Unit-I

Demand and Supply

Q1). What are the key determinants of demand?

Sol: Some of the key determinants of demand are:

【1】Price of the product

When all other factors remain constant or equal, people make decisions with price as a parameter. According to the law of demand, this means that the increase in demand follows the decrease in price, and the decrease in demand follows the increase in the price of similar goods.

The demand curve and demand schedule help you determine the demand quantity at the price level. Elastic demand implies a robust variation with price changes. Similarly, inelastic demand means that even if there is a change in price, the quantity does not change much.

[2] Consumer income

An increase in income leads to an increase in the number of goods demanded by consumers. Similarly, a decrease in income is accompanied by a decrease in the level of consumption. This relationship between income and demand isn't linear in nature. Marginal utility determines the percentage of changes in demand levels.

3] Prices of related goods or services

Complementary products-an increase in the price of one product causes a decrease in the amount required for complementary products. Example: an increase in the price of bread reduces the demand for butter. This occurs because the product is complementary in nature.

Alternative products-an increase in the price of one product causes an increase in demand for alternative products. Example: an increase in the price of tea will increase the demand for coffee and decrease the demand for tea.

4] Consumer expectations

The expectation of higher income or the expectation of an increase in the price of goods leads to an increase in the required amount. Similarly, the expectation of a decrease in income or a decrease in commodity prices would reduce the amount requested.

5] Number of buyers in the market

The number of buyers has a significant impact on aggregate or net demand. As the number increases, the demand increases. In addition, this is true regardless of the change in the price of the goods.

Q2).What are the Determinants of Supply?

- Price of goods / services

The most obvious determinant of supply is the price of the product/service. If all other parameters are equal, the higher the relative price will increase the supply of the product. The reason is simple. Companies offer goods and services to make a profit, and when the price goes up, so does the profit.

2. Related products prices

Let's say the price of wheat has gone up. Therefore, it will be more profitable for the enterprise to supply wheat, compared to corn and soybeans. Thus, the supply of wheat increases, but the supply of corn and soybeans decreases.

Therefore, we can say that if the price of related goods increases, the enterprise will increase the supply of goods with higher prices. This leads to a decrease in the supply of goods with lower prices.

3. Price of production factors

The production of goods costs a lot. If the price of a particular factor of production increases, the cost of manufacturing goods that use the element in large quantities increases significantly. The cost of production of goods that use the above elements in a relatively small amount increases slightly.

For example, the increase in the cost of land has a significant impact on the cost of wheat production, and a small impact on the cost of production of cars.

So, when the price of one factor of production changes, the relative profitability of different production lines changes. This causes producers to shift from one line to another, resulting in changes in the supply of goods.

4. Current status of technology

Technological innovations and inventions tend to make it possible to use the same resources to produce better quality and/or quantity of goods. Thus, the state of technology can increase or decrease the supply of certain goods.

5. Government policy

Goods taxes, such as excise duty, import duty, GST, etc., have a big impact on the cost of production. These taxes could raise the overall cost. Therefore, the supply of goods affected by these taxes will only increase if the price increases. Subsidies, on the other hand, reduce the cost of production, which usually leads to an increase in supply.

6. Other factors

There are many other factors that affect the supply of goods or services: government industrial and foreign policy, corporate goals, infrastructure facilities, market structure, natural factors.

Q3). Q1. In the case of demand curve movement, it:

a. Move upwards or downwards

b. Move left or right

c. Both of the above

d .None of the above

Sol: the demand curve movement occurs when all other factors affecting the requested quantity remain constant and only the price changes. Therefore, demand moves upwards or downwards along the same curve. So the correct answer is Option A.

Q4). The relation between the quantity of supply and price is _____ proportional.

a .Direct

b. Indirectly.

c. Not relevant

d. None of the above

Sol: the correct answer is A. With the increase in the price of goods; the supply by the company also increases. Therefore, the relationship between price and supply is direct and positive.

Q5). Explain the impact of tax increases on the supply curve.

Sol: tax increases benefit directly towards greater production costs. The increase in production costs reduces the profit margin of goods. Declining profit margins discourage producers from producing goods as they shift to better options now.

Therefore, the supply of goods goes down. As you can see, taxes and supplies have the opposite relationship. Taxes are included in factors other than price, so any change will lead to a shift in the supply curve.

Q6). Which of the following is correct about the product cost?

A. Product cost refers to the distribution system.

B. Product costs are the sum of fixed, variable, and semi-variable costs

c. It shows the total cost of the product.

D. Product cost refers to the sale of a product.

Sol: when calculating the cost of a product, it includes the sum of all costs associated with the production of a certain amount of goods or services. The correct option is B.

Q7)What are the factors affecting the decision of prices?

Sol: The factors that affect the pricing of products are:

1] Product cost

The cost of the product is one of the most important factors that affect the price. This includes the sum of fixed, variable and semi-variable costs incurred through the manufacture, distribution and sale of products. Fixed costs refer to costs that remain fixed at all levels of production or sales. For example, rent, salary, etc.

Variable costs are attributed to costs directly related to the level of production or sales. For example, the cost of basic materials, the cost of apprenticeships, etc. Semi-variable costs take into account these costs, which vary depending on the level of activity, but not in direct proportions.

2] Utility and demand

Habitually, end users demand more units of the product when the price is low, and vice versa. On the other hand, if the demand for the product is elastic, then the volume of demand can change significantly if the price fluctuations are small. On the other hand, if there is no elasticity, the change in price will not have a significant impact on demand. In addition, the buyer is ready to pay to the point where he feels that the utility from the product is at least equal to the price paid.

3] Degree of competition in the market

The next consistent factor that affects the price of manufactured goods is the nature and degree of competition in the market. If the degree of competition is low, companies can fix any price for their products. However, if there is competition in the market, we will fix the price, taking into account the price of the replacement.

4] Government and regulatory regulations

Companies that monopolize the market habitually impose high prices on their products. To protect the interests of the people, the government intervenes and regulates the price of goods. For this purpose, it declares some products as indispensable products. For example, life-saving drugs.

5] Pricing purposes

Another consistent factor affecting the price of an item for consumption or service is the purpose of pricing. Maximizing profits, gaining market share leadership, surviving in a competitive market and achieving product quality leadership are the goals of the company's pricing? Generally, companies charge higher prices to cover higher quality and higher costs if backed by the above objectives.

6] Used marketing methods

Various marketing methods such as distribution system, salesman quality, marketing, wrapping type, regular customer service, etc. also affect the price of manufactured goods. For example, if an organization uses elegant materials for packaging a product, the organization will charge an ultra-high amount of revenue.

Q8) Define elasticity of demand.

Sol: Price elasticity of demand measures the degree of responsiveness of demand to changes in the price of goods.Therefore, its measurement depends on comparing the rate of change in prices with the rate of change in the resulting volume of demand. There are slight problems with calculating the rate of change in this way. Depending on whether you move the demand curve up or down, you will get different answers. 1 way to avoid this difficulty is to take the average of 2 prices and 2 quantities in the range you are considering and compare the change in the mean, rather than comparing it with the price or quantity at the start of the change.

The formula for calculating the price elasticity of demand looks like this:

Q9) What are the different kinds of price elasticity?

Sol: The different types are:

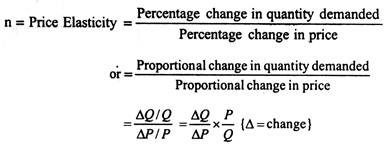

a.Price resilient demand:

If the price elasticity of demand is greater than 1, this is called the price elasticity demand.When the price changes by 1%, a larger response occurs than when the demand changes by 1%: ΔP<ΔQ.

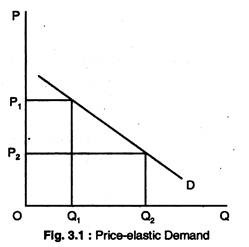

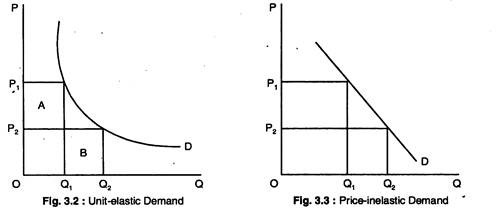

b.Single price elasticity of demand:

In this case, if the price changes by 1%, then the volume of demand changes by exactly 1%.

c.Demand without price elasticity:

Thus, a 1% change in price causes a response of less than 1% change in the volume of demand: ΔP>ΔQ.

Q10). What are the Determinants of price elasticity?

Sol: Determinants of price elasticity are:

a.Ease of substitution:

The more substitutes are available for the product, the greater the elasticity of demand.For example, the demand for Whole Foods is not very resilient, but if you consider certain foods, you can see that the elasticity of demand is much greater.This is because you can not find an alternative to the whole food, but you can always find an alternative to one type of food.

b.Number of uses:

The more times the goods are used, the greater the elasticity of demand.For example, electricity has many applications such as heating, lighting and cooking.Soaring electricity prices not only make people economical in all these areas, but in some cases could replace other fuels.

c.Percentage of revenue spent on products:

If the price of a packet of salt rises by 50 per cent, for example, from 20p to 30p, it would discourage most people because their share of income is so small.However,if the price of a car rises from £ 4,000 to £ 6,000,even the same percentage rise will have a huge impact on sales.

The larger the percentage of income that the price of a product represents, the more resilient the demand tends to be.

d.Time:

In general, demand elasticity tends to be greater in the long term than in the short term.The period we are considering plays an important role in shaping the demand curve.For example, if the price of meat has increased disproportionately to other foods, you can not immediately change your diet.

Therefore, people will continue to demand the same amount of meat in the short term.But in the long run, people will start looking for alternatives.Whether this is a noticeable effect depends on whether the consumer finds a suitable alternative.It may also be possible to mask the opposite effect.

e.Durability:

The more durable the product is, the more resilient the demand tends to be.For example, if the price of potatoes increases, you can not eat the same potatoes twice.But if the price of furniture rises, you can make the existing furniture last longer.

f.Addiction:

If a product such as a cigarette forms a habit, this tends to reduce the elasticity of demand.

g.Price of other products:

We know that when the price of a product rises, the demand for substitutes increases and the demand for complements decreases.So when demand increases (or decreases) at a certain rate, the elasticity does not change, but when you shift the curve to the right for a certain amount, the elasticity decreases.