UNIT 3

ACHIEVING SUCCESS AT WORK: COORDINATION AND CONTROL

Q1) Explain the meaning and need of Coordination.

A1) Co-ordination can be defined as the orderly arrangement of group efforts to provide unity of action in the persuit of common objectives. It is the integration or synchronization of activities or action. The activities of individuals and departments are linked with each other, so that they work most effectively together in accomplishing goals of the organization. Co-ordination is the essence of management as in order to coordinate the activities of his subordinates, a manager has to perform all the other functions of management, viz., planning, organizing, staffing, directing and controlling.

Theo Haimann states that, “Co-ordination is the orderly synchronizing of efforts of the subordinates to provide the proper amount, timing and quality of execution so that their efforts lead to the stated objective, namely the common purpose of the enterprise.”

There is a need for coordination in every function of management. It is a process of integration of the activities of the members of an organization to accomplish organizational goals. There is a need to have proper coordination throughout the organization.

(i) The top level managers co-ordinate the activities of the middle level managers.

(ii) The middle level managers coordinate the activities of the lower level managers.

(iii)The lower level managers co-ordinate the activities of their subordinates.

Co-ordination refers to inter-linking of actions. There is a need for co-ordination throughout the organization and at all levels.

Need for Co-ordination

Coordination is needed in the organisation for the following reasons:

1) Large number of employees: In the corporate sector, the number of employees is large and it becomes necessary to co-ordinate the activities of the individual to attain common enterprise goal.

2) Team spirit: Co-ordination develops team spirit in the organization. Superiors coordinate the activities of their subordinates for the purpose of achieving group objectives. For this purpose, managers need to develop team spirit among their subordinates.

3) Unity of action ensured: The departmental goals are set towards achievements of overall objectives and co-ordination helps in integrating the efforts of all the individuals towards a common goal.

4) Reduced conflict of interest: Co-ordination blends the interest of all departments into one common objective thereby reducing conflicts of interest of each department.

5) Interdependence of Departments: One department cannot do work alone. The performance of one department is the input of other department. This link is necessary to integrate jobs in all the departments for maximum returns, and this is done by the function of co-ordination.

6) Encourage Initiative: Effective co-ordination encourages subordinates to make use of initiative. Employees may come up with new ideas, and they may provide effective suggestions.

7) Corporate image: Co-ordination develops a better image for the Organization. Co-ordination enables the Organization to achieve its goals. There can be better quality of goods and services. This enables the firm to earn name and goodwill for the Organization.

8) Optimum use of resources: Co-ordination facilitates optimum use of resources. There is optimum use of both physical and human resources. The resources of the Organization are put to best possible use by the members of the Organization.

9) Higher Efficiency: Efficiency can be measured in terms of returns and costs. Higher efficiency is a result of high returns and low costs due to optimum utilizations of resources. So co-ordination leads to high efficiency.

Q2) Explain the meaning and need of control.

A2) After the planning, organising, staffing and directing have been carried out, the final managerial function of controlling assures that the activities planned are being accomplished or not. Control is a primary goal-oriented function of management in an organisation. Control can be defined as the process of analysing whether actions are being taken as planned and taking corrective actions to make these to confirm to planning. It is a process of comparing the actual performance with the set standards in order to ensure that activities are performed according to the plans and taking corrective action, if necessary. Controlling is performed at the lower, middle and upper levels of the management.

The managerial function of controlling is defined by Koontz and O’Donnell as, “the measurement and correction to the performance of activities of subordinates in order to make sure that enterprise objectives and the plans devised to attain them are being accomplished.”

George R. Terry remarked, “Controlling is determining what is being accomplished, that is evaluating the performance and, if necessary, applying corrected measures so that the performance takes place according to plans.”

Thus, management control is the process by which managers assure that resources are obtained and used effectively and efficiently in the accomplishment of the organisation’s objectives. Further, it is defined as the process by which managers in the organisation assure that activities and efforts are producing the desired objectives in the organisation.

Need for Control:

Controlling helps the management and the organization in many ways. It is an indispensable part of management. Planning will be meaningless in the absence of controlling. The importance of controlling is briefly stated below:

Q3) Discuss the techniques of co-ordination.

A3) The following measures or techniques need to be adopted in practice as tools for securing better co-ordination in the working of an organisation:

1. Simplified Organisation: In large organisations, there is a tendency towards over- specialisation. The organisation gets divided into an entire series of units all of which concentrates just on its own task. In fact, each unit tends to be bureaucratic and its activities become ends in themselves instead of being means to the general ends of the organisation. This creates problems of co-ordination. The remedy for this lies in placing the closely-related functions and operations under the charge of an executive who functions as a coordinator. Re-arrangement of departments can also be considered to cause a greater deal of harmony among the varied wings of the organisation.

Furthermore, clear-cut organisation structure and procedures that are well-known to all concerned will ensure co-ordination. Organisational procedures should cover all activities and every person must tend to understand what he's liable for and how his work is said thereto of other individuals.

2. Harmonized Programmes and Policies: The ideal time to cause co-ordination is at the planning stage. The plans prepared by different individuals or divisions should be checked up to make sure that they all fit together into an integrated and balanced whole. The coordinating executive must make sure that all the plans add up to a unified programme. Moreover, co-ordinated activities must not only be according to each other, but even be performed at the right time.

3. Well-designed Methods of Communication: Good communication brings about proper co-ordination and helps the members of a business organisation to work together. Flow of communication will facilitate co-ordination and smooth working of the enterprise. The utilization of formal tools like orders, reports and dealing papers, and informal devices just like the grapevine will provide adequate information to all or any concerned. Continuous, clear and meaningful communication provides every member with a clear understanding of the character and scope of his work also as that of other persons whose responsibilities are associated with him. This aids the executives in coordinating the efforts of the members of their teams.

4. Special Coordinators: Generally, in big organisations, special coordinators are appointed. They normally add staff capacity to facilitate the working of the main managers. A co-ordination cell can also be created. The basic responsibility of the cell is to gather the relevant information and to send this to varied heads of sections or departments in order that inter-departmental work and relationship are co-ordinated.

5. Co-ordination by Committees: Co-ordination in management by committees is achieved through meetings and conferences. Sometimes different committees are appointed to look after different areas of management, namely, Purchase Committee, Production Committee, Sales Committee, finance committee, etc. These committees take the group decision by exchanging their views and ideas then it is coordinating elements.

6. Group Discussion: Group discussion is another tool for co-ordination. It provides opportunities for free and open exchange of views and interchange of ideas, problems, proposals and solutions. Face-to-face communication enables the members to achieve improved understanding of organisation-wide matters and results in better co-ordination.

7. Voluntary Co-ordination: In ideal conditions, co-ordination should happen through voluntary co-operation of the members. Each department or section or individual affects others and is additionally affected by others. Therefore, if those departments, sections or individuals apply a way of working which facilitates others, voluntary co-ordination is achieved. This will be done by horizontal communication.

8. Co-ordination through Supervision: The supervising executives have a vital part to play in coordinating the work of their subordinates. Where the work-load of an executive is so heavy that he cannot find adequate time for co-ordination, staff assistants could also be employed. They will recommend to the senior official the action that he may take for ensuring co-ordination.

The cardinal principle involved in co-ordination is that the balancing and keeping together the various activities for a well-knit aggregate function, and its effectiveness depends upon satisfactory delegation of authority, sharing of responsibilities and accountability, and proper supervision—keeping in sight the oneness of the organisation.

Q4) Explain the difficulties in establishing coordination.

A4) The following factors are responsible within the way of effective coordination:

i. Lack of Administrative Talent: Selection of inefficient personnel leads to ineffective coordination.

ii. Clash of Interests: Often individuals are pursuing narrow personal interests by sacrificing organizational interests. Sometimes, individuals fail to know how the achievement of organizational goals will satisfy their own goals. As a result, there exists a conflict between individual goals and organizational goals.

iii. Differences in Attitudes and dealing Styles: Every individual has his own way of handling problems. Moreover, there are differences in attitudes of people to achieve a selected goal. Above all, the capacity and talent of individuals differ widely. This leads to ineffective coordination.

iv. Complexity of Operations: In a big organization, an outsized number of individuals process the work on various levels. It is going to be difficult to speak the policies, orders, and managerial actions on a face-to-face basis. If the operations of a corporation are diversified and sophisticated, then the necessity for coordination is felt everywhere. The large size of an operation brings about problems of coordination.

v. Specialization: Specialists lookout of varied specialized functions (such as purchasing, production, finance, marketing, etc.). They are more curious about developing their own departments. They pursue their own special interests at the value of organizational goals. This leads to ineffective coordination.

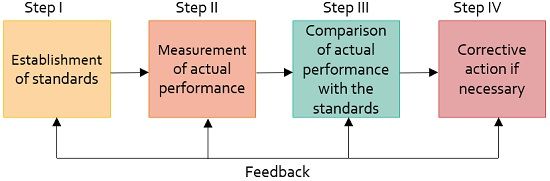

Q5) Explain the steps in the process of control.

A5) Control process involves the following steps as shown in the figure:

Q6) Discuss the techniques in establishing control.

A6) Control is a fundamental managerial function. Managerial control regulates the organizational activities. It compares the actual performance and expected organizational standards and goals. For deviation in performance between the actual and expected performance, it ensures that necessary corrective action is taken.

There are various techniques of managerial control which can be classified into two broad categories namely- 1. Traditional techniques and, 2. Modern techniques.

Traditional Techniques of Managerial Control

Traditional techniques are those which have been used by the companies for a long time now. These include the following:

1. Personal Observation:

This is the most traditional method of control. Personal observation is one of those techniques which enables the manager to collect the information as first-hand information. It also creates a phenomenon of psychological pressure on the employees to perform in such a manner so as to achieve well their objectives as they are aware that they are being observed personally on their job. However, it is a very time-consuming exercise & cannot effectively be used for all kinds of jobs.

2. Statistical Reports

Statistical reports can be defined as an overall analysis of reports and data which is used in the form of averages, percentage, ratios, correlation, etc., present useful information to the managers regarding the performance of the organization in various areas. This type of useful information when presented in the various forms like charts, graphs, tables, etc., enables the managers to read them more easily & allow a comparison to be made with performance in previous periods & also with the benchmarks.

3. Break-even Analysis

Breakeven analysis is a technique used by managers to study the relationship between costs, volume & profits. It determines the overall picture of probable profit & losses at different levels of activity while analyzing the overall position. The sales volume at which there is no profit, no loss is known as the breakeven point. There is no profit or no loss.

Breakeven point can be calculated with the help of the following formula:

Breakeven point = Fixed Costs/Selling price per unit – variable costs per unit

4. Budgetary Control

Budgetary control can be defined as such technique of managerial control in which all operations which are necessary to be performed are executed in such a manner so as to perform and plan in advance in the form of budgets & actual results are compared with budgetary standards.

Therefore, the budget can be defined as a quantitative statement prepared for a definite future period of time for the purpose of obtaining a given objective. It is also a statement which reflects the policy of that particular period. The common types of budgets used by an organization are:

Sales budget: A statement of what an organization expects to sell in terms of quantity as well as value.

Production budget: A statement of what an organization plans to produce in the budgeted period.

Material budget: A statement of estimated quantity & cost of materials required for production.

Cash budget: Anticipated cash inflows & outflows for the budgeted period.

Capital budget: Estimated spending on major long-term assets like a new factory or major equipment.

Research & development budget: Estimated spending for the development or refinement of products & processes.

Modern Techniques of Managerial Control:

Modern techniques of controlling are those which are of recent origin & are comparatively new in management literature. These techniques provide a refreshingly new thinking on the ways in which various aspects of an organization can be controlled. These include the following:

1. Return on Investment

Return on investment (ROI) can be defined as one of the important and useful techniques. It provides the basics and guides for measuring whether or not invested capital has been used effectively for generating a reasonable amount of return. ROI can be used to measure the overall performance of an organization or of its individual departments or divisions.

2. Ratio Analysis

The most commonly used ratios used by organizations can be classified into the following categories: Liquidity ratios, Solvency ratios, Profitability ratios, Turnover ratios.

3. Responsibility Accounting

Responsibility accounting can be defined as a system of accounting in which overall involvement of different sections, divisions & departments of an organization are set up as ‘Responsibility centers’. The head of the center is responsible for achieving the target set for his center.

4. Management Audit

Management audit refers to a systematic appraisal of the overall performance of the management of an organization. The purpose is to review the efficiency &n effectiveness of management & to improve its performance in future periods.

5. PERT & CPM

PERT (programmed evaluation & review technique) & CPM (critical path method) are important network techniques useful in planning & controlling. These techniques, therefore, help in performing various functions of management like planning; scheduling & implementing time-bound projects involving the performance of a variety of complex, diverse & interrelated activities.

Therefore, these techniques are so interrelated and deal with such factors as time scheduling & resources allocation for these activities.

Q7) Discuss the difficulties in establishing control.

A7) Control function has many contributions in the smooth functioning of the organization. However, there are difficulties in establishing proper control due to certain limitations. These are stated below:

1. Difficulty in setting quantitative standards: Control system loses its effectiveness when standard of performance cannot be defined in quantitative terms and it is very difficult to set quantitative standard for human behaviour, efficiency level, job satisfaction, employee’s morale, etc. In such cases judgment depends upon the discretion of manager.

2. No control on external factors: An enterprise can not control the external factors such as government policy, technological changes, change in fashion, change in competitor’s policy etc.

3. Resistance from employees: Employees often resist control and as a result effectiveness of control reduces. Employees feel control reduces or curtails their freedom. Employees may resist and go against the use of cameras, to observe them minutely.

4. Costly affair: Control is an expensive process it involves lot of time and effort as sufficient attention has to be paid to observe the performance of the employees. To install an expensive control system organisations have to spend large amount. Management must compare the benefits of controlling system with the cost involved in installing them.

The benefits must be more than the cost involved then only controlling will be effective otherwise it will lead to inefficiency.