, RFID helps avoid backorders thanks to unexpected out-of-stock conditions.

Reduction of labor costs

RFID systems reduce the quantity of manual labour required in 3 ways. The method of recording the movement of products in and out of inventory are often highly automated, reducing the necessity to take care of records manually. Manual inventory will occasionally check for defective or untagged items. Fewer errors eliminate the necessity for manual work to correct inventory mistakes. Labor costs related to RFID tagging will increase, but using tags to exchange barcode labels can reduce the value increase.

Better Asset Utilization

In addition to the particular product, warehouse assets include dollies, trucks, and other means of transportation, also because the warehouse itself. If the corporate knows the particular level of product inventory, it can reduce inventory and respond confidently to customer demands instead of processing uncertain quotes. When dollies and trucks transport goods, they will take full advantage of some products that are but full load, instead of manipulating them. You'll make the warehouse itself smaller, otherwise you can store more or differing types of inventories. Enterprises got to balance these savings with the value of buying and installing tags and tag readers to work out if RFID systems are economically meaningful.

Key takeaways:

- An inventory management system is a technology solution that integrates all aspects of an organization's inventory tasks, including shipping, purchasing, receiving, warehousing, turnover, tracking, and reordering.

- An inventory management system helps you track your inventory and provides you with the data you need to manage and manage your inventory.

- In a regular inventory management system, companies also keep shipping costs in a separate account from their main inventory account.

- A regular inventory system is a software system that supports regular inventory acquisition.

- SMEs with a small number of SKUs use a regular system if they are not concerned about expanding their business over time.

- The recurring inventory system does not track inventory daily. Rather, the organization can know the start and end inventory levels for a particular time period.

- The main advantages of adopting a recurring inventory system are its ease of implementation, its low cost, and the reduction in personnel required to implement it.

- First, when the physical inventory is completed, normal business activities are almost interrupted.

- An example of a recurring system would include accounting for the starting inventory and all purchases made during the period as credits.

- The permanent inventory system uses technology to track and update inventory records each time you receive or sell an item.

- A Perpetual Inventory System can be defined as "a system of records maintained by the management department that reflects the physical movement of inventory and the current balance."

- An inventory management system is a set of hardware and software-based tools that automate the process of inventory tracking.

- The ability to track inventory is very important in retail stores, especially those that sell a large number or variety of merchandise.

- The automatic inventory system works by scanning the item's barcode. Barcode scanners are used to read barcodes, and the information encoded by the barcodes is read by the machine.