UNIT I

Accounting Standards issued by ICAI and Inventory Valuation

PART A

Question Bank

Q1) Companies have a practice of valuing inventory according to FIFO. This year, the company changed its valuation method to the weighted average method. The value of inventory per FIFO is Rs. It is 2 lakhs, which is Rs according to the weighted average method. 18,000. AS 1 --How does the company disclose such matters in its financial statements in accordance with the disclosure of accounting policies? (5 marks)

A1) A simple disclosure that the accounting policy has changed is not very useful to the reader of the financial statements. Therefore, the impact of the change should be disclosed whenever it is identifiable. The company switched from its previous practice of using FIFOs to a weighted average to check inventory costs. When the final stock by FIFO is Rs. It is 2 lakhs, which is Rs according to the weighted average equation. 18,000 rupees, change of accounting policy will reduce the profit and value of inventory by rupees. 20,000. Companies can disclose changes in accounting policies in the following ways:

"The company evaluates inventory by cost or net realizable value, whichever is lower. The company evaluates inventory at cost because the net realizable value of all items in inventory this year exceeded their respective costs. This year, the company changed to a weighted averaging formula that better reflects inventory consumption patterns to see inventory costs from previous practices of using it for FIFO purposes. Due to policy changes, inventory profits and value have been reduced by Rs. 20,000 feet.

Accounting policy changes are disclosed when they are reasonably expected to have a significant impact on future accounting periods, even if the changes do not have a significant impact on the current accounting period.

Q2) How much does a Service Provider's Inventory Cost? (5 marks)

A2) Service provider inventory costs are measured in production costs. These costs mainly include labor costs and labor costs that are directly related to the provision of services. This includes supervisors and overhead costs associated with the provision of such services.

Personnel costs and other costs related to selling, general and administrative operations are not included in inventory costs. However, we recognize that such costs are the costs of the period in which they were incurred.

In addition, service provider inventory costs do not include rates of return or overheads not attributable to such services. These are often considered at the price requested by the service provider.

Inventory Valuation Method

Different methods of inventory valuation include:

1. Specific Identification Method

To apply a particular identification method, you need to be able to easily identify each item sold and each item that closes inventory. Such a method can only be applied if the various purchases made by the company can be physically distinguished.

Therefore, items sold at a particular cost during the accounting period can be included in the cost of goods sold. Also, the cost of certain items left or on hand can be included in the final inventory. Companies that manufacture or handle expensive, easily distinguishable items can take advantage of this valuation method. Such items include cars, furniture, jewellery and more.

2. First-in first-out (FIFO)

The first-in, first-out method assumes that the goods are consumed in the order in which they were purchased. That is, the first item purchased is consumed first in the manufacturing industry and sold first in the case of a merchandising company.

Therefore, with this method, recently purchased items are part of the final inventory.

3. Weighted Average Cost Method (WAC)

This method calculates the average cost of each item that can be sold. Such costs are calculated using the weighted average of similar items available at the beginning of the year and the cost of similar items purchased or manufactured that year. In addition, cost of goods sold and end-of-term inventories are calculated at the average cost so calculated.

In addition, the weighted average is calculated on a regular basis or, in some cases, on the arrival of new cargo.

Disclosure in Financial Statements

In accordance with Accounting Standard 2 (AS 2), financial statements must disclose the following details regarding inventories:

- The accounting policy used to measure inventory. This includes the method of inventory valuation that you follow.

- Amount of inventory recorded as an expense over a period of time.

- Total inventories and carrying amount in the classification of raw materials, work in process, finished products, spare parts, etc. applicable to companies.

- Book value of inventories recorded at fair value after deduction of selling costs.

- Devaluation of inventory recognized as an expense during the period.

- Reversal of write-downs identified as a decrease in the amount of inventory identified as an expense during the period.

- Events that lead to the cancellation of write-downs on inventories.

- Inventories pledged as collateral for debt.

Q3) What is inventory cost? (5 marks)

A3) The cost of inventories includes the following costs:

- Purchase,

- Conversion.

- Keep inventory in current location and status

Let's look at these individually.

1. Purchase cost

The cost of purchasing inventories includes the following costs:

Inventory Purchase or Purchase Price

Import duties and other taxes (if applicable) (this does not include duties and taxes that the entity can later recover from the relevant tax authorities)

Transportation, handling and other costs directly related to the purchase of materials, finished products and services.

When calculating the purchase cost, it should be noted that discounts, rebates, and items of similar nature are reduced.

2. Conversion cost

The conversion cost of inventories consists of the costs directly related to the conversion of raw materials to finished products. For example, direct labor. These costs can be divided into two types:

- With fixed production costs

- Variable costs of production

Fixed cost

These are indirect production costs that do not change as the output level changes. For example, depreciation, administration and administration costs, maintenance of factory buildings, etc.

Fixed production costs are allocated to conversion costs based on the entity's normal capacity. Normal capacity is none other than the amount of production that is likely to be achieved on average over the number of seasons or production period under normal circumstances. It also takes into account capacity loss due to planned maintenance.

Fluctuating Production Costs

On the other hand, variable costs are costs that fluctuate depending on the amount of production. For example, indirect labor, materials, etc.

Such costs are allocated to conversion costs based on the actual utilization of the production equipment.

In the manufacturing process, multiple products may be manufactured at the same time. In such cases, it is difficult to individually identify the conversion costs associated with the product. For example, the production of joint products or the production of major products also produces by-products. Therefore, conversion costs in such cases are allocated on a reasonable and consistent basis.

Other costs

Other costs also form part of the inventory to the extent that such costs contribute to returning the inventory to its current state and location.

Therefore, the above three types of costs are taken into account when calculating the cost of inventory. However, some costs are not included in the inventory estimate. Rather, they are perceived as expenses during the period in which they occur. Examples of such costs are:

- Unusual amounts of waste, labor costs, or other production costs,

- Storage costs in addition to the costs essential to the production process prior to the next production stage,

- Management overhead of a nature that is not responsible for acquiring inventory at the current location and condition,

- Selling costs,

Q4) What are inventories and net realizable value? (5 marks)

A4) Inventory, sometimes referred to as merchandise, refers to the merchandise or materials that a company holds to sell to its customers in the near future.

In other words, these goods and materials serve no other purpose in the business except that they are sold to customers for profit. They are not used to promote produce or business. The sole purpose of these liquid assets is to sell them to customers for profit, but just because an asset is sold does not mean that it is considered inventories. To determine if an asset needs to be accounted for as a commodity, you need to look at three key characteristics of inventory.

First, the assets need to be part of the company's core business. For example, sandwich store delivery trucks are not considered inventories because they have nothing to do with the main business of manufacturing and selling sandwiches. This is considered a sandwich store fixed asset. On the other hand, for car dealers, this truck is considered in stock because it is in the business of selling vehicles.

Second, the asset must be sellable, otherwise it will be immediately available for sale. If you were able to sell some of your business assets, but have never actually been able to sell them, they are not in stock. These are just assets or investments in the company.

Third, the purpose of owning assets must be to sell them to customers. Returning to the sandwich store example, the truck was not intended to be sold to customers. It was purchased to deliver sandwiches and sold when the job could not be accomplished. Car dealers, on the other hand, buy vehicles for resale only. Therefore, trucks are considered in stock for them.

Inventory is an asset such as:

- Holding for sale in the normal business process.

- In the production process of such sales.

Also, in the form of materials or consumables consumed in the production process or provision of services.

Such inventories are recorded at cost or net realizable value, whichever is lower.

To understand this inventory measurement, let's look at the definitions of concepts such as net realizable value, fair value, and inventory cost.

The net realizable value is the value that can be obtained from the sale of an asset minus the cost of completing and executing such sale. In other words, it is the selling price of inventory in normal business processes minus the estimated costs associated with the completion and sale of such inventory.

The fair value of inventory is the amount by which inventory can be exchanged between knowledgeable buyers and sellers in the market. However, this exchange must be a business-to-business transaction.

Therefore, the net realizable value of an inventory may not be equal to or equal to its fair value minus the cost of selling the inventory.

Q5) How to recognize and disclose the amount of cancellation of the valuation reduction of inventories as the reduction of inventories? (5 marks)

A5) Section 34, “Especially” of Ind AS 2, states that “the amount of cancellation of inventory write-down resulting from an increase in net realizable value shall be recognized as a decrease in the amount of inventory recognized as an expense”. It is stipulated. During the period when the reversal occurs. "

Section 36 (f) requires disclosure of "the amount of write-down reversal recognized as a decrease in the number of inventories recognized as an expense during the period in accordance with Section 34".

In accordance with the above, the write-down reversal should be recognized in the income statement as a decrease in the amount of inventory that is recognized as an expense. The following is a sample disclosure in the financial statements in this regard.

Q6) What is the difference between "net realizable value" and "fair value"? are you able to explain with an honest example? (8 marks)

A6) Net Realizable Value Method:

This method is used for damaged or partially obsolete inventory. Net realizable value is the estimated selling price minus the cost of completion. Shares are valued at acquisition cost, as the selling price is usually lower.

Losses incurred by writing down shares to their net realizable value are adjusted to the income statement.

This method should not exceed the expected feasible value.

Net realizable value is that the estimated asking price during a normal business process minus the estimated cost of completion and therefore the estimated cost of selling.

Fair value is the actual value of an asset (commodity, stock, or security) agreed upon by both the seller and the buyer. Fair value applies to products sold or traded within the market to which it belongs or under normal conditions, to not products that are liquidated. It is designed to create a fair amount and value for the buyer without damaging the seller.

For example, Company A sells shares to his Company B for $ 30 per share. The owner of Company B believes that the acquired shares can be sold for $ 50 per share, so he decides to buy one million shares at the original price. The sale is considered fair value because the price has been agreed upon by both parties and both have benefited from the sale, despite the potential for significant profits for Company B.

Fair value is that the price you receive to sell an asset or transfer a liability in an orderly transaction between market participants on the measurement date.

According to the definition above, net realizable value is that the net amount that a corporation expects to be realized from the sale of inventories within the normal course of business. Fair value, on the opposite hand, reflects the worth at which an orderly transaction of selling an equivalent inventory during a major (or most favourable) market takes place between market participants on the measurement date. The previous is an entity-specific measurement. The latter may be a market-based measurement. Internet realizable value of inventories might not be adequate to the fair value after deducting the value of sale.

Example:

The entity holds a listing of 10000 units, and after selling the value, each can sell an equivalent on the market at Rs.10 /-. The entity has an order to sell inventory at Rs. 11 /-In this example, the fair value is Rs 10 /-each, but internet realizable value is Rs. 11 /-Each.

Fair Value and Market Value

- Market prices also differ from fair value in the following ways:

- The market price fluctuates more than the market price.

- It may be based on the latest pricing or quote for the asset. For example, if Company A's stock valued $ 30 in the last three months and dropped to $ 20 during the latest valuation, its market value would be $ 20.

- Market value depends on the supply and demand of the market in which the asset is bought and sold. For example, the price of a home for sale is determined by existing market conditions in the area.

- If the owner tries to sell the property for $ 200,000 during a downturn in the real estate market, it may not be sold due to low demand. But if it's offered for $ 500,000 during a high time, it may sell at that price.

Q7) Write short note on Radio Frequency Identification (RFID). (8 marks)

A7) Radio frequency identification (RFID) tags are attached to individual products or product boxes to get radio signals that contain information about the merchandise. Passive tags reflect a sign generated by a reader which will read the tag from about 10 feet away. The active tag contains an influence supply and generates its own signal, which expands the range. When products within the warehouse are tagged, readers can instantly determine inventory on racks on shelves, improving inventory accuracy and control.

A7) Radio frequency identification (RFID) tags are attached to individual products or product boxes to get radio signals that contain information about the merchandise. Passive tags reflect a sign generated by a reader which will read the tag from about 10 feet away. The active tag contains an influence supply and generates its own signal, which expands the range. When products within the warehouse are tagged, readers can instantly determine inventory on racks on shelves, improving inventory accuracy and control.

Reduction of Inventory Shrinkage

Inventory reduction may be a term used for product identification, storage, shipping errors, and inventory loss caused by theft. Improved inventory tracking with RFID tags reduces errors because the method is fully automated once the tags are attached. Discrepancies are going to be immediately visible to the staff liable for tracking inventory. Companies also reduce the prospect of theft if RFID systems track products and warehouse warehousing management systems track access to warehouses.

Real-Time Inventory Management

Non-RFID inventory management systems believe records of products received and shipped, and regular manual inventory to work out the amount of things available. These numbers are often inaccurate. If all items available have RFID tags and a reader is found near each rack on the shelf, the amount of things available is that the actual number supported the amount of things on the shelf at that point. Is displayed as. Therefore, RFID helps avoid backorders thanks to unexpected out-of-stock conditions.

Reduction of labor costs

RFID systems reduce the quantity of manual labour required in 3 ways . The method of recording the movement of products in and out of inventory are often highly automated, reducing the necessity to take care of records manually. Manual inventory will occasionally check for defective or untagged items. Fewer errors eliminate the necessity for manual work to correct inventory mistakes. Labor costs related to RFID tagging will increase, but using tags to exchange barcode labels can reduce the value increase.

Better Asset Utilization

In addition to the particular product, warehouse assets include dollies, trucks, and other means of transportation, also because the warehouse itself. If the corporate knows the particular level of product inventory, it can reduce inventory and respond confidently to customer demands instead of processing uncertain quotes. When dollies and trucks transport goods, they will take full advantage of some products that are but full load, instead of manipulating them. You'll make the warehouse itself smaller, otherwise you can store more or differing types of inventories. Enterprises got to balance these savings with the value of buying and installing tags and tag readers to work out if RFID systems are economically meaningful.

Q8) How does the Barcode Inventory System work? (5 marks)

A8) The automatic inventory system works by scanning the item's barcode. Barcode scanners are used to read barcodes, and the information encoded by the barcodes is read by the machine. This information is tracked by a central computer system. For example, a purchase order may contain a list of items that are pulled for packaging and shipping. In this case, the inventory tracking system can perform various functions. Helps workers find items in the warehouse order list, encodes shipping information such as tracking numbers and shipping addresses, removes these purchased items from inventory, and removes the exact number of items in stock can be maintained.

All this data works together to provide the enterprise with real-time inventory tracking information. Inventory management systems make it easy to find and analyze inventory information in real time with a simple database search and are an integral part of any business that moves the supply of goods.

Barcode Stocking Software

Some of the inventory management systems that need to be considered are software. Barcode inventory software is a core component because it has the ability to assist in inventory management in a warehouse or retail environment. The right software for your needs can help streamline your system, update inventory automatically, maintain accuracy, and reduce mistakes. Talk to your inventory specialist to find the right software.

There are many benefits to using barcodes in the inventory management process, including:

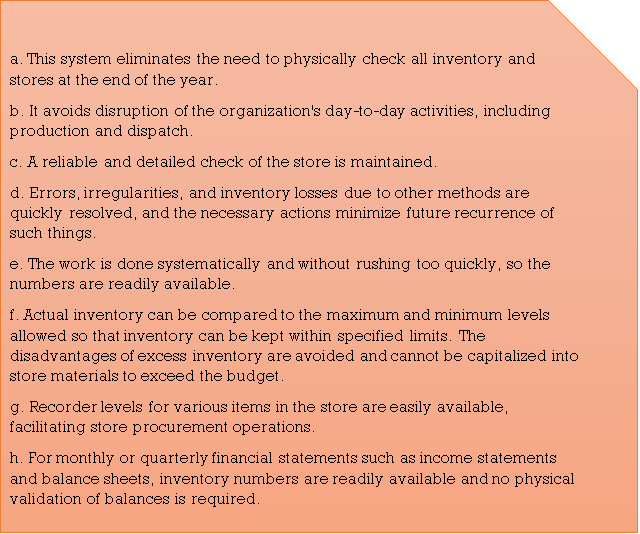

Q9) What is a Perpetual Inventory System? (8 marks)

A9) The permanent inventory system uses technology to track and update inventory records each time you receive or sell an item. In a perpetual inventory system, the sale of inventory items increases cost of goods sold (COGS) and is also updated in accounting records to ensure that the number of items in the store or in storage is accurately reflected in the inventory account.

Permanent inventory systems are more robust than regular inventory systems, where companies regularly audit inventory to update inventory information. These audits include regular and regular physical inventory. The main difference between a permanent inventory system and a regular inventory system is that the former has a system that updates inventory information in real time, while the latter uses a more manual process.

Increased use of Perpetual Inventory System

Until now, permanent inventory systems have not been widely used due to the difficulty of recording and processing large amounts of data quickly and accurately.

However, in recent years, technical capabilities have improved, business and accounting practices have improved, inventory tracking systems can now be managed using computers and scanners, and the burden of permanent inventory tracking has been reduced.

A Perpetual Inventory System can be defined as "a system of records maintained by the management department that reflects the physical movement of inventory and the current balance." Therefore, it is a system that checks the balance each time material is received and issued through inventory records to facilitate regular checks and avoid closing the company for inventory. To ensure the accuracy of permanent inventory records (bincards and store ledgers), physical verification of the store is carried out by an ongoing inventory program.

The operation of the Permanent Inventory System is as follows: -

a. Inventory records are maintained and up-to-date transaction postings are made so you always know your current balance.

b. Various sections of the store are taken up by rotation for physical checks. Some items are checked daily, so all items may be checked many times during the year.

c. Stores that have arrived but are awaiting quality inspection are not yet listed in the inventory record, so they will not be confused with regular stores at the time of on-site confirmation.

d. In some cases, after counting, weighing, measuring, or listing, the physical inventory available in the store is properly recorded on the bin card / inventory tag and inventory check sheet.

Do not confuse the permanent inventory system with continuous inventory. Continuous inventory is an important feature of the permanent inventory system. Permanent inventory means a system of inventory records and continuous inventory, and continuous inventory means only physical verification of inventory records with actual inventory.

In continuous inventory, physical verification is done throughout the year. Randomly pick and check 10 to 15 items every day so that you can keep the surprise element of inventory check and check each item many times each year. On the other hand, regular checks are usually done at the end of the year, so the surprise element is missing.

Benefits of Perpetual Inventory System:

Q10) When will the regular inventory system be used? (8 marks)

A10) SMEs with a small number of SKUs use a regular system if they are not concerned about expanding their business over time. Depending on the product and needs, the recurring system can also be used in combination with a permanent system.

Any company can use a recurring system because no additional equipment or coding is required to use the recurring system. Therefore, the cost is low. Implement and maintain. In addition, you can train your staff to provide easy inventory when time is limited or when staff turnover is high. For example, seasonal staff may come and go. You can quickly count the products you are working on, but permanent systems that provide more accurate inventory require staff training on electronic scanners and data entry. Read the Perpetual Inventory Guide to learn more about the Perpetual System and how it provides a more accurate inventory solution.

If you manage your supply chain process, sell some products, and look at the products that flow through your business, you can also use a recurring system. If you need to investigate to identify missing inventory or disproportionate numbers, a regular system will not help. This issue arises as operations grow and become more difficult to actively manage.

Milner describes the regular system as "a simple approach to inventory management that helps those small organizations that have a simple approach to inventory management." These businesses do not always have a clear relationship between raw materials or purchased items and the final product sold. An example of a business that uses a regular system is a food bank. They frequently counted physical inventories to determine final inventory quantities. "

Overview

The recurring inventory system does not track inventory daily. Rather, the organization can know the start and end inventory levels for a particular time period. These types of inventory management systems use physical inventory to track inventory. When the physical inventory is complete, the balance of the purchase account shifts to the inventory account and is adjusted to match the cost of the closing inventory. Organizations can choose whether to calculate the cost of closing inventory using the LIFO or FIFO inventory accounting method or another method.

Note that the starting stock is the ending stock for the previous period.

Benefits of Regular Inventory System

The main advantages of adopting a recurring inventory system are its ease of implementation, its low cost, and the reduction in personnel required to implement it. Adding a regular system to your business takes only a short time. You can collect product data with a simple count of legitimate paper, especially if you only offer a small number of products. In many cases, a basic daytime or weekly count is sufficient for SMEs to properly handle their inventory. This means you don't need expensive and complex equipment, only important information gathering tools such as pens and paper.

However, one of the major drawbacks is that it collects minimal information, usually only the number of individual products. In addition, we do not collect or report this data in "real time". Inventory numbers are updated at different times, not when buying or selling. In fact, if you need to track your product from start to finish or investigate shortages or excesses, you don't have much information to move on. The cause of the problem cannot be quickly identified.

Disadvantages or Drawbacks:

There are some drawbacks to using a Periodic Inventory System.

First, when the physical inventory is completed, normal business activities are almost interrupted. As a result, workers may rush physical counts due to time constraints. Recurring inventory systems typically do not use inventory trackers and therefore cannot maintain inventory continuously, which can lead to more prevalence of errors and fraud. Also, with a regular inventory management system, the intervals between counts are so long that it is more difficult to pinpoint where inventory count discrepancies occur. The effort required for a regular inventory management system is better suited for small businesses.

- Estimated Error: During the period between inventory, you need to estimate the cost of goods sold and the products and quantities available. After completing the physical count, this estimate may be far from the actual cost of goods sold.

- Significant Adjustment: During the period between inventories, there is no way to describe lost, excess, or obsolete merchandise. This can result in significant and costly adjustments after the next physical count. The periodic table is up-to-date only immediately after inventory and accounting events.

- Unable to Scale: Regular systems have some margin because they are based on their ability to track merchandise. However, expanding your business with a regular system takes more time and effort as you grow and add products to your inventory.

Example:

An example of a recurring system would include accounting for the starting inventory and all purchases made during the period as credits. Instead of recording their own sales during the debit period, the company finally performs a physical count and now adjusts the account.

Cost flow assumptions are inventory costing methods in the periodic system that companies use to calculate COGS and final inventory. Starting inventory and purchases are the inputs that an accountant uses to calculate the cost of an item that can be sold. Then apply this number to cost flow assumptions that your company chooses to use, such as FIFO, LIFO, and weighted average.

PART B

Question Bank

Q11) ABC Ltd. Was making provision for non-moving inventories based on issues for the last 12 months up to 31.3.2016. The company wants to provide during the year ending 31.3.2017 based on technical evaluation:( 5 marks)

Total value of inventory Rs. 100 lakhs

Provision required based on 12 months issue Rs. 3.5 lakhs

Provision required based on technical evaluation Rs. 2.5 lakhs

Does this amount to change in Accounting Policy? Can the company change the method of provision?

A1) The decision of making provision for non-moving inventories on the basis of technical evaluation does not amount to change in accounting policy. Accounting policy of a company may require that provision for non-moving inventories should be made. The method of estimating the amount of provision may be changed in case a more prudent estimate can be made.

In the given case, considering the total value of inventory, the change in the amount of required provision of non-moving inventory from Rs. 3.5 lakhs to Rs. 2.5 lakhs is also not material. The disclosure can be made for such change in the following lines by way of notes to the accounts in the annual accounts of ABC Ltd. For the year 2016-17:

“The company has provided for non-moving inventories on the basis of technical evaluation unlike preceding years. Had the same method been followed as in the previous year, the profit for the year and the corresponding effect on the year end net assets would have been lower by Rs. 1 lakh.”

Q12) The company deals in three products, A, B and C, which are neither similar nor interchangeable. At the time of closing of its account for the year 2016-17, the Historical Cost and Net Realisable Value of the items of closing stock are determined as follows:( 5 marks)

Items | Historical Cost (Rs. in lakhs) | Net Realisable Value (Rs. in lakhs) |

A | 40 | 28 |

B | 32 | 32 |

C | 16 | 24 |

Calculate the value of closing stock.

A2) As per AS 2 (Revised) on ‘Valuation of Inventories’, inventories should be valued at the lower of cost and net realisable value. Inventories should be written down to net realisable value on an item-by-item basis in the given case.

Items | Historical Cost (Rs. in lakhs) | Net Realisable Value (Rs. in lakhs) | Valuation of closing stock (Rs. in lakhs) |

A | 40 | 28 | 28 |

B | 32 | 32 | 32 |

C | 16 | 24 | 16 |

| 88 | 84 | 76 |

Hence, closing stock will be valued at Rs. 76 lakhs.

Q13) X Co. Limited purchased goods at the cost of Rs. 40 lakhs in October, 2016. Till March, 2017, 75% of the stocks were sold. The company wants to disclose closing stock at Rs. 10 lakhs. The expected sale value is Rs. 11 lakhs and a commission at 10% on sale is payable to the agent. The company needs your advice on the correct value of closing stock to be disclosed as at 31.3.2017.

A3) As per AS 2 (Revised) “Valuation of Inventories”, the inventories are to be valued at lower of cost or net realisable value.

In this case, the cost of inventory is Rs. 10 lakhs. The net realisable value is 11,00,000 x 90% = Rs. 9,90,000. So, the stock should be valued at Rs. 9,90,000.

Q14) In a production process, normal waste is 5% of input. 5,000 mtr of input were put in process resulting in wastage of 300 mtr. Cost per mtr of input is Rs. 1,000. The entire quantity of waste is on stock at the year end. State with reference to Accounting Standard, how will you value the inventories in this case? (5 marks)

A4) As per AS 2 (Revised), abnormal amounts of wasted materials, labour and other production costs are excluded from cost of inventories and such costs are recognised as expenses in the period in which they are incurred.

In this case, normal waste is 250 mtr and abnormal waste is 50 mtr. The cost of 250 mtr will be included in determining the cost of inventories (finished goods) at the year end. The cost of abnormal waste (50 mtr x 1,052.6315 = Rs. 52,632) will be charged to the profit and loss statement.

Cost per mtr (Normal Quantity of 4,750 mtr) = 50,00,000 / 4,750 = Rs. 1,052.6315

Total value of inventory = 4,700 mtr x Rs. 1,052.6315 = Rs. 49,47,368.

Q15) The Board of Directors decided on 31.3.2017 to increase the sale price of certain items retrospectively from 1st January, 2017. In view of this price revision with effect from 1st January 2017, the company has to receive Rs. 15 lakhs from its customers in respect of sales made from 1st January, 2017 to 31st March, 2017. Accountant cannot make up his mind whether to include Rs. 15 lakhs in the sales for 2016-2017.Advise.

A5) Price revision was affected during the current accounting period 2016-2017. As a result, the company stands to receive Rs. 15 lakhs from its customers in respect of sales made from 1st January, 2017 to 31st March, 2017. If the company is able to assess the ultimate collection with reasonable certainty, then additional revenue arising out of the said price revision may be recognised in 2016-2017.

Q16) Y Ltd., used certain resources of X Ltd. In return X Ltd. Received Rs. 10 lakhs and Rs. 15 lakhs as interest and royalties respective from Y Ltd. During the year 2016-17. You are required to state whether and on what basis these revenues can be recognised by X Ltd.

A6) As per AS 9 on Revenue Recognition, revenue arising from the use by others of enterprise resources yielding interest and royalties should only be recognised when no significant uncertainty as to measurability or collectability exists. These revenues are recognised on the following bases:

(i) Interest: on a time, proportion basis taking into account the amount outstanding and the rate applicable.

(ii) Royalties: on an accrual basis in accordance with the terms of the relevant agreement.

Q17) A claim lodged with the Railways in March, 2015 for loss of goods of Rs. 2,00,000 had been passed for payment in March, 2017 for Rs. 1,50,000. No entry was passed in the books of the Company, when the claim was lodged. Advise P Co. Ltd. About the treatment of the following in the Final Statement of Accounts for the year ended 31st March, 2017. (5 marks)

A7) AS 9 on ‘Revenue Recognition’ states that where the ability to assess the ultimate collection with reasonable certainty is lacking at the time of raising any claim, revenue recognition is postponed to the extent of uncertainty involved. When recognition of revenue is postponed due to the effect of uncertainties, it is considered as revenue of the period in which it is properly recognised. In this case it may be assumed that collectability of claim was not certain in the earlier periods. This is supposed from the fact that only Rs. 1,50,000 were collected against a claim of Rs. 2,00,000. So, this transaction cannot be taken as a Prior Period Item.

In the light of AS 5, it will not be treated as extraordinary item. However, AS 5 states that when items of income and expense within profit or loss from ordinary activities are of such size, nature, or incidence that their disclosure is relevant to explain the performance of the enterprise for the period, the nature and amount of such items should be disclosed separately. Accordingly, the nature and amount of this item should be disclosed separately.

Q18) Prepare a statement showing the pricing of issues, on the basis of

(a) FIFO and

(b) Weighted Average methods from the following information pertaining to Material-D (8 marks)

2016 March 1 Purchased 100 units @ Rs 10 each

2 Purchased 200 units @ Rs 10.2 each.

5 Issued 250 units to Job X vide M.R.No.12

7 Purchased 200 units @ Rs 10.50 each

10 Purchased 300 units @ Rs 10.80 each

13 Issued 200 units to Job Y vide M.R.No.15

18 Issued 200 units to Job Z vide M.R.No.17

20 Purchased 100 units @ Rs 11 each

25 Issued 150 units to Job K vide M.R.No.25

A8)

- FIFO Method

Stores Ledger

Date | Receipts | Issues | Balance | ||||||

Qty. | Price Rs | Value Rs | Qty. | Price Rs | Value Rs | Qty. | Price Rs | Value Rs | |

2016 March 1 |

100 |

10 |

1000 |

-- |

-- |

-- |

100 |

|

1000 |

March 2 | 200 | 10.20 | 2040 |

|

|

| 100 | 10 | 1000 |

|

|

|

|

|

|

| 200 | 10.20 | 2040 |

March 5 | -- | -- | -- | 100 | 10 | 1000 |

|

|

|

|

|

|

| 150 | 10.20 | 1530 | 50 | 10.20 | 510 |

March 7 | 200 | 10.50 | 2100 | -- | -- | -- | 50 | 10.20 | 510 |

|

|

|

|

|

|

| 200 | 10.50 | 2100 |

March 10 | 300 | 10.80 | 3240 | -- | -- | -- | 50 | 10.20 | 510 |

|

|

|

|

|

|

| 200 | 10.50 | 2100 |

|

|

|

|

|

|

| 300 | 10.80 | 3240 |

March 13 | -- | -- | -- | 50 | 10.20 | 510 |

|

|

|

|

|

|

| 150 | 10.50 | 1575 | 50 | 10.50 | 525 |

|

|

|

|

|

|

| 300 | 10.80 | 3240 |

March 18 | -- | -- | -- | 50 | 10.50 | 525 |

|

|

|

|

|

|

| 150 | 10.80 | 1620 | 150 | 10.80 | 1620 |

March 20 | 100 | 11 | 1100 | -- | -- | -- | 150 | 10.80 | 1620 |

|

|

|

|

|

|

| 100 | 11 | 1100 |

March 25 | -- | -- | -- | 150 | 10.80 | 1620 | 100 | 11 | 1100 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

b. Weighted Average Method

Stores Ledger

Date | Receipts | Issue | Balance | |||||

Qty. | Price Rs | Value Rs | Qty. | Price Rs | Value Rs | Qty. | Value Rs | |

2016 March 1 |

100 |

10 |

1000 |

-- |

-- |

-- |

100 |

1000 |

March 2 | 200 | 10.2 | 2040 | -- | -- | -- | 300 | 3040 |

March 5 | -- | -- | -- | 250 | 10.13 | 2533 | 50 | 507 |

March 7 | 200 | 10.5 | 2100 | -- | -- | -- | 250 | 2607 |

March 10 | 300 | 10.8 | 3240 | -- | -- | -- | 550 | 5847 |

March 13 | -- | -- | -- | 200 | 10.63 | 2126 | 350 | 3721 |

March 18 | -- | -- | -- | 200 | 10.63 | 2126 | 150 | 1595 |

March 20 | 100 | 11 | 1100 | -- | -- | -- | 250 | 2695 |

March 25 | -- | -- | -- | 150 | 10.78 | 1617 | 100 | 1078 |

Working Notes:

Calculation of price for Issue on March 5th

= 3040/300 = Rs 10.13

Calculation of price for Issue on March 13th

= 5847/550 = Rs 10.63

Calculation of price for Issue on March 18th

= 3721/350 = Rs 10.63

Calculation of price for Issue on March 25th

= 2695/250 = Rs 10.78

Q19) The stock of material held on 1-4-2015 was 400 units @ 50 per unit. The following receipts and issues were recorded. You are required to prepare the Stores Ledger Account, showing how the values of issues would be calculated under Base Stock Method, through FIFO base being 100 units. (8 marks)

2-4-2015 | Purchased 100 units @Rs. 55 per unit |

|

6-4-2015 | Issued 400 units |

|

10-4-2015 | Purchased 600 units @ Rs. 55 per unit |

|

13-4-2015 | Issued 400 units |

|

20-4-2015 | Purchased 500 units @ Rs. 65 per unit. |

|

25-4-2015 | Issued 600 units |

|

10-5-2015 | Purchased 800 units @ Rs. 70 per unit |

|

12-5-2015 | Issued 500 units |

|

13-5-2015 | Issued 200 units |

|

15-5-2015 | Purchased 500 units @ Rs. 75 per unit |

|

12-6-2015 | Issued 400 units |

|

15-6-2015 | Purchased 300 units @ Rs. 80 per unit |

|

A9)

Stores Ledger Account [under Base Stock through FIFO Method]

Date | Receipts | Issues | Balance | ||||||

Qty. | Price Rs | Value Rs | Qty. | Price Rs | Value Rs | Qty. | Price Rs | Value Rs | |

1-4-2015 | -- | -- | -- | -- | -- | -- | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 300 | 50 | 15,000 |

2-4-2015 | 100 | 55 | 5,500 | -- | -- | -- | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 300 | 50 | 15,000 |

|

|

|

|

|

|

| 100 | 55 | 5,500 |

6-4-2015 | -- | -- | -- | 300 | 50 | 15,000 |

|

|

|

|

|

|

| 100 | 55 | 5,500 | 100 | 50 | 5,000 |

10-4-2015 | 600 | 55 | 33,000 | -- | -- | -- | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 600 | 55 | 33,000 |

13-4-2015 | -- | -- | -- | 400 | 55 | 22,000 | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 200 | 55 | 11,000 |

20-4-2015 | 500 | 65 | 32,500 | -- | -- | -- | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 200 | 55 | 11,000 |

|

|

|

|

|

|

| 500 | 65 | 32,500 |

25-4-2015 | -- | -- | -- | 200 | 55 | 11,000 | 100 | 50 | 5,000 |

|

|

|

| 400 | 65 | 26,000 | 100 | 65 | 6,500 |

10-5-2015 | 800 | 70 | 56,000 | -- | -- | -- | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 100 | 65 | 6,500 |

|

|

|

|

|

|

| 800 | 70 | 56,000 |

12-5-2015 | -- | -- | -- | 100 | 65 | 6,500 | 100 | 50 | 5,000 |

|

|

|

| 400 | 70 | 28,000 | 400 | 70 | 28,000 |

13-5-2012 | -- | -- | -- | 200 | 70 | 14,000 | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 200 | 70 | 14,000 |

15-5-2015 | 500 | 75 | 37,500 | -- | -- | -- | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 200 | 70 | 14,000 |

|

|

|

|

|

|

| 500 | 75 | 37,500 |

12-6-2015 | -- | -- | -- | 200 | 70 | 14,000 | 100 | 50 | 5,000 |

|

|

|

| 200 | 75 | 15,000 | 300 | 75 | 22,500 |

15-6-2015 | 300 | 80 | 24,000 | -- | -- | -- | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 300 | 75 | 22,500 |

|

|

|

|

|

|

| 300 | 80 | 24,000 |

Q20) Adnan Naeem Imports, Ltd has the following information about the inventory of electronic components for October 2016. (8 marks)

Date | Quantity | Cost per item (Rs) |

Opening Inventory | 150 | 32 |

5 October Purchase | 200 | 32 |

17 October Purchase | 450 | 31 |

28 October Purchase | 100 | 33 |

As at the end of October, 220 components remained in inventory.

Required:

- If the company uses FIFO method of allocating inventory, what would is the cost of goods sold for October?

- If the company uses FIFO method of allocating inventory costs, what would be the ending inventory?

- If the company uses average cost method of allocating inventory costs, what would is the ending inventory for October?

A10)

- Cost of Goods Sold

Units | @ | Amount |

150 | 32 | 4,800 |

200 | 32 | 6,400 |

330 | 31 | 10,230 |

680 |

| Rs. 21,430 |

b. Cost of Closing Inventory

Units | @ | Amount |

120 | 31 | 3,720 |

100 | 33 | 3,300 |

220 |

| 7,020 |

c. Cost of Closing Inventory

Units | @ | Amount |

220 | 31.61 | 6954.20 |

Average rate = 28450/900 = Rs 31.61 per unit

Q21) The stock of material held on 1-4-2015 was 400 units @ 50 per unit. The following receipts and issues were recorded. You are required to prepare the Stores Ledger Account, showing how the values of issues would be calculated under Base Stock Method, through FIFO base being 100 units.

2-4-2015 | Purchased 100 units @Rs. 55 per unit |

|

6-4-2015 | Issued 400 units @ Rs. 65 |

|

10-4-2015 | Purchased 600 units @ Rs. 55 per unit |

|

13-4-2015 | Issued 400 units @ Rs. 67 |

|

20-4-2015 | Purchased 500 units @ Rs. 65 per unit. |

|

25-4-2015 | Issued 600 units @ Rs. 73 |

|

10-5-2015 | Purchased 800 units @ Rs. 70 per unit |

|

12-5-2015 | Issued 500 units @ Rs. 70 |

|

13-5-2015 | Issued 200 units @ Rs. 75 |

|

15-5-2015 | Purchased 500 units @ Rs. 75 per unit |

|

12-6-2015 | Issued 400 units @ Rs. 80 |

|

15-6-2015 | Purchased 300 units @ Rs. 80 per unit |

|

Also calculate the Cost of Goods Sold and the Gross Profit. ( 8 marks)

A11) Stores Ledger Account [under Base Stock through FIFO Method]

Date | Receipts | Issues | Balance | ||||||

Qty. | Price Rs | Value Rs | Qty. | Price Rs | Value Rs | Qty. | Price Rs | Value Rs | |

1-4-2015 | -- | -- | -- | -- | -- | -- | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 300 | 50 | 15,000 |

2-4-2015 | 100 | 55 | 5,500 | -- | -- | -- | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 300 | 50 | 15,000 |

|

|

|

|

|

|

| 100 | 55 | 5,500 |

6-4-2015 | -- | -- | -- | 300 | 50 | 15,000 |

|

|

|

|

|

|

| 100 | 55 | 5,500 | 100 | 50 | 5,000 |

10-4-2015 | 600 | 55 | 33,000 | -- | -- | -- | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 600 | 55 | 33,000 |

13-4-2015 | -- | -- | -- | 400 | 55 | 22,000 | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 200 | 55 | 11,000 |

20-4-2015 | 500 | 65 | 32,500 | -- | -- | -- | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 200 | 55 | 11,000 |

|

|

|

|

|

|

| 500 | 65 | 32,500 |

25-4-2015 | -- | -- | -- | 200 | 55 | 11,000 | 100 | 50 | 5,000 |

|

|

|

| 400 | 65 | 26,000 | 100 | 65 | 6,500 |

10-5-2015 | 800 | 70 | 56,000 | -- | -- | -- | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 100 | 65 | 6,500 |

|

|

|

|

|

|

| 800 | 70 | 56,000 |

12-5-2015 | -- | -- | -- | 100 | 65 | 6,500 | 100 | 50 | 5,000 |

|

|

|

| 400 | 70 | 28,000 | 400 | 70 | 28,000 |

13-5-2012 | -- | -- | -- | 200 | 70 | 14,000 | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 200 | 70 | 14,000 |

15-5-2015 | 500 | 75 | 37,500 | -- | -- | -- | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 200 | 70 | 14,000 |

|

|

|

|

|

|

| 500 | 75 | 37,500 |

12-6-2015 | -- | -- | -- | 200 | 70 | 14,000 | 100 | 50 | 5,000 |

|

|

|

| 200 | 75 | 15,000 | 300 | 75 | 22,500 |

15-6-2015 | 300 | 80 | 24,000 | -- | -- | -- | 100 | 50 | 5,000 |

|

|

|

|

|

|

| 300 | 75 | 22,500 |

| 2,800 |

| 1,88,500 |

|

|

| 300 | 80 | 24,000 |

Calculation of Cost of Goods Sold

COGS = Opening Inventory + Purchases – Closing Inventory

= 5,000 + 1,88,500 – 24,000

= Rs. 1,69,500

Calculation of Gross Profit

Particulars | Amount (Rs) |

Sales: Qty x Selling price |

|

6-4: 400 x 65 | 26,000 |

13-4: 400 x 67 | 26,800 |

25-4: 600 x 73 | 43,800 |

12-5: 500 x 70 | 35,000 |

13-5: 200 x 75 | 15,000 |

12-6: 400 x 80 | 32,000 |

Total Sales | 1,78,600 |

Less: COGS | 1,69,500 |

Gross Profit | 9,100 |

Q22) Use the following information of Fatima Malik and Co.

A company just starting business made the following four inventory purchases in June 2016:

June 1 150 units Rs. 6.60/unit cost Rs. 990

June 10 200 units Rs. 6.30/unit cost 1,260

June 15 200 units Rs. 5.85/unit cost 1,170

June 28 150 units Rs. 5.20/unit cost 780

Rs. 4,200

A physical count of merchandise inventory on June 30 reveals that there are 250 units on hand.

Requirement (a): Using the periodic LIFO inventory method, the value of the ending inventory on June 30 is? (5 marks)

A12)

Cost Ending Inventory

Units | @ | Amount |

100 | 6.30 | 630 |

150 | 6.60 | 990 |

250 |

| Rs 1,620 |

Requirement (b): Using the periodic FIFO inventory method, the amount allocated to cost of goods sold for June is?

Units | @ | Amount |

150 | 6.60 | 990 |

200 | 6.30 | 1,260 |

100 | 5.85 | 585 |

450 |

| 2,835 |