Unit 1

Introduction Concepts of financial statements

Q1) Define financial statement. Also discuss its features. 5

A1) A financial statement is a collection of data organized according to logical and consistent accounting procedures. Its purpose is to convey an understanding of some financial aspects of a business firm. It may show a position at a moment in time, as in the case of a balance sheet, or may reveal a series of activities over a given period of time, as in the case of an income statement. The term ‘financial statements’ generally refer to the two statements-

i) The position statement or the balance sheet; and

(ii) The income statement or the profit and loss account.

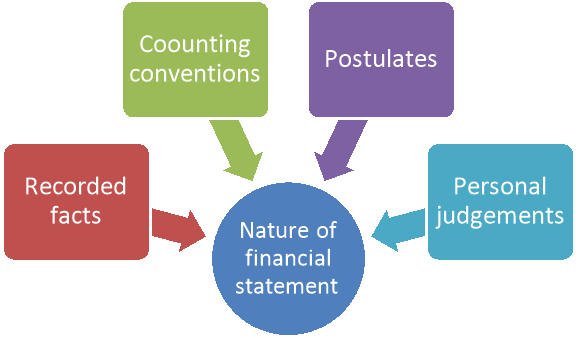

Nature of financial statement

The nature of financial statement is discussed below-

Figure: Nature of financial statement

1. Recorded Facts:

The term ‘recorded facts’ refers to the data taken out from the accounting records. The records are maintained on the basis of actual cost data. The original cost or historical cost is the basis of recording various transactions. The figures of various accounts such as cash in hand, cash in bank, bills receivables, sundry debtors, fixed assets etc. are taken as per the figures recorded in the accounting books. The assets purchased at different times and at different prices are put together and shown at cost prices. As recorded facts are not based on replacement costs, the financial statements do not show current financial condition of the concern.

2. Accounting Conventions:

Certain accounting conventions are followed while preparing financial statements. The convention of valuing inventory at cost or market price, whichever is lower, is followed. The valuing of assets at cost less depreciation principle for balance sheet purposes is followed. The convention of materiality is followed in dealing with small items like pencils, pens, postage stamps, etc. These items are treated as expenditure in the year in which they are purchased even though they are assets in nature. The stationery is valued at cost and not on the principle of cost or market price whichever is less. The use of accounting conventions makes financial statements comparable, simple and realistic.

3. Postulates:

The accountant makes certain assumptions while making accounting records. One of these assumptions is that the enterprise is treated as a going concern. The other alternative to this postulate is that the concern is to be liquidated, this, is untenable if management shows an intention to liquidate the concern. So the assets are shown on a going concern basis. Another important assumption is to presume that the value of money will remain the same in different periods. Though there is a drastic change in purchasing power of money the assets purchased at different times will be shown at the amount paid for them. While preparing profit and loss account, the revenue is treated in the year in which the sale was undertaken even though the sale price may be received in a number of years. The assumption is known as realization postulate.

4. Personal Judgments:

Even though certain standard accounting conventions are followed in preparing financial statements but still personal judgment of the accountant plays an important part. For example, in applying the cost or market value whichever is less to inventory valuation the accountant will have to use his judgment in computing the cost in a particular case. There are a number of methods for valuing stock, viz.; last in first out, first in first out, average cost method, standard cost, base stock method, etc. The accountant will use one of these methods for valuing materials. The selection of depreciation method, to use one of the several methods for estimating uncollectible debts, to determine the period for writing off intangible assets are some of the examples where judgment of the accountant will play an important role in choosing the most appropriate course of action.

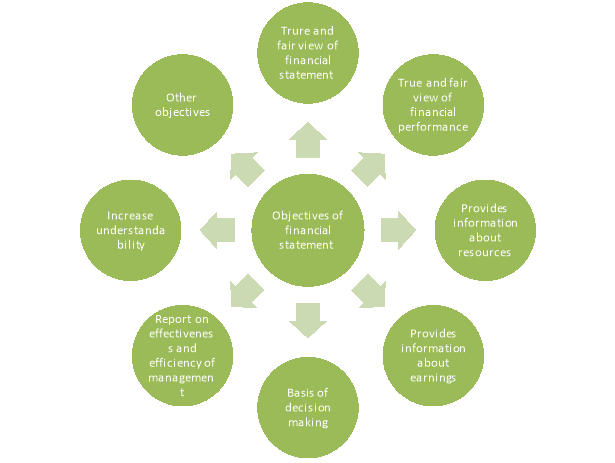

Q2) Explain the objectives of financial statement. 12

A 2) Financial statements are important documents of a company as it provides essential information to the stakeholders. The Accounting Principles Board of America (APB) states the following objectives of financial statements:

(i) To provide reliable financial information about economic resources and obligations of a business firm.

(ii) To provide other needed information about changes in such economic resources and obligations.

(iii) To provide reliable information about changes in net resources (resources less obligations) arising out of business activities.

(iv)To provide financial information that assists in estimating the earning potentials of business.

Some of the general objectives of financial statement are-

Figure: Objectives of financial statement

1. True & Fair view of financial position

- Balance sheet shows the financial position of the business i.e. it enlists the assets and liabilities. The difference between those represents the net worth (i.e. book value of the business). Net worth includes the capital infused by the owners plus the profits earned till date.

- Decreasing in the net worth is bad indicator of growth. This gives the management various hints to improvise the financial position.

- Financial position is presented for current year and previous year. The increase is assets represents growth of the earning capacity and decrease in liabilities represents the repaying capacity of the entity.

- Thus, the utmost objective of true and fairness is very essential here.

2. True & fair view of financial performance

- Income statement shows the financial performance of the entity i.e. its revenue and its expenses. The difference between those represents the profit or loss earned during the period.

- Decrease in revenue has direct impact in decrease in profits. Increase in expense have reverse impact of decrease in profits.

- If the accounting standards are not followed appropriately, it shows that management can play with revenue & expenses figures.

- Thus, the true and fairness is essential objective in preparing the income statement.

3. To provide information about resources

- Another objective behind financial statements is to provide information about the resources available with business (i.e. production capacity, labour hours, cash reserves, inventory, WIP percentage, delivery mechanism, etc.) and its usage parameters. It also gives information about changes in the resources between two periods.

- This information helps in better understanding of the business as changes in the utilisation and acquisition of the resources helps the stakeholders to take financial decisions.

4. To provide Information about the earning potential

- Financial statements should also hint about earning potential of the business. This information is for the top management level of the organisation.

- With the economic assets and liabilities, the management can decide on the expansion levels.

- The three components of financial statements in together should provide information about the earning capacity of the entity.

- Earning potential is also linked with the utilisation of available resources.

5. To form basis for decisions of the stakeholders

- Stakeholders means the owners, directors, customers, suppliers, employees, workman, government, finance providers and the public at large.

- Employees needs to take decision whether to stay employed or not. Customer needs to take decision whether to give more orders. Suppliers needs to think about whether to supply or not. Finance providers also have to take decision whether it is feasible to give loans to the entity. Public at large needs to think whether to invest in the entity. Directors have to decide on the dividend pay-outs, raising finance, employing more staff, acquisition of resources and many other things to keep the business running.

- All such decisions are based primarily on the financial statements.

6. To report on the effectiveness and efficiency of the management

- Owners have no time to attend the daily operations of the business and thus, they appoint the management to look forward for the entity. The strong financials are the picture of the effectiveness and efficiency with which the decisions are taken by the management.

- Effectiveness means whether the purpose is served or not. So, owners can think whether the decision made by them in appointing the management is appropriate or whether it needs any change. It also shows whether the internal policies are strong.

- Efficiency means whether the target is achieved in reasonable time. Owners can think upon their decision by observing the gross profit ratio and the net profit ratios of recent years.

7. To increase the understand ability of the end users.

- End users means the owners, for whom the financial statements are prepared. All the laws, regulations, accounting standards, accounting framework, etc. are here to ensure the understand ability of the end users.

- Financial statements are summaries of the operations during the year and therefore it is required to provide various disclosures to help the owners understand the statements in a better manner.

- If the end users can arrive at correct decision with the help of financial statements, this objective is achieved.

8. Other Objectives

- To help settle disputes arising between various parties.

- To provide information about the credibility of the entity in the finance world.

- To decide on whether it is right time to replace the assets of the firm with new assets having increased capacities

- To decide whether to invest in other entities so to expand the empire.

- To help government with information about payment of taxes, etc.

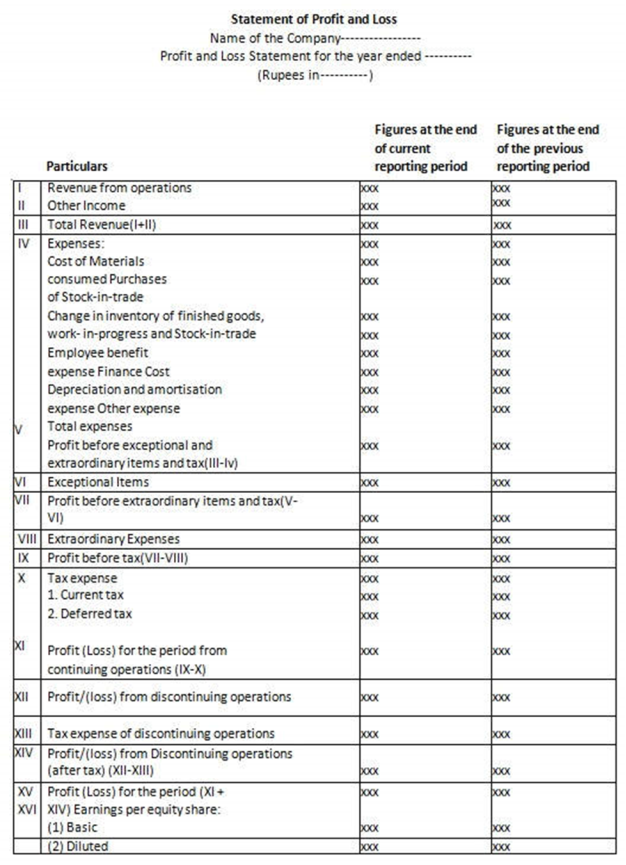

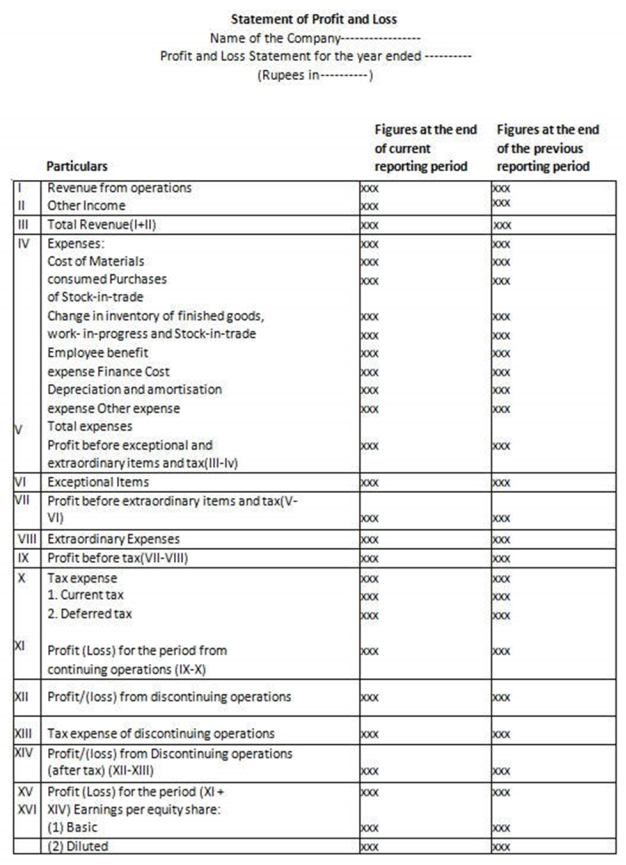

Q3) What is income statement? Also draw the specimen of income statement. 5

A3) Income statement is a financial statement of the company that shows profits/loss of the company for an accounting period. It is also known as profit and loss accounts which records sales, purchase and all direct and indirect expenses related to the respective accounting period. The specimen format of income statement is depicted below-

Q4) Write a brief note on income statement. 12

A4) Income statement is a financial statement of the company that shows profits/loss of the company for an accounting period. It is also known as profit and loss accounts which records sales, purchase and all direct and indirect expenses related to the respective accounting period. The specimen format of income statement is depicted below-

The items of statement of profit and loss are discussed as follows:

- Revenue from operations

This includes: (i) Sale of products

(ii) Sale of services

(iii) Other operating revenues.

In respect to a finance company, revenue from operational shall include revenue from interest, dividend and income from other financial services. It may be noted that under each of the above heads shall be disclosed separately by way of notes to accounts to the extent applicable.

2. Other income

(i) Interest income (in case of a company other than a finance company),

(ii) Dividend income,

(iii)Net gain/loss on sale of investments,

(i) Other non-operating income (net of expenses directly attributable to such income).

3.Expense :

Expenses incurred to earn the income shown under various heads as discussed below:

(a) Cost of Materials: It applies to manufacturing companies. It consists of raw materials and other materials consumed in manufacturing of goods.

(b) Purchase of Stock-in-trade: It means purchases of goods for the purpose of trading.

(c) Changes in inventories: It is the difference between opening inventory (stock) finished goods, WIP and of finished goods, WIP and stock-in-trade and closing stock-in-trade inventory.

(d) Employees benefit expenses: Expenses incurred on employees towards salary, wages, leave encashment, staff welfare, etc., are shown under this head. Employees benefit expenses may be further categorised into direct and indirect expenses.

(e) Finance cost: It is the expenses towards interest charges during the year on the borrowings. Only the interest cost is to be shown under this head. Other financial expenses such as bank charges are shown under “Other Expenses”.

(f) Depreciation: Depreciation is the diminution in the value of fixed assets whereas amortisation is writing off the amount relating to intangible assets.

(g) Other expenses: All other expenses which do not fall in the above categories are shown under other expenses. Other expenses may further be categorised into direct expenses, indirect expenses and non-operating expenses.

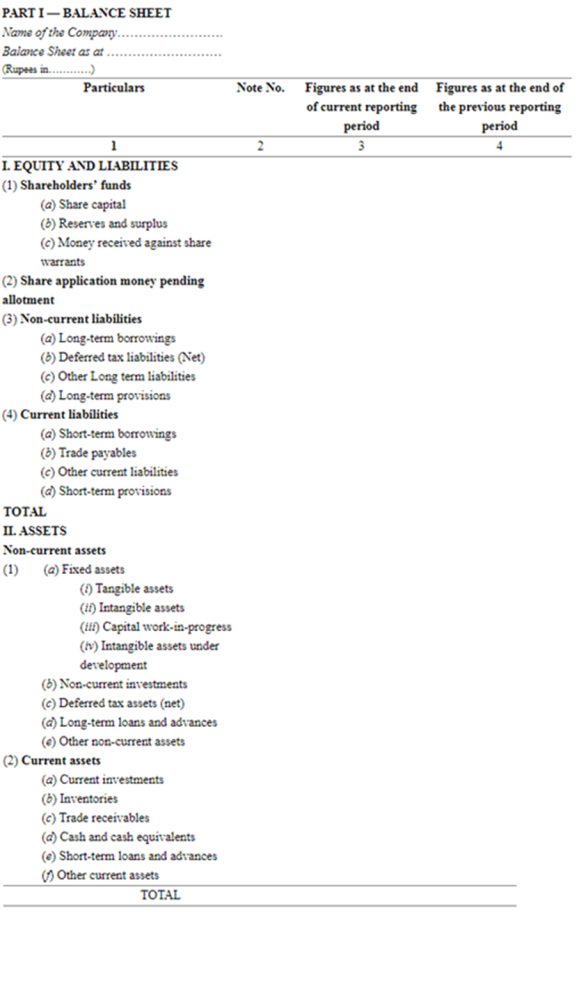

Q5) What is balance sheet? Also draw the specimen of Balance sheet. 5

A6) Balance sheet is a financial statement prepared at the end of the accounting period to know the financial position of the company. The balance provides information about the nature and quality of assets and liabilities of the company. Schedule III of the Companies Act, 2013 deal with the Balance sheet and profit and loss account. The specimen format of the balance sheet is depicted below-

Q6) Discuss about the liability items of a balance sheet. 8

A7) The items of liability side of balance sheet is discussed below-

- Share capital:

a. The number and amount of shares authorized.

b. The number of shares issued, subscribed and fully paid, and subscribed but not fully paid.

c. Par value per share.

d. A reconciliation of the number of shares outstanding at the beginning and at the end of the reporting period.

e. The rights, preferences and restrictions attaching to each class of shares including restrictions on the distribution of dividends and the repayment of capital.

f. Shares in respect of each class in the company held by its holding company or its ultimate holding company including shares held by or by subsidiaries or associates of the holding company or the ultimate holding company in aggregate.

g. Shares in the company held by each shareholder holding more than 5 per cent, shares specifying the number of shares held.

h. Shares reserved for issue under options and contracts/commitments for the sale of shares/disinvestment, including the terms and amounts.

i. For the period of five years immediately preceding the date as at which the Balance Sheet is prepared.

a) Aggregate number and class of shares allotted as fully paid-up pursuant to contract(s) without payment being received in cash.

b) Aggregate number and class of shares allotted as fully paid-up by way of bonus shares.

c) Aggregate number and class of shares bought back.

j. Terms of any securities convertible into equity/preference shares issued along with the earliest date of conversion in descending order starting from the farthest such date.

k. Calls unpaid (showing aggregate value of calls unpaid by directors and officers).

l. Forfeited shares (amount originally paid-up).

2. Reserves and Surplus

i) Capital Reserves;

Ii) Capital Redemption Reserve;

Iii) Securities Premium Reserve;

Iv)Debenture Redemption Reserve;

v) Revaluation Reserve;

Vi)Share Options Outstanding Account;

Vii) Other Reserves (specify the nature and purpose of each reserve and the amount in respect thereof);

Viii) Surplus i.e., balance in Statement of Profit and Loss disclosing allocations and appropriations such as dividend, bonus snares and transfer to/from reserves, etc.

3. Long-Term Borrowings

i) Bonds/debentures

Ii) Term loans:

(a) from banks.

(b) from other parties

Iii) Deferred payment liabilities;

Iv) Deposits;

v) Loans and advances from related parties;

Vi) Long term maturities of finance lease obligations;

Vii) Other loans and advances (specify nature)

- Other Long-term Liabilities

(i) Trade payables

(ii) Others.

- Long-term provisions

i) Provision for employee benefits

Ii) Others (specify nature).

- Short-term borrowings

i) Loans repayable on demand

(a) from banks

(b) from other parties

(c) Loans and advances from related parties

(d) Deposits

(e) Other loans and advances (specify nature).

7. Other current liabilities

i) Current maturities of long-term debt;

Ii) Current maturities of finance lease obligations;

Iii) Interest accrued but not due on borrowings;

Iv) Interest accrued and due on borrowings;

v) Income received in advance;

Vi) Unpaid dividends;

Vii) Application money received for allotment of securities and due for refund and interest accrued thereon. Share application money includes advances towards allotment of share capital. The terms and conditions including the number of shares proposed to be issued, the amount of premium, if any, and the period before which shares shall be allotted shall be disclosed. It shall also be disclosed whether the company has sufficient authorised capital to cover the share capital amount resulting from allotment of shares out of such share application money. Further, the period for which the share application money has been pending beyond the period for allotment as mentioned in the document inviting application for shares along with the reason for such share application money being pending shall be disclosed. Share application money not exceeding the issued capital and to the extent not refundable shall be shown under the head Equity and share application money to the extent refundable, i.e., the amount in excess of subscription or in case the requirements of minimum subscription are not met, shall be separately shown under “Other current liabilities”;

Viii) Unpaid matured deposits and interest accrued thereon;

Ix) Unpaid matured debentures and interest accrued thereon;

x) Other payables (specify nature).

8. Short-term provisions

i) Provision for employee benefits

Ii) Others (specify nature).

Q7) Explain about the assets appear in the balance sheet. 8

A8) Tangible assets

i) Land

Ii) Buildings;

Iii) Plant and Equipment;

Iv) Furniture and Fixtures;

v) Vehicles;

Vi) Office equipment;

Vii) Others (specify nature).

Intangible assets

i) Goodwill

Ii) Brands /trademarks;

Iii) Computer software;

Iv) Mastheads and publishing titles;

v) Mining rights;

Vi) Copyrights, and patents and other intellectual property rights, services and operating rights;

Vii) Recipes, formulae, models, designs and prototypes;

Vii) Licences and franchise;

Viii) Others (specify nature).

Non-current investments

i) Investment property;

Ii) Investments in Equity Instruments;

Iii) Investments in preference shares;

Iv) Investments in Government or trust securities;

v) Investments in debentures or bonds;

Vi) Investments in Mutual Funds;

Vii) Investments in partnership firms;

Viii) Other non-current investments (specify nature). Under each classification, details shall be given of names of the bodies corporate indicating separately whether such bodies are

(a) subsidiaries,

(b) associates,

(c) joint ventures, or

(d) controlled special purpose entities in whom investments have been made and the nature and extent of the investment so made in each such body corporate (showing separately investments which are partly-paid). In regard to investments in the capital of partnership firms, the names of the firms (with the names of all their partners, total capital and the shares of each partner) shall be given.

Long-term loans and advances

i) Capital Advances;

Ii) Security Deposits;

Iii) Loans and advances to related parties (giving details thereof);

Iv) Other loans and advances (specify nature).

Other non-current assets

i) Long-term Trade Receivables (including trade receivables on deferred credit terms);

Ii) Others (specify nature);

Iii) Long term Trade Receivables, shall be sub-classified as:

(a) Secured, considered good;(b) Unsecured, considered good;

(c) Doubtful

Current Investments

i) Investments in Equity Instruments;

Ii) Investment in Preference Shares;

Iii) Investments in Government or trust securities:

Iv) Investments in debentures or bonds;

v) Investments in Mutual Funds;

Vi) Investments in partnership firms;

Vii) Other investments (specify nature).

Inventories

i) Raw materials;

Ii) Work-in-progress;

Iii) Finished goods;

Iv) Stock-in-trade (in respect of goods acquired for trading);

v) Stores and spares;

Vi) Loose tools;

Vii) Others (specify nature)

Trade Receivables

Aggregate amount of Trade Receivables outstanding for a period exceeding six months from the date they are due for payment

i) Secured, considered good;

Ii) Unsecured, considered good;

Iii) Doubtful.

Cash and cash equivalents

i) Balances with banks;

Ii) Cheques, drafts on hand;

Iii) Cash on hand;

Iv) Others (specify nature)

Short-term loans and advances

i) Loans and advances to related parties (giving details thereof);

Ii) Others (specify nature).

Sub-categorised as a) Secured, considered good; b) Unsecured, considered good; c) Doubtful.

Other current assets (specify nature)

Which incorporates current assets that do not fit into any other asset categories

Contingent liabilities

i) Claims against the company not acknowledged as debt

Ii) Guarantees;

Iii) Other money for which the company is contingently liable.

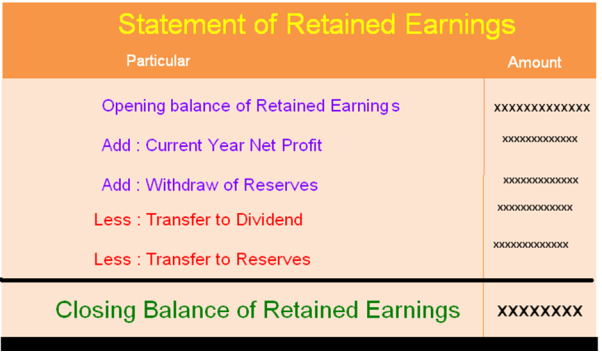

Q8) Define statement of retained earning with its specimen format. 5

A9) The statement of retained earnings, also known as the retained earnings statement, is a financial statement that shows the changes in a company’s retained earnings account for a period of time. This statement is used to reconcile the beginning and ending retained earnings for a specified period when it is adjusted with information such as net income and dividends. It is used by analysts to figure out how corporate profits are used by the company. It shares a lot of familiarities with the statement of changes in equity, but it only shows how retained earnings have changed during the period. The statement of retained earnings includes the following basic elements:

- Beginning balance of retained earnings

- Corrections for previous errors along with any tax effect

- Net income

- Dividends or withdrawals by the owner

This statement of retained earnings appears as a separate statement or it can also be included on the balance sheet or an income statement. The statement contains information regarding a company’s retained earnings, also including amounts distributed to shareholders through dividends and net income. An amount is set aside to handle certain obligations other than dividend payments to shareholders, as well as any amount directed to cover any losses. Each statement covers a specified period of time, usually a year, as noted in the statement.

It is calculated as-

Retained Earnings=Beginning Retained Earnings + New Net Income−Dividends

Q9) Define statement of retained earnings. Also discuss its importance for a company. 5

A10) The statement of retained earnings, also known as the retained earnings statement, is a financial statement that shows the changes in a company’s retained earnings account for a period of time. This statement is used to reconcile the beginning and ending retained earnings for a specified period when it is adjusted with information such as net income and dividends. It is used by analysts to figure out how corporate profits are used by the company. It shares a lot of familiarities with the statement of changes in equity, but it only shows how retained earnings have changed during the period. The statement of retained earnings includes the following basic elements:

- Beginning balance of retained earnings

- Corrections for previous errors along with any tax effect

- Net income

- Dividends or withdrawals by the owner

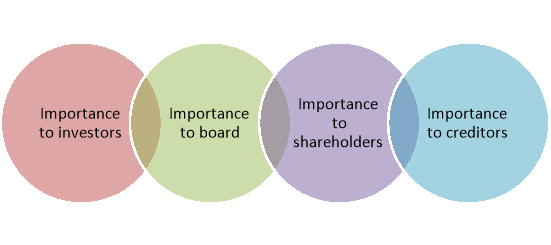

Importance of Retained Earnings Statement

The statement of retained earnings has great importance to investors, shareholders, and the Board of Directors.

Figure: Importance of retained earnings

- Importance to Investors

A company releases its statement of retained earnings to the public to raise market and shareholder confidence. Investors can judge the health of a company by evaluating this statement. The statement is of great importance to individuals within the organization as well. Outside investors can gauge the potential earnings of a company by analysing the statement of retained earnings.

2. Importance to Board

Essentially, a statement of retained earnings is crucial for a company’s growth, as it gives the Board of Directors confidence that the company is well worth the investment in both money and time. The Board of Directors are responsible to shareholders. Ultimately, they have to make the decision to keep the shareholders happy. Retained earnings tell the Board how much money the company has, and enables them to make an informed decision.

3. Importance to Shareholders

Using the retained earnings, shareholders can find out how much equity they hold in the company. Dividing the retained earnings by the no. Of outstanding shares can help a shareholder figure out how much a share is worth.

4. Importance to Creditors

Creditors view this statement as well, as they want to look at several performance measures before they can issue credit to a company. Low or negative retained earnings indicate that the company may have problems repaying its debt. This may result in the creditors choosing not to provide credit to these businesses or charge them a higher interest rate to compensate for the risk.

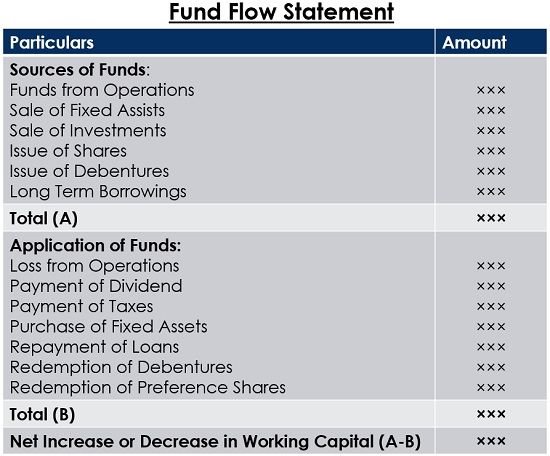

Q10) Write a note on fund flow statement. 8

A11) A fund flow statement is a statement prepared to analyse the reasons for changes in the financial position of a company between two balance sheets. It portrays the inflow and outflow of funds i.e. sources of funds and applications of funds for a particular period. The fund flow statement is a summary of the source of funds and the application of funds that compares the balance sheets of two different dates and analyse from where company has earned money and where the company has spent money. With the help of fund flow statement format, it becomes a condensed version to analyse the sources and application of fund.

Three Parts of Fund Flow Statement Format are-

Figure: Parts of financial statement

- Statement of Changes in Working Capital: Working capital means the difference between the current assets and current liabilities. If there is an increase in working capital, then it will be an application of funds, and if there is a decrease in working capital, then it will be a source of funds.

2. Funds from Operations: If we earn a profit, then it will be a source of funds, and if there is a loss, then it will be an application of funds.

3.Fund Flow Statement: After preparing the above two requirements, we will prepare the fund flow statement, which will comprise all outflow and inflow of funds.

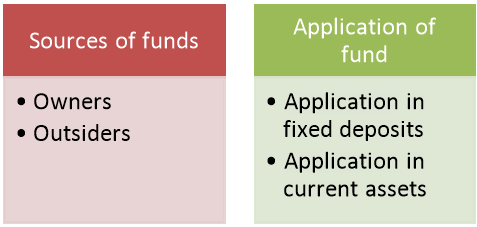

Components of a fund flow statement

A fund flow statement comprises of:

Figure: Components of financial statement

- Sources of funds: It talks about the extent of funds availed from

Owners

Outsiders.

- Application of funds: It talks about how the funds have been utilized

Funds deployed in Fixed assets

Funds deployed in Current assets

Figure: Specimen of fund flow statement

Q11) State the benefits and limitations of financial statement analysis. 8

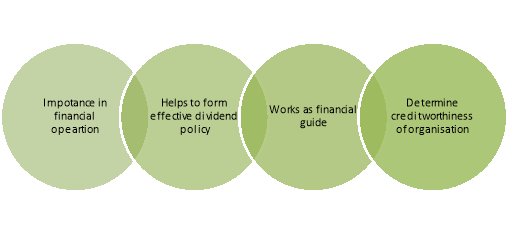

A12) Benefits of Funds Flow Statement

A statement of the business’s funds flow is an essential financial tool to monitor and regulate working capital. Below are some benefits of Funds Flow Statement that financial analysts and managers opt for.

Figure: Benefits of fund flow statement

- Analytical importance in financial operations

Even though financial statements show the resources and their utilisations, it doesn’t reveal the reasons for such changes in the Balance Sheet. The statement thus provides an analytical view of the differences between current assets and current liabilities. Hence, it also explains how these changes take place in the context of the funds of a concerned company. In some cases, even if the company runs on profit, scenarios of cash shortage may arise. In such circumstances, this statement provides a clear picture of the profit earned by an organization.

2. Helps to form effective dividend policy

Sometimes a firm possesses substantial available profit to be distributed as a dividend but finds it difficult to do so due to a lack of sufficient liquidity. A Funds Flow Statement thus helps identify liquidity blockage and assists in planning an effective dividend policy.

3. Works as a financial guide

This statement also serves as a financial guide for a company. It brings out the financial issues that a concerned company could face in the near future. The management can thus chalk out an appropriate strategy to protect the company from any significant future financial loss.

4. Helps to determine the creditworthiness of an organization

Institutions lending finances often opt to evaluate this statement for a series of years to assess the creditworthiness of an applicant company before approving a loan. Hence, it also portrays the credibility of a firm in terms of fund management.

Limitations of Funds Flow Statement

In spite of several essential utilities, financial analysts encounter some Funds Flow Statement problems indicating at the limitations to its use.

- This statement cannot portray financial parameters represented in a Balance Sheet or Income Statement. It only focuses on the movement of funds during a specific timeline and does not quantify other essential items.

- The statement doesn’t add any new numerical value to a company’s financial standing. It only re-arranges the available information to identify issues with fund management.

- Due to its historical nature, this statement can’t conclude with accuracy the present-day financial standing of a business.

- Working capital plays an essential role in business finance. However, the movement of cash is more important for a promising financial future of a business. Thus, the flow of funds does not serve as an effective barometer for the purpose.