Unit II

Budgeting and Budgetary Control

Q1) Explain budgeting.

A1)

The term ‘Budget’ appears to have been derived from the French word ‘baguette’ which means ‘little bag' , or a container of documents and accounts. A budget is an accounting plan. It is a formal plan of action expressed in monetary terms. It could be seen as a statement of expected income and expenses under certain anticipated operating conditions. It is a quantified plan for future activities – quantitative blue print for action.

Every organization achieves its purposes by coordinating different activities. For the execution of goals efficient planning of these activities is very important and that is why the management has a crucial role to play in drawing out the plans for its business. Various activities within a company should be synchronized by the preparation of plans of actions for future periods. These comprehensive plans are usually referred to as budgets. Budgeting is a management device used for short‐term planning and control.I t is not just accounting exercise.

Q2) Explain budgetary control.

A2)

Budgetary Control is a method of managing costs through preparation of budgets. Budgeting is thus only a part of the budgetary control. According to CIMA, “Budgetary control is the establishment of budgets relating to the responsibilities of executives of a policy and the continuous comparison of the actual with the budgeted results, either to secure by individual action, the objective of the policy or to provide a basis for its revision.”

The main features of budgetary control are:

Advantages of budgetary control

Q3) Explain budgeting and budgetary control.

A3)

The term ‘Budget’ appears to have been derived from the French word ‘baguette’ which means ‘little bag' , or a container of documents and accounts. A budget is an accounting plan. It is a formal plan of action expressed in monetary terms. It could be seen as a statement of expected income and expenses under certain anticipated operating conditions. It is a quantified plan for future activities – quantitative blue print for action.

Every organization achieves its purposes by coordinating different activities. For the execution of goals efficient planning of these activities is very important and that is why the management has a crucial role to play in drawing out the plans for its business. Various activities within a company should be synchronized by the preparation of plans of actions for future periods. These comprehensive plans are usually referred to as budgets. Budgeting is a management device used for short‐term planning and control. It is not just accounting exercise.

Budgetary Control is a method of managing costs through preparation of budgets. Budgeting is thus only a part of the budgetary control. According to CIMA, “Budgetary control is the establishment of budgets relating to the responsibilities of executives of a policy and the continuous comparison of the actual with the budgeted results, either to secure by individual action, the objective of the policy or to provide a basis for its revision.”

The main features of budgetary control are:

Advantages of budgetary control

Q4) Explain preparation of different budget.

A4)

Preparation of different budgets

Functional Classification:

2. PRODUCTION BUDGET: The production budget is prepared on the basis of estimated production for budget period. Usually, the production budget is based on the sales budget. At the time of preparing the budget, the production manager will consider the physical facilities like plant, power, factory space, materials and labour, available for the period. Production budget envisages the production program for achieving the sales target. The budget may be expressed in terms of quantities or money or both. Production may be computed as follows: Units to be produced = Desired closing stock of finished goods + Budgeted sales – Beginning stock of finished goods.

3. PRODUCTION COST BUDGET: This budget shows the estimated cost of production. The production budget demonstrates the capacity of production. These capacities of production are expressed in terms of cost in production cost budget. The cost of production is shown in detail in respect of material cost, labour cost and factory overhead. Thus production cost budget is based upon Production Budget, Material Cost Budget, Labour Cost Budget and Factory overhead.

4. RAW‐MATERIAL BUDGET: Direct Materials budget is prepared with an intention to determine standard material cost per unit and consequently it involves quantities to be used and the rate per unit. This budget shows the estimated quantity of all the raw materials and components needed for production demanded by the production budget.

5. PURCHASE BUDGET: Strategic planning of purchases offers one of the most important areas of reduction cost in many concerns. This will consist of direct and indirect material and services. The purchasing budget may be expressed in terms of quantity or money.

6. LABOUR BUDGET: Human resources are highly expensive item in the operation of an enterprise. Hence, like other factors of production, the management should find out in advance personnel requirements for various jobs in the enterprise. This budget may be classified into labour requirement budget and labour recruitment budget. The labour necessities in the various job categories such as unskilled, semi‐skilled and supervisory are determined with the help of all the head of the departments. The labour employment is made keeping in view the requirement of the job and its qualifications, the degree of skill and experience required and the rate of pay.

7. PRODUCTION OVERHEAD BUDGET: The manufacturing overhead budget includes direct material, direct labour and indirect expenses. The production overhead budget represents the estimate of all the production overhead i.e. fixed, variable, semi‐variable to be incurred during the budget period.

8. SELLING AND DISTRIBUTION COST BUDGET: The Selling and Distribution Cost budget is estimating of the cost of selling, advertising, delivery of goods to customers etc. throughout the budget period. This budget is closely associated to sales budget in the logic that sales forecasts significantly influence the forecasts of these expenses. Nevertheless, all other linked information should also be taken into consideration in the preparation of selling and distribution budget. The sales manager is responsible for selling and distribution cost budget.

9. ADMINISTRATION COST BUDGET: This budget includes the administrative costs for non‐manufacturing business activities like directors fees, managing directors’ salaries, office lightings, heating and air condition etc. Most of these expenses are fixed so they should not be too difficult to forecast. There are semi‐variable expenses which get affected by the expected rise or fall in cost which should be taken into account. Generally, this budget is prepared in the form of fixed budget.

10. CAPITAL‐ EXPENDITURE BUDGET: This budget stands for the expenditure on all fixed assets for the duration of the budget period. This budget is normally prepared for a longer period than the other functional budgets. It includes such items as new buildings, land, machinery and intangible items like patents, etc. This budget is designed under the observation of the accountant which is supported by the plant engineer and other functional managers.

11. CASH BUDGET: The cash budget is a sketch of the business estimated cash inflows and outflows over a specific period of time. Cash budget is one of the most important and one of the last to be prepared. It is a detailed projection of cash receipts from all sources and cash payments for all purposes and the resultants cash balance during the budget. It is a mechanism for controlling and coordinating the fiscal side of business to ensure solvency and provides the basis for forecasting and financing required to cover up any deficiency in cash. Cash budget thus plays avital role in the financing management of a business undertaken.

FIXED AND FLEXIBLE BUDGET:

2. FLEXIBLE BUDGET: This is a dynamic budget. In comparison with a fixed budget, a flexible budget is one “which is designed to change in relation to the level of activity attained.” The underlying principle of flexibility is that a budget is of little use unless cost and revenue are related to the actual volume of production. The statistics range from the lowest to the highest probable percentages of operating activity in relation to the standard operating performance. Flexible budgets are a part of the feed advance process and as such are a useful part of planning. An equally accurate use of the flexible budgets is for the purposes of control.

TIME BUDGET

(a) Long term Budget: These budgets are prepared on the basis of long‐term projection and portray a long range planning. These budgets generally cover plans for three to ten years. In this regard it is mostly prepared in terms of physical quantities rather than in monetary values.

(b) Short term Budget: In this budget forecasts and plans are given in respect of its operations for a period of about one to five years. They are generally prepared in monetary units and are more specific than long term budgets.

(c) Current Budgets: These budgets cover a very short period, may be a month or a quarter or maximum one year. The preparation of these budgets requires adjustments in short term budgets to current conditions.

(d) Rolling Budgets: A few companies follow the practice of preparing a rolling or progressive budget. In this case companies prepare the budget for a year in advance. A new budget is prepared after the end of each month or quarter for a full year in advance. The figures for the month or quarter which has rolled down are dropped and the statistics for the next month or quarter are added.

MASTER BUDGET

The master budget is a review budget which combines all functional budgets and it may take the form of Financial Statements at the end of budget period. It is also called the operating budget. It embraces the impact of both operating decisions and financing decisions. It provides the necessary plan for operations during the period when all detailed budgets have been completed. A master budget becomes a principal document for the operations of the industry during the period it covers.

Key takeaways –

Q5) Explain variance analysis with budgeted figure.

A5)

Variance Analysis deals with an analysis of deviations in the budgeted and actual financial performance of a company. The causes of the difference between the actual outcome and the budgeted numbers are analyzed to showcase the areas of improvement for the company. At times, it is also a sign of unrealistic budgets, and therefore, in such cases, budgets can be revised.

Variance = Actual Income/Expense – Budgeted Income/Expense.

Need and Importance of Variance Analysis.

• Variance analysis aids efficient budgeting activity as management wishes to have lower deviations from the planned budgets. Wanting a lower deviation usually leads managers to make detailed and forward-looking budgetary decisions.

• Variance analysis acts as a control mechanism. Analysis of significant deviation on essential items helps the company in knowing the causes, and it helps management look into possible ways of how much deviation can be avoided.

• Variance analysis facilitates assigning responsibility and engages control mechanisms on departments where it is required. For example, if labor efficiency variance is seen to be unfavorable or procurement of raw material cost variance is unfavorable, the management can enhance control of these departments to increase efficiency.

Q6) A company produces a product X and operates a system of standard costing. Details of information for the month of July, 2002 are as under:

Standard output from each ton of material: 50 units

Standard price per ton: Rs.150

Actual usage: 100 tons

Actual price per ton: Rs.200

Actual output: 6000 units

Calculate material variances.

A6)

(a) Material Price Variance (MPV):

Actual Quantity (Standard Price – Actual Price)

= 100 [150 – 200]

= Rs.5,000 (Adverse)

(b) Material Usage Variance (MUV):

Standard price [Standard quantity – Actual Quantity]

= 150 [120 – 100]

= Rs.3,000 (Favourable)

(c) Material Cost Variance (MCV):

Standard cost of Material – Actual cost of Material

= [Standard quantity for Actual output x Standard price] – [Actual quantity for Actual output x Actual Price]

= [120 x 150] – [100 x 200]

= 18,000 – 20,000

= Rs.2,000 (Adverse)

Rectification / Verification:

MCV = MPV + MUV

Rs.2,000 (Adverse) = Rs.5,000 (Adverse) + Rs.3,000 (Favourable)

Or, Rs.2,000 (Adverse) = Rs.2,000 (Adverse)

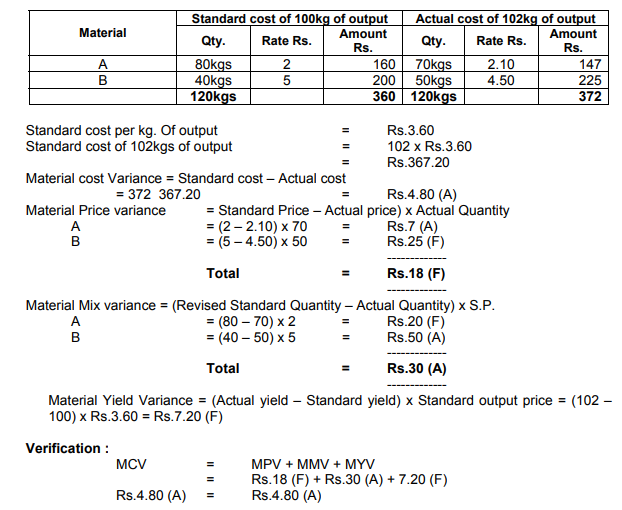

Q7) 80 Kg. of material A at a standard price of Rs.2 per kg and 40kgs. of material B at a standard price of Rs.5 per kg. Were to be used to manufacture 100kgs. of a chemical. During a month, 70kgs. of material A priced at Rs.2.10per kg. And 50kgs. of Material B priced at Rs.4.50per kg. were actually used and the output of the chemical was 102 kgs.

Find out the material variance.

A7)

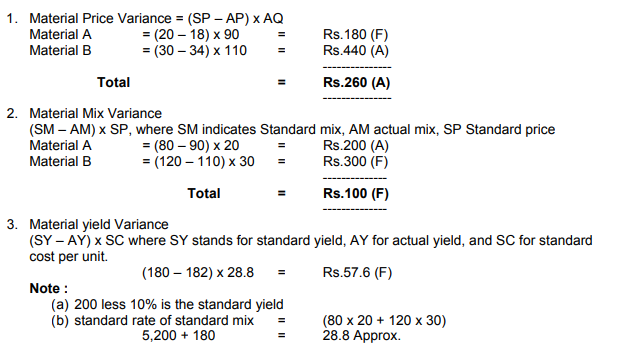

Q8) The standard cost of a chemical mixture is:

40% material A at Rs.20 per kg.

60% material B at Rs.30 per kg.

A standard loss of 10% expected in production. During a period there is used:

90kgs material A at cost of Rs.18 per kg

110kgs material B at cost of Rs.24 per kg.

The weight produced is 182kgs of good product.

Calculate:

1. Material price variance

2. Material mix variance

3. Material yield variance

4. Material cost variance.

A8)

Materials Cost Variance = Materials price Variance + Materials Mix Variance + Material

Yield Variance

Rs.102.40 (A) = Rs.260 (A) + Rs.100 (F) + Rs.57.60 (F) = Rs.102.40.

Q9) With the help of the following data, calculate:

(i) Labour Cost Variance,

(ii) Labour Rate Variance,

(iii) Labour Efficiency Variance

Standard hours: 40 @ Rs.3 per hour

Actual hour: 50 @ Rs.4 per hour

A9) (i) Labour Cost Variance [LCV]:

[Standard Time x Standard Rate] – [Actual Time x Actual Rate]

= [40 x 3] – [50 x 4]

= 120 – 200

= Rs.80 (Adverse)

(ii) Labour Rate Variance [LRV]:

Actual Time [Standard Rate – Actual Rate]

= 50 [3 – 4]

= Rs.50 (Adverse)

(iii) Labour Efficiency Variance [LEV]:

Standard Rate [Standard Time – Actual Time]

= Rs.3 [40 – 50]

= Rs.30 (Adverse)

Reconciliation / Check :

LCV = LRV + LEV

Rs.80 (Adverse) = Rs.50 (Adverse) + Rs.30 (Adverse).

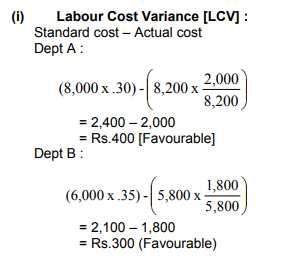

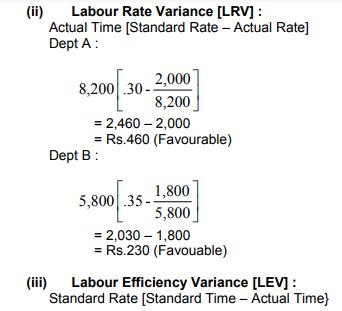

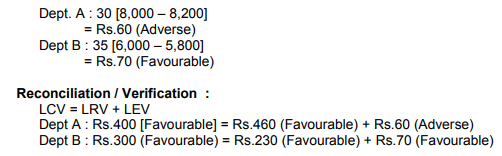

Q10) From the data given below, calculate labour variances for the two departments-

A10)

Q11) Calculate Labour variances from the following data:

Gross Direct wages Rs.30,000

Standard hours 1,600

Standard rate per hour Rs.15

Actual hours paid 1,500

Actual hours paid include hours not worked (abnormal idle time) : 50

A11)

(i) Labour Cost Variance [LCV] :

[Standard Time x Standard Rate] – [Actual Time x Actual Rate]

= [1,600 x 15] – [1,500 x 20]

= 24,000 – 30,000

= Rs.6,000 (Adverse)

(ii) Labour Rate Variance [LRV]:

Actual Time [Standard Rate – Actual Rate]

= 1,500 [15 – 20]

= Rs.7,500 (Adverse)

(iii) Labour Efficiency Variances [LEV] :

Standard Rate [Standard Time – Actual Time]

= 15 [1,600 – 1,450]

= Rs.2,250 (Favourable)

(iv) Labour Idle time Variance [LITV] :

Standard Rate x Abnormal Idle Time

= 15 x 50

= Rs.750 (Adverse)

Reconciliation / Check:

LCV = LRV + LEV + LITV

Rs.6,000 (Adverse) = Rs.7,500 (Adverse) + Rs.2,250 (Favourable) + Rs.750 (Adverse)

Q12) A factory has estimated its overheads for one year at Rs.96,000. The factory runs for 300 days in a year. It works for 8 hours a day. The total budgeted production for the year is 24,000 articles.

Actual data are also given to you as under for the month of April.

Actual overhead Rs.8,500

Output 2,100 articles

Idle time 4 hours

Calculate: (1) Overhead cost variance, (2) Overhead budget variance, (3) Overhead efficiency variance, (4) Idle Time variance.

A12)

(1) Overhead Cost Variance:

Formula:

Standard overhead cost of actual output – Actual overhead cost

= Rs.8,400 – Rs.8,500 = Rs.100 (A)

(2) Overhead budget variance or expenditure variance

Budget overheads – Actual overheads

= Rs.8,000 – Rs.8,500 = Rs.500 (A)

(3) Overhead efficiency variance

(i) Where standard overhead rate per unit is given

(Actual production – Standard production in actual hours) x Standard overhead rate per unit

= (2,100 – 1,960) x Rs.4 = Rs.560 (F)

(ii) Where standard overhead rate per hour is given

(Actual Hours – Standard hours for actual production) x Standard overhead rate per hour

= (196 – 210) x Rs.40 = Rs.560 (F)

(4) Idle Time variance:

(i) Where standard overhead rate per unit is given

Formula:

Production lost in idle time x overhead standard rate per unit

= 40 x Rs.4 = Rs.160 (A)

(ii) Where standard overhead rate per hour is given

Formula:

Idle Time x overhead standard rate per hour

= 4 x Rs.40 = Rs.160 (A)

Check:

Overhead efficiency variance + Overhead idle time variance = Overhead volume variance

Rs.560 (F) + Rs.160 (A) = Rs.400 (F)

Overhead volume variance + Overhead budget variance = Overhead cost variance

Rs.400 (F) + Rs.500 (A) = Rs.100 (A)

Working Notes:

(i) Standard overhead cost of actual output

If monthly production is 2,000 units, overhead cost is Rs.8,000

If monthly production is 2,100 units, overhead cost is

8,000 / 2,000 x 2,100 = Rs.8,400

(ii) Standard production in actual hours

Yearly hours 300 days x 8 = 2,400 hours

Monthly hours = 2,400 / 12 = 200 hours

∴Actual hours worked = 200 – 4 = 196 hours

If factory runs 200 hours standard production is 2,000 units

If factory runs 196 hours standard production 2,000 / 200 x 196 = 1,960 units

(iii) Standard overhead rate per hour

Monthly overhead cost Rs.8,000

Standard hours in a month 200

∴Rate per hour = 8,000 / 200 = Rs.40 per hour.

(iv) Standard overhead rate per unit

Standard units 2,000

Overhead cost Rs.8,000

∴Rate per unit 8,000 / 2,000 = Rs.4 per unit

Q13) A manufacturing company operates a costing system and showed the following data in respect of the month of November.

Actual No. of working days 22

Actual man hours worked during the month 4,300

Number of products produced 425

Actual overhead incurred (Rs.) 1,800

Relevant information from the company’s budget and standard cost data are as follows :

Budgeted number of working days per month 20

Budgeted man hours per month 4,000

Standard man hours per product 10

Standard overhead rate per man hour Rs.0.50

You are required to calculate for the month of November.

(a) the overhead variance.

(b) The calendar variance

(c) The volume variance.

A13)

(a) Overhead cost variance

Standard overhead cost of actual production – Actual overhead cost

Rs.2,125 – Rs.1,800 = Rs.325 (F)

(b) Overhead calendar variance

(i) where standard overhead rate per unit is given

(Revised budgeted quantity, i.e., budgeted quantity on the basis of actual no. of working days – Budgeted quantity) x Standard rate per unit

(440 – 400) x Rs.5 = Rs.200 (F)

(ii) where standard rate per hour is given

(Budgeted No. of hours for actual working days – Budgeted hours) x Standard overhead rate per hour

(4,400 – 4,000) x Re.0.50 = Rs.200 (F)

(c) Overhead volume variance

(i) Where standard rate per unit is given

(Actual production – Budgeted production) x Standard overhead rate per unit

(425 – 400) x Rs.5 = Rs.125 (F)

(ii) Where standard rate per hour is given

(Standard hours for Actual production – Budgeted hours) x Standard overhead rate per hour

(4,250 – 4,000) x Re.0.50 = Rs.125 (F)

Working Notes :

(1) Standard cost per unit

Re.0.50P x 10 hours = Rs.5 per unit

(2) Standard overhead cost of actual production

425 units x Rs.5 per unit = Rs.2,125

(3) Revised budgeted quantity

If 20 are the working days, standard production 400 units

If 22 are the working days, standard production 400/20 x 22 = 440 units

(4) Budgeted hours for actual working days

In 20 working days, the standard hours are 4,000

∴ In 22 working days, the standard hours are 4,000 / 20 x 22 = 4,400 hours

(5) Standard hours for actual production

Actual production x Standard hours per unit = 425 x 10 = 4,250 hours