IF

UNIT – 4Foreign Exchange Risk, Appraisal & Tax Management Q1) What is Foreign Exchange Risk management? Which risks are associated with foreign exchange market?A1) Foreign exchange risk is the most common form of market price risk managed by treasurers – the other common ones being interest rate and commodity risk. Market price risk is one of several groups of risks that businesses must manage within their ERM (Enterprise Risk Management) framework. Like all risks, Foreign Exchange (FX) risk is managed using the standard risk management process, which looks something like this for FX:

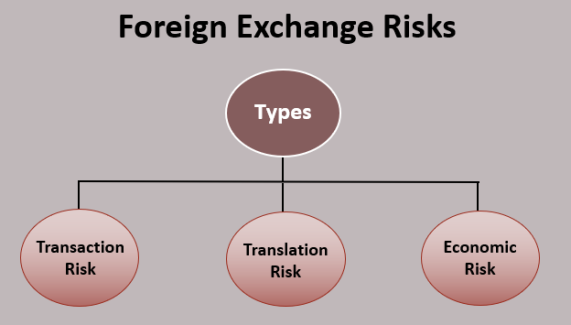

Types of Foreign Exchange RiskThe three types of foreign exchange risk include:

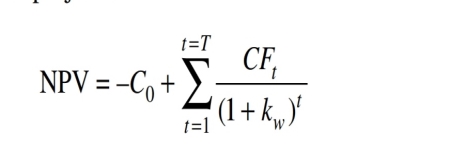

a) Transaction riskTransaction risk is the risk faced by a company when making financial transactions between jurisdictions. The risk is the change in the exchange rate before transaction settlement. Essentially, the time delay between transaction and settlement is the source of transaction risk. Transaction risk can be resolved by using forwards and options.For example, a Indian company with operations in China is looking to transfer CNY600 in earnings to its Indian account. If the exchange rate at the time of the transaction was 1 Rs for 6 CNY, and the rate subsequently falls to 1 Rs for 7 CNY before settlement, an expected receipt of Rs100 (CNY600/6) would instead of Rs86 (CNY600/7). b) Economic riskEconomic risk, also known as forecast risk, is the risk that a company’s market value is impacted by unavoidable exposure to exchange rate fluctuations. Such a type of risk is usually created by macroeconomic conditions such as geopolitical instability and/or government regulations.For example, Indian Company that sells locally face economic risk from automobile importers, especially if the Indian currency unexpectedly strengthens. c) Translation riskTranslation risk, also known as translation exposure, refers to the risk faced by a company headquartered domestically but conducting business in a foreign jurisdiction, and of which the company’s financial performance is denoted in its domestic currency. Translation risk is higher when a company holds a greater portion of its assets, liabilities, or equities in a foreign currency.For example, a parent company that reports in USA dollars but oversees a subsidiary based in China faces translation risk, as the subsidiary’s financial performance – which is in Chinese yuan – is translated into USA dollar for reporting purposes. Q2) What is the foreign portfolio management? Which institution invests in the foreign portfolios?A2) A foreign portfolio investment is a grouping of assets such as stocks, bonds, and cash equivalents. Portfolio investments are held directly by an investor or managed by financial professionals. In economics, foreign portfolio investment is the entry of funds into a country where foreigners deposit money in a country's bank or make purchases in the country's stock and bond markets, sometimes for speculation.An investment portfolio held by a bank or an individual contains various investments that typically include stocks (equity), bonds, loans, financial derivatives (options, futures, etc.), investible commodities such as gold or platinum, real estate, or similar assets of value. The investor is the entity that holds the portfolio and may be a company, a bank, or an individual. Portfolio management involves determining the contents and the structure of the portfolio, monitoring its performance, making any changes, and deciding which assets to acquire and which assets to divest. Portfolio managers weigh both the expected risk and return characteristics of individual assets, the performance of the entire portfolio, and the investor’s financial objectives in order to find an optimal combination of investments that provides the highest level of return for any given level of risk. Banks use several approaches to measure portfolio performance and reduce credit losses. The approaches utilize quantitative assessment tools to predict the likelihood of a default and estimate the impact of the default. A financial asset is simply a legal claim to a future cash flow. The basic principleunderlying the price of any financial asset is that its price should be determined by the present value of its expected cash flow, by which we mean the expected stream of cash receipts over the life of the asset. Note that we are referring to the expected cash flow, and this may be known with a high degree of certainty both with regard to the timing of payments and their size, or may be highly uncertain, or somewhere between these extremes.There are a number of factors that will influence the degree of certaintywith which the cash flow is expected. One is the nature of the financial asset.In the case of debt security the cash flow is usually more certain with regard to both the timing and amount compared to an equity security (that is, shares). With shares both the timing and size of dividend cash flows will be very much affected by the future performance of the company. Another important factor that will influence the degree of certainty of cash flows is the nature of the issuer of the financial asset; Treasury bonds issued by governments are usually regarded as risk-free in that a government is highly unlikely to renege on its commitments, since it can simply print the money to redeem the bond if need be. The same cannot be said of corporate bonds; a corporation may face financial difficulties that force it to renege on or reschedule part or all of its commitments. Another important factor is that today many governments and corporationsissue financial assets that are denominated in foreign currencies. In thiscase a domestic investor might know what the return is likely to be in the foreign currency, but the unpredictability of exchange rate movements will mean that the value of the payments when converted into the domestic currency is uncertain. The investor thus faces exchange-rate risk. Q3) Explain the concept of tax neutrality and tax equity.A3) Tax neutrality has its foundations in the principles of economic efficiency and equity. Tax neutrality is determined by three criteria-i) Capital-export neutrality is the criterion that an ideal tax should be effective in raising revenue for the government and not have any negative effects on the economic decision-making process of the taxpayer. That is, a good tax is one that is efficient in raising tax revenue for the government and does not prevent economic resources from being allocated to their most appropriate use no matter where in the world the highest rate of return can be earned. Obviously, capital-export neutrality is based on worldwide economic efficiency. ii) A second neutrality criterion is national neutrality . That is, taxable income is taxed in the same manner by the taxpayer’s national tax authority regardless of where in the world it is earned. In theory, national tax neutrality is a commendable objective, as it is based on the principle of equality. In practice, it is a difficult concept to apply. In the United States, for example, foreign-source income is taxed at the same rate as U.S.-earned income and a foreign tax credit is given against taxes paid to a foreign government. However, the foreign tax credit is limited to the amount of tax that would be due on that income if it were earned in the United States. Thus, if the tax rate paid on foreign-source income is greater than the U.S. tax rate, part of the credit may go unused. Obviously, if the U.S. tax authority did not limit the foreign tax credit to the equivalent amount of U.S. tax, U.S. taxpayers would end up subsidizing part of the tax liabilities of U.S. MNCs’ foreign earned income. iii) The third neutrality criterion is capital-import neutrality . To illustrate, this criterion implies that the tax burden a host country imposes on the foreign subsidiary of a MNC should be the same regardless of the country in which the MNC is incorporated and the same as that placed on domestic firms. Implementing capital import neutrality means that if the U.S. tax rate were greater than the tax rate of a foreign country in which a U.S. MNC earned foreign income, additional tax on that income above the amount paid to the foreign tax authority would not be due in the United States. The concept of capital-import neutrality, like national neutrality, is based on the principle of equality, and its implementation provides a level competitive playing field for all participants in a single marketplace, at least with respect to taxation. Nevertheless, implementing capital-import neutrality means that a sovereign government follows the taxation policies of foreign tax authorities on the foreign source income of its resident MNCs and that domestic taxpayers end up paying a larger portion of the total tax burden. Obviously, the three criteria of tax neutrality are not always consistent with one another. The underlying principle of tax equity is that all similarly situated taxpayers should participate in the cost of operating the government according to the same rules. Operationally, this means that regardless of the country in which an affiliate of a MNC earns taxable income, the same tax rate and tax due date apply. A dollar earned by a foreign affiliate is taxed under the same rules as a dollar earned by a domestic affiliate of the MNC. The principle of tax equity is difficult to apply; as we will see in a later section, the organizational form of a MNC can affect the timing of a tax liability. Q4) How International Business benefits its participants?A4) a) Increased revenuesOne of the top advantages of international trade is that one may be able to increase the number of potential clients. Each country that have been added can open up a new pathway to business growth and increased revenues.b). Decreased competitionThe product and services may have to compete in a crowded market domestically but it may find better access and less competition in other countries. c) Longer product lifespanSales can dip for certain products domestically, as domestic consumers stop buying them or move to upgraded versions over time. d) Easier cash-flow managementGetting paid upfront may be one of the hidden advantages of international trade. When trading internationally, it may be a general practice to ask for payment upfront, whereas at home we may have to be more creative in managing cash flow while waiting to be paid. Expanding business overseas could help businesspersons to manage cash flow better.e) Better risk managementOne of the significant advantages of doing business internationally is market diversification. Focusing only on the domestic market may expose to increased risk from downturns in the economy, political factors, environmental events and other risk factors. Becoming less dependent on a single market may help businesspersons to mitigate potential risks in their core market.f) Benefiting from currency exchangeThose who add international trade to their portfolio may also benefit from currency fluctuations. For example, when the U.S. dollar is down, you may be able to export more as foreign customers benefit from the favorable currency exchange rate.g) Access to export financingAnother one of the advantages of international trade is that one may be able to leverage export financing. The Export-Import Bank s (EXIM) of respective countries and may be places to explore for export financing options. Q5) What is Tax heaven? List six top tax heavens around the world.A5) A tax haven is a country or place with very low "effective" rates of taxation for foreign investors. In some traditional definitions, a tax haven also offers financial secrecy. However, while countries with high levels of secrecy but also high rates of taxation (e.g. the United States and Germany in the Financial Secrecy Index can feature in some tax haven lists, they are not universally considered as tax havens. In contrast, countries with lower levels of secrecy but also low "effective" rates of taxation (e.g. Ireland in the FSI rankings), appear in most § Tax haven lists. Three main types of tax haven lists have been produced to date: Governmental, Qualitative: these lists are qualitative and political; they never list members (or each other), and are largely disregarded by academic research; the OECD had one country on its 2017 list, Trinidad & Tobago; the EU had 17 countries on its 2017 list, none of which were OECD or EU countries, or § Top 10 tax havens. Non–governmental, Qualitative: these follow a subjective scoring system based on various attributes (e.g. type of tax structures available in the haven); the best known are Oxfam's Corporate Tax Havens list, and the Financial Secrecy Index (although the FSI is a list of "financial secrecy jurisdictions", and not specifically tax havens). Non–governmental, Quantitative: by following an objective quantitative approach, they can rank the relative scale of individual havens. Top Tax Havens in the WorldBermuda – Declared the world’s worst (or best if you’re looking to avoid taxation) corporate tax haven in 2016 by Oxfam with a zero percent tax rate and no personal income tax. Netherlands – Most popular tax haven among the world’s Fortune 500. The government uses tax incentives to attract businesses to invest in their country. One such tax incentive cost an estimated 1.2 billion euros in 2016 to the Netherlands. Luxembourg – It gives benefits such as tax incentives and zero percent withholding taxes. Cayman Islands – No personal income taxes, no capital gains taxes, no payroll taxes, no corporate taxes, and the country does not withhold taxes on foreign entities. Singapore – Charges reasonable nominal corporate taxes. Reasonable corporate tax rates are provided through tax incentives, lack of withholding taxes, and what appears to be substantial profit shifting. The Channel Islands – No capital gains taxes, no council taxes, and no value-added taxes. Isle of Man – No capital gains tax, turnover tax, or capital transfer tax. It also imposes a low income tax, with the highest rates at 20%. Mauritius – Low corporate tax rate and no withholding tax. Switzerland – Full or partial tax exemptions, depending on the bank used. Ireland – Referred to as a tax haven despite officials asserting that it is not. Apple discovered that two of the company’s Irish subsidiaries were not classified as tax residents in the United States or Ireland, despite being incorporated in the latter country. Q6) What is International Project appraisal? What are the techniques used for project appraisal?A6) Project appraisal is concerned the motive to answer the questions : whether or not to put the money in the project? At a very basic level it means comparing return on investment with the cost of the funds i.e the business or project will fruitful or not if someone put efforts on it. Only if the return is higher than the cost of funds, it would make sense to put the money in a project. This presumes, of course, that the purpose and rationale for undertaking a project is to generate a surplus. A literature survey on the motivation factors for undertaking FDI may highlight diverse strategic. behavioural and economic factors viz. follow the leader, bandwagon effect., market seekers, follow the customers, raw material seekers. efficiency seekers. cutting cost, that is. taking advantage of lower labour or input cost in other countries. pre-emption of competition, international diversification.There are generally two techniques of project appraisal.NonDCF and DCF are the two broad groups. DCF means Discounted Cash Flow. The main difference between non-DCF and DCF techniques is that while non-DCF techniques use undiscounted or unadjusted for time value of money cash flow data, the DCF techniques use discounted or adjusted for time value of money cash flows.. The time value of money is a very critical concept in project appraisal. Time value of money means a rupee today 1s worth more than a rupee tomorrow. Or, you may say a rupee tomorrow is worth less than a rupee today. This is true as long as there is inflation in the economy. Inflation causes loss of purchasing power of currencies. Q7) Give a review of NPV approach in international project appraisal.A7) Consider the well-known Net Present Value (NPV) formula widely used in evaluating domestic investment projects

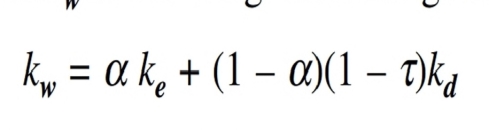

…………equation 1Here, C0 is the initial capital cost of the project incurred at t = 0 and CFt is the net cash flow from the project at the end of period t. Each cash flow CFt is discounted by the discount factor (1+ kw)t where kw is the weighted average cost of capital defined by

In this equation, ke is the cost of equity capital, kd is the pre-tax cost of debt, t is the corporate tax rate and a is the proportion of equity finance for the project.Keep in mind that the cash flows in the numerator of equation (1) must be incremental cash flows attibutable to the project. This means among other things that (1) Any change in the cash flows from some of the existing activities of the firm which arise on account of the project must be attributed to the project (2) Only net increase in overheads which would be on account of thisproject should be charged to the project.The virtue of the simple formula (2) is that it captures in a single parameter, viz. kw all the financing considerations allowing the project evaluator to focus on cash flows associated with the project. The problem is, there are two implicit assumptions. One is that the project being appraised has the same business risk as the portfolio of the firm’s current activities and the other is that the debt : equity proportion in financing the project is same as the firm’s existing debt : equity ratio. If either assumption is not true, the firm’s cost of equity capital, ke changes and the above convenient formula gives no clue as to how it changes. Thus, even in a purely domestic context, the standard NPV approach has limitations.The Adjusted Present Value (APV) approach seeks to disentangle the effects of particular financing arrangements of the project from the NPV of the project viewed as an all-equity financed investment. Q8) How does the foreign project is different from domestic project? Why investors consider intra- corporate financing ?A8) There are some challenges which differentiates a foreign project from a domestic project; They are-Exchange Risk and Capital Market Segmentation Cash flows from a foreign project are in a foreign currency and therefore subject to exchange risk from the parent’s point of view. How to incorporate this risk in project evaluation? And also what is the appropriate cost of capital when the host and home country capital markets are not integrated? Are the main areas of concern. Political or “Country” Risk Assets located abroad are subject to risks of appropriation or nationalisation (without adequate compensation) by the host country government. Also, there maybe changes in applicable withholding taxes, restrictions on remmittances by the subsidiary to the parent, etc. How should we incorporate these risks in evaluating the project? International Taxation In addition to the taxes the subsidiary pays to the host government, there will generally be withholding taxes on dividends and other income remitted to the parent. In addition, the home country government may tax this income in the hands of the parent. If double taxation avoidance treaty is in place, the parent may obtain some credit for the taxes paid abroad. The specific provisions of the tax code in the host and home countries will affect the kinds of financial arrangements between the parent and the subsidiary. There is also the related issue of transfer pricing which may enable the parent to further reduce the overall tax burden. Blocked Funds Sometimes, a foreign project can become an attractive proposal because the parent has some funds accumulated in a foreign country which cannot be taken out (or can be taken out only with heavy penalties in the form of taxes). Investing these funds locally in a subsidiary or a joint venture may then represent a better use of such blocked funds. In addition, like in domestic projects, we must be careful to take account of any interactions between the new project and some existing activities of the firm, e.g. local production will usually mean loss of export sales.Firstly ,their effects can be estimated more precisely than those of external financing; Secondly , the nature of internal financing arrangements is sensitive to the particular features of the tax law in the host and home countries; Thirdly , it always forces us to keep in mind that any change in the nature ofintra-corporate financial relationships impinges only on the allocation of profits between the parent and the subsidiary and not a net gain or loss. Q9) What is tax liability? What are its types?A9) Tax liability is the amount of money that a person owe to tax authorities or government of the nation. When one person have a tax liability, he has a legally binding debt to creditor. Both individuals and businesses can have tax liabilities.The government uses tax payments to fund social programs and administrative roles. For example, funding in various govt prescribed programmes, constructing/investing in public goods.Here are some tax liabilities which are generally incurred by small business enterprisesa) Income tax liabilityWorking individuals are generally required to pay income tax, and possibly state and local income taxes, on their earnings. This is generally based upon the principle of Ability to pay .Employers withhold income tax liabilities from employee wages. But in case of a small business owner, there won’t any payment of wages (unless one is incorporated). And when one don’t receive wages, do not have income taxes withheld from his earnings.b) Business tax liabilityThe business holder/player is required to pay taxes on its profits. However, if the structure of business as a sole proprietorship, partnership, S corporation, or LLC (not taxed as a corporation), then one can enjoy pass-through taxation. Pass-through taxation means the business taxes pass through your business and on the person, which is why you include the business income tax liability as income on his personal income tax return.c) Self-employment tax liabilityWorking individuals must pay Social Security and Medicare taxes on their earnings. For employees, these taxes are withheld from their wages in the form of FICA tax, which is an employer and employee tax. Self-employed individuals pay these taxes in the form of self-employment tax.As a small business owner, one has a self-employment tax liability unless his business is incorporated. Self-employment tax essentially covers both the employer and employee portions of Social Security and Medicare taxes.An individual’s self-employment tax liability is (approx)15.3% of you’re his earnings. d) Payroll tax liabilityIf one has employees, then he will be responsible for withholding, filing, and remitting payroll taxes. And also the individual must pay employer taxes. The money which is withhold from employees, as well as the money spend as the employer, make up his payroll tax liability.Together, income, unemployment, and FICA taxes make up the payroll tax liability. One must deposit these taxes with the IRS according to his depositing schedule.e) Sales tax liabilitysales tax occurs when someone sales some goods or services. After collecting the sales tax from the customers; constitutes a sales tax liability. One must remit the sales tax to the state or local government.Sales tax is a percentage of a customer’s total bill. The sales tax rate differs based on businesses physical presence.f) Capital gains tax liabilityWhen an individual or a firm sell an investment or another type of asset for a profit it incurred Capital gains tax. Capital gain taxes are taxes you pay on the gain. Your gain is the difference between what you purchased the asset for minus what you sold it for.g) Property tax liabilityProperty tax liability incurred when business holds its real estates(e.g., buildings, land, etc). Property tax is a tax that property owners pay to their local governments.Property tax rates vary on the basis of differences in property as tax liability is based on the value of the property. Generally, the government will reassess the tax rate per year. Multiply your tax rate by the market value of individual/firm’s property to calculate the property tax liability. Q10) Explain the concept of Arbitrage and Speculation with some examples.A10) Active management or speculation means a company has open interest rate gap or currency gap and tries to obtain higher returns in risky environment. It is possible to speculate on future direction or volatility of price movement. Active strategies rely on forecasts, valuation analysis, credit analysis, yield spread analysis, volatility analysis. Active management includes strategies that attempt to outperform a passive benchmark portfolio. These strategies use derivatives (especially options) as an instrument to increase returns. Arbitrage is defined as transaction of buying a security at a low price in one market and simultaneously selling in another market (or at the same market but in different time) at a higher price to make a profit. In efficient markets such opportunities cannot exist. For most of firms arbitrage opportunities do not exist. Arbitrage may be compared to money being left on the street .Arbitrage is a particular type of position taking in which offsetting positions are taken in closely related markets with the intention of generating low risk (but also generally low return) net positions. Classic example — FX arbitrage between quotations in two different centers. This type of pure informational arbitrage has been largely eliminated by the power of modern technology which gives rapid access to information. Second example — buy a basket of stocks which mimics an index and sell the future on the index. Depends on capital investment in computers and people to simultaneously purchase a large number of stocks. Might invest in a statistical model to determine a smaller, more manageable basket which closely tracks index, but this introduces some risk.

|

|

|

|

0 matching results found