Unit – III

Public Finance

Q1) What is the scope of Public Finance?

A1) Prof. Dalton classifies the scope of public finance into four areas as follows –

Public Income:

As the name suggests, public income refers to the income of the government. The government earns income in two ways – tax income and non-tax income. Tax income is easy to recognize, it’s the tax paid by people of the country in the form of income tax, sales tax, duties, etc. On the other hand non-tax income includes interest income from lending money to other countries, rent & income from government properties, donations from world organizations, etc.

This area studies methods of taxation, revenue classification, methods of increasing government revenue and its impact on the economy as a whole, etc.

Public Expenditure:

Public expenditure is the money spent by government entities. Logically, the government is going to spend money on infrastructure, defense, education, healthcare, etc. for the growth and welfare of the country.

This area studies the objectives and classification of public expenditure, effects of expenditure in different areas, effects of public expenditure on various factors such as employment, production, growth, etc.

Public Debt:

When public expenditure exceeds public income, the gap is filled by borrowing money from the public, or from other countries or world organizations such as The World Bank. These borrowed funds are public debt.

This area of public finance explains the burden of public debt, why it is necessary and its effect on the economy. It also suggests methods to manage public debt.

Financial Administration:

As the name suggests this area of public finance is all about the administration of all public finance i.e. public income, public expenditure, and public debt. Financial administration includes preparation, passing, and implementation of government budget and various government policies. It also studies the policy impact on the social-economic environment, inter-governmental relationships, foreign relationships, etc.

Q2) What is the principle of Maximum Social Advantage?

A2) The fiscal or budgetary operations of the state have manifold effects on the economy. The revenue collected by the state through taxation and the dispersal of public expenditures can have significant influence on the consumption, production and distribution of the national income of the country.

The fiscal operations of the government resolve themselves into a series of transfers of purchasing power from one section of the community to another, along with the variations in the total incomes available in the community. In fact, the fiscal activities of the state affect the allocation of resources, the use of resources from one channel to another, hence, the level of income, output and employment.

Hence, it is desirable that some standard or criterion should be laid down to judge the appropriateness of a particular operation of public finance — the government’s revenue and expenditures. In a modern welfare state, such a criterion can obviously be nothing else but the economic welfare of the people.

It follows, thus, that the particular financial activity of the state which leads to an increase in economic welfare is considered as desirable. It may be considered as undesirable if such an activity does not cause an increase in the welfare or even sometimes, it may be the cause of a reduction in the general economic welfare. The guiding principle of state policy has been technically desirable as the Principle of Maximum Social Advantage by Hugh Dalton.

According to Dalton, the principle of maximum social advantage is the most fundamental principle lying at the root of public finance. Hence, the best system of public finance is that which secures the maximum social advantage from its fiscal operations. Maximum social advantage is the maxim for the states. The optimum financial activities of a state should, therefore, be determined by the principle of maximum social advantage.

It is obvious that taxation by itself is a loss of utility to the people, while public expenditure by itself is a gain of utility to the community. When the state imposes taxes, some disutility or dissatisfaction is experienced in the society. This disutility is in the form of sacrifice involved in the payment of taxes — in parting with the purchasing power.

Similarly, when the state spends money, some utility is created in the society. Some satisfaction is experienced by a group of people in the society on whom, or for whom, the public expenditure is incurred by the state. This is the social benefit of welfare of the public expenditure.

As such, the maximum social advantage is achieved when the state in its financial activities maximise the surplus of social gain or utility (resulting from public expenditure) over the social sacrifice or disutility (involved in payment of taxes.) The principle of public finance, thus, requires the state to compare the sacrifice and benefits of the society in its fiscal operations.

The principle of maximum social advantage implies that public expenditure is subject to diminishing marginal social benefits and taxes are subject to increasing marginal social costs. Thus, an equilibrium is reached when social advantage is maximised, i.e., when the size of the budget is such that marginal social benefits of public expenditures are equal to the marginal social sacrifice of taxation.

Dalton states, “Public expenditure in every direction should be carried just so far, that the advantages to the community of a further small increase in any direction is just counter-balanced by the disadvantage of a corresponding small increase in taxation or in receipts from any other sources of public expenditure and public income.”

Thus, a rational state seeks to maximise the net social advantage of its fiscal operations. The social net advantage is maximum when the aggregate social benefits resulting from public expenditure is maximum and the aggregate social sacrifice involved in raising the public revenue is minimum. According to the principle of maximum social advantage, the public expenditure should be carried on up to the marginal social sacrifice of the last unit of rupee taxed.

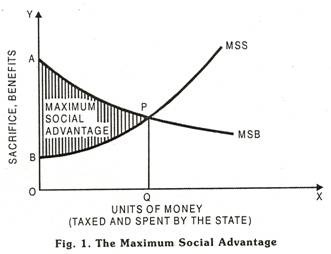

Q3) Give the Diagrammatic Representation maximum social net advantage.

A3) The maximum social net advantage is achieved when the marginal social sacrifice (disutility) of taxation and the marginal social benefit (utility) of public expenditure are equated. Thus, the point of equality between the marginal social benefit and the marginal social sacrifice is referred to as the point of aggregate maximum social advantage or least aggregate social sacrifice.

The equilibrium point of maximum social advantage may as well be illustrated by means of a diagram, as in Fig. 1.

The Maximum Social Advantage

In Fig. 1, MSS is the marginal social sacrifice curve. It is an upward sloping curve implying that the social sacrifice per unit of taxation goes on increasing with every additional unit of money raised. MSB is the marginal social benefit curve. It is a downward sloping curve implying that the social benefits per unit diminishes as the public expenditure increases.

The curves MSS and MSB intersect at point P. This equality (P) of MSS and MSB curves is regarded as the optimum limit of the state’s financial activity. It is easy to see that so long as the MSB curve lies above the MSS curve, each additional unit of revenue raised and spent by the state leads to an increase in the net social advantage.

This beneficial process would then be continued till marginal social sacrifice (MSS) becomes just equal to the marginal social benefit (MSB). Beyond this point, a further increase in the state’s financial activity means the marginal social sacrifice exceeding the marginal social benefit, hence the net social loss.

Thus, only under the condition of MSS = MSB, the maximum social advantage is achieved. Diagrammatically, the shaded area APB (the area between MSS and MSB curves, till both intersect each other) represents the quantum of maximum social advantage. OQ is the optimum amount of financial activities of the state.

Q4) What are tax and its types?

A4) A tax is a mandatory fee or financial charge levied by any government on an individual or an organization to collect revenue for public works providing the best facilities and infrastructure. The collected fund is then used to fund different public expenditure programs. If one fails to pay the taxes or refuse to contribute towards it will invite serious implications under the pre-defined law.

Types of Taxes:

Be it an individual or any business/organization, all have to pay the respective taxes in various forms. These taxes are further subcategorized into direct and indirect taxes depending on the manner in which they are paid to the taxation authorities. Let us delve deeper into both types of tax in detail:

Direct Tax:

The definition of direct tax is hidden in its name which implies that this tax is paid directly to the government by the taxpayer.

The general examples of this type of tax in India are Income Tax and Wealth Tax.

From the government’s perspective, estimating tax earnings from direct taxes is relatively easy as it bears a direct correlation to the income or wealth of the registered taxpayers.

Indirect Tax:

Indirect taxes are slightly different from direct taxes and the collection method is also a bit different. These taxes are consumption-based that are applied to goods or services when they are bought and sold.

The indirect tax payment is received by the government from the seller of goods/services.

The seller, in turn, passes the tax on to the end-user i.e. buyer of the good/service.

Thus the name indirect tax as the end-user of the good/service does not pay the tax directly to the government.

Some general examples of indirect tax include sales tax, Goods and Services Tax (GST), Value Added Tax (VAT), etc.

Q5) What are the most important principles or canons of a good tax system?

A5) These four canons are of:

1. Principle or Canon of Equality:

The first canon or principle of a good tax system emphasised by Adam Smith is of equality. According to the canon of equality, every person should pay to the Government according to his ability to pay, that is in proportion of the income or revenue he et jove onder the protection of the State.

Thus under the tax system based on equality principle the richer persons in the society will pay more than the poor. On the basis of this canon of equality or ability to pay Adam Smith argued that taxes should be proportional to income, that is, everybody should pay the same rate or percentage of his income as tax.

However, modem economists interpret equality or ability to pay differently from Adam Smith. Based on the assumption of diminishing marginal utility of money income, they argue that ability to pay principle calls for progressive income tax, that is, the rate of tax increases as income rises. Now, in most of the countries, progressive system of income and other direct taxes have been adopted to ensure equality in the tax system.

It may, however, be mentioned here that there are two aspects of ability to pay principle. First is the concept of horizontal equity. According to the concept of horizontal equity, those who are equal, that is, similarly situated persons ought to be treated equally.

This implies that those who have same income should pay the same amount of tax and there should be no discrimination between them. Second is the concept of vertical equity. The concept of vertical equity is concerned with how people with different abilities to pay should be treated for the purposes of division of tax burden. In other words, what various tax rates should be levied on people with different levels of income, A good tax system must be such as will ensure the horizontal as well as vertical equity.

2. Canon of Certainty:

Another important principle of a good tax system on which Adam Smith laid a good deal of stress is the canon of certainty. To quote Adam Smith, ‘The tax which each individual is bound to pay ought to be certain and not arbitrary.

The time of payment, the manner of payment, the quantity to be paid ought all to be clear and plain to the contributor and to every other person. A successful function of an economy requires that the people, especially business class, must be certain about the sum of tax that they have to pay on their income from work or investment.

The tax system should be such that sum of tax should not be arbitrarily fixed by the income tax authorities. While taking a decision about the amount of work effort that a person should put in or how much investment should he undertake under risky circumstances, he must know with certainty the definite amount of the tax payable by him on his income. If the sum of tax payable by him is subject to much discretion and arbitrariness of the tax assessment authority, this will weaken his incentive to work and invest more.

Moreover, lack of certainty in the tax system, as pointed out by Smith, encourages corruption in the tax administration. Therefore in a good tax system, “individuals should be secure against unpredictable taxes levied on their wages or other incomes. The law should be clear and specific; tax collectors should have little discretion about how much to assess tax payers, for this is a very great power and subject to abuse.”

In the opinion of the present author the Indian tax system violates this canon of certainty as under the Indian income tax law a lot of discretionary powers have been given to the income tax officers, which have been abused with impunity. As a result, there is a lot of harassment of the tax payers and corruption is rampant in the income tax department.

3. Canon of Convenience:

According to the third canon of Adam Smith, the sum, time and/manner of payment of a tax should not only be certain but the time and manner of its payment should also be convenient to the contributor. If land revenue is collected at the time of harvest, it will be convenient since at this time farmers reap their crop and obtain income.

In recent years efforts have been made to make the Indian income tax convenient to the taxpayers by providing for its payments in installments as advance payments at various times during the year. Further, income tax in India is levied on the basis of income received rather than income accrued during a year. This also makes the income tax system convenient. However, there is a lot of harassment of the tax payers as they are asked to come to the income tax office several times during a year for clarifications of their income tax returns.

4. Canon of Economy:

The Government has to spend money on collecting taxes levied by it- Since collection costs of taxes add nothing to the national product, they should be minimized as far as possible. If the collection costs of a tax are more than the total revenue yielded by it, it is not worthwhile to levy it.

More complicated a tax system, more elaborate administrative machinery will be employed to collect it and consequently collection costs will be relatively larger. Therefore, even for achieving economy in the tax collection, the taxes should be as simple as possible and tax laws should not be subject to different interpretations.

Q6) What is the Benefits Received Rule?

A6) The Benefits Received Rule, or benefits received principle, may take one of two related definitions: one as a tax theory; and one as a tax provision. The two definitions are:

The Benefits Received Principle, which is a theory of income tax fairness that says people should pay taxes based on the benefits they receive from the government.

A tax provision that says a donor who receives a tangible benefit from making a charitable contribution must subtract the value of that benefit from the amount claimed as an income tax deduction.

Q7) What is the ability to pay?

A7) Ability to pay is an economic principle that states that the amount of tax an individual pays should be dependent on the level of burden the tax will create relative to the wealth of the individual. The ability to pay principle suggests that the real amount of tax paid is not the only factor that has to be considered and that other issues such as the ability to pay should also be factored into a tax system.

Understanding Ability to Pay

The application of this principle gives rise to the progressive tax system, a system of taxation in which individuals with higher incomes are asked to pay more tax than individuals with lower incomes. The ideology behind this principle is that individuals and business entities that earn higher income can afford to pay more in taxes than lower-income earners. Ability to pay is not the same as straight income brackets. Rather, it extends beyond brackets in determining whether an individual taxpayer can pay his or her entire tax burden or not.

For instance, individuals should not be taxed on transactions in which they don’t receive any cash. Using stock options as an example, these securities have value for the employee who receives them and are, thus, subject to taxation. However, since the employee does not receive any cash, s/he would not pay tax on the options until s/he cashes them in.

Advocates of ability-to-pay taxation argue that it allows those with the most resources the ability to pool together the fund required to provide services needed by many. Critics of this system believe that the practice discourages economic success since it burdens wealthier individuals with a disproportionate amount of taxation. Classical economists like Adam Smith believed any elements of socialism, such as a progressive tax, would destroy the initiative of the population within a free market economy. However, many countries have blended capitalism and socialism with a great degree of success.

In banking, ability to pay is called “capacity.” It is used by lending institutions to determine a borrower’s ability to make his interest and principal repayments on a loan, using his or her disposable income or cash flow. Some bankers judge a borrower’s capacity using the standard Five C’s of Credit – credit history, capital base, capacity to generate cash flow, collateral, and current conditions in the economy. For municipal debt issuers, ability to pay refers to the issuers or lender’s present and future ability to create sufficient tax revenue to fulfill its contractual obligations.

Q8) What are the Economic effects of taxation?

A8) 1. Effects of Taxation on Production:

Taxation can influence production and growth. Such effects on production are analysed under three heads:

a) Effects on the ability to work, save and invest

b) Effects on the will to work, save and invest

c) Effects on the allocation of resources.

2. Effects on the Ability to Work Save:

Imposition of taxes results in the reduction of disposable income of the taxpayers. This will reduce their expenditure on necessaries which are required to be consumed for the sake of improving efficiency. As efficiency suffers, ability to work declines. This ultimately adversely affects savings and investment. However, this happens in the case of poor persons.

Taxation on rich persons has the least effect on the efficiency and ability to work. Not all taxes, however, have adverse effects on the ability to work. There are some harmful goods, such as cigarettes, whose consumption has to be reduced to increase ability to work. That is why high rates of taxes are often imposed on such harmful goods to curb their consumption.

But all taxes adversely affect the ability to save. Since rich people save more than the poor, progressive rate of taxation reduces savings potentiality. This means a low level of investment. Lower rate of investment has a dampening effect on economic growth of a country.

Thus, on the whole, taxes have the disincentive effect on the ability to work, save and invest.

3. Effects on the will to Work, Save and Invest:

The effects of taxation on the willingness to work, save and invest are partly the result of money burden of tax and partly the result of psychological burden of tax.

Taxes which are temporarily imposed to meet any emergency (e.g., Kargil Tax imposed for a year or so) or taxes imposed on windfall gain (e.g., lottery income) do not produce adverse effects on the desire to work, save and invest. But if taxes are expected to continue in the future, it will reduce the willingness to work and save the taxpayers.

Taxpayers have a feeling that every tax is a burden. This psychological state of mind of the taxpayers has a disincentive effect on the willingness to work. They feel that it is not worth taking extra responsibility or putting in more hours because so much of their extra income would be taken away by the government in the form of taxes.

However, if taxpayers are desirous of maintaining their existing standard of living in the midst of payment of large taxes, they might put in extra efforts to make up for the income lost in tax.

It is suggested that effects of taxes upon the willingness to work, save and invest depends on the income elasticity of demand. Income elasticity of demand varies from individual to individual.

If the income demand of an individual taxpayer is inelastic, a cut in income consequent upon the imposition of taxes will induce him to work more and to save more so that the lost income is at least partially recovered. On the other hand, the desire to work and save of those people whose demand for income is elastic will be adversely affected.

Thus, we have conflicting views on the incentives to work. It would seem logical that there must be a disincentive effect of taxes at some point but it is not clear at what level of taxation that crucial point would be reached.

4. Effects on the Allocation of Resources:

By diverting resources to the desired directions, taxation can influence the volume or the size of production as well as the pattern of production in the economy. It may, in the ultimate analysis, produce some beneficial effects on production. High taxation on harmful drugs and commodities will reduce their consumption.

This will discourage production of these commodities and the scarce resources will now be diverted from their production to the other products which are useful for economic growth. Similarly, tax concessions on some products are given in a locality which is considered as backward. Thus, taxation may promote regional balanced development by allocating resources in the backward regions.

However, not necessarily such beneficial effects will always be reaped. There are some taxes which may produce some unfavourable effects on production. Taxes imposed on certain useful products may divert resources from one region to another. Such unhealthy diversion may cause reduction of consumption and production of these products.

5. Effects of Taxation on Income Distribution:

Taxation has both favourable and unfavourable effects on the distribution of income and wealth. Whether taxes reduce or increase income inequality depends on the nature of taxes. A steeply progressive taxation system tends to reduce income inequality since the burden of such taxes falls heavily on the richer persons.

But a regressive tax system increases the inequality of income. Further, taxes imposed heavily on luxuries and nonessential goods tend to have a favourable impact on income distribution. But taxes imposed on necessary articles may have a regressive effect on income distribution.

However, we often find some conflicting roles of taxes on output and distribution. A progressive system of taxation has a favourable effect on income distribution but it has disincentive effects on output.

A high dose of income tax will reduce inequalities but such will produce some unfavourable effects on the ability to work, save, investment and, finally, output. Both the goals—the equitable income distribution and larger output—cannot be attained simultaneously.

6. Other Effects of Taxation:

If taxes produce favourable effects on the ability and the desire to work, save and invest, there will be a favourable effect on the employment situation of a country. Further, if resources collected via taxes are utilized for development projects, it will increase employment in the economy. If taxes affect the volume of savings and investment badly then recession and unemployment problems will be aggravated.

Again, the effect of taxes on the price level may be favourable and unfavourable. Sometimes, taxes are imposed to curb inflation. Again, as an imposition of commodity taxes lead to rising costs of production, taxes aggravate the problem of inflation.

Thus, taxation creates both favourable and unfavourable effects on various parameters. Unfavourable effects of taxes can be wiped out by the judicious use of progressive taxation.

Q9) Explain Wagner’s Law.

A9) Wagner's law of state, is known as the law of increasing state spending, is a principle named after the German economist Adolph Wagner (1835–1917).He first observed it for his own country and then for other countries. The theory holds that for any country, that public expenditure rises constantly as income growth expands. The law predicts that the development of an industrial economy will be accompanied by an increased share of public expenditure in gross national product:

The advent of modern industrial society will result in increasing political pressure for social progress and increased allowance for social consideration by industry.

Wagner's law suggests that a welfare state evolves from free market capitalism due to the population voting for ever-increasing social services as general income levels grow across broad spectrums of the economy. In spite of some ambiguity, Wagner's statement in formal terms has been interpreted by Richard Musgrave as follows:

As progressive nations industrialize, the share of the public sector in the national economy grows continually. The increase in State Expenditure is needed because of three main reasons. Wagner himself identified these as (i) Social activities of the state, (ii) administrative and protective actions, and (ii) Welfare functions. The material below is an apparently much more generous interpretation of Wagner's original premise.

Socio-political, i.e., the state social functions expand over time: retirement insurance, natural disaster aid (either internal or external), environmental protection programs, etc.

Economic: science and technology advance, consequently there is an increase of state assignments into the sciences, technology and various investment projects, etc.

Historical: the state resorts to government loans for covering contingencies, and thus the sum of government debt and interest amount grow; i.e., it is an increase in debt service expenditure.

Q10) What is the effect of Public expenditure on Production and Distribution?

A10) The effect of public expenditure on production can be examined with reference to its effects on ability & willingness to work, save & invest and on diversion of resources.

Ability to work, save and invest : Socially desirable public expenditure increases community's productive capacity. Expenditure on education, health, communication, increases people's productivity at work and therefore their incomes. With rise in income savings also increases and this in turn has a beneficial effect on investment and capital formation.

Willingness to work, save and invest : Public expenditure, sometimes, brings adverse effects on people's willingness to work and save. Government expenditure on social security facilities may bring such unfavourable effects. For e.g. Government spends a considerable portion of its income towards provision of social security benefits such as unemployment allowances, old age pension, insurance benefits, sickness benefit, medical benefit, etc. Such benefits reduce the desire to work. In other words they act as disincentives to work.

Effect on allocation of resources among different industries & trade : Many a times the government expenditure proves to be an effective instrument to encourage investment in a particular industry. For e.g. If the government decides to promote exports, it provides benefits like subsidies, tax benefits to attract investment towards such industry. Similarly the government can also promote a particular region by providing various incentives for those who make investment in that region.