UNIT II

Internal Reconstruction

Q1) What is Reconstruction? State the purpose of it.

A1) Rebuilding is the process of restructuring a company in terms of law, operations, ownership and other structures by revaluing assets and revaluing liabilities. It refers to the transfer of the business of a company or multiple companies to a new company. Therefore, this means that the old company will be liquidated, and therefore shareholders agree to acquire shares of equal value in the new company. The financial statements do not reflect the true and fair position of the business, as if the company has suffered losses over the years, it will need to be rebuilt and the net worth will be higher than the actual net worth. Hmm.

In other words, "reconstruction" is the dissolution of an existing company and the transfer of its assets and liabilities to a new company established for the purpose of business succession or succession of the existing company. Shareholders of the existing company will become shareholders of the new company. The business content and shareholders of the new company are almost the same as those of the old company.

Purpose of Reconstruction

The main purposes of the reconstruction are:

Q2) What are the types of Reconstruction?

A2) Types of Reconstruction

The company can be rebuilt in one of two ways. These are:

External Restructuring: If a company suffers losses over the past few years and faces a financial crisis, it can sell its business to another newly established company. In fact, the new company was established to take over the assets and liabilities of the old company. This process is called external reconstruction. In other words, external reconstruction means selling the business of an existing company to another company established for that purpose. In the external reconstruction, one company will be liquidated and the other will be newly established. The liquidated company is called the "Vendor Company" and the new company is called the "Purchasing Company". The shareholders of the selling company are the shareholders of the purchasing company.

Internal Restructuring: Internal restructuring refers to the internal restructuring of a company's financial structure. It is also called a restructuring that allows an existing company to survive. In general, equity capital is reduced to amortize the company's past cumulative losses.

Q3) Write the significance of Internal Reconstruction.

A3) Internal reconstruction is done by the company in the following cases:

Conditions and regulations regarding Internal Reconstruction

1. Approval by Articles of Incorporation: The company must be approved by the Articles of Incorporation to appeal for capital reduction. The Articles of Incorporation contain all the details of the company's internal affairs and refer to provisions that include how to reduce capital.

2. Passing a special resolution: The company must pass a special resolution before appealing for a capital reduction. Special resolutions will only be passed if a majority of stakeholders agree to internal reconstruction. This special resolution must be signed by the arbitral tribunal and deposited with a registrar appointed under the Companies Act 2013.

3. Court Permission: The company must obtain the court or the court's legitimate permission before starting the capital reduction process. The court will only grant permission if the company is fair and is satisfied with the positive consent of all stakeholders.

4. Borrowing Payment: According to Article 66 of the Companies Act 2013, a company must repay all the amount deposited and its interest before reducing its capital.

5. Creditor Consent: The company that reduces the capital requires the written consent of the creditor. The court requires the company to secure the interests of the dissenting creditors. The company obtains the court's permission after the court determines that the reduction of capital does not harm the interests of the creditors.

6. Announcement: The company must announce according to the instructions of the tribe for a capital reduction. The company must also explain the justification.

Q4) Distinguish between Internal and External Reconstruction.

A4) The main difference between internal reconstruction and external reconstruction

Due to the difference between internal and external reconstructions, the subsequent points are relevant:

- Internal restructuring is often defined as a restructuring of a corporation without liquidating an existing company and establishing a replacement one. On the opposite hand, external restructuring may be a sort of corporate restructuring that liquidates an existing company and creates a replacement company so as to continue the business of the prevailing company.

- A new company won't substitute the interior reorganization. Conversely, a replacement company are going to be established for external reconstruction and therefore the business of the prevailing company is going to be appropriated.

- Internal restructuring reduces the company's capital, and external liabilities like bond holders and creditors waive their debt at a reduction. On the opposite hand, external reconstruction doesn't reduce the company's capital.

- Internal reconstruction requires court approval and court confirmation, as a discount in capital stock can affect shareholder rights. On the contrary, external reconstruction doesn't require such approval.

- If the corporate goes through an indoor rebuilding process, the record created after the method will include the term "And Reduced". In contrast, within the case of external reconstruction, no particular term is employed on the record.

- In internal reconstruction, no new company are going to be established, so there'll be no transfer of assets or liabilities.

Basis For Comparison | Internal Reconstruction | External Reconstruction |

Meaning | Internal reconstruction refers to the method of corporate restructuring wherein existing company is not liquidated to form a new one. | External reconstruction is one in which the company undergoing reconstruction is liquidated to take over the business of existing company. |

New company | No new company is formed. | New company is formed. |

Use of specific terms in Balance Sheet | Balance Sheet of the company contains "And Reduced". | No specific terms are used in the Balance sheet. |

Capital reduction | Capital is reduced and the external liability holders waive their claims. | No reduction in the capital |

Approval of court | Approval of court is must. | No approval of court is required. |

Transfer of Assets and Liabilities | No such transfer takes place. | Assets and liabilities of existing company are transferred to the new company. |

Q5) What are the various methods of Internal Reconstruction?

A5) There are various methods of internal reconstruction, shown:

1. Alteration of Share Capital

If approved by the Articles of Incorporation, the limited liability company may change (change) the capital clause of the Articles of Incorporation. There are various ways to change stock capital:

Increase in stock capital due to issuance of new shares

2. Reverse Stock Split

Consolidation refers to the conversion of shares with a smaller par value to shares with a larger par value.

Example: His 5000 shares of Rs. 10 pieces can be integrated into a stock of 500 rupees. 100 each.

3. Stock Split

Subdivision is the conversion of high par value stocks to low par value stocks.

Example: 5000 shares of Rs. Each 100 can be split into 50000 shares of Rs. 10 each.

4. Equity of Shares

The company can convert its shares into shares. Stocks can be fractions that are not possible in the case of stocks. Central government approval is required to convert shares into shares.

5. Transfer of Shares

Reconstruction plans may require shareholders to relinquish some of their ownership. Such a waiver may be issued prior to immediate cancellation or to satisfy some of the company's creditors.

6. Cancellation of Unissued Shares

If the company cancels unissued shares, it does not need to pass an accounting entry. The authorized share capital of the company will be the amount of unissued shares currently cancelled.

Q6) Write short note on Stock Split and Consolidation.

A6) If approved by the Articles of Incorporation, the company may, by passing a normal resolution, decide at the General Assembly to split or consolidate the shares into an amount less or higher than the amount stipulated in the Articles of Incorporation. The ratio of paid-in to unpaid shares will continue to be the same as for the original shares.

Notifications identifying changes must be submitted to the Registrar within 30 days of the changes.

For example, a company with capital of 10,000,000 split into 10,000 shares and paid 75 for every 100 shares decides to split 100 shares of 100 shares into 10 shares to recognize capital. Each. The resulting entry passed in such a case is —

| Dr. | Cr. | |

| |||

Equity Share Capital ( 100) A/c | Dr. | 7,50,000 |

7,50,000 |

To Equity Share Capital ( 10) A/c |

| ||

(Being the sub-division of 10,000 shares of 100 each with 75 paid up thereon into 1,00,000 shares of 10 each with 7.50 paid up thereon as per the resolution of shareholders passed in the General Meeting held on...) | |||

Similar entries are passed when consolidating a smaller amount of stock into a larger amount of stock.

Q7) How are Fully Paid-In Shares converted to Shares?

A7) According to Article 61 of the Companies Act 2013, a company may convert fully paid-in shares into shares and convert the shares back into shares. If approved by the Articles of Incorporation, the company may, by passing a normal resolution, convert the fully paid shares into shares and reconvert the shares into shares at a general meeting of shareholders. Stock is the integration of equity capital into one of his units that can be split into aliquot parts. A stock is a fully paid bundle of stock that, for convenience, can be split into any amount and transferred to any fraction and subdivision, regardless of the original par value of the stock. He cannot have one share of equity capital, but he can transfer any amount of shares. However, in reality, the company limits the transfer of shares to multiples, such as 100 times his. Companies can convert fully paid shares into shares. When the company converts its shares into shares, the bookkeeping items only record the transfer from the stock capital account to the stock account. Another share registration will be initiated where the details of the member's holdings are entered and the annual returns change accordingly.

Example

C Ltd. Split the authorized capital of 5,000,000 into 100 shares each on March 12, 20X1, of which 4,000 were issued and paid in full. In June 220X2, the Company converted the issued shares into shares. Decided to do. However, in June 20X3, we reconverted the shares to his 10 shares and paid in full.

Pass an entry to show how equity capital appears in the balance sheet notes, such as 31-12-20X1, 31-12-20X2, 31-12-20X3.

Journal Entries

20X2 |

| |||

June | Equity Share Capital A/c | Dr | 4,00,000 |

|

| To Equity Stock A/c |

|

| 4,00,000 |

| (Being conversion of 4,000 fully paid Equity Shares of 100 into 4,00,000 Equity Stock as per resolution in General meeting dated…) |

|

|

|

20X3 |

|

|

|

|

June | Equity Stock A/c | Dr | 4,00,000 |

|

| To Equity Share Capital A/c |

|

| 4,00,000 |

| (Being re-conversion of 4,00,000 Equity Stock into 40,000 shares of 10 fully paid Equity Shares as per Resolution in General Meeting dated...) |

|

|

|

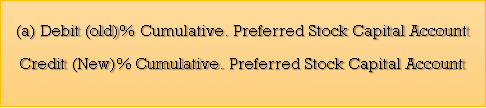

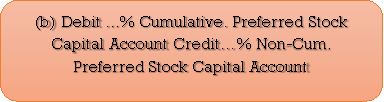

Q8) What does changes in Shareholder Rights mean?

A8) Under Article 48 of the Companies Act 2013, if a company issues different types of shares and grants such shares different rights or privileges, the rights relating to dividends, voting rights, etc. may be changed in any way. I will. This is done by the written consent of his three or more owners of her quarter of the issued shares of that type, or by a special resolution adopted at another meeting of the owners of the issued shares of that type. I will. (a) If the company's memorandum or articles of incorporation include provisions for such variations. Or (b) if there is no such provision in the Memorandum of Understanding or the Articles of Incorporation, or if such changes are not prohibited by the terms and conditions of issuance of shares of that class, provided that changes made by a shareholder of one class are the rights of another shareholder. When Impacting Regarding the type of shareholders, the consent of three-quarters of the other types of shareholders shall also be obtained and the provisions of this section shall apply to such changes.

For example, a company may (a) Change the dividend rate of preferred stock or (b) Convert cumulative preferred stock to non-cumulative preferred stock without changing the amount of equity capital by going through the following journal: can.

For example, a company may (a) Change the dividend rate of preferred stock or (b) Convert cumulative preferred stock to non-cumulative preferred stock without changing the amount of equity capital by going through the following journal: can.

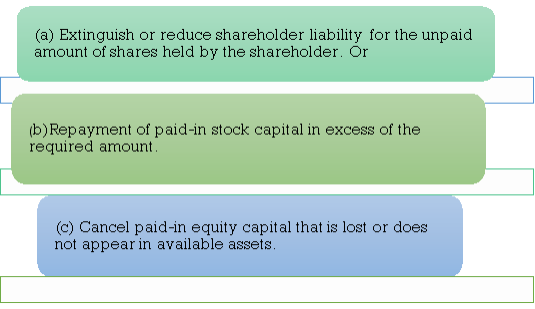

Q9) Explain the process of Reduction of Stock Capital.

A9) Article 66 of the Companies Act 2013 provides procedures for reducing stock capital. Subject to court confirmation of the company's application, the company may, by special resolution, reduce its share capital in the following ways:

In general, the reduction of equity capital occurs when a company suffers continuous losses over a long period of time and is not truly reflected in its assets. In such cases, the capital reduction scheme must amortize the portion of the capital that has already been lost.

This reduction is a shareholder sacrifice, and the amount of the reduction or sacrifice is credited to a new account called a capital reduction account (or restructuring account). The accounting process is as follows.

(a) Shareholders' liability to extinguish or diminish their liability for the accrued amount of shares held by the shareholders

The shareholders are not required to pay the accrued amount of their shares in the future. For example, a company decides to reduce 10 per share from 10 to 7.5 by cancelling the unpaid amount of 2.5 per share. The entry in this case looks like this:

Share Capital (Partly Paid-Up) Account Dr. ( 7.5 X No. of Shares)

To Share Capital (Fully Paid-up) Account ( 7.5 X No. of Shares)

(b) If the paid-in excess capital is refunded: If the company is unable to secure profitability, it may decide to refund the paid-in capital as excess to shareholders. For example, if a company with 10 fully paid shares each decides to refund 2 shares per share to make 8 fully paid shares, the entry would be:

Share Capital Account ( 10) Dr. ( 10 X No. Of Shares)

To Share Capital Account ( 8) ( 8 X No. of Shares)

To Sundry Shareholders Account ( 2 X No. of Shares) Sundry Shareholders Account Dr. ( 2 X No. Of Shares)

To Bank Account ( 2 X No. of Shares)

(c) If lost or hidden paid-in capital is cancelled:

Share Capital Account Dr. ( 90 X No. of Shares)

To Capital Reduction Account

(90 X No. Of Shares)

Q10) Draw the Proforma of Capital Reduction Account.

A10) Capital Reduction A/c

Particulars | Rs. | Particulars | Rs. |

To P & L A/c (Loss written off) To Goodwill A/c (Written off) To Preliminary expenses A/c (Written off) To Discount on Shares/Debentures (Written off) To Assets A/c (Decrease in value) To Bank A/c (payment of unrecorded liability) To Bank A/c (payment of Reconstruction Expenses) To Bank A/c (Refund of Directors Fees) To Capital Reserve (Balancing figure) | XX XX

XX

XX

XX

XX

XX XX XX | By Share Capital A/c (Amount of reduction) By Debentures A/c (Amount of Reduction) By Creditors A/c (Amount of Sacrifice) By Assets A/c (Increase in value) By Bank A/c (sate of unrecorded assets) | XX

XX

XX

XX

XX |

| XXX |

| XXX |

Q11) Following is the Balance sheet of M/s. Careful Ltd. As on 31st March, 2010.

Liabilities | Rs. | Assets | Rs. |

50,000 – 8% |

| Goodwill Freehold Property Leasehold Property Plant & Machinery Furniture Stock Debtors Preliminary Exp. Profit & Loss A/c | 1,00,000 1,50,000 2,40,000 3,00,000 1,00,000 50,000 1,00,000 9,000 2,07,000 |

Cumulative |

| ||

Preference Shares of |

| ||

Rs.10/- each. | 5,00,000 | ||

40,000 – Equity Shares of Rs.10/- each. | 4,00,000 | ||

|

| ||

Security Premium | 8,000 | ||

9% Debentures | 1,00,000 | ||

Accrued Debenture |

| ||

Interest | 6,000 | ||

Sundry Creditors | 1,00,000 | ||

Bank Overdraft | 1,42,000 | ||

| 12,56,000 |

| 12,56,000 |

Note –

- Preference dividend was in arrears for 3 years.

- There was a contingent liability of Rs.30,000/- for workmen compensation.

Following scheme of reconstruction was approved & implemented.

- The Preference shares were reduced to Rs.8/- per share fully paid & Equity Shares to Rs.3/- per share fully paid.

- One new Equity share of Rs.10/- each was issued of every Rs.50/- gross preference dividend in arrears.

- After reduction, both classes of shares were consolidated into Rs.10/- shares.

- The balance of Securities Premium was utilized.

- Plant & Machinery was written of down to Rs.2,50,000/-.

- Furniture was sold to Rs.75,000/-

- Preliminary expenses debit balance in Profit & Loss A/c, debt of Rs.25,000/- & obsolete stock Rs.18,000/- were to be written off.

- Contingent liability for which no provision has been made was settled at Rs.15,000/-. However, the amount of Rs.11,000/- was recovered from insurance company.

- Debenture holders agreed to Forgo principal amount by Rs.50,000/- & accrued debenture interest in full.

Pass journal entries. Prepare capital reduction account & Balance sheet after reconstruction.

A11)

Journal of Careful Ltd.

Date | Particulars | Debit (Rs.) | Credit (Rs.) |

1. | 8% Preference Share Cap. A/c.....Dr. (50,000X10) To 8% Preference Share Capital A/c (50,000X8) To Capital Reduction A/c (50,000X2) (Being reduction in 8% Preference Capital.) | 5,00,000 |

4,00,000

1,00,000 |

| 8% Preference Share Capital A/c….Dr. (40,000X8) To 8% Preference Share Capital A/c (32,000X10) (Being consolidation of 8% Preference Shares.) | 3,20,000 |

3,20,000 |

3. | Equity Share Capital A/c.........Dr. (40,000X10) To Equity Share Capital A/c (40,000X3) To Capital Reduction A/c (40,000X7) (Being reduction in Equity Share Capital) | 4,00,000 |

1,20,000 2,80,000 |

4. | Equity Share Capital A/c.........Dr. (40,000X3) To Equity Share Capital A/c (12,000X10) (Being consolidation of Equity Shares.) | 1,20,000 |

1,20,000 |

5. | Capital Reduction A/c............Dr. To Equity Share Capital A/c [(8%X5,00,000X 3)/50] (Being arrears of Preference dividend paid by issue of Equity shares.) | 24,000 |

24,000 |

6. | Security Premium A/c............Dr. To Capital Reduction A/c (Being Security Premium used.) | 8,000 |

8,000 |

7. | Bank A/c.....................Dr. Capital Reduction A/c...........Dr. To Furniture A/c (Being sale of Furniture at a loss of Rs.25,000/-) | 75,000 25,000 |

1,00,000 |

8. | Capital Reduction A/c...........Dr. To Bank A/c (Being payment of contingent liability.) | 15,000 |

15,000 |

9. | Bank A/c.....................Dr. To Capital Reduction A/c (Being recovery of claim from insurance company.) | 11,000 |

11,000 |

10. | 9% Debentures A/c.............Dr. Accrued Debenture interest A/c...Dr. To Capital Reduction A/c (Being sacrifice made by debenture holders) | 50,000 6,000 |

56,000 |

11. | Capital Reduction A/c...........Dr. To Plant & Machinery A/c (3,00,000 – 2,50,000) To Preliminary Expenses A/c To Profit & Loss A/c To Sundry Debtors A/c To Stock A/c To Capital Reserve A/c (Being losses & Assets written off.) | 3,91,000 |

50,000

9,000 2,07,000 25,000 18,000 82,000 |

Capital Reduction Account

Dr. Cr.

Particulars | Amt. | Particulars | Amt. |

To Equity Share Cap. A/c | 24,000 | By 8% Pref. Share Cap. A/c

By Equity Share Capital A/c By Security Premium By 9% Debentures

By Accrued interest on debentures By Bank (Insurance) |

1,00,000 |

(Preference Dividend) |

|

| |

To Furniture | 25,000 |

| |

To Plant & Machinery A/c | 50,000 | 2,50,000 | |

To Preliminary Expenses | 9,000 | 8,000 50,000 | |

To Profit & Loss A/c | 2,07,000 |

| |

To Sundry Debtors A/c | 25,000 |

| |

To Stock | 18,000 | 6,000 | |

To Bank | 15,000 | 11,000 | |

(Contingent liability) |

|

| |

To Capital Reserve | 82,000 |

| |

| 4,55,000 |

| 4,55,000 |

Balance Sheet of Careful Ltd (AND REDUCED)

| Notes | Current Year |

(in Rs.) | ||

EQUITY AND LIABILITIES |

|

|

Shareholders Fund |

|

|

Share Capital | 1 | 5,44,000 |

Reserves & Surplus | 2 | 82,000 |

Money Received against Warrants |

|

|

|

|

|

|

|

|

Share Application Money pending allotment |

|

|

|

|

|

Non-current Liabilities |

|

|

Long Term Borrowings | 3 | 50,000 |

Deferred Tax Liabilities (Net) |

|

|

Other Long Term Liabilities |

|

|

Long Term Provisions |

|

|

|

|

|

Current Liabilities |

|

|

Short Term Borrowings | 4 | 71,000 |

Trade Payables |

| 1,00,000 |

Other Current Liabilities |

|

|

Short Term Provisions |

|

|

|

|

|

|

|

|

Total |

| 8,47,000 |

|

|

|

ASSETS |

|

|

Non-current Assets |

|

|

Fixed Assets | 5 |

|

Tangible Assets |

| 6,40,000 |

Intangible Assets |

| 1,00,000 |

Capital Work-in-Progress |

|

|

Intangible Assets under development |

|

|

Non-current Investments |

|

|

Deferred Tax Assets (Net) |

|

|

Long Term Loans & Advances |

|

|

Other Non-current Assets |

|

|

|

|

|

Current Assets |

|

|

Current Investments |

|

|

Inventories |

| 32,000 |

Trade Receivables |

| 75,000 |

Cash and Cash Equivalents |

|

|

Short Term Loans & Advances |

|

|

Other Current Assets |

|

|

|

|

|

|

|

|

Total |

| 8,47,000 |

|

|

|

Schedules forming a part of Balance Sheet

Particulars | Amount Rs | Amount Rs |

1. SHARE CAPITAL |

|

|

Authorised Share Capital : |

| - |

--- Equity Shares of Rs.-- each |

|

|

|

|

|

Issued Subscribed and Paid Up Capital : |

|

|

14,400 Equity Shares of Rs.10 each |

| 1,44,000 |

4,00,000, 8% Preference shares of Rs 10 each |

| 4,00,000 |

|

|

|

Total |

| 5,44,000 |

|

|

|

2. RESERVES & SURPLUS |

|

|

|

|

|

Capital Reserve |

| 82,000 |

|

|

|

Total |

| 82,000 |

|

|

|

3. LONG TERM BORROWINGS |

|

|

Secured |

|

|

9% Debentures(1,00,000-50,000) |

| 50,000 |

|

|

|

Total |

| 50,000 |

|

|

|

4. SHORT TERM BORROWINGS |

|

|

Unsecured |

|

|

Bank Overdraft |

| 71,000 |

Total |

| 71,000 |

|

|

|

5. FIXED ASSETS |

|

|

Tangible |

|

|

Freehold Property | 1,50,000 |

|

Leasehold Property | 2,40,000 |

|

Plant & Machinery | 2,50,000 | 6,40,000 |

|

|

|

|

|

|

Intangible Assets |

|

|

Goodwill |

| 1,00,000 |

|

|

|

Total Assets |

| 7,40,000 |

Q12) Following is the Balance Sheet of Shobha Ltd. As on 31st March, 2020.

Liabilities | Amt. | Assets | Amt. |

Share Capital |

| Goodwill | 3,00,000 |

1,50,000 Equity Shares |

| Land & Building | 2,40,000 |

Of Rs.5/- each fully paid | 7,50,000 | Equipment | 2,10,000 |

|

| Sundry Debtors | 2,00,970 |

5,000 6% Preference Shares of Rs.100/- each fully paid |

5,00,000 | Stock Investment Cash at Bank | 3,32,440 44,000 21,000 |

8% Debentures | 3,00,000 | Profit & Loss A/c | 7,51,590 |

Bank Overdraft | 1,70,000 |

|

|

Sundry Creditors | 3,80,000 |

|

|

(including Rs.22,000 int. |

|

|

|

On Bank Overdraft) |

|

|

|

| 21,00,000 |

| 21,00,000 |

Note: Preference dividend is in arrears for Five years.

Following scheme of reconstruction was approved by the court.

1) Equity Shares be reduced to Rs.150/- each of then to be consolidated into shares of Rs.10/- each.

2) 6% Preference shares be reduced to Rs.50/- each & then to be subdivided into shares of Rs.10/- each.

3) Interest accrued but not due on 8% debentures. For half year ended 31st March 2008 has not been provided in the above Balance Sheet. The debenture holders have agreed to received 30% of this interest in cash immediately & provision for the balance be made in the books of account.

4) Rs.20,000/- be paid to Preference shareholders in lieu of arrears of Preference dividend.

5) The debenture holders have also agreed to accept equal number of 9% debentures of Rs.60/- each in exchange of 8% debentures of Rs.100/- each.

6) Bank has agreed to take over 50% stock in full satisfaction of its claim including interest. The remaining stock be revalued at Rs.80,000/-.

7) Investment be sold for Rs.39,000/-.

8) Tangible Fixed assets be appreciated by 15% & provision be made for doubtful debts of Rs.18,000/-.

Give journal entries for the above scheme of reconstruction. Prepare Capital Reduction Account in the books of Shobha Ltd. & Balance sheet of the company after reconstruction.

A12)

Journal of Shobha Ltd.

Sr No | Particulars | Debit (Rs.) | Credit (Rs.) |

1. | Equity Shares Capital A/c (5)......Dr. To Equity Share Capital A/c(1.50) To Capital Reduction A/c (3.50) (Being 1,50,000 Equity Shares of Rs.5/- each reduced to Rs.1.50 each.) | 7,50,000 |

2,25,000 5,25,000 |

2. | Equity Share Capital A/c (1.50)....Dr. To Equity Share Capital (10) (Being 1,50,000 Equity shares of Rs.1.50 consolidated into shares of Rs.10/- each.) | 2,25,000 |

2,25,000 |

3. | 6% Preference Share Capital A/c (100) ..Dr. To 6% Preference Share Capital A/c (50) To Capital Reduction A/c (Being 6% Preference shares of Rs.100/- each reduced to shares of Rs.50/- each.) | 5,00,000 |

2,50,000 2,50,000 |

4. | 6% Preference Share Capital A/c...Dr. To 6% Preference Shares Capital A/c (Being 6% Preference shares of Rs.50/- each subdivided into shares of Rs.10/- each.) | 2,50,000 |

2,50,000 |

5. | Capital Reduction A/c...........Dr. To Bank A/c To Interest on Debentures A/c (Being payment of accrued interest on debentures to the extent of 30% & provided for the balance.) | 12,000 |

3,600 8,400 |

6. | Capital Reduction A/c...........Dr. To Bank A/c (Being paid to preference share holders in lieu of arrears of dividend.) | 20,000 |

20,000 |

7. | 8% Preferences A/c (100)........Dr. To 9% Debentures A/c (60) To Capital Reduction A/c (Being exchanged 8% debentures by 9% debentures.) | 3,00,000 |

1,80,000 1,20,000 |

8. | Bank Overdraft A/c.............Dr. Sundry Creditors A/c............Dr. (Interest on Bank Overdraft) To Stock A/c To Capital Reduction A/c (Being taken over 50% of the Stock by the bank in satisfaction of bank overdraft.) | 1,70,000 22,000 |

1,66,220 25,780 |

9. | Capital Reduction A/c...........Dr. To Stock A/c (Being reduction in Stock.) | 86,220 |

86,220 |

10. | Bank A/c.....................Dr. Capital Reduction A/c...........Dr. To Investment A/c (Being sale of investment at a loss.) | 39,000 5,000 |

44,000 |

11. | Capital Reduction A/c...........Dr. To Profit & Loss A/c To Provision for doubtful debts A/c To Capital Reserve A/c (Being written off profit & loss account debit balance, provided for reduction redemption reserve & transferred the remaining amount to Capital Reserve Account.) | 8,65,040 |

7,51,590 18,000 95,470 |

12. | Land & Building A/c............Dr. Equipment A/c................Dr. To Capital Reduction A/c (Being appreciation in Land & Building & Equipment.) | 36,000 31,500 |

67,500 |

Capital Reduction Account

Dr. Cr.

Particulars | Amt. | Particulars | Amt. |

To Bank A/c | 3,600 | By Equity Share Capital A/c By 6% Preference Share Capital A/c By 8% Debentures A/c By Bank Overdraft & Creditors A/c By Land & Building A/c By Equipment’s A/c |

5,25,000

2,50,000 1,20,000

25,780 36,000 31,500 |

To Int. On debentures | 8,400 | ||

To Bank A/c | 20,000 | ||

To Stock A/c | 86,220 | ||

To Investment A/c | 5,000 | ||

To Profit & Loss A/c | 7,51,590 | ||

To Provision for doubtful |

| ||

Debts. | 18,000 | ||

To Capital Reserve | 95,470 | ||

| 9,88,280 |

| 9,88,280 |

Balance Sheet of Shobha Ltd (AND REDUCED)

| Notes | Current Year |

(in Rs.) | ||

EQUITY AND LIABILITIES |

|

|

Shareholders Fund |

|

|

Share Capital | 1 | 4,75,000 |

Reserves & Surplus | 2 | 95,470 |

Money Received against Warrants |

|

|

|

|

|

|

|

|

Share Application Money pending allotment |

|

|

|

|

|

Non-current Liabilities |

|

|

Long Term Borrowings | 3 | 1,80,000 |

Deferred Tax Liabilities (Net) |

|

|

Other Long Term Liabilities |

|

|

Long Term Provisions |

|

|

|

|

|

Current Liabilities |

|

|

Short Term Borrowings |

|

|

Trade Payables |

| 3,58,000 |

Other Current Liabilities | 4 | 8,400 |

Short Term Provisions |

|

|

|

|

|

|

|

|

Total |

| 11,16,870 |

|

|

|

ASSETS |

|

|

Non-current Assets |

|

|

Fixed Assets | 5 |

|

Tangible Assets |

| 5,17,500 |

Intangible Assets |

| 3,00,000 |

Capital Work-in-Progress |

|

|

Intangible Assets under development |

|

|

Non-current Investments |

|

|

Deferred Tax Assets (Net) |

|

|

Long Term Loans & Advances |

|

|

Other Non-current Assets |

|

|

|

|

|

Current Assets |

|

|

Current Investments |

|

|

Inventories |

| 80,000 |

Trade Receivables | 6 | 1,82,970 |

Cash and Cash Equivalents |

| 36,400 |

Short Term Loans & Advances |

|

|

Other Current Assets |

|

|

|

|

|

|

|

|

Total |

| 11,16,870 |

|

|

|

Schedules forming a part of Balance Sheet

Particulars | Amount Rs | Amount Rs |

1. SHARE CAPITAL |

|

|

Authorised Share Capital : |

| - |

--- Equity Shares of Rs.-- each |

|

|

|

|

|

Issued Subscribed and Paid Up Capital : |

|

|

22,500 Equity Shares of Rs.10 each |

| 2,25,000 |

25,000, 6% Preference shares of Rs 10 each |

| 2,50,000 |

|

|

|

Total |

| 4,75,000 |

|

|

|

2. RESERVES & SURPLUS |

|

|

|

|

|

Capital Reserve |

| 95,470 |

|

|

|

Total |

| 95,470 |

|

|

|

3. LONG TERM BORROWINGS |

|

|

Secured |

|

|

30,000, 9% Debentures of Rs 60 each |

| 1,80,000 |

|

|

|

Total |

| 1,80,000 |

|

|

|

4. OTHER CURRENT LIABILITIES |

|

|

Interest payable on debentures |

| 8,400 |

|

|

|

Total |

| 8,400 |

|

|

|

5. FIXED ASSETS |

|

|

Tangible |

|

|

Land & Building | 2,76,000 |

|

Equipments | 2,41,500 | 5,17,500 |

|

|

|

Intangible Assets |

|

|

Goodwill |

| 3,00,000 |

Total Assets |

| 8,17,500 |

|

|

|

6. TRADE RECEIVABLES |

|

|

Sundry Debtors |

| 2,00,970 |

Less: Provision for Doubtful Debts |

| (18,000) |

|

| 1,82,970 |

Q13) Following is the Balance sheet of Punjani Ltd. As on 31st March, 2020.

Liabilities | Amt. | Assets | Amt. |

16,000 12% Preference |

1,60,000

70,000

1,80,000

1,70,000

2,80,000

21,500

3,50,000 | Goodwill | 90,000 |

Shares of Rs.10/- each Fully paid up | Patents Land & Building | 50,000 1,50,000 | |

1,40,000 10% Preference shares of Rs.10/-, Rs.5/- per | Plant & Machinery Furniture Investment | 3,00,000 35,000 85,000 | |

Share paid up | Sundry Debtors | 3,00,000 | |

| Bills Receivables | 1,20,000 | |

18,000 Equity Share of | Bank | 30,000 | |

Rs.10/- each fully paid Up | Profit & Loss A/c | 71,500 | |

12% Debenture of |

|

| |

Rs.100/- each |

|

| |

11% Debentures of |

|

| |

Rs.100/- each |

|

| |

Interest due on |

|

| |

Debenture |

|

| |

Sundry Creditors |

|

| |

| 12,31,500 |

| 12,31,500 |

The following scheme of reconstruction was submitted & approved by the court.

1) 12% Preference Shares of the Rs.10/- each fully paid were reduced to 13% Preference Shares of Rs.10/- each, Rs.6/- per share paid up.

2) 10% Preference share of Rs.10/- each, Rs.5/- per share paid up were reduced to 13% Preference shares of Rs.10/- each, Rs.4/- per share paid up.

3) Equity Shares of Rs.10/- each fully paid were reduced to the denomination of Rs.7/- each fully paid.

4) 11% Debenture holders agreed to accept 44,800 Equity Shares of Rs.5/- each in full settlement of their claims.

5) Debentures holders agreed to Forgo the interest due on debentures.

6) Sundry Creditors agreed to Forgo 20% of their claims.

7) The company recovered as damages as sum of Rs.60,000/- which was not recorded in the books.

8) Cost of reconstruction was paid Rs.3,000/-.

9) Assets are to be revalued as under : Land & Buildings Rs.2,05,000/-, Plant & Machinery Rs.2,50,000/-, Furniture Rs.10,000/-, Investment Rs.1,05,000/-, Sundry Debtors Rs.2,77,000/-.

10) All intangible assets & accumulated losses are to be written off.

You are required to –

i) Pass journal entries in the books of Punjani Ltd.

Ii) Prepare Capital Reduction Account & Balance Sheet after reconstruction.

A13)

Journal of Punjani Ltd.

Date | Particulars | Debit (Rs.) | Credit (Rs.) |

1. | 12% Preference Share Capital A/c..Dr. To 13% Preference Share Capital A/c To Capital Reduction A/c (Being reduction in 12% Preference Capital.) | 1,60,000 |

96,000 64,000 |

2. | 10% Preference Share Capital A/c..Dr. To 13% Preference Share Capital A/c To Capital Reduction A/c (Being reduction in 13% Preference Capital.) | 70,000 |

56,000 14,000 |

3. | Equity Share Capital A/c.........Dr. To Equity Share Capital A/c To Capital Reduction A/c (Being reduction in Equity Share Capital.) | 1,80,000 |

1,26,000 54,000 |

4. | 11% Debenture A/c............Dr. To Equity Share Capital A/c To Capital Reduction A/c (Being reduction in debentures.) | 2,80,000 |

2,24,000 56,000 |

5. | Interest due on Debenture A/c.....Dr. To Capital Reduction A/c (Being interest dues on debentures cancelled.) | 21,500 |

21,500 |

6. | Creditors A/c.................Dr. To Capital Reduction A/c (Being Creditors dues reduced.) | 70,000 |

70,000 |

7. | Bank A/c.....................Dr. To Capital Reduction A/c (Being damages recovered.) | 60,000 |

60,000 |

8. | Capital Reduction A/c...........Dr. To Bank A/c (Being costs of reconstruction paid.) | 3,000 |

3,000 |

9. | Land & Building A/c............Dr. Investment A/c................Dr. To Capital Reduction A/c (Being increase in valuations.) | 55,000 20,000 |

75,000 |

10. | Capital Reduction A/c...........Dr. To Plant & Machinery A/c To Furniture A/c To Sundry Debtors A/c To Goodwill A/c To Patents A/c To Profit & Loss A/c To Capital Reserve A/c | 5,01,500 |

50,000 25,000 23,000 90,000 50,000 71,500 1,02,000 |

Capital Reduction Account

Dr. Cr.

Particulars | Amt. | Particulars | Amt. |

To Bank A/c | 3,000 | By 12% Preference Share Capital A/c By 10% Preference Share Capital A/c By Equity Share Capital A/c By 11% Debenture A/c By Interest due on Debentures By Sundry Creditors By Bank A/c By Land & Building A/c By Investment A/c |

|

To Plant & Machinery | 50,000 | 64,000 | |

To Furniture A/c | 25,000 |

| |

To Sundry Debtors A/c | 23,000 | 14,000 | |

To Goodwill A/c | 90,000 |

| |

To Patents A/c | 50,000 | 54,000 | |

To Profit & Loss A/c | 71,500 | 56,000 | |

To Capital Reserve A/c | 10,200 |

| |

|

| 21,500 | |

|

| 70,000 | |

|

| 60,000 | |

|

| 55,000 | |

|

| 20,000 | |

| 4,14,500 |

| 4,14,500 |

Balance Sheet of Punjani Ltd (AND REDUCED)

| Notes | Current Year |

(in Rs.) | ||

EQUITY AND LIABILITIES |

|

|

Shareholders Fund |

|

|

Share Capital | 1 | 5,02,000 |

Reserves & Surplus | 2 | 1,02,000 |

Money Received against Warrants |

|

|

|

|

|

|

|

|

Share Application Money pending allotment |

|

|

|

|

|

Non-current Liabilities |

|

|

Long Term Borrowings | 3 | 1,70,000 |

Deferred Tax Liabilities (Net) |

|

|

Other Long Term Liabilities |

|

|

Long Term Provisions |

|

|

|

|

|

Current Liabilities |

|

|

Short Term Borrowings |

|

|

Trade Payables |

| 2,80,000 |

Other Current Liabilities |

|

|

Short Term Provisions |

|

|

|

|

|

|

|

|

Total |

| 10,54,000 |

|

|

|

ASSETS |

|

|

Non-current Assets |

|

|

Fixed Assets | 4 | 4,65,000 |

Tangible Assets |

|

|

Intangible Assets |

|

|

Capital Work-in-Progress |

|

|

Intangible Assets under development |

|

|

Non-current Investments |

| 1,05,000 |

Deferred Tax Assets (Net) |

|

|

Long Term Loans & Advances |

|

|

Other Non-current Assets |

|

|

|

|

|

Current Assets |

|

|

Current Investments |

|

|

Inventories |

|

|

Trade Receivables | 5 | 3,97,000 |

Cash and Cash Equivalents |

| 87,000 |

Short Term Loans & Advances |

|

|

Other Current Assets |

|

|

|

|

|

|

|

|

Total |

| 10,54,000 |

|

|

|

Schedules forming a part of Balance Sheet

Particulars | Amount Rs | Amount Rs |

1. SHARE CAPITAL |

|

|

Authorised Share Capital : |

| - |

--- Equity Shares of Rs.-- each |

|

|

|

|

|

Issued Subscribed and Paid Up Capital : |

|

|

18,000 Equity Shares of Rs.7 each |

| 1,26,000 |

44,800 Equity Shares of Rs.5 each |

| 2,24,000 |

16,000, 13% Preference shares of Rs 10 each, Rs 6 paid up |

| 96,000 |

14,000, 13% Preference shares of Rs 10 each, Rs 4 paid up |

| 56,000 |

|

|

|

Total |

| 5,02,000 |

|

|

|

2. RESERVES & SURPLUS |

|

|

|

|

|

Capital Reserve |

| 1,02,000 |

|

|

|

Total |

| 1,02,000 |

|

|

|

3. LONG TERM BORROWINGS |

|

|

Secured |

|

|

12% Debentures of Rs 100 each |

| 1,70,000 |

|

|

|

Total |

| 1,70,000 |

|

|

|

4. FIXED ASSETS |

|

|

Tangible |

|

|

Land & Building | 2,05,000 |

|

Plant & Machinery | 2,50,000 |

|

Furniture | 10,000 | 4,65,000 |

Intangible Assets |

|

|

|

| - |

Total Assets |

| 4,65,000 |

|

|

|

5. TRADE RECEIVABLES |

|

|

Sundry Debtors |

| 2,77,000 |

Bills Receivable |

| 1,20,000 |

|

| 3,97,000 |

Q14)

Following is the Balance sheet of Roshni Ltd. As on 31st March, 2009.

Liabilities | Amt. | Assets | Amt. |

Share Capital |

| Fixed Assets |

|

7,000 10% Preference |

| Goodwill | 50,000 |

Share of Rs.10/- each. | 7,00,000 | Patents & Trade marks | 30,000 |

40,000 Equity Shares |

| Building | 3,20,000 |

Of Rs.10/- each. | 4,00,000 | Plant & Machinery | 2,80,000 |

|

| Furniture | 1,20,000 |

Reserve & Surplus |

|

|

|

Capital Reserve | 40,000 | Current Assets, Loans |

|

|

| & Advances |

|

Secured loans |

| Stock | 1,55,000 |

6% Debentures of |

| Sundry Debtors | 85,000 |

Rs.100/- each | 2,00,000 | Bank | 85,000 |

Debentures interest |

| Cash | 35,000 |

Due | 70,000 |

|

|

|

| Miscellaneous |

|

Current Liabilities & |

| Expenditure |

|

Provisions |

| Discount on |

|

Sundry Creditors | 1,40,000 | Debentures | 35,000 |

|

| Profit & Loss A/c | 3,55,000 |

| 15,50,000 |

| 15,50,000 |

Note : Preference dividend is in arrears for three years. The following scheme of reconstruction was prepared & duly approved by the court.

1) The Preference Shares shall be converted into equal number of 11% Preference shares of Rs.50/- each.

2) The Equity Share shall be reduced to Rs.2/- each. However, the Face Value will remain the same.

3) 6% Debentures shall be converted into equal number of 7% debentures of Rs.85/- each. The debenture holders also agreed to waived 60% of the accrued interest.

4) Arrears of Preference dividend is to be reduced to one years dividend which is paid in cash.

5) The sundry creditors agreed to waived 40% of their claims & to accept Equity Shares for Rs.40,000/- in part settlement renewed claims.

6) The assets are to be revalued as under :

Building Rs.4,00,000/-

Plant & Machinery Rs.2,20,000/-

Furniture Rs.70,000/-

Stock Rs.1,00,000/-

Debtors Rs.70,000/-

7) Intangible assets & fictitious assets are to be written off.

Pass journal entries.

Prepare Capital Reduction Account

A14)

Journal of Roshni Ltd

Date |

Particulars | Debit (Rs.) | Credit (Rs.) |

1. | 10% Preference Share Capital A/c..Dr. To 11% Preference Share Capital A/c To Capital Reduction A/c (Being 10% Preference shares converted into 11% Preference Shares.) | 7,00,000 |

3,50,000 3,50,000 |

2. | Equity Share Capital A/c Dr. To Capital Reduction A/c (Being reduction in Equity Shares.) | 3,20,000 |

3,20,000 |

3. | 6% Debentures A/c Dr. To 7% Debentures A/c To Capital Reduction A/c (Being converted debentures into 7% debentures.) | 2,00,000 |

1,70,000 30,000 |

4. | Debentures Interest Due A/c Dr. To Capital Reduction A/c (Being accrued interest on debentures waived.) | 45,000 |

45,000 |

5. | Preference Dividend A/c Dr. To Cash / Bank A/c (Being paid on year‟s dividend.) | 70,000 |

70,000 |

6. | Creditors A/c Dr. To Equity Share Capital A/c To Capital Reduction A/c (Being settled sundry creditors.) | 96,000 |

40,000 56,000 |

7. | Building A/c..................Dr. To Capital Reduction A/c (Being appreciation in building.) | 80,000 |

80,000 |

8. | Capital Reduction A/c...........Dr. To Discount on Debentures A/c To Profit & Loss A/c To Goodwill A/c To Patent & Trademark A/c To Preference Dividend A/c To Plant & Machinery A/c To Furniture A/c To Stock A/c To Debtors A/c To Capital Reserve A/c (Being assets/losses written off.) | 8,81,000 |

35,000 3,55,000 50,000 30,000 70,000 60,000 50,000 55,000 15,000 1,61,000 |

Capital Reduction Account

Dr. Cr.

Particulars | Amt. | Particulars | Amt. |

To Discount on |

| By 10% Preference Share Capital A/c By Equity Share Capital A/c By 6% Debentures A/c By Interest due on Debentures A/c By Creditors A/c By Building A/c |

3,50,000

3,20,000 30,000

45,000 56,000 80,000 |

Debentures A/c | 35,000 | ||

To Profit & Loss A/c | 3,55,000 | ||

To Goodwill A/c | 50,000 | ||

To Patent & Trademark |

| ||

A/c | 30,000 | ||

To Preference Dividend |

| ||

A/c | 70,000 | ||

To Plant & Machinery |

| ||

A/c | 60,000 | ||

To Furniture A/c | 50,000 | ||

To Stock A/c | 55,000 | ||

To Debtors A/c | 15,000 | ||

To Capital Reserve A/c | 1,61,000 | ||

| 8,81,000 |

| 8,81,000 |

Q15)

Following is the balance sheet of Bhushan Ltd. As on 31st March, 2020.

Liabilities | Amt. | Assets | Amt. |

Share Capital |

| Fixed Assets Premises Plant & Machinery Investment Current Assets, Loans & Advances Stock Debtors Deposits & Advance

IV Miscellaneous Expenditure Publicity Campaign Expenses Profit & Loss Account |

|

25,000 10% Preference |

| 3,25,000 | |

Shares of Rs.10/- each. | 2,50,000 | 5,00,000 | |

Equity Share of Rs.10/- |

|

| |

Each. | 4,50,000 | 1,50,000 | |

Secured loans |

|

| |

16% Debentures of |

|

| |

Rs.100/- each | 5,00,000 | 1,35,000 | |

Current Liabilities & Provisions |

| 1,00,000 50,000 | |

Sundry Creditors | 2,10,000 |

| |

Bank Overdraft | 1,30,000 |

| |

Other Liability | 1,10,000 |

| |

|

| 2,00,000 | |

|

| 1,90,000 | |

| 16,50,000 |

| 16,50,000 |

It is observed that the new product launched by the company has not succeeded even after three years of marketing. The management is of the opinion that the assets & liabilities are not valued correctly & also finds it difficult to raise finance.

To overcome the situation a scheme of reconstruction is prepared by the directors & approved by all authorities.

The salient features of the scheme are

1) Plant & Equipment having book value of Rs.10,000/- is obsolete. This is sold as scrap for Rs.36,000/-.

2) The auditors have pointed out that depreciation on plant is not provided to the extent Rs.30,000/-

3) Stock includes items valued Rs.50,000/- which is sold at a loss of 50%.

4) The present realizable value of investments is Rs.55,000/-.

5) Dividend on Preference Shares is in arrears for 3 years. This amount is not payable.

6) All losses & Fictitious assets are to be written off.

7) The expenses paid for forming & implementing scheme is Rs.10,000/-.

8) The paid up value of Equity Share is to be reduced to Rs.2/- per share & preference share to Rs.5/- per share. However, the face value remains unchanged.

9) The Creditors due are settled as.

• 30% immediate payment in Cash.

• 40% amount is cancelled.

• 30% paid by issue of 15% debentures.

10) Other Current liabilities includes Rs.45,000/- payable to directors towards remuneration. This liability is to be cancelled.

11) A call of Rs.3/- per share on Equity Share is made & received.

12) Bank Overdraft is paid off to the extent possible.

You are required to show :

i) Journal entries for above scheme of reconstruction.

Ii) Show Bank A/c & Capital Reduction A/c

A15)

Journal In the books of Bhushan Ltd.

Date | Particulars | Debit (Rs.) | Credit (Rs.) |

1. | Equity Share Capital A/c.........Dr. 10% Preference Share Capital A/c..Dr. To Capital Reduction A/c (Being reduction of Equity & Preference Share Capital.) | 3,60,000 1,25,000 |

4,85,000 |

2. | Creditors A/c.................Dr. To Cash / Bank A/c (30%) To Capital Reduction A/c (40%) To 15% Debentures A/c (30%) (Being Creditors dues settled as per Scheme of reconstruction.) | 2,10,000 |

63,000 84,000 63,000 |

3. | Other Liabilities A/c............Dr. To Capital Reduction A/c (Being dues to directors cancelled.) | 45,000 |

45,000 |

4. | Cash / Bank A/c...............Dr. Capital Reduction A/c...........Dr. To Plant & Equipment A/c (Being sale of plant having book value of Rs.1,00,000/- for Rs.36,000/-.) | 36,000 64,000 |

1,00,000 |

5. | Capital Reduction A/c...........Dr. To Plant & Equipment A/c (Being depreciation provided.) | 30,000 |

30,000 |

6. | Cash / Bank A/c...............Dr. Capital Reduction A/c...........Dr. To Plant & Machinery A/c (Being sale of stock having took value of Rs.50,000/- at a loss of 50%.) | 25,000 25,000 |

50,000 |

7. | Capital Reduction A/c...........Dr. To Investment A/c (Being reduction in value by Rs.95,000/-.) | 95,000 |

95,000 |

8. | Capital Reduction A/c...........Dr. To Profit & Loss A/c To Publicity Campaign Expenses A/c (Being brought forward losses & fictitious assets written off as per scheme of reconstruction.) | 3,90,000 |

1,90,000 2,00,000 |

9. | Capital Reduction A/c...........Dr. To Cash / Bank A/c (Being paid expenses on reconstruction.) | 10,000 |

10,000 |

10. | Cash / Bank A/c (45,000X3).......Dr. To Equity Share Capital A/c (Being receipt of all money on 45,000 shares @ Rs.3/- each.) | 1,35,000 |

1,35,000 |

11. | Bank Overdraft A/c.............Dr. To Cash / Bank A/c (Being balance in Cash / Bank used to pay off overdraft.) | 1,23,000 |

1,23,000 |

Bank Account

Dr. Cr.

Particulars | Amt. | Particulars | Amt. |

To Plant & Equipment A/c To Stock A/c To Equity Share Capital A/c |

36,000 25,000

1,35,000 | By Capital Reduction A/c By Sundry Creditors A/c By Bank Overdraft A/c | 10,000 63,000 1,23,000 |

| 1,96,000 |

| 1,96,000 |

Capital Reduction Account

Dr. Cr.

Particulars | Amt. | Particulars | Amt. |

To Plant (Loss on sale) | 64,000 | By Equity Share Capital A/c By Preference Share Capital A/c By Creditors By Other dues (Directors) |

|

To Plant (Depreciation) | 30,000 | 3,60,000 | |

To Stock | 25,000 |

| |

To Investment | 95,000 | 1,25,000 | |

To Profit & Loss A/c | 1,90,000 | 84,000 | |

To Publicity Expenses | 2,00,000 | 45,000 | |

To Cash (Exp.) | 10,000 |

| |

| 6,14,000 |

| 6,14,000 |

Q16) Green Limited had decided to reconstruct the Balance Sheet since it has accumulated huge losses. The following is the summarized Balance Sheet of the Company on 31.3.2012 before reconstruction.

Balance Sheet of Green Limited as at 31.3.2012

Liabilities | Rs. | Assets | Rs. |

Share Capital: |

| Fixed Assets: |

|

Authorised: |

| Goodwill | 20,00,000 |

1,50,000 Equity Shares of Rs. 50 each | 75,00,000 | Building | 10,00,000 |

Subscribed and Paid up Capital: |

| Plant | 10,00,000 |

50,000 Equity Shares of Rs. 50 each | 25,00,000 | Computers | 25,00,000 |

1,00,000 Equity Shares of Rs. 50 each, |

| Investments | Nil |

Rs. 40 per share paid up | 40,00,000 | Current Assets | Nil |

Secured Loans: |

| Profit and Loss A/c-Loss | 20,00,000 |

12% First Debentures | 5,00,000 |

|

|

12% Second Debentures | 10,00,000 |

|

|

Current Liabilities: |

|

|

|

Sundry Creditors | 5,00,000 |

|

|

| 85,00,000 |

| 85,00,000 |

The following is the interest of Mr. X and Mr. Y in Green Limited:

| Mr. X Rs. | Mr. Y Rs. |

12% First Debentures 12% Second Debentures Sundry Creditors | 3,00,000 7,00,000 2,00,000 | 2,00,000 3,00,000 1,00,000 |

| 12,00,000 | 6,00,000 |

Fully paid up Rs. 50 shares Partly paid-up shares (Rs. 40 paid up) | 3,00,000 5,00,000 | 2,00,000 5,00,000 |

The following Scheme of Reconstruction is approved by all parties interested and also by the Court:

(a) Uncalled capital is to be called up in full and such shares and the other fully paid-up shares be converted into equity shares of Rs. 20 each.

(b) Mr. X is to cancel Rs. 7,00,000 of his total debt (other than share amount) and to pay Rs. 2 lakhs to the company and to receive new 14% First Debentures for the balance amount.

(c) Mr. Y is to cancel Rs. 3,00,000 of his total debt (other than equity shares) and to accept new 14% First Debentures for the balance.

(d) The amount thus rendered available by the scheme shall be utilised in writing off of Goodwill, Profit and Loss A/c Loss and the balance to write off the value of computers.

(e) You are required to draw the Journal Entries to record the same and also show the Balance Sheet of the reconstructed company.

A16)

Green Limited Journal Entries

- Bank Account Dr. 10,00,000

To Equity Share Capital Account 10,00,000

(Balance of Rs. 10 per share on 1,00,000 equity shares

Called up as per reconstruction scheme)

2. Equity Share Capital Account (Rs. 50) Dr. 75,00,000

To Equity Share Capital Account (Rs. 20) 30,00,000

To Capital Reduction Account 45,00,000

(Reduction of equity shares of Rs. 50 each to shares of Rs. 20

Each as per reconstruction scheme)

3. 12% First Debentures Account Dr. 3,00,000

12% Second Debentures Account Dr. 7,00,000

Sundry Creditors Account Dr. 2,00,000

To X

(The total amount due to X, transferred to his account) 12,00,000

4. Bank Account Dr. 2,00,000

To X 2,00,000

(The amount paid by X under the reconstruction scheme) 2,00,000

5. 12% First Debentures Account Dr. 2,00,000

12% Second Debentures Account Dr. 3,00,000

Sundry Creditors Account Dr. 1,00,000

To Y 6,00,000

(The total amount due to Y, transferred to his account)

6. X Dr. 14,00,000

To 14% First Debentures Account 7,00,000

To Capital Reduction Account 7,00,000

(The cancellation of Rs. 7,00,000 out of total debt of Mr. X and issue of 14% first debentures for the balance amount as per reconstruction scheme)

7. Capital Reduction Account Dr. 55,00,000

To Goodwill Account 20,00,000

To Profit and Loss Account 20,00,000

To Computers Account 15,00,000

(The balance amount of capital reduction account utilised in writing off goodwill, profit and loss account, and computers— Working Note)

Balance Sheet of Green Limited (and reduced) as on 31st March

Particulars | Notes | Rs. | |||||

1

2

3

1 |

A A A

A | Equity and Liabilities Shareholders' funds Share capital Non-current liabilities Long-term borrowings

Current liabilities Trade Payables

Assets Non-current assets Fixed assets |

Total |

1 |

30,00,000 | ||

2 | 10,00,000 | ||||||

| 2,00,000 | ||||||

| 42,00,000 | ||||||

| |||||||

Tangible assets 2 Current assets Cash and cash equivalents Total | 3 | 30,00,000

12,00,000 | |||||

42,00,000 | |||||||

Notes to Accounts

|

| Rs. | |

1. Share Capital |

|

|

|

Equity share capital |

|

| |

Issued, subscribed and paid up |

|

| |

150,000 equity shares of Rs. 20 each |

| 30,00,000 | |

| Total | 30,00,000 | |

2. Long-term borrowings |

|

| |

Secured |

|

| |

14% First Debentures |

| 10,00,000 | |

| Total | 10,00,000 | |

3. Tangible assets |

|

| |

Building |

| 10,00,000 | |

Plant |

| 10,00,000 | |

Computers |

| 10,00,000 | |

| Total | 30,00,000 | |

Working Note:

Capital Reduction Account

| Rs. |

| Rs. |

To Goodwill A/c | 20,00,000 | By Equity Share Capital A/c | 45,00,000 |

To P & L A/c | 20,00,000 | By X | 7,00,000 |

To Computers (Bal. Fig.) | 15,00,000 | By Y | 3,00,000 |

| 55,00,000 |

| 55,00,000 |

Q17) The following is the Balance sheet of Weak Ltd. As on 31.3.2012:

Liabilities | Rs. | Assets | Rs. |

Equity shares of Rs.100 each | 1,00,00,000 | Fixed assets | 1,25,00,000 |

12% cumulative preference shares of Rs.100 each | 50,00,000 | Investments (Market value Rs.9,50,000) | 10,00,000 |

10% debentures of Rs.100 each | 40,00,000 | Current assets | 1,00,00,000 |

Sundry creditors | 50,00,000 | P & L A/c | 4,00,000 |

Provision for taxation | 1,00,000 | Preliminary expenses | 2,00,000 |

| 2,41,00,000 |

| 2,41,00,000 |

The following scheme of reorganization is sanctioned:

(i) All the existing equity shares are reduced to Rs.40 each.

(ii) All preference shares are reduced to Rs.60 each.

(iii) The rate of interest on debentures is increased to 12%. The debenture holders surrender their existing debentures of Rs.100 each and exchange the same for fresh debentures of Rs.70 each for every debenture held by them.

(iv) One of the creditors of the company to whom the company owes Rs.20,00,000 decides to forgo 40% of his claim. He is allotted 30,000 equity shares of Rs.40 each in full satisfaction of his claim.

(v) Fixed assets are to be written down by 30%.

(vi) Current assets are to be revalued at Rs.45,00,000.

(vii) The taxation liability of the company is settled at Rs.1,50,000.

(viii) Investments to be brought to their market value.

(ix) It is decided to write off the fictitious assets.

Pass Journal entries and show the Balance sheet of the company after giving effect to the above.

A17) Journal Entries in the books of Weak Ltd.

| Rs. | Rs. |

(i) Equity share capital (Rs.100) A/c Dr. To Equity Share Capital (Rs.40) A/c To Capital Reduction A/c (Being conversion of equity share capital of Rs.100 each into Rs.40 each as per reconstruction scheme) | 1,00,00,000 |

40,00,000 |

12% Cumulative Preference Share capital (Rs.100) A/c Dr. To 12% Cumulative Preference Share Capital (Rs.60) A/c To Capital Reduction A/c (Being conversion of 12% cumulative preference share capital of Rs.100 each into Rs.60 each as per reconstruction scheme) | 50,00,000 |

30,00,000 20,00,000 |

10% Debentures A/c Dr. To 12% Debentures A/c To Capital Reduction A/c (Being 12% debentures issued to 10% debenture holders for 70% of their claims. The balance transferred to capital reduction account as per reconstruction scheme) | 40,00,000 |

28,00,000 12,00,000 |

Sundry Creditors A/c Dr. To Equity Share Capital A/c To Capital Reduction A/c (Being a creditor of Rs.20,00,000 agreed to surrender his claim by 40% and was allotted 30,000 equity shares of Rs.40 each in full settlement of his dues as per reconstruction scheme) | 20,00,000 |

12,00,000 8,00,000 |

Provision for Taxation A/c Dr. Capital Reduction A/c Dr. To Liability for Taxation A/c (Being conversion of the provision for taxation into liability for taxation for settlement of the amount due) | 1,00,000 50,000 |

1,50,000 |

Capital Reduction A/c Dr. To P & L A/c To Preliminary Expenses A/c To Fixed Assets A/c To Current Assets A/c To Investments A/c To Capital Reserve A/c (Being amount of Capital Reduction utilized in writing off P & L A/c (Dr.) Balance, Preliminary Expenses, Fixed Assets, Current Assets, Investments and the Balance transferred to Capital Reserve) | 99,50,000 |

4,00,000 2,00,000 37,50,000 55,00,000 50,000 |

Liability for Taxation A/c Dr. To Current Assets (Bank A/c) (Being the payment of tax liability)

| 1,50,000 |

1,50,000 |

Balance Sheet of Weak Ltd. (and reduced) as on 31.3.2020

|  | Particulars | Notes | Rs. | ||

|

| Equity and Liabilities |

|

|

| |

1 |

| Shareholders' funds |

|

|

| |

| a | Share capital |

| 1 | 82,00,000 | |

| b | Reserves and Surplus |

| 2 | 50,000 | |

2 |

| Non-current liabilities |

|

|

| |

| a | Long-term borrowings |

| 3 | 28,00,000 | |

3 |

| Current liabilities |

|

|

| |

| a | Trade Payables |

|

| 30,00,000 | |

|

|

| Total |

| 1,40,50,000 | |

|

| Assets |

|

|

| |

1 |

| Non-current assets |

|

|

| |

| a | Fixed assets |

|

|

| |

|

| Tangible assets |

| 4 | 87,50,000 | |

| b | Investments |

| 5 | 9,50,000 | |

2 |

| Current assets |

| 6 | 43,50,000 | |

|

|

| Total |

| 1,40,50,000 | |

|

|

|

|

|

| |

Notes to Accounts

|

| Rs. |

1. Share Capital Equity share capital Issued, subscribed and paid up |

|

|

150,000 equity shares of Rs. 20 each Preference share capital Issued, subscribed and paid up 12% Cumulative Preference shares of Rs. 60 each

| 1,25,00,000 (37,50,000) | 52,00,000

30,00,000 |

Total |

| 82,00,000 |

2. Reserves and Surplus Capital Reserve |

|

50,000 |

3. Long-term borrowings Secured 12% Debentures |

|

28,00,000 |

4. Tangible assets Fixed Assets Adjustment under scheme of reconstruction |

|

87,50,000 |

5. Investments Adjustment under scheme of reconstruction |

10,00,000 (50,000) |

9,50,000 |

6. Current assets Adjustment under scheme of reconstruction |

45,00,000 (1,50,000) |

43,50,000 |

Working Note:

Capital Reduction Account

| Rs. |

| Rs. |

To Liability for taxation A/c | 50,000 | By Equity share capital | 60,00,000 |

To P & L A/c | 4,00,000 | By 12% Cumulative preference share capital | 20,00,000 |

To Preliminary expenses | 2,00,000 | By 10% Debentures | 12,00,000 |

To Fixed assets | 37,50,000 | By Sundry creditors | 8,00,000 |

To Current assets | 55,00,000 |

|

|

To Investment | 50,000 |

|

|

To Capital Reserve | 50,000 |

|

|

(Balancing figure) |

|

|

|

| 1,00,00,000 |

| 1,00,00,000 |

Q18) The following is the summarized Balance Sheet of X Ltd. As on 31st March, 2020:

Liabilities | Rs. | Assets | Rs. |

12,000, 10% Preference shares of |

| Goodwill | 90,000 |

Rs.100 each | 12,00,000 |

|

|

24,000, Equity shares of Rs.100 each | 24,00,000 | Land & building | 12,00,000 |

10% Debentures | 6,00,000 | Plant & machinery | 18,00,000 |

Bank overdraft | 6,00,000 | Stock | 2,60,000 |

Sundry Creditors | 3,00,000 | Debtors | 2,80,000 |

|

| Cash | 30,000 |

|

| Profit & Loss Account | 14,00,000 |

|

| Preliminary expenses | 40,000 |

| 51,00,000 |

| 51,00,000 |

On the above date, the company adopted the following scheme of reconstruction:

(i) The equity shares are to be reduced to shares of Rs.40 each fully paid and the preference shares to be reduced to fully paid shares of Rs.75 each.

(ii) The debenture holders took over stock and debtors in full satisfaction of their claims.

(iii) The Land and Building to be appreciated by 30% and Plant and machinery to be depreciated by 30%.

(iv) The fictitious and intangible assets are to be eliminated.

(v) Expenses of reconstruction amounted to Rs.5,000.

Give journal entries incorporating the above scheme of reconstruction and prepare the reconstructed Balance Sheet.

A18) In the books of X Ltd.

Journal Entries 31st March, 2020

|

| Rs. | Rs. | |

(i) | Equity Share Capital A/c (Rs. 100) To Equity Share Capital A/c (Rs. 40) To Capital Reduction A/c (Being 24,000 equity shares of Rs.100 each reduced to Rs.40 each fully paid up) | Dr. | 24,00,000 |

|

|

|

| 9,60,000 | |

|

|

| 14,40,000 | |

(ii) | 10% Preference Share Capital A/c (Rs.100) To 10% Preference Share Capital A/c (Rs.75) To Capital Reduction A/c (Being 12,000 Preference shares of Rs.100 each reduced to Rs.75 each fully paid up) | Dr. | 12,00,000 |

|

|

|

| 9,00,000 | |

|

|

| 3,00,000 | |

(iii) | 10% Debentures A/c To Stock A/c To Debtors A/c To Capital Reduction A/c (Being Debenture holders given stock and debtors in full settlement of their claims) | Dr. | 6,00,000 |

|

|

|

| 2,60,000 | |

|

|

| 2,80,000 | |

|

|

| 60,000 | |

(iv) | Land & Building A/c To Capital Reduction A/c (Being Land & Building appreciated by 30%) | Dr. | 3,60,000 |

|

|

|

| 3,60,000 | |

(v) | Reconstruction expenses A/c To Cash A/c (Being expenses of reconstruction paid) | Dr. | 5,000 |

|

|

|

| 5,000 | |

(vi) | Capital Reduction A/c To Goodwill A/c To Profit and Loss A/c To Plant & Machinery A/c To Preliminary expenses A/c To Reconstruction expenses A/c To Capital Reserve A/c (Bal. Fig.) (Being various losses written off, assets written down and balance in Capital Reduction A/c transferred to Capital Reserve A/c) | Dr. | 21,60,000 |

|

|

|

| 90,000 | |

|

|

| 14,00,000 | |

|

|

| 5,40,000 | |

|

|

| 40,000 | |

|

|

| 5,000 | |

|

|

| 85,000 | |

Balance Sheet (and reduced) of X Ltd. As at 31st March 2020

Particulars | Notes | Rs. | |||

1

2

1

2 |

a b

a b

a | Equity and Liabilities Shareholders' funds Share capital Reserves and Surplus Current liabilities Trade Payables Short term borrowings

Assets Non-current assets Fixed assets Tangible assets Current assets Cash and cash equivalents (30,000 -5,000) |

Total

Total |

1 |

18,60,000 |

2 | 85,000 | ||||

| 3,00,000 | ||||

| 6,00,000 | ||||

| 28,45,000 | ||||

|

28,20,000 | ||||

| 25,000 | ||||

| 28,45,000 | ||||

Notes to Accounts

|

|

| Rs. |

1. | Share Capital Equity share capital 24,000 equity shares of Rs. 40 each fully paid-up Preference share capital 12,000, 10% Preference shares of Rs. 75 each fully Paid up Total Reserves and Surplus Capital Reserve Tangible assets Land and Building Plant and Machinery |

|

|

|

| 9,60,000 | |

|

|

9,00,000 | |

|

| 18,60,000 | |

2. |

|

| |

|

| 85,000 | |

3. |

|

| |

| 15,60,000 |

| |

| 12,60,000 |

| |

|

| 28,20,000 |

Q19) The following scheme of reconstruction has been approved for Win Limited:

(i) The shareholders to receive in lieu of their present holding at 1,00,000 shares of Rs.10 each, the following:

(a) New fully paid Rs.10 Equity shares equal to 3/5th of their holding.

(b) 10% Preference shares fully paid to the extent of 1/5th of the above new equity shares.

(c) Rs.40,000, 8% Debentures.

(ii) An issue of Rs.1 lakh 10% first debentures was made and allotted, payment for the same being received in cash forthwith.

(iii) Goodwill which stood at Rs.1,40,000 was completely written off.

(iv) Plant and machinery which stood at Rs.2,00,000 was written down to Rs.1,50,000.

(v) Freehold property which stood at Rs.1,50,000 was written down by Rs.50,000.

You are required to draw up the necessary Journal entries in the Books of Win Limited for the above reconstruction. Suitable narrations to Journal entries should form part of your answer.

A19)

|

| Rs. | Rs. |

Equity Share Capital (old) A/c | Dr. | 10,00,000 |

|

To Equity Share Capital (Rs.10) A/c |

|

| 6,00,000 |

To 10% Preference Share Capital A/c |

|

| 1,20,000 |

To 8% Debentures A/c |

|

| 40,000 |

To Reconstruction A/c |

|

| 2,40,000 |

(Being new equity shares, 10% Preference Shares, 8% Debentures issued and the balance transferred to Reconstruction account as per the Scheme) |

|

|

|

Bank A/c | Dr. | 1,00,000 |

|

To 10% First Debentures Application & Allotment A/c |

|

| 1,00,000 |

(Being amount received on issue of 10% First Debentures for application and allotment Account) |

|

|

|

10% First Debentures Application and allotment A/c

To 10% First Debentures Account (Being allotment of 10% first Debentures) | Dr. | 1,00,000 |

1,00,000 |

Reconstruction A/c To Goodwill Account To Plant and Machinery Account To Freehold Property Account (Being Reconstruction Account utilized for writing off of Goodwill, Plant and Machinery and Freehold property as per the scheme) |  | 2,40,000 |

1,40,000 50,000 50,000 |

Q20) The following is the summarized Balance Sheet of Buxbaum Limited as at 31st March, 2020:

| |

Sources of funds |

|

Authorized capital |

|

50,000 Equity shares of 10 each | 5,00,000 |

10,000 Preference shares of 100 each | 10,00,000 |

| 15,00,000 |

Issued, subscribed and paid up |

|

30,000 Equity shares of 10 each | 3,00,000 |

5,000, 8%Redeemable Preference shares of 100 each | 5,00,000 |

Reserves & Surplus |

|

Securities Premium | 6,00,000 |

General Reserve | 6,50,000 |

Profit & Loss A/c | 1,80,000 |

2,500, 9% Debentures of 100 each | 2,50,000 |

Sundry Creditors | 1,70,000 |

| 26,50,000 |

Application of funds |

|

Fixed Assets (net) | 7,80,000 |

Investments (market value 5,80,000) | 4,90,000 |

Deferred Tax Assets | 3,40,000 |

Sundry Debtors

| 6,20,000 |

Cash & Bank balance | 2,80,000 |

Preliminary expenses | 1,40,000 |

| 26,50,000 |

In Annual General Meeting held on 20th June, 2020 the company passed the following resolutions:

(i) To split equity, share of 10 each into 5 equity shares of 2 each from 1st July, 2012.

(ii) To redeem 8% preference shares at a premium of 5%.

(iii) To redeem 9% Debentures by making offer to debenture holders to convert their holdings into equity shares at 10 per share or accept cash on redemption.

(iv) To issue fully paid bonus shares in the ratio of one equity share for every 3 shares held on record date.

On 10th July, 2012 investments were sold for 5,55,000 and preference shares were redeemed.

40% of Debenture holders exercised their option to accept cash and their claims were settled on 1st August, 2012.

The company fixed 5th September, 2012 as record date and bonus issue

Was concluded by 12th September, 2012.

You are requested to journalize the above transactions including cash transactions and prepare Balance Sheet as at 30th September, 2020. All working notes should form part of your answer.

A20) Buxbaum Limited Journal Entries

2020 |

| Dr. () | Cr. () |

July 1 | Equity Share Capital A/c ( 10 each) Dr. To Equity share capital A/c ( 2 each) (Being equity share of 10 each splitted into 5 equity shares of 2 each) | 3,00,000 |

|

|

| 3,00,000 | |

July 10 | Cash & Bank balance A/c Dr. To Investment A/c To Profit & Loss A/c (Being investment sold out and profit on sale credited to Profit & Loss A/c) | 5,55,000 |

|

|

| 4,90,000 | |

|

| 65,000 | |

July 10

July 10

July 10

Aug 1

Aug 1

Sept. 5

Sept. 12

|

8% Redeemable preference share capital A/c Dr. Premium on redemption of preference share A/c Dr. To Preference shareholders A/c (Being amount payable to preference shareholders on redemption) Preference shareholders A/c Dr. To Cash & Bank A/c (Being amount paid to preference shareholders) Securities premium A/c Dr. To Capital redemption reserve A/c (Being amount equal to nominal value of preference shares transferred to Capital Redemption Reserve A/c on its redemption as per the law) 9% Debentures A/c Dr. Interest on debentures A/c Dr. To Debenture holder’s A/c (Being amount payable to debenture holders along with interest payable) Debenture holder’s A/c Dr. To Cash & bank A/c (1,00,000 + 7,500) To Equity share capital A/c To Securities premium A/c (Being claims of debenture holders satisfied) Securities premium A/c Dr. To Bonus to shareholders A/c (Being securities premium capitalized to issue bonus shares) Bonus to shareholders A/c Dr. To Equity share capital A/c (Being 55,000 fully paid equity shares of 2 each issued as bonus in ratio of 1 share for every 3 shares held) |

5,00,000 25,000

5,25,000

5,00,000

2,50,000 7,500

2,57,500

1,10,000

1,10,000

|

5,25,000

5,25,000

5,00,000

2,57,500

1,07,500 30,000 20,000 1,20,000

1,10,000

1,10,000 |

|

|

|

|

Sept. 30 | Securities Premium A/c To Premium on redemption of preference shares A/c (Being premium on preference shares adjusted from securities premium account) | 25,000 |

25,000 |

| Profit & Loss A/c Dr. To Interest on debentures A/c (Being interest on debentures transferred to Profit and Loss Account) | 7,500 |

7,500 |

Note: For capitalisation of Bonus shares and transfer to capital redemption reserve account any other free reserves given in the balance sheet may also be used.

Balance Sheet as at 30th September, 2020

Particulars | Notes | Rs. | |||

1

2

1

2 |

a b

a

a | Equity and Liabilities Shareholders' funds Share capital Reserves and Surplus Current liabilities Trade Payables

Assets Non-current assets Fixed assets Tangible assets Current assets Cash and cash equivalents Trade payables Other current assets |

Total

Total |

1 |

4,40,000 |

2 | 14,72,500 | ||||

| 1,70,000 | ||||

| 20,82,500 | ||||

|

7,80,000 | ||||

| 2,02,500 | ||||

| 6,20,000 | ||||

3 | 4,80,000 | ||||

| 20,82,500 | ||||

|

| Rs. |

1. Share Capital Authorized share capital  |

5,00,000 |

|

10,000 Preference shares of 100 each |

| 10,00,000 |

|

|

|

| 15,00,000 |

Issued, subscribed and paid up |

|

|

|

2,20,000 Equity shares of 2 each |

|

| 4,40,000 |

2. Reserves and Surplus |

|

|

|

Securities Premium |

| 85,000 |

|

Capital Redemption Reserve |

| 5,00,000 |

|

General Reserve |

| 6,50,000 |

|

Profit & Loss A/c (1,80,000 + 65,000 – 7,500) |

| 2,37,500 |

|

| Total |

| 14,72,500 |

3. Other current assets |

|

|

|

Preliminary expenses |

| 1,40,000 |

|

Deferred tax assets |

| 3,40,000 |

|

| Total |

| 4,80,000 |

Working Notes:

| ||||

2,500 Debentures of 100 each Less: Cash option exercised by 40% holders Conversion option exercised by remaining 60% Equity shares issued on conversion = 1,50,000 = 15,000 shares 10 3. Issue of Bonus Shares Existing equity shares after split (30,000 x 5) Equity shares issued on conversion Equity shares entitled for bonus Bonus shares (1 share for every 3 shares held) to be issued |

5,00,000

25,000 5,25,000

2,50,000 (1,00,000)

1,50,000

1,50,000 shares 15,000 shares 1,65,000 shares 55,000 shares | |||

4. Securities Premium A/c Balance as per balance sheet Add: Premium on equity shares issued on conversion of debentures (15,000 x 8)

Less: Capitalization for bonus issue (55,000 x 2) Adjustment for premium on preference shares Transfer to capital redemption reserve Balance 5. Cash and Bank Balance Balance as per balance sheet Add: Realization on sale of investment