Unit 4

Cost Ascertainment

Q1) What are the types of costing are typically used to determine costs?

A1) The following types of costing are typically used to determine costs:

1. Uniform costing

If many companies in the industry agree to follow the same costing system in detail and adopt common terms for different items and processes, they are said to follow a uniform costing system. In such cases, you can compare the performance of each company to the performance of other companies, or to the average performance of the industry. Under such a system, it is also possible to determine the production cost of goods that apply to the entire industry. This is useful if your government requires tax cuts or protection.

2. Marginal cost:

This is defined as a confirmation of marginal costs by distinguishing between fixed and variable costs. It is used to see the impact of changes in production volume or type of production volume on profits.

3. Standard costing and variance analysis

This is the name given to the method in which the standard cost is pre-determined and then compared to the recorded actual cost. Therefore, this is a cost verification and cost management technique. This technique can be used in combination with any costing method. However, it is especially suitable when the manufacturing method involves the production of repetitive standardized products.

4. Historical cost principle

Confirmation of costs after incurred. The usefulness of this type of costing is limited.

5. Direct costing

This is the practice of charging all overhead costs to operations, processes, or products and amortizing all overhead costs to the profits they generate.

6. Absorption costing

This is the practice of charging all operational, process, or product costs, both variable and fixed. This is different from the marginal cost excluding fixed costs.

Q2) What is the unit price?

A2) Unit costing is understood as "output" or "single output" costing. Following unit costing, there are concerns about the continual production of one product on an outsized scale. The value unit is that the same cost. Additionally, the merchandise has uniform and homogeneous properties. This product isn't manufactured during a continuous process. This is often the most difference between unit costing and process costing.

In some cases, concerns generate quite one grade of a product. Therein case, single costing or output costing is performed. Once a product is produced, cost collection and price verification are very easy.

In this method, the entire cost incurred is split by the entire production to work out the value per unit. Additionally, costs are collected for every element, and therefore the cost for every element is split by the entire output to work out the value per unit for every element.

A cost statement is made containing the figures for the previous period to supply comparison and control. We’ve successfully calculated unit costs within the manufacture of homogeneous products like bricks, pencils, pens, books, computers and laptops.

Q3) What subsequent costing information is required for unit costing?

A3) The subsequent costing information is required for unit costing:

1. Value of raw materials consumed

Material request documents are the idea for collecting the worth of staple consumption. Materials are only issued supported approved material request documents.

Approval documents provide details on the quantity of fabric with different grade and sort values. If the fabric is broken during storage and handling, we'll increase and adjust the difficulty price of the fabric to point normal loss. Unusual losses should be charged to the costing of the earnings report.

2. Labor costs

Labor is often divided into two categories: direct labor and indirect labor. If workers are engaged in direct manufacturing activities, they're treated as direct labor and may identify and calculate direct labor with the assistance of production details. Several workers engaged generally factory activities. They will be placed in several categories of wage tables.

3. Overhead

Overhead is assessed on a functional basis for unit costing purposes. Factory overhead or production overhead, office and management overhead, and sales and distribution overhead are categories of overhead. These overhead costs are collected at a given rate for costing purposes.

The actual overhead incurred is collected from the financial records. Cost statements are made at short intervals with the assistance of certain overhead costs.

Q4) Define costing with its method.

A4) Costing is an accounting method that records and analyses all costs associated with the execution of a process, project, or product. Such analysis helps management make strategic decisions.

Costing uses a variety of techniques to make your organization cost-effective. Everything you need to know about the different costing methods. The term "costing method" can be used to refer to the various processes or procedures used to determine and display costs.

There are different costing methods in different industries, depending on the nature of the job. Costing methods can be studied under the head below. -1. Method based on the principle of job costing 2. Method based on the principle of process costing.

Costing methods can be studied under the head below. -1. Method based on the principle of job costing 2. Method based on the principle of process costing.

Some of the methods based on the principles of process costing are: -

1. Process costing

2. Operating costing

3. Department costing

4. Single or unit or output costing

5. Operation or operation or work or service costing

6. Multiple or combined costing.

In addition, some other costing methods are: -

1. Uniform costing

2. Multiple or combined costing

3. Department costing

4. Cost plus method

5. Target costing method 6. Farm costing

7. Activity-based costing.

Different types of costing methods: job costing, contract costing, batch costing, process costing, and operating costing.

Q5) Explain the different methods of costing.

A5) The costing method refers to the cost confirmation and costing system. Industries differ in their nature, the products they produce, and the services they provide. Therefore, different costing methods are used in different industries. For example, the costing method used by building contractors is different from that of shipping companies.

Job costing and process costing are two basic methods of costing. Job costing is suitable for industries that manufacture or perform work according to customer specifications. Process costing is suitable for industries where production is continuous and the units of production are the same. All other methods are a combination, extension, or improvement of these basic methods.

Let's take a closer look at how to calculate costs.

Method # 1 Job costing:

This is also known as specific order costing. There is no standard product and each job or work order is adopted in a different industry. The work is done strictly according to the customer's specifications, and the work is usually completed in a short time. The purpose of job costing is to see the cost of each job individually. Job costing is used in printing presses, motor repair shops, car garages, movie studios, the engineering industry, and more.

Method # 2 Contract Costing:

This is also known as terminal costing. Basically, this method is similar to job costing. However, it is used when the work is large and it takes a long time. The work will be done according to the customer's specifications.

The purpose of contract costing is to see the costs incurred in each contract individually. Therefore, a separate account is provided for each contract. This method is used by companies engaged in the construction of ships, buildings, bridges, dams and roads.

Method # 3 Batch Costing:

This is an extension of job costing. A batch is a group of identical products. All units in a particular batch are uniform in nature and size. Therefore, each batch is treated as a cost unit and is costed separately. The total cost of the batch is checked and divided by the number of units in the batch to determine the cost per unit. Batch costing is adopted by manufacturers of biscuits, ready-made garments, spare parts medicines and more.

Method # 4 Process Costing:

This is called continuous costing. In certain industries, raw materials go through various processes before they take the form of final products. In other words, the finished product of one process becomes the raw material for the next process. Process costing is used in these industries.

A separate account is opened for each process to see the total cost and cost per unit at the end of each process. Process costing applies to continuous process industries such as chemicals, textiles, paper, soaps and foam.

Method # 5 Unit costing:

This method is also known as single costing or output costing. It is suitable for industries with continuous production and the same unit. The purpose of this method is to see the total cost and the cost per unit. Create a cost sheet considering material costs, labor costs, and overhead costs. Unit costing applies to mines, oil rig units, cement factories, brick factories and unit manufacturing cycles, radios, washing machines, etc.

Method # 6 Operating cost:

This method is followed by the industry that provides the service. To determine the cost of such services, use composite units such as passenger kilometres and tone kilometres to determine the cost. For example, for a bus company, operating costs represent the cost of carrying passengers per kilometre. Operating costs are used in air railways, road transport companies (commodities and passengers) hotels, movie theatres, power plants, etc.

Method # 7 Operating cost:

This is a more detailed application of process costing. It includes costing by all operations. This method is used when there is a repetitive mass production with many operations. The main purpose of this method is to see the cost of each operation.

For example, manufacturing a bicycle handlebar involves many operations such as cutting a steel plate into appropriate strips, forming, machining, and finally polishing. The cost of these operations can be viewed individually. Operating costs provide a detailed analysis of costs to achieve accuracy and apply to industries such as spare parts, toy manufacturing, and engineering.

Method # 8 Multiple Costing:

It is also known as compound costing. This refers to a combination of two or more of the above costing methods. It is used in the industry where multiple parts are manufactured separately and assembled into a single product.

Q6) Define operating cost. Write its classification.

A6) Operating costs are a way of checking the cost of providing or operating a service. This costing method is applied by the operator who provides the service, not the production of the goods. For example, such businesses are: Transportation concerns, gas companies; power companies; hospitals; theatres, etc.

The cost system used is different from the manufacturing concerns because the nature of the activities performed by the service business varies. The industries that are suitable or applicable to operating costs are:

- Transportation services: buses, taxis, trucks, railroads, etc.

- Welfare services: water bottles, hospitals, libraries.

- Utility suppliers: gas, electricity, water.

- Municipal services: street lights, road maintenance.

Classification of operating costs

Operating costs can be divided into three categories. For example, in the transportation business, these three categories are:

- Operating and running costs – Includes costs of a variable nature. For example:

a) Gasoline and diesel costs.

b) Lubricating oil, grease, etc.

c) Wages for drivers, conductors, etc. (if payments are based on time or travel distance).

d) The committee undertakes the bridge (charged).

e) Depreciation (if allocated based on mileage execution and treated as variable).

2. Maintenance Costs – These costs are semi-variable and include the following costs:

a) Tires and tubes,

b) Repair and maintenance,

c) Spares and accessories, overhauls, etc.

3. Fixed or Permanent Charges – These costs are inherently fixed, but the operation is done in a standing position.

a) Garage rent,

b) insurance,

c) Road license,

d) Depreciation,

e) Interest in capital,

f) Management overhead

g) Automobile tax

h) Garage rent

i) General supervision

j) Salary of operation managers, supervisors, etc.

Q7) Draw the specimen of operating cost.

A7) Format of Statement of Operating Cost

Statement of Operating Cost

For one month

Particulars | $ | Total Cost ($) | Cost per km ($) |

Fixed/ standing cost |

|

|

|

Salary of manager | **** |

|

|

Salary of accountant | **** |

|

|

Salary of cleaner | **** |

|

|

Salary of mechanic | **** |

|

|

Garage rent | **** |

|

|

Driver’s salary | **** |

|

|

Insurance | **** |

|

|

Taxes | **** | **** | **** |

Maintenance cost |

|

|

|

Repair Expense | **** |

|

|

Maintenance expense | **** |

|

|

Tires and tubes | **** |

|

|

Servicing and cleaning | **** |

|

|

Painting | **** |

|

|

Store parts and components | **** | **** | **** |

Operating or variable expenses |

|

|

|

Petrol | **** |

|

|

Oil and sundries | **** |

|

|

Lubricating oil | **** |

|

|

Grease | **** |

|

|

Depreciation | **** |

|

|

Cost per ton-km |

| **** | **** |

|

| **** | **** |

Q8) How is confirmation made of cost per unit in unit costing?

A8) Confirmation of cost per unit in unit costing

The main purpose of unit costing is to ascertain the value per unit. The aim is then to research the value of every element and its share in total cost. For this purpose, costs are cumulative and analysed under various factors of cost.

Financial records are wont to collect direct costs and costs. Costing records are wont to collect overhead and expenses. Cost records like material summaries, wage summaries, time records, and price ledgers are a part of the records used for cost confirmation purposes.

Use the subsequent formula to work out the value per unit.

Cost Per Unit = Total Cost / Number of Units Produced

Costing is an accounting method that records and analyses all costs associated with the execution of a process, project, or product. Such analysis helps management make strategic decisions.

Costing uses a variety of techniques to make your organization cost-effective. Everything you need to know about the different costing methods. The term "costing method" can be used to refer to the various processes or procedures used to determine and display costs.

There are different costing methods in different industries, depending on the nature of the job.

Q9) How are units measured in unit costing?

A9) Unit of measure in unit costing

Units of measure are a crucial factor for cost confirmation on the cost method. There are many units of measure. They’re units, litres, dozens, yards or meters, square feet, gloss, tones, veils, millilitres, kilograms, bags and more.

The company may choose or adopt one among the above units of measurement, counting on the character of the industry

Sl. | Nature of Industry | Unit of Measurement |

1 | Sugar | A Quintal |

2 | Bricks | Thousand |

3 | Collieries | A tone of Coal |

4 | Pens, Pencils | Dozen, Gross |

5 | Breweries | A liter |

6 | Cement | Tones |

7 | Paper Mills | A kg of paper, Tones |

8 | Hospitals | Patient - days |

9 | Dairies | A liter of milk |

10 | Road Transport | Passenger - Kilometers |

11 | Automobile | No. Of units |

12 | Electricity | Kilowatts - hour |

13 | Cable | Meter or Kilometer |

14 | Steel | Tones |

15 | Chemical | Liter, Kilogram, Tone |

16 | Canteen | Number of Meals, Number of cups of tea or coffee |

17 | Gas | Cubic Meter |

18 | Boiler | Kilograms |

19 | Metal Plating | Square meters |

20 | Flour Mills | Sack of flour |

Q10) What is the procedure of Cost accumulation in unit costing?

A10) Cost accumulation procedure in unit costing

Cost details for the varied elements of cost are collected from financial records. Thereto end; you'll properly design your financial records. Therefore, you are doing not got to maintain a separate set of books to gather costing information. The subsequent costing information is required for unit costing:

1. Value of raw materials consumed

Material request documents are the idea for collecting the worth of staple consumption. Materials are only issued supported approved material request documents.

Approval documents provide details on the quantity of fabric with different grade and sort values. If the fabric is broken during storage and handling, we'll increase and adjust the difficulty price of the fabric to point normal loss. Unusual losses should be charged to the costing of the earnings report.

2. Labor costs

Labor are often divided into two categories: direct labor and indirect labor. If workers are engaged in direct manufacturing activities, they're treated as direct labor and may identify and calculate direct labor with the assistance of production details. Several workers engaged generally factory activities. They will be placed in several categories of wage tables.

3. Overhead

Overhead is assessed on a functional basis for unit costing purposes. Factory overhead or production overhead, office and management overhead, and sales and distribution overhead are categories of overhead. These overhead costs are collected at a given rate for costing purposes.

The actual overhead incurred is collected from the financial records. Cost statements are made at short intervals with the assistance of certain overhead costs.

Q11) Define Job Costing.

A11) Job costing generally refers to the specific accounting method used to track the costs of creating your own products. The job costing form has space to include direct labor, direct materials, and overhead costs.

Job costing meaning

The cost remains in the work in process account throughout the job. When the jobs are finally completed, they will be transferred to the finished product account. Using this method, accountants can understand the complex work that is going on towards the process of completion.

Overhead, such as overhead, is applied as part of the overhead. Use of association with working hours or activity-based costing. In this way, by using the workforce or certain tools, overhead costs are not excluded from the equation and companies can use job costing to ensure that they cover all significant costs.

Industries that produce products as a job use this method. This includes, but is not limited to, job costing of construction. Shipping, auditing, maintenance and repair, installation, and any industry that creates products that are specific to their needs. Job costing is often the most efficient method in this situation.

Job costing Example

For example, Roy was once a curator at a large museum in the United States. He has connected with the scientific community at various levels and enjoyed his career. After a while, Roy decided to change jobs. Since then, he has set up a company that provides maintenance work for historical works in museums.

Roy has all the connections needed for this business, including other curators, archaeologists, and his entire Rolodex community. After a little effort, he was able to connect with the people doing this job. Roy acts as a salesperson, but he had to hire a team to perform the operation. Roy is a huge success. One of his concerns, an area of ignorance to him, is how bookkeeping is done. So he hires an accountant, holds a meeting, and begins learning how his business overcomes this need.

Meaning and definition of job costing:

Job costing as a characteristic method is a specific form of order costing that is adopted to perform work strictly according to customer specifications. The manufacturing process depends on the members of your order. Such production is not standardized and is essentially intermittent. Manufactured goods are not for storage, but for delivery as soon as they are completed in all respects.

All work orders are different for each customer, so costs are identified individually for each job. The purpose of job costing is to see the profits or losses incurred in each job. The cost of additional work is compared to the estimated cost to indicate whether the estimate was incomplete or the actual cost incurred was excessive. Such an analysis will help improve efficiency and take corrective action to facilitate the correction of estimates.

According to Eric Caller, "Job costing is a method of costing, with continuously identifiable units, applicable materials, labor, and specific quantities of products and equipment that move the production process as direct costs. The costs of repairs, repairs, or other services are summarized. Normally, the calculated portion of the overhead is charged to the job order.

From the above definition, it is clear that job costing is a costing method that allows you to see the cost of each job individually. This is a specific form of order costing that applies when work is done to meet the special requirements of the customer. Unlike contract costing, each job has a relatively short duration.

Features of job costing:

The features of job costing are as follows:

(1) Job costing is adopted due to manufacturing and non-manufacturing concerns.

(2) Following the job costing method These concerns produce goods for specific orders from customers, not inventory.

(3) Job costing is adopted when the work done is analyzed into different jobs and each job is considered as a separate cost unit.

(4) From the start date to the completion date, a separate account will be opened for each job for which all costs incurred in that job will be deducted. This allows concerns to know the cost of each job.

(5) In job costing, the cost of each job is confirmed after the job is completed.

(6) Since each job is different from other jobs, each job needs to be processed individually under job costing.

(7) By comparing the actual cost of each job with the price charged to each job, you can see the profit or loss incurred by each job.

(8) In this method, the cost of each job and the profit or loss of each job are calculated separately.

(9) With this method, production is intermittent, not continuous.

(10) The industry does not have to bear the sales and distribution costs because the customer places the order and collects the goods after production.

Examples of industries that employ job costing include foundries, printers, machine tool manufacturing, engineering workshops, toy manufacturing concerns, furniture manufacturing concerns, management consulting concerns, upholstery, musical instruments, and advertising concerns.

Q12) What are the main Objectives of job costing?

A12) All work orders are different for each customer, so costs are identified individually for each job. The purpose of job costing is to see the profits or losses incurred in each job. The cost of additional work is compared to the estimated cost to indicate whether the estimate was incomplete or the actual cost incurred was excessive. Such an analysis will help improve efficiency and take corrective action to facilitate the correction of estimates.

According to Eric Caller, "Job costing is a method of costing, with continuously identifiable units, applicable materials, labor, and specific quantities of products and equipment that move the production process as direct costs. The costs of repairs, repairs, or other services are summarized. Normally, the calculated portion of the overhead is charged to the job order.

From the above definition, it is clear that job costing is a costing method that allows you to see the cost of each job individually. This is a specific form of order costing that applies when work is done to meet the special requirements of the customer. Unlike contract costing, each job has a relatively short duration.

The main objectives are of job costing are:

1) The main purpose of job costing is to see the cost and profit or loss of each job.

(2) Another purpose of job costing is to find highly profitable and low-profitable or low-profitable jobs.

(3) Cost management by comparing the actual cost with the estimated cost is also one of the purposes of job costing.

(4) Job costing also aims to show whether the estimation is incorrect or the actual cost is excessive by comparing the actual cost of the job with its estimated cost.

(5) Another purpose of job costing is to provide a basis for estimating or determining the cost of similar work to be done in the future.

Similarities between job costing and contract costing

(1) Both individual costing and contract costing are specific order costing.

(2) For both job costing and contract costing, each job or contract constitutes a cost unit.

(3) Both methods have the same purpose of finding costs and benefits.

(4) Either method will open another account.

(5) Since customers come by either method, there is no demand creation in either case.

(6) Either method will work according to the customer's specifications.

(7) In either case, work will start after receiving an order from the customer.

(8) In both cases, the customer will call you a quote before ordering.

Q13) Explain the Procedure of job costing.

A13) The procedures that are generally applicable to regular sales transactions also apply to job costing.

1. Accepting inquiries:

Before placing an order with the manufacturer, customers typically inquire about price, quality to maintain, duration of order, and other job specifications.

2. Job price quote:

Cost calculators estimate the cost of a job, taking into account various factors of cost and keeping customer specifications in mind. It is based on the cost of running similar jobs from the previous year and takes into account changes that may occur due to various factors in the cost. The prospect is then notified of the estimated cost of the job.

3. Receipt of order:

The customer places an order if he / she is satisfied with the quoted price and other job execution conditions. The production control department receives orders and assigns a number called the job order number to each received order. The job will be recognized by this number until it completes.

4. Preparation of manufacturing instructions:

The production instructions created by the production control department are sent to related parties such as employees so that they can carry out their duties. It is also sent to the shopkeeper so that all the necessary materials can be stored and sent to the costing officer. Create a job cost sheet to see the profits of all completed jobs.

The production order consists of the following details:

(I) The date the order was prepared,

(II) Job order number,

(III) Description of the products produced,

(IV) Number of products produced,

(V) Work start date,

(VI) Work completion date,

(VII) List of materials used,

(VIII) Sequence of manufacturing process,

(IX) Signature of production manager, etc.

5. Design preparation:

If the work you perform requires special processing, the production planning department will create a design that meets your specifications. This is done by the engineering department in consultation with the production planning department.

6. Job execution and its inspection:

Start the job according to the production schedule. Complete production with the materials, employees, tools and more you need. The production process is overseen from time to time by the production manager or supervisor to ensure that the jobs performed are in compliance with customer specifications and completed according to the production schedule.

7. Shipping of goods:

The finished product is then packed according to the delivery schedule and delivered to the customer. Payments will be settled according to the agreed payment method.

8. Accounting system under job costing: When a job is performed directly on the job, the employee records the job number to indicate that the job is a direct job. The costing department collects all working hours tickets, records the employee's wage rate on the ticket, and calculates the labor cost of the work.

Treatment of overtime pay in job costing:

If overtime is done to speed up production for the purpose of shortening delivery times, overtime is debited to work that is done as part of the factory's daily work. Overhead.

9. Direct expenses:

Direct costs in the job ordering industry typically include design, molds, hiring specialized tools and equipment, and maintenance costs for such tools.

10. Factory overhead:

In most cases, pre-determined overhead is used to absorb factory overhead. The pre-determined overhead rate is calculated at the beginning of the year by estimating the total overhead for the year and dividing by one

Q14) What are the four components to cost?

A14) There are four components to cost (that is, materials, labor, billable costs, and overheads), which also apply to job costing.

They are discussed as follows:

1. Material cost:

Materials are classified into direct and indirect materials based on the traceability of the material to work. Materials that can be tracked by the job are treated as prime cost factors, and materials that cannot be tracked by the job are treated as manufacturing overhead.

2. Direct labor costs: Direct labor costs are debited to jobs where the work is done directly. Clock cards are used to record the working hours of each employee. At the end of each week, the payroll department uses the information on the clock card to calculate the salary for each employee. The clock card only records the total working hours of each employee.

It is used to indicate how much time an employee has worked during that period, and the employer is used to determine how much to pay the employee for that job. The clock card does not record the time each employee spends on work. This information is recorded on the time ticket by the employee. The time ticket shows the date the work was completed, the name of the employee, the name of the department, and the start and end times of the work.

When a job is performed directly on the job, the employee records the job number to indicate that the job is a direct job. The costing department collects all working hours tickets, records the employee's wage rate on the ticket, and calculates the labor cost of the work.

Treatment of overtime pay in job costing:

If overtime is done to speed up production for the purpose of shortening delivery times, overtime is debited to work that is done as part of the factory's daily work. Overhead.

3. Direct expenses:

Direct costs in the job ordering industry typically include design, molds, hiring specialized tools and equipment, and maintenance costs for such tools.

4. Factory overhead:

In most cases, pre-determined overhead is used to absorb factory overhead. The pre-determined overhead rate is calculated at the beginning of the year by estimating the total overhead for the year and dividing by one.

Direct working costs or direct working hours. Over the year, overhead costs are applied to calculate overhead costs and are therefore charged to the job.

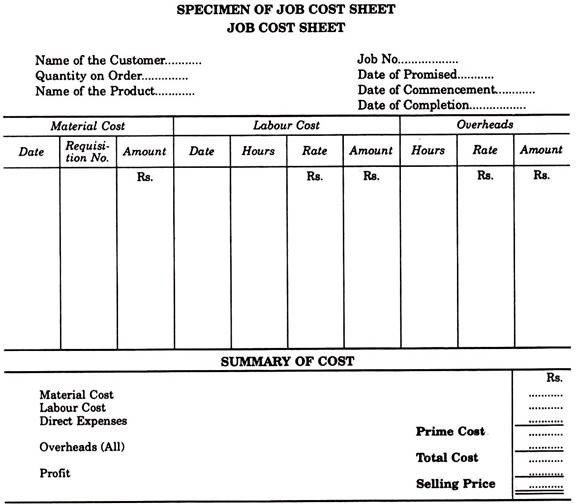

Q15) Draw the specimen of cost sheet.

A15) Job costing creates a job costing sheet for every job. It shows the cost data associated with the job. It shows different factors of cost, such as direct materials, direct labor, direct costs, and overhead costs under different cost categories such as prime cost, working cost, production cost, total cost. It also describes selling prices and profits or losses at work.

Advantages of job costing:

(1) It is convenient to check the cost and profit or loss of each job individually.

(2) It helps management to know about the profitability of their work.

(3) Ideal for cost plus contracts.

(4) Provides a detailed analysis of cost factors. This is very helpful in making cost estimates and estimates.

(5) This costing method makes it easy to identify corrupt or defective jobs and lock their responsibilities to specific departments or individuals.

(6) Job costing data is very useful for preparing future budgets.

(7) Cost data related to completed jobs helps managers understand trends in material costs, labor costs, and overhead costs and manage future job costs.

Limitations of job costing

(1) Increased clerical work for collecting expenses. In addition, it includes more directors. These increase costs and increase costs.

(2) With this costing method, it is necessary to collect costs for many small jobs. Therefore, the potential for error in cost collection lies in job costing.

(3) Job costing, which is historical in nature, is not very useful for cost control unless combined with estimated or standard costing.

Q16) Give an example to explain Batch Costing.

A16) Specific order costing is also called batch costing. Job costing refers to the job costing performed on a particular order, but in batch costing, the material is manufactured for inventory. The finished product may require different components to assemble and may be manufactured in economical batch lots.

When you receive orders from different customers, the orders have a common product. You can then place a job in batch that consists of a given quantity of each type of product. In such cases, the batch costing method is used to calculate the cost of each batch.

The cost per unit is determined by dividing the total cost of the batch by the number of items produced in that batch. For that purpose, a batch cost sheet is available. Creating a batch cost sheet is similar to creating a job cost sheet. This method is mainly applied to biscuit manufacturing, garment manufacturing, spare parts and component manufacturing, pharmaceutical companies, etc.

Illustration

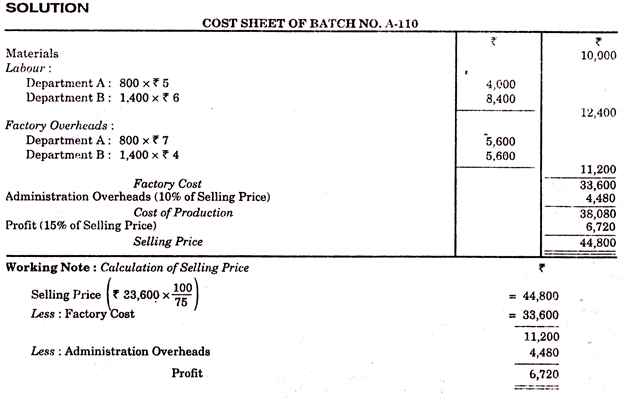

Batch number A-110 incurred the following costs:

Direct material Rs10,000

Department: 800 working hours at 500 rupees per hour

B1400 Working hours @ 6 rupees per hour

Factory overhead is absorbed on a working hour basis, with rates of Rs 7 per hour for department A and Rs 4 per hour for department B. The company uses a cost plus system to sell prices and expects a gross profit of 25% (sales minus factories). Cost). The management fee is absorbed at 10% of the selling price. Calculate the selling price per unit, assuming that A-110 units were produced in batch A-110.

Production is usually done in batches, and each batch can contain any number of component units. The optimum quantity for a batch is the quantity that minimizes setup and shipping costs. Such optimal quantities are known as economical batch quantities or economical lot sizes.

Economical lot size determination is important in industries where batch costing is employed.

Need for determining economic lot size:

(I) Every time you create a component / product, you need to set up the tool. This causes a loss of production time. Therefore, to reduce the cost per unit, the maximum number of units is generated when the machine is configured.

(II) Such mass production in a single run leads to the accumulation of inventory and associated costs.

(III) Therefore, there are quantities in which the reduction in production costs is offset by the transportation costs of the quantity inventory. Many factors related to cost and economy needs to be considered in determining the most economical batch quantity.

Illustration:

Check the economic batch quantity from the details below.

Annual demand Rs.9,600

Setting cost Rs.200

Production cost per unit Rs.50

Interest rate 10% p.a.

Solution

Q17) Explain the procedure and treatment of Contract costing.

A17) Contract costing, unlike short-term jobs, is a special system of job costing that applies to long-term contracts. Contract costing applies primarily to civil engineering and engineering projects, shipbuilding, road and rail contracts, bridge construction, and more.

Contract costing may be a sort of specific order costing. This applies to contracts that take a considerable amount of time to complete and fall into different accounting periods. However, periods longer than one year are not an essential feature of long-term contracts. Some contracts with a term shorter than one year should be accounted for as long-term contracts if they are significant enough for the activity of that term.

CIMA defines contract costs and contract costs as follows:

The total price related to one contract specified as a price unit."

Features of contract costing:

Contracts to which contract costing applies have the following features:

(A) The contract is based on the special requirements of the customer.

(B) The contract period is relatively long.

(C) Contract work is done on-site, unlike manufacturing under the roof.

(D) Contract work mainly consists of construction activities.

Accounting procedure for contract costing:

If there are many contracts, an identification number and name are given to each contract for accounting and management reasons. A separate contract account is maintained for every contract.

All costs associated with the contract will be charged to each contract account. In the contract cost structure, the majority of spending is of a direct nature in the form of materials, wages, plant and store use, direct costs, etc., and only a small portion is charged as allocated overheads.

Accounting Treatment of Costs:

1. Material:

(A) All materials purchased for the contract or sent to the site will be charged for the contract.

(B) If the material is returned to the store, or is on an unused site, or if the material is transferred to another contract site, it will be credited to the contract account.

(C) If the material is not needed immediately, the material will be stored and its costs will be debited to the stock account.

2. Labor:

All labor employed or worked in the field is treated as direct labor and all costs associated with them are charged to the contract account. Salaries and incentives for management and supervisory staff of a particular contract are also charged for that particular contract.

3. Plants:

(A) If the plant is hired, the employment fee will be charged to the contract account.

(B) If the plant was specially purchased for a contract or the plant was sent to the site, the value of the plant is debited to the contract account. The value of the returned or remaining on-site plant will be credited to the contract account. The balance between the debited amount and the credited amount in the contract represents the value of the plant used in the field.

(C) The depreciation amount provided by the plant may be debited to the contract account instead of displaying the value of the plant issued to the site and remaining on the site.

4. Subcontract fee:

Part of the contract work may be provided on a subcontract basis and payments made in the subcontract work may be debited to the contract account.

5. Overhead:

General overhead and head office expenses are fairly distributed to different contracts, and some overhead is charged to the contract account.

6. Difficulty of cost control:

Contracts are generally large and contract work is done on-site. This causes some problems with material use, labor utilization, labor supervision, plant and work damage, material and tool theft, and more. This site-based work makes it difficult to control the cost of contracts.

7. Surveyor Certificate and Deposit:

In contract work, surveyors, architects, and civil engineers visit the site on a regular basis to inspect the completed work. He issues a certificate stating the completion stage of the work and the value of the work completed by the certificate issuance date. Payment will be released to the contractor by the contractor based on the certificate.

Payments are typically released only up to a certain percentage, for example 80% of certified work. The balance of certified work is retained by the contractor until the entire contract is successfully completed.

The amount of money so reserved is called a "reservation". The contractor does so to protect itself from the risks that may arise from the contractor. Generally, the percentage of retained earnings is up to 20% of the amount of certified work.

8. Work in progress:

The amount of work in process includes the value of certified and uncertified work in process as it appears in your contract account.

9. Cost of running contract:

Due to the long-term nature of the contract, it was necessary to determine the profit attributable to each accounting period. For long-term contracts, it is believed that the results can be evaluated with reasonable certainty before they are signed, and imputed profits should be carefully calculated and included in the current account.

The profits taken up should be based on the principles of standard costing. For completed contracts, all profits arising from the contract can be transferred to the income statement.

However, in the case of an incomplete contract, preparations are made to deal with unforeseen circumstances and unexpected losses, so depending on the scope of work completed in the contract, only part of the profit is reflected in the income statement Will be done. There are no strict rules for calculating profits reflected in the income statement.

However, in general, the following principles are followed:

(1) If an incomplete contract causes a loss, the entire loss will be debited to the income statement.

(2) Profit should only be considered for certified jobs. Uncertified work should be evaluated at cost.

(3) Contract completion is less than 25% of the contract price – no profit should be recorded on the income statement and the entire amount is retained as a reserve for contingencies.

(4) Contract completion up to 25% or more, less than 50% of the contract price – in this case, one-third of the profit, a decrease in the ratio of cash received to the certified work will be reflected in the profit and loss. Account. The balance remains as a reserve in case of contingency.

(5) Contract completions up to 50% or more and less than 90% – in this case, two-thirds of the profit is reduced by the percentage of cash received for the work authorized to be brought into the income statement, leaving the rest Keep up the amount of reserve.

The formula is given below: